Over the past decade, the U.S. has seen its lowest interest rates in history which has made REITs, with their naturally high yields and low volatility, attractive so-called "bond alternatives."

However, in reality, there are important differences between bonds and REITs that investors need to understand when deciding what asset allocation is right for them.

Let's take a look at what these differences are, the pros and cons of each kind of asset, and most importantly, what the right mix of bonds and REITs is reasonable for a retirement portfolio.

Most Important Differences Between Bonds and REITs

As you can see below, there are a number of major differences between bonds and REITs. The most important difference between bonds and REITs is that bonds are fixed-income investments issued by governments and companies that pay a set coupon (interest rate), usually once every six months.

These payments are typically fixed and thus the value of a bond (which trades daily on the bond market) is largely a function of time to maturity and prevailing interest rates (both long-term Treasury yields and rates on similar bonds being issued today). Bonds have a limited lifespan because they eventually mature.

The other important thing to know is that bonds have a higher priority in the capital stack, which is comprised of the total capital invested in a business (common equity, preferred equity, mezzanine debt, and senior debt).

In other words, bond investors get preferential treatment in terms of repayment in the event that the bond issuer experiences financial distress. That's why bonds have relatively lower risk.

In contrast, REITs (see our detailed guide to investing in REITs here) are a type of equity, meaning they represent partial ownership in a company that makes its money by owning commercial real estate properties and collecting on rents from tenants.

REITs are perpetual investments that have no maturity date and can theoretically continue to exist and grow their asset bases for decades. Unlike bonds, REITs tend to pay rising dividends over time as their cash flow grows, and thus tend to have offer better capital appreciation potential than bonds.

So now that we know the basic differences between these two assets, let's look at the advantages and disadvantages of owning both bonds and REITs.

Advantages and Disadvantages of Bonds

Due to their fixed interest payments and lower-risk profiles, bonds don't generate nearly the kinds of total returns that stocks do.

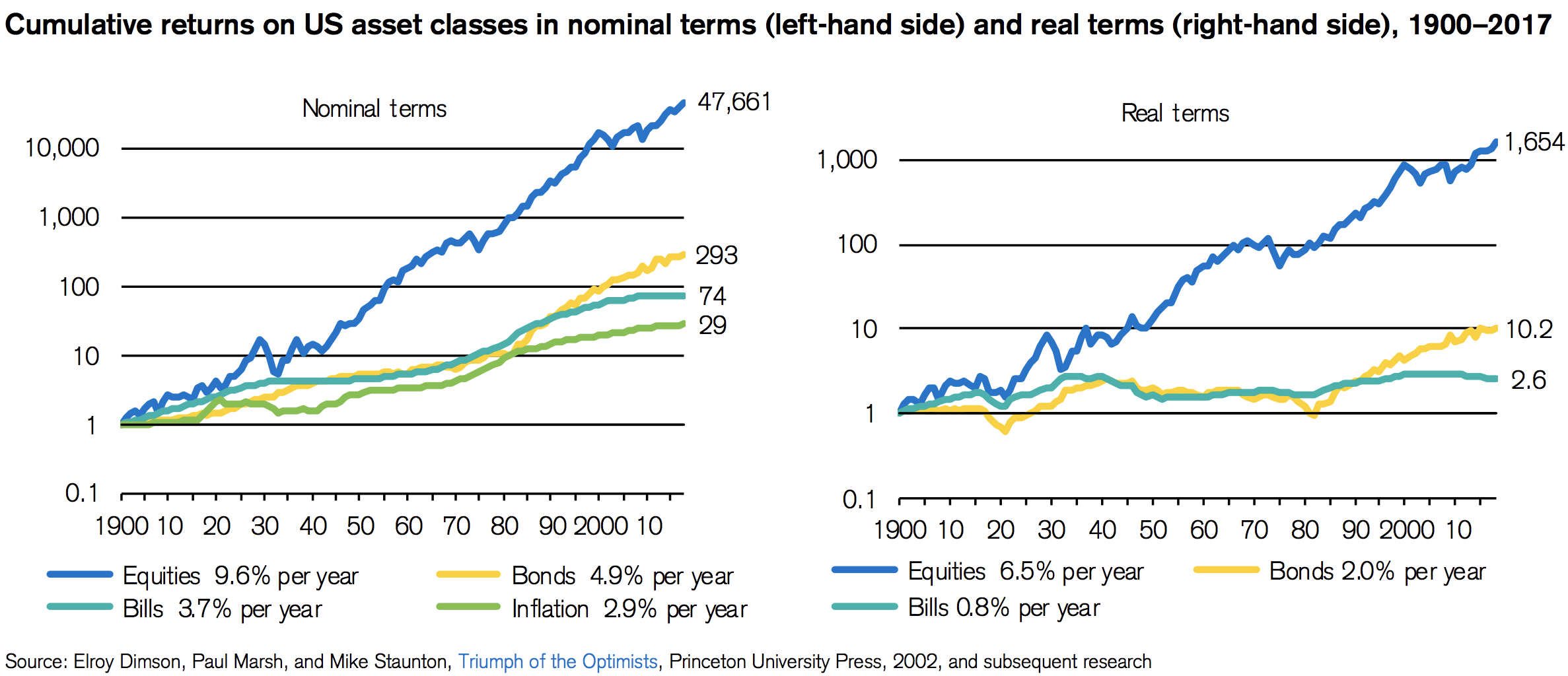

Since 1900, both on an absolute and inflation-adjusted basis, equities (including REITs) have vastly outperformed bonds as well as cash equivalents like short-term Treasury bills.

Source: Credit Suisse

However, the reason that most financial advisors still recommend investors own some bonds (more on this in a moment) is that bonds serve an important role in your portfolio.

Not only do bonds generate fixed income, but they tend to be much less volatile than stocks and have historically had very low correlations with stocks. For instance, between 1928 and 2017 the correlation between stocks and bonds was just 0.03, meaning that these two asset classes traded almost completely independent of each other.

The benefit of such low correlation is that owning some bonds can drastically reduce your portfolio's overall volatility, especially when the stock market experiences one of its inevitable bear markets.

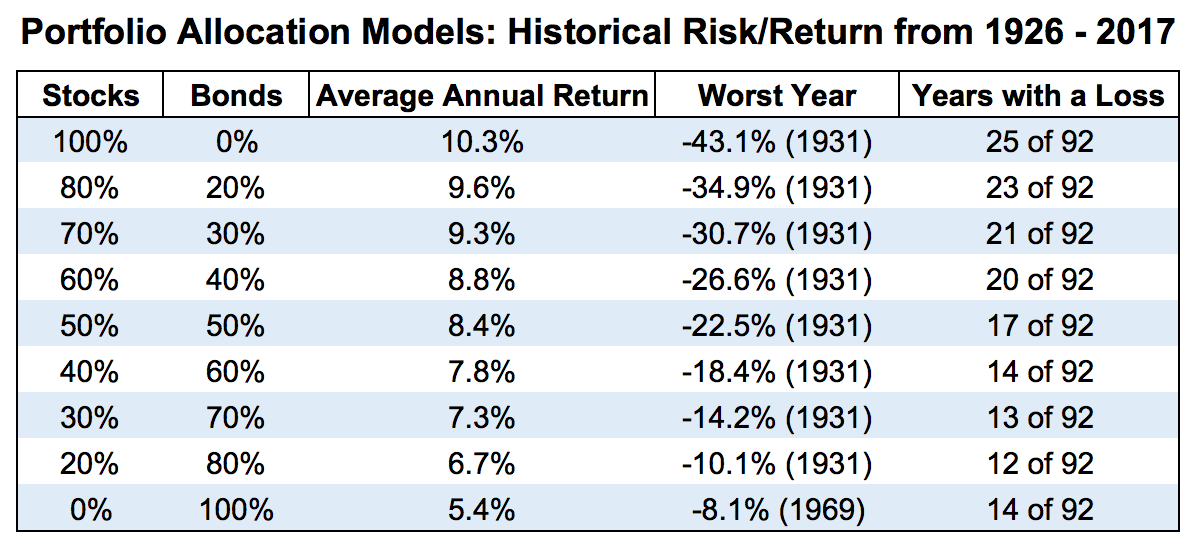

This is why the default recommendation for most retirement portfolios (once you are already retired) is 60% stocks and 40% bonds. Such a portfolio has historically captured much of the upside of a 100% stock portfolio but with far smaller declines during years when stocks crash.

1974 and 2008 have been the worst years for stocks since World War II and provide good examples of the stability bonds can provide:

1974: S&P 500 lost 26.5% (60/40 portfolio declined 14.7%)

2008: S&P 500 lost 37.0% (60/40 portfolio declined 13.9%)

Bonds, which tend to appreciate during market declines (flight to safety and falling interest rates), are thus a good way to smooth out your total returns while still typically enjoying a healthy rate of compounding.

Historically, a 60/40 stock/bond portfolio has captured the majority of a 100% stock portfolio's total returns while significantly reducing a portfolio's drawdowns.

Source: Vanguard, Simply Safe Dividends

So that settles it, bonds are great and your portfolio should consist of 40% bonds, right? Well, not necessarily.

While historical data is a useful guide to making long-term investment decisions, it's important to keep in mind that bond returns over the last few decades were boosted by an interest rate environment that is unlikely to persist in the future.

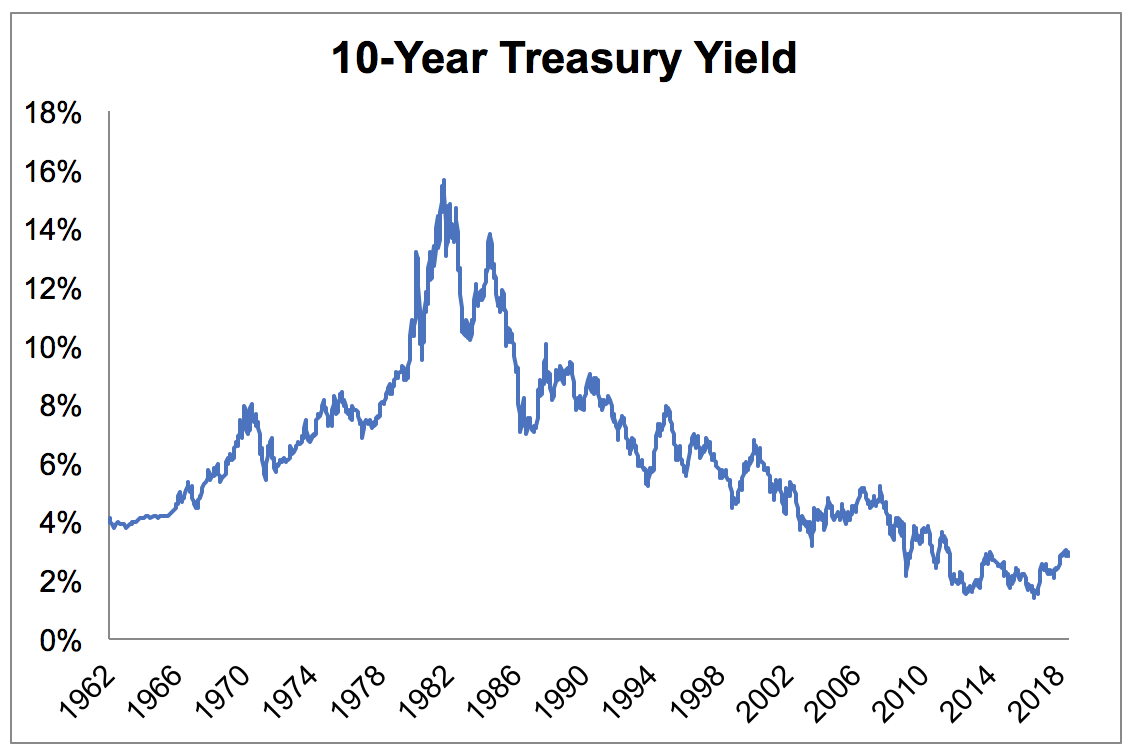

Specifically, between 1981 and 2016 the benchmark 10-year Treasury yield declined steadily from a high of nearly 16% to its lowest level in history (1.4% in July 2016).

Source: St. Louis Federal Reserve, Simply Safe Dividends

Bond prices move inversely to interest rates, so this asset class enjoyed a 35-year secular bull market that greatly benefited fixed income investors over most of our investing lifetimes.

Going forward, the outlook for long-term bonds looks much less attractive. In fact, during Berkshire Hathaway's 2018 shareholder meeting, Warren Buffett commented that "long-term bonds are a terrible investment at current rates and anything close to current rates."

The yield on a 10-year Treasury sits near 3% today. Since interest paid by these bonds is taxable at the Federal level, their after-tax yield is roughly 2.5%. And if the Federal Reserve successfully hits its 2% annual inflation target, then the after tax return, adjusted for inflation, on these long-term bonds would be about 0.5% per year.

As Buffett said, long-term bonds at these rates are “ridiculous.” Investors thinking about buying long-term bonds need to keep this in mind, especially as they look at historical returns of various retirement portfolio allocations.

Future bonds returns are unlikely to come close to what they delivered in past decades. Therefore, playing too conservatively by investing heavily in long-term bonds could result in a nest egg not lasting long enough to cover a full retirement given its lower returns.

Like bonds, REITs also have several pros and cons. Let's look at the role REITs can serve in providing growing income and long-term capital appreciation in a retirement portfolio.

Advantages and Disadvantages of REITs

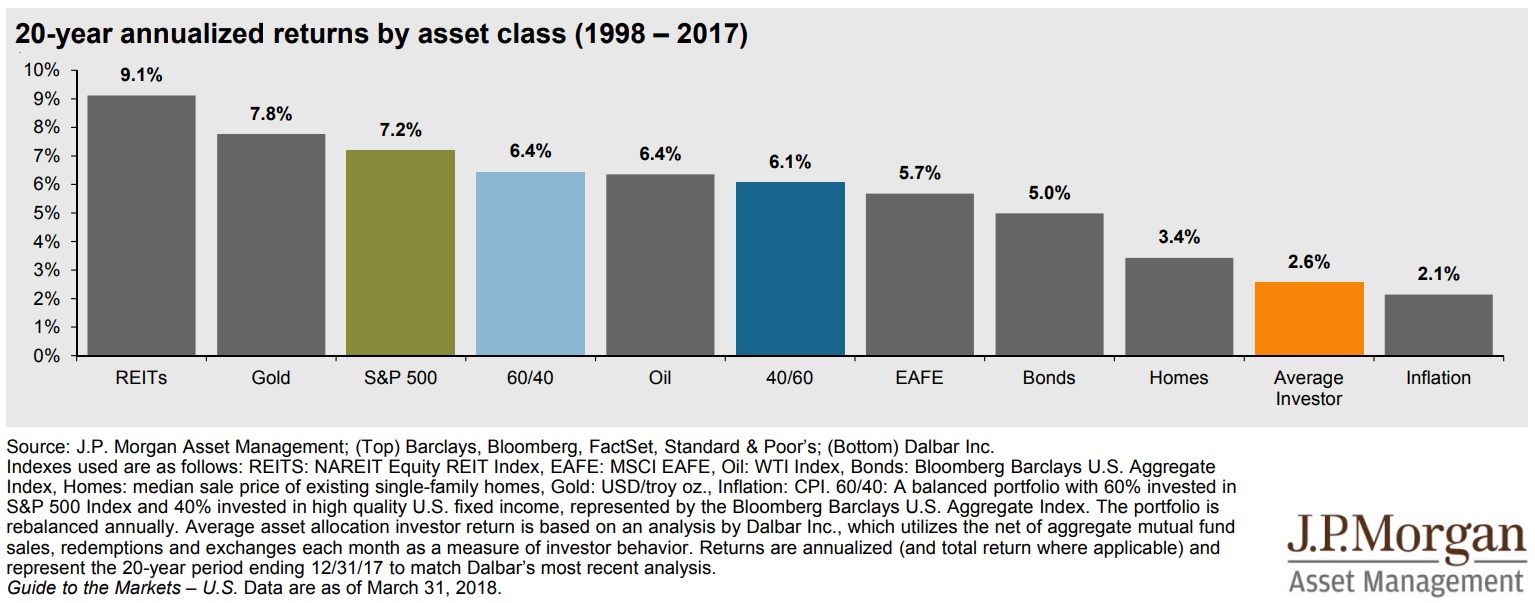

Historically, REITs have been a reliable source of safe and growing income while delivering healthy total returns as well. In fact, over the past 20 years, REITs were the best performing asset class in the U.S. and nearly doubled the rate of return delivered by bonds.

Source: J.P. Morgan Asset Management

Unlike bonds, which pay a fixed amount of interest and have a set maturity date, REITs are productive assets that can increase in value indefinitely. As these businesses profitably acquire more properties, they grow their cash flow, can increase their dividends, and see their stock prices appreciate over time.

REITs are appealing holdings in many retirement portfolios because they are required by law to pay out at least 90% of their taxable income as dividends. As a result, many REITs have high dividend yields between 5% and 10%, providing much more current income than bonds while also offering the potential for income growth and capital appreciation.

Similar to bonds, the performance of REITs can be sensitive to interest rate fluctuations over the short term. However, since these are productive assets that can grow their cash flow over time, interest rates are less of a factor in the long term.

In fact, Standard and Poor's published a study reviewing the impact of rising interest rates on REITs. The firm stated that “when expectations about future interest rates change suddenly, REITs have often experienced high volatility and rapid price changes.”

However, Standard & Poor's concluded that interest rate fluctuations are much less meaningful over longer stretches of time:

“Ultimately, whether interest rates are rising or falling does not seem to be the key driver of REIT performance over medium- and long-term periods. Rather, the more important dynamics to address are the underlying factors that drive rates higher. If interest rates are rising due to strength in the underlying economy and inflationary activity, stronger REIT fundamentals may very well outweigh any negative impact caused by rising rates.”

Furthermore, since 1972 equity REITs (the ones that own commercial rental properties) have outperformed all three major stock market indexes. That's despite high and rising interest rates in the 1970s and early 1980s.

In fact, since 1972 the correlation between the benchmark 10-year Treasury yield and REIT total returns has been just 0.04 (effectively zero). This shows that, while REITs can be sensitive to long-term interest rates in the short term, over the long term this sensitivity cancels out.

And it's not just in the U.S. that REITs have delivered healthy total returns over time. A Dutch study looked at global REIT total returns (adjusted for inflation) from 1960 to 2015 and found solid performance compared to other asset classes as well:

Global REIT inflation-adjusted total returns: 6.4%

Global stock real returns: 5.5%

Non-government bonds: 3.5%

Government bonds: 3.1%

In every single decade, REITs outperformed stocks, and typically bonds as well. And that's across a wide variety of economic, industry, and interest rate environments.

However, before you think that investing exclusively in REITs is the answer to achieving your financial goals (such as living off dividends during retirement), there are some big downsides to know about REITs.

First, the very thing that makes this such a high-yielding sector, the requirement to pay out nearly all taxable income as dividends, also means that REITs are highly dependent on external capital markets to fund their growth.

Specifically, since very little cash flow is retained to fund new property acquisitions, growing REITs must frequently issue equity and debt to keep their businesses growing. Buying real estate is not cheap, so REITs are generally highly leveraged.

Given the long-term nature of REIT leases and their stable cash flows, this isn't usually a major risk factor. However, in the event that credit markets collapse (as happened during the Financial Crisis), REITs with weak balance sheets can be forced to cut their dividends, even if their cash flow covers their payouts.

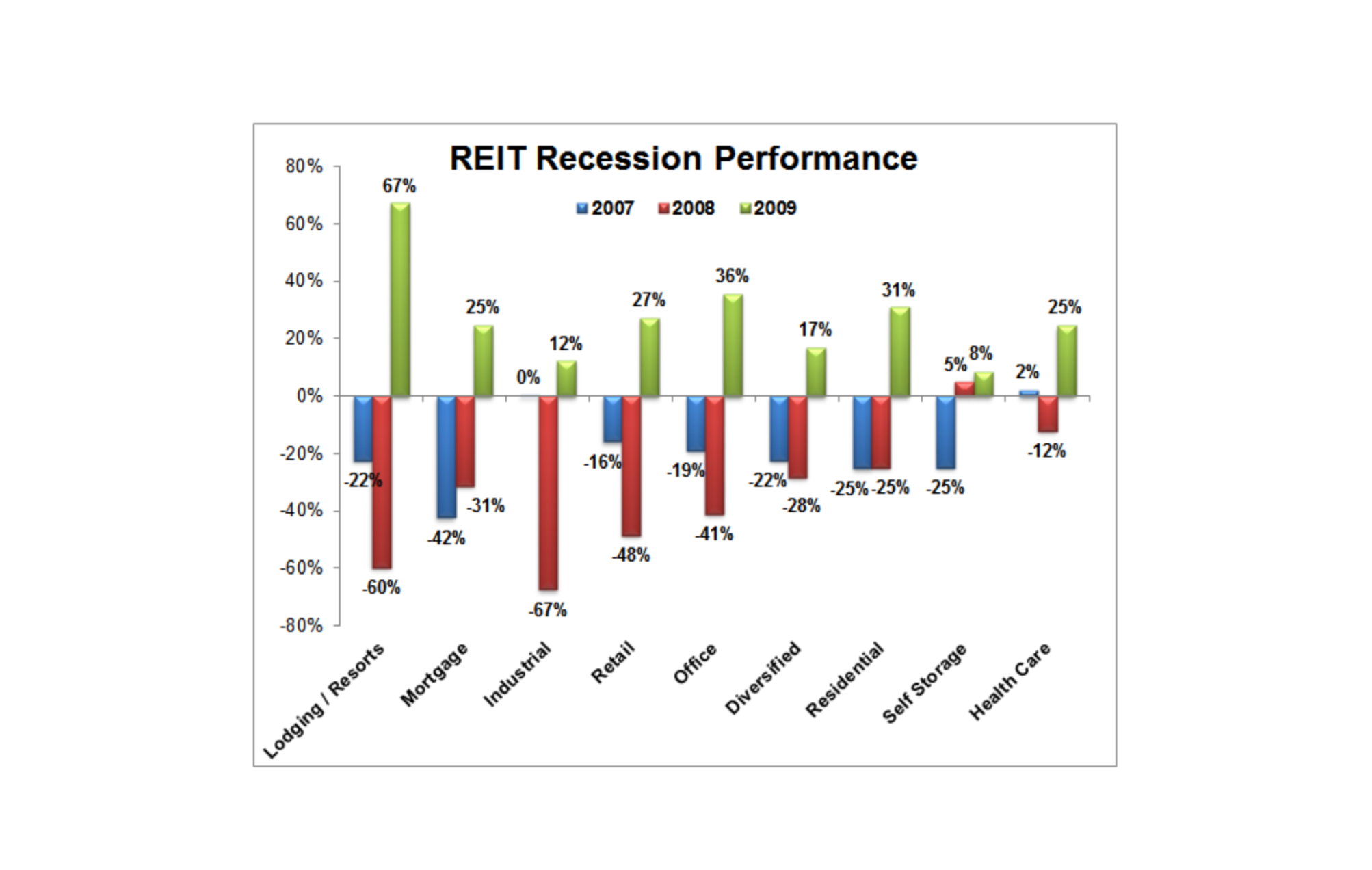

During the Great Recession, many REITs were overleveraged, thanks to taking on too much debt during the low-interest rate environment of the 2000s. When credit markets slammed shut, from May 2008 through March 2009 about 30% of all REITs suspended, cut, or switched to paying part of their dividend in company stock, per The Wall Street Journal.

In part due to these dividend cuts, REITs as a sector fell 70%, far worse than the S&P 500's 57% peak-to-trough decline. This was a major shock to REIT investors who have typically enjoyed much lower volatility during bear markets.

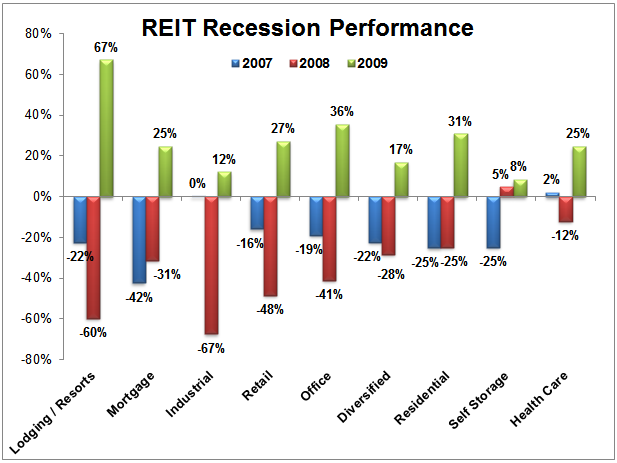

As you can see, certain types of REITs held up better than others. Defensive areas like self storage and healthcare held up the best in 2008. However, each REIT subindustry was hammered compared to Treasury bonds, which actually gained in value during the financial crisis.

Source: Simply Safe Dividends, REIT.com

Simply put, REITs are more vulnerable to market selloffs than bonds. Fortunately, REITs today have the strongest collective balance sheets in their history, according to data from NAREIT and Hoya Capital Real Estate.

In other words, barring an even worse Financial Crisis in the future, more REITs will presumably be able to maintain or even grow their dividends even during future economic downturns and bear markets. However, there is another important disadvantage REITs face that you need to be aware of.

Specifically, REITs grow both via issuing debt and additional equity. This is due to their "pass-through" nature, in which they retain little cash flow to fund growth because they are required to pay out most of it in the form of dividends.

Blue-chip REITs that are conservatively run are able to adjust their capital raises to continue growing their property bases, cash flow, and dividends, in all manner of share price and interest rate environments.

For example, during REIT bull markets, when share prices are high and cost of equity low (making equity raises more accretive to cash flow per share), REITs sell more shares. During bear markets, they turn to low cost, fixed-rate bonds to fund their growth.

But smaller REITs (typically newer ones) often lack large economies of scale and access to large amounts of low-cost capital. Thus they can be highly reliant on equity markets for growth funding.

When REITs are out of favor, their low share prices create high costs of equity that can make profitable growth challenging, and in some cases impossible. And since new REITs tend to IPO with high dividends (to attract investor interest) they can take several years to grow into their dividends and bring their payout ratios to safe levels.

Thus conservative income growth investors typically want to stick with large, well-established REITs that have strong access to low-cost growth capital and solid long-term dividend growth track records.

So what's the right mix of REITs and bonds in a retirement portfolio? While that answer will be different for everyone, there are some geeneral rules of thumb you can follow.

What's the Right Mix of REITs and Bonds in a Retirement Portfolio?

Rather than focusing on whether you should own lots of bonds or lots of REITs, the right way to think about your portfolio is via a holistic, total asset allocation strategy. That usually means talking with a certified financial planner to work out the best mix of stocks, bonds, and cash that is most likely to meet your unique long-term financial needs.

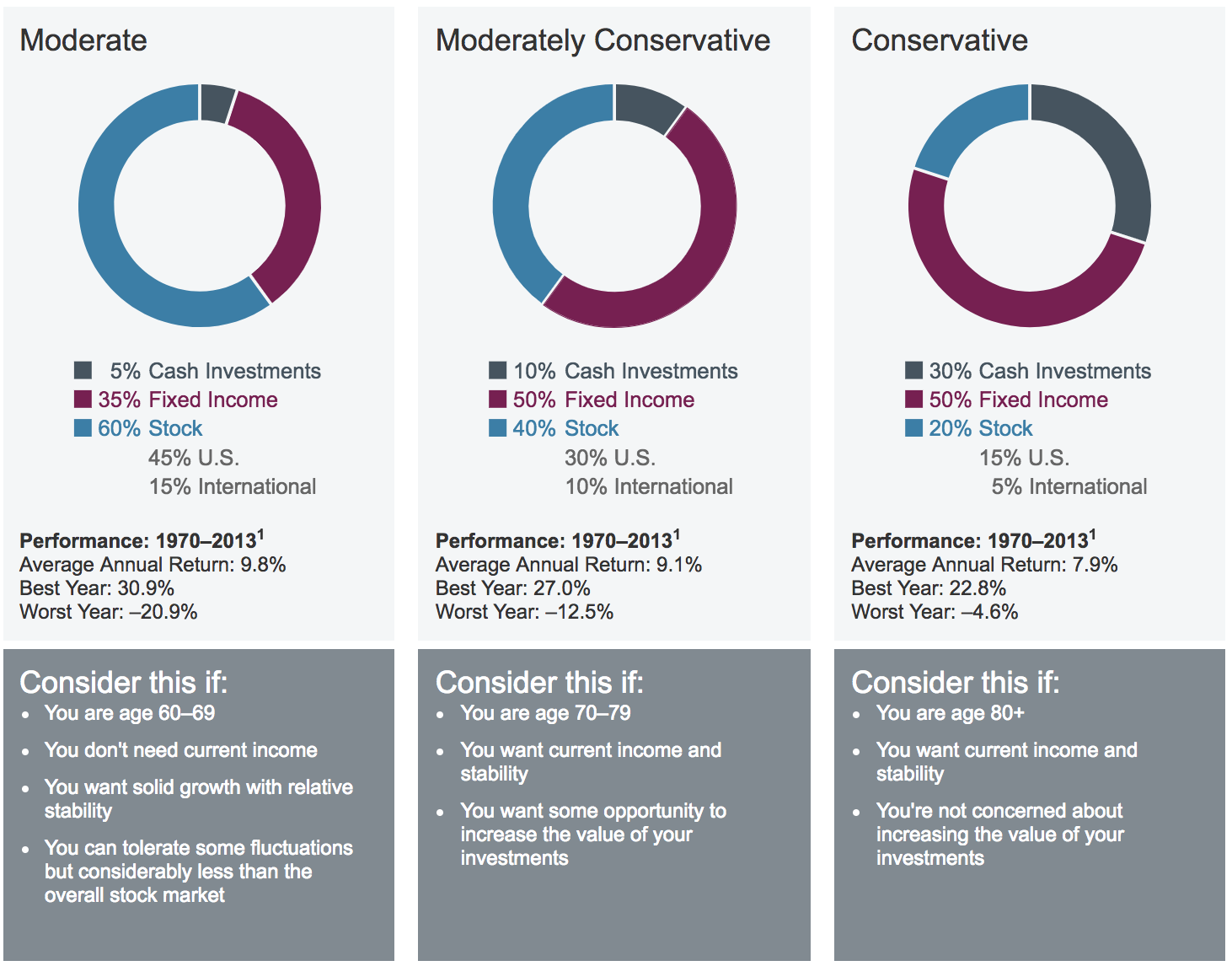

While everyone's optimal asset allocation is different, and a lower interest rate environment in the future might change the default setting for most investors, here's what bank and brokerage firm Charles Schwab has historically recommended for retirees.

Source: Charles Schwab

The reason for owning a mix of stocks, bonds, and cash is because each type of asset serves a different purpose. Cash is to provide for your short- to medium-term living expenses. The average bear market has historically lasted about three years (from when stocks peaked to when they hit new all-time highs again). Thus having sufficient cash is useful in avoiding having to sell other assets to fund living expenses.

Bonds, because they tend to rise during bear markets in stocks, can provide moderate income to live off, as well as represent a low-volatility asset you can sell in case the slump in stocks takes longer than usual to recover from.

Stocks are there to both generate income (dividends) as well as build wealth over time so you avoid running out of money during retirement (say if you're using the 4% rule).

REITs are a kind of equity, so the right way to think about them isn't as an alternative to bonds (REITs are not "bond proxies" over the long term) but rather what percentage of your stock portfolio should be in REITs.

Again, the right amount of REIT exposure depends on your individual goals, risk tolerances, and portfolio size, among other considerations. However, a good rule of thumb we like to follow is that no single sector should represent more than 25% of your equity portfolio. That's to ensure that, in the event of an extreme historical anomaly (like REITs getting clobbered during the Financial Crisis), your income and stock portfolio avoid suffering a disaster.

Closing Thoughts on REITs vs. Bonds

The last decade saw the lowest interest rates in U.S. history, creating a "hunt for yield" in which many income investors turned to REITs as a bond alternative. However, bonds and REITs are very different, both in terms of their advantages and disadvantages.

REITs are a form of equity (stock) that should continue enjoying total returns that are superior to bond returns over time while also doling out higher amounts of current income. When you buy shares of a REIT, you own a perpetual stake in an expanding real estate operation that hopefully pays steadily rising dividends as it grows in value over time.

Bonds are a fixed-income asset that is lower risk due to its preferred position in the capital stack. However, bonds are highly sensitive to inflation and interest rates since their coupon payments are fixed. And with interest rates remaining near historic lows (bond prices fall when rates rise), future long-term bond returns seem likely to be mediocre compared to the past.

While both REITs and bonds have enjoyed lower volatility compared to stocks, bonds are the lower volatility asset class due to their much lower correlation with stocks. Meanwhile, REITs can experience significant share price volatility, especially over short periods of time. Their dividends are also not as safe as bond coupon payments over a full economic cycle.

The right way to think about REITs versus bonds is in the sense of your total asset allocation. REITs can make up a certain amount of the equity portion of your portfolio, while bonds should be owned separately because they serve a different purpose during a recession and bear market (capital preservation).

In general, a good rule of thumb is that REITs should not make up more than 25% of a well-diversified dividend stock portfolio, depending on your individual goals (such as what portfolio yield and long-term dividend growth rate you're targeting, and how much volatility you can stomach).

And as always, the primary focus of conservative REIT investors should be on maximizing safe income, rather than taking on excessive risk by reaching for yield in stocks with potentially unsustainable dividends. Our Dividend Safety Scores can help investors sidestep stocks with the riskiest payouts.