When it comes to building a dividend portfolio, there are many different opinions on the best approach.

Investors often debate the ideal number of stocks, how to diversify across sectors, and whether to focus on high dividend stocks or those with growth potential.

While there's no one-size-fits-all answer, here are the general guidelines we like to follow when building a dividend portfolio:

Hold between 20 and 60 stocks to reduce company-specific risk

Roughly equal-weight each position

Invest no more than 25% of your portfolio in any one sector

Before reviewing a dividend stock portfolio example, let’s explore why a diversified portfolio is crucial for generating consistent income and managing risk when building a dividend portfolio from scratch.

Building a Portfolio Reduces Risk

Why should investors build a dividend portfolio instead of investing in just one or two companies that they like the most?

For one thing, investing involves a tremendous amount of randomness and luck. The world constantly changes in unpredictable ways, so even the “best” investment professionals are wrong around half of the time.

If we invested all of our cash into a single company, even one with seemingly “low” risk, we will likely generate returns that are significantly different than the market’s performance – for better or worse.

Many investors do not have the stomach for this level of volatility, especially since numerous unexpected events could occur to put your capital at risk of being permanently lost.

Remember Enron? What about Lehman Brothers? Going “all-in” on any single company can have severe consequences.

On the other end of the spectrum, suppose you bought shares of every stock in the market. For each company in your portfolio that experienced bad news, you would likely own just as many firms experiencing unexpectedly good news.

In other words, you would no longer be dependent on any single stock to drive your investment returns and dividend income. Your portfolio could weather a few unanticipated storms because it was diversified across a number of different companies.

So long as America continues to survive and advance, there would be virtually no chance of your portfolio experiencing a permanent loss of capital – the market has historically appreciated over long periods of time and will likely continue to do so.

Of course, it is impractical for an individual investor to buy shares of every company in the market without the use of exchange-traded funds (ETFs), but you can understand the advantages of owning more than just a couple of stocks.

Properly constructed portfolios can help us find the right balance to diversify risk and get closer to our objectives. Building a dividend portfolio starts with an understanding of the key risk factors that influence a portfolio’s returns and volatility, beginning with how many stocks to own.

Hold Between 20 and 60 Stocks

Many of the best investment professionals run concentrated portfolios. For example, Apple accounts for over 20% of Berkshire Hathaway's overall stock portfolio (check out Warren Buffett's dividend stocks here).

They invest with conviction behind their top ideas, believing in Warren Buffett's statement that "diversification is protection against ignorance."

But as individual investors on the outside looking in, we do not have Warren Buffett’s resources, connections, and insights needed to responsibly run a concentrated portfolio.

For that reason, we prefer to spread our bets over a reasonable mix of different stocks to avoid shooting ourselves in the foot with a concentrated bet that sours.

The fewer stocks you own, the greater your portfolio can deviate from the market’s return. So how many dividend-paying stocks should you own to maximize the benefits of diversification? Plenty of academic studies have tried answering this question over the last 50 years.

The American Association of Individual Investors (AAII) wrote a 2004 article citing that:

“Holding a single stock rather than a perfectly diversified portfolio increases annual volatility by roughly 30%… Thus, the single-stock investor will experience annual returns that average a whopping 35% above or below the market – with some years closer to the market and some years further from the market.”

The AAII study went on to state that, as a rule of thumb, diversifiable (i.e. company-specific) risk will be reduced by the following amounts compared to owning a single stock

Holding 25 stocks reduces diversifiable risk by about 80%

Holding 100 stocks reduces diversifiable risk by about 90%

Holding 400 stocks reduces diversifiable risk by about 95%

A more recent study was released in a 2014 paper titled, “Equity Portfolio Diversification: How Many Stocks are Enough? Evidence from Five Developed Markets.”

Notable findings were that a greater number of stocks are needed to diversify risk during periods when markets are in financial distress – correlations between stocks are often the highest in this type of environment.

Within the U.S., the researchers concluded that, to be confident of reducing 90% of the diversifiable risk 90% of the time, the number of stocks needed on average is about 55. In times of distress, however, that figure can increase to more than 110 stocks.

Overall, we believe creating a dividend portfolio with 20 to 60 stocks provides a reasonable balance between the need for diversification, a desire to keep trading activity low, and a limited amount of research time to devote to maintaining a portfolio.

Investors with larger portfolios, a greater willingness to spend time on research, and an increased comfort from being more diversified may lean towards the high end of our recommend number of holdings.

Portfolios filled with more speculative stocks facing a wider range of outcomes may also prefer to spread their bets over a larger number of holdings. Figuring out how much to invest in each position is the next step.

Equally-Weight Your Holdings

"It's tough to make predictions, especially about the future." The late Yogi Berra, who played professional baseball and never shied away from sharing his unconventional wisdom, could have been explaining the reasoning behind our next portfolio construction guideline.

When creating a dividend portfolio from scratch, we prefer to roughly equal-weight our positions because it is hard to know which holdings will be the best long-term performers.

The stock market is quite efficient in the long run. This largely explains why so few active fund managers, who spend millions of dollars on research each year, have outperformed their respective benchmarks over time.

In fact, S&P found that 93% of all U.S. active stock fund managers underperformed their benchmarks in the past 20-year period through 2023.

Over the years we have met with several portfolio managers of funds that have impressive long-term track records and conduct world-class research. None of them could escape the inherent uncertainties that can make investing difficult.

In fact, some of these managers shared with us that they could never predict which holdings would do the best any given decade.

The bulk of their outperformance was driven by only a couple of holdings as well, with around 40-50% of their investment ideas ultimately failing to work out.

We aren't any smarter than them. And spreading our bets evenly across our portfolio ensures we don't outsmart ourselves either.

Invest No More Than 25% of Your Portfolio in Any Sector

Owning more stocks can reduce risk, but investors can still end up with poorly diversified portfolios if they are drawn to certain types of stocks (e.g. consumer products with familiar brands) or investing “rules” (e.g. only buy stocks with price-to-earnings ratios less than 12x).

A dividend portfolio holding lots of stocks that have many shared characteristics may not be adequately diversified.

This is because stocks from similar industries are often sensitive to the same factors and move together in the market (i.e. they are highly correlated).

If a shared factor, such as interest rates or the price of oil, becomes unfavorable, your portfolio could significantly underperform the market.

Picking stocks from different sectors and industries helps diversify away this risk. When some sectors are struggling, others are likely doing well.

The pie chart below shows the sector breakdown of the S&P 500. You can see that only one sector, Information Technology, accounts for more than 15% of the overall market.

Our preference is to invest no more than 25% of our portfolio in any single sector, and we try to own companies with little overlap in their operations.

Source: S&P Dow Jones Indices

However, sector diversification should not come at the expense of violating valuation principles or extending outside of your circle of competence.

Just because consumer staples account for about 6% of the S&P 500 doesn’t mean you must buy a stock in that sector if you cannot find one that is reasonably priced.

Equally important, you should not diversify into a sector or industry that is outside of your comfort zone.

For example, many conservative investors remain underweight the technology sector because its pace of change is too fast. Trying to predict which tech companies will still be relevant in five years can be challenging.

When in doubt about whether an investment is in your wheelhouse, famous fund manager Peter Lynch provided a helpful test:

Never invest in any idea you can’t illustrate with a crayon.

The bottom line is that you should be intentional with your diversification across sectors and business models, but you don’t need to play everywhere. Stick to areas of the market you are comfortable with and use common sense as you look to diversify.

Target Companies With Safe Dividends

Building a dividend growth portfolio for regular income works only if the dividends do not get cut.

Dividend cuts happen most frequently when the tide goes out during recessions. Companies with too much debt, cyclical profits, inconsistent free cash flow generation, and poor dividend coverage are more likely to put their payouts on the chopping block.

Investors creating a monthly dividend portfolio should avoid businesses with these qualities. That means looking for companies with low leverage ratios, resilient earnings streams, conservative payout ratios, time-tested operations, and long track records of paying reliable dividends.

Certain groups of stocks like the S&P Dividend Aristocrats are popular because they consist of companies that have paid higher dividends without interruption for decades.

But dividend streaks alone aren't always a great indicator of safety. For example, of the 60 dividend aristocrats that existed heading into the 2007-09 financial crisis, 16 of them cut or suspended their dividends.

Our Dividend Safety Scores™ can help investors avoid dividend cuts before they happen. We monitor payout ratios, leverage, earnings estimates, news, and more to evaluate the sustainability of a company's dividend over a full economic cycle.

Since our scoring system's inception in 2015, we have recorded every dividend cut in our coverage in realtime. Investors who stuck with companies that had Safe or Very Safe Dividend Safety Scores™ would have avoided 97% of the 700-plus cuts we have seen.

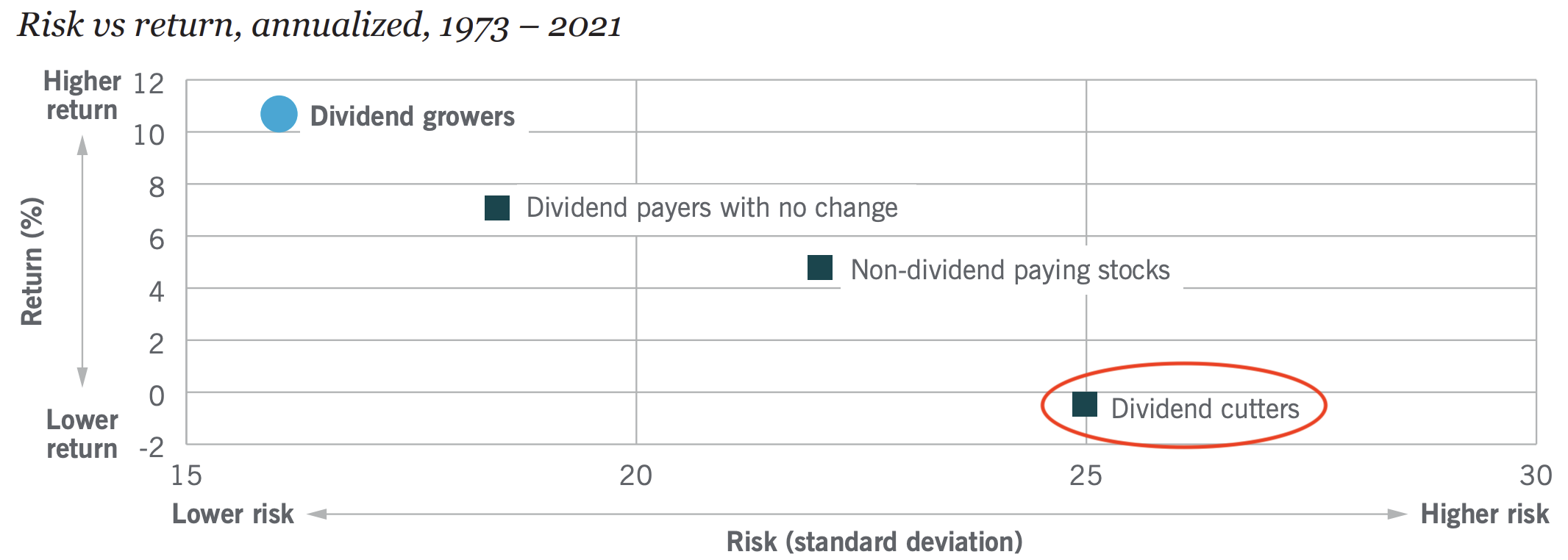

The chart below, courtesy of Nuveen, shows the performance from 1973 through 2021 of S&P 500 stocks grouped by dividend policies. Dividend cutters had lower returns and higher volatility compared to other stocks.

Source: Nuveen, Ned Davis Research, Refinitiv

Steering clear of these companies can help your portfolio deliver more predictable returns and steadily rising income.

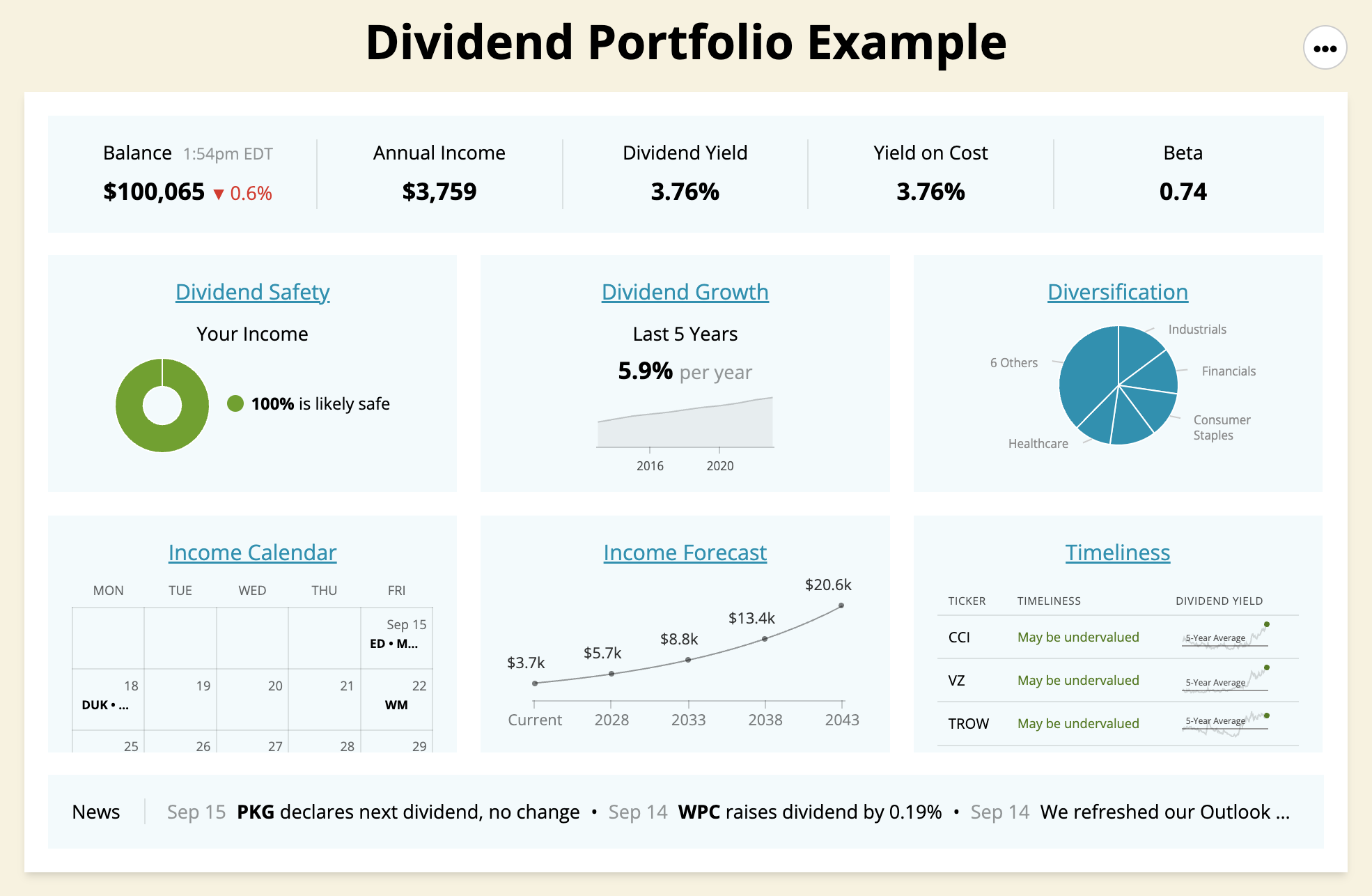

Dividend Portfolio Example

Putting our four portfolio-building guidelines into practice, we put together an example dividend stock portfolio.

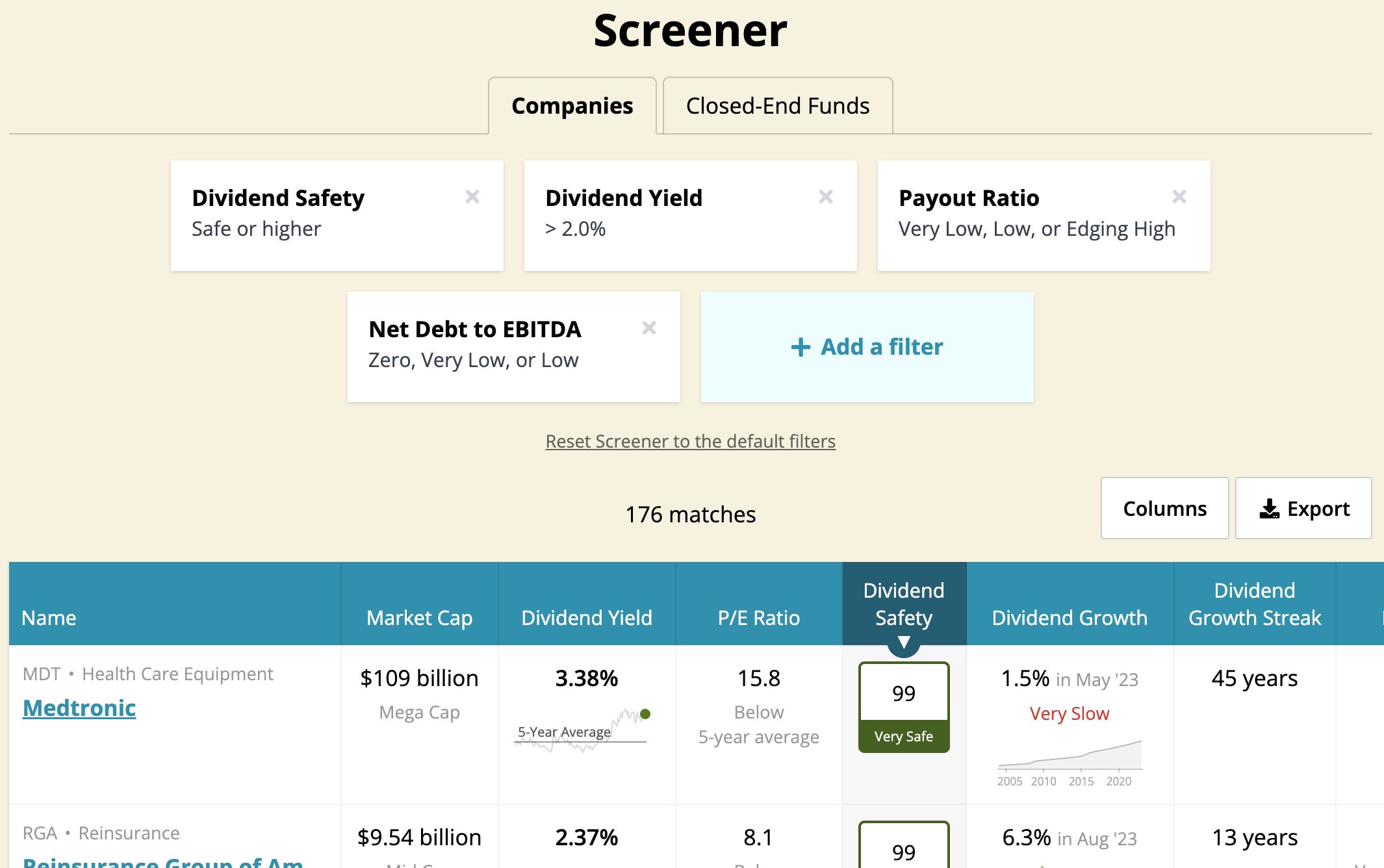

We used our stock screener to select 40 dividend stocks with Safe or Very Safe Dividend Safety Scores™, dividend yields above 2%, simple business models, moderate-to-low payout ratios and leverage, and a diverse mix of sectors. Here are all 40 stocks in our example dividend portfolio:We then equally-weighted these 40 dividend stocks (each 2.5% of the portfolio's market value) and loaded them into our website's portfolio tracker.

Here's a position sizing example. Suppose Company A traded at $10 per share and Company B is $2 per share, and we wanted to invest $1,000 in each stock.

We would need to buy 100 shares of Company A (100 shares x $10 per share = $1,000) and 500 shares of Company B (500 shares x $2 per share = $1,000).

Highlights from the reports below show that our example dividend portfolio sports a 3.8% dividend yield, has grown its income by 5.9% annually over the past five years, is well diversified across sectors, and generates 100% of its income from stocks with Safe or Very Safe Dividend Safety Scores™.

Source: Simply Safe Dividends

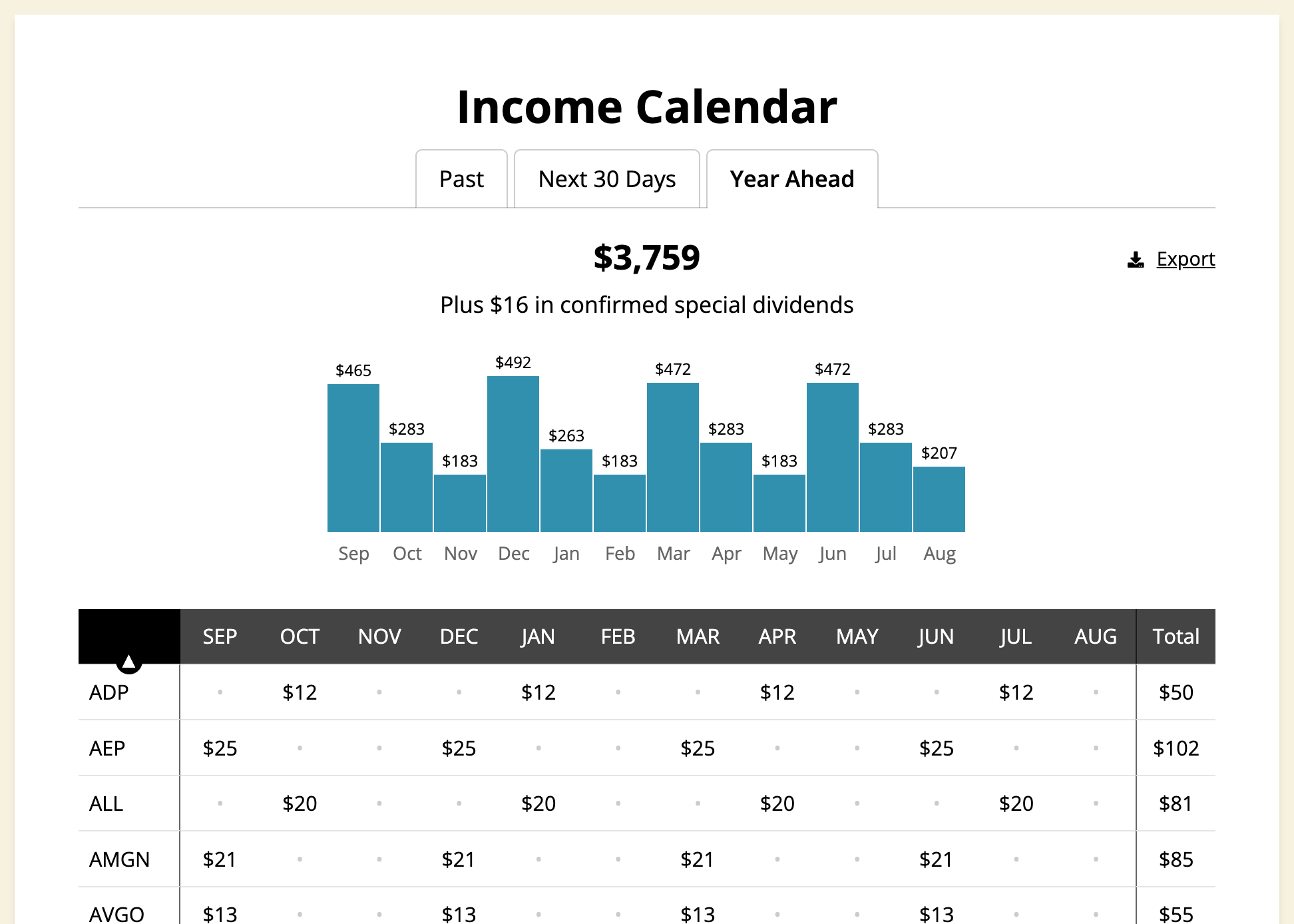

Owning a diversified portfolio of dividend stocks results in a predictable monthly income stream. Drilling into our portfolio's Income Calendar report, we can see how much each stock is paying us and when.

Some investors like to smooth their monthly income by purchasing stocks that pay certain months of the year. However, this should be a very secondary priority to the portfolio construction guidelines we shared.

Source: Simply Safe Dividends

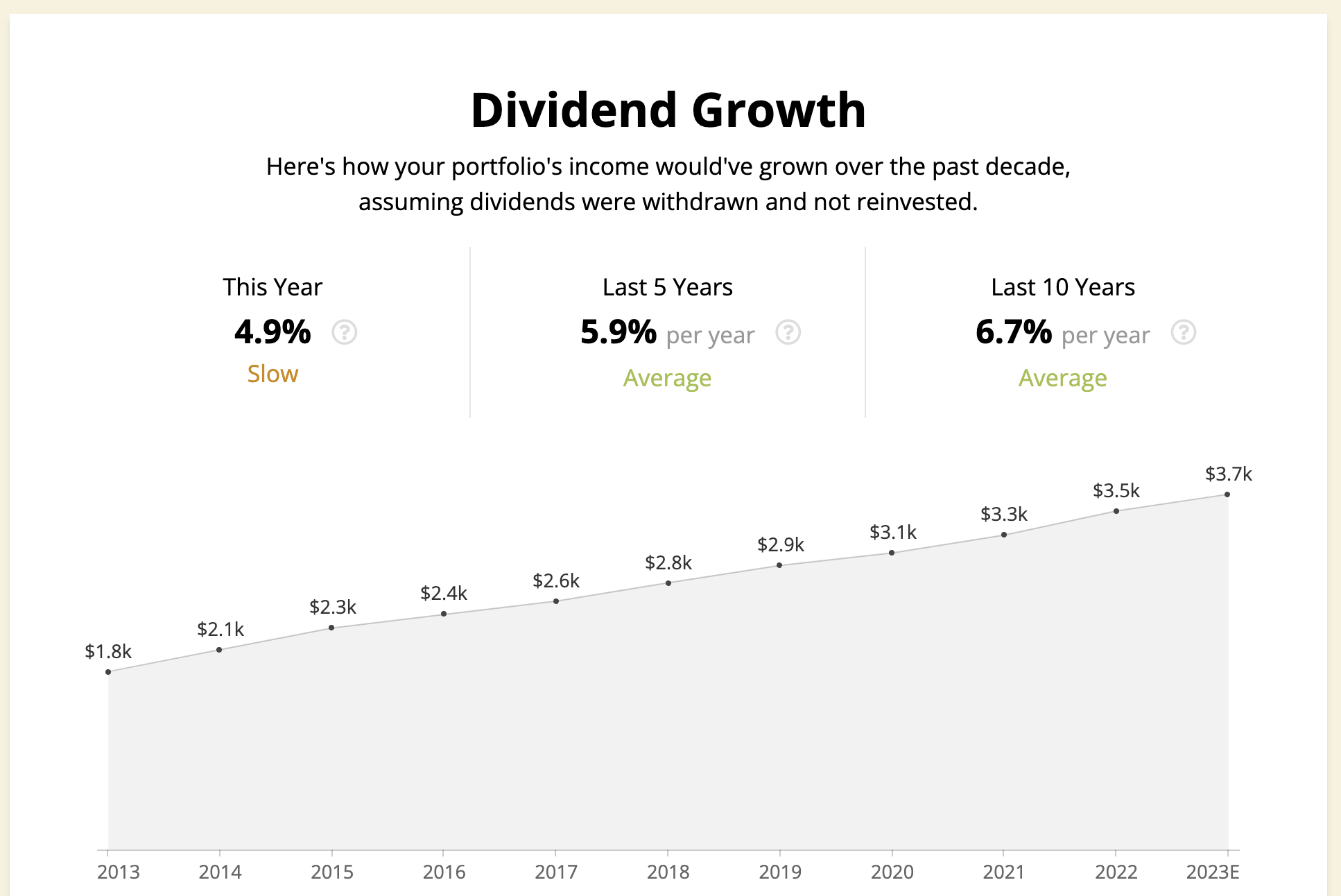

Our portfolio's Dividend Growth report shows that this annual income stream has steadily increased over the years. Our holdings collectively grew their dividends by around 7% annually during the last decade.

Source: Simply Safe Dividends

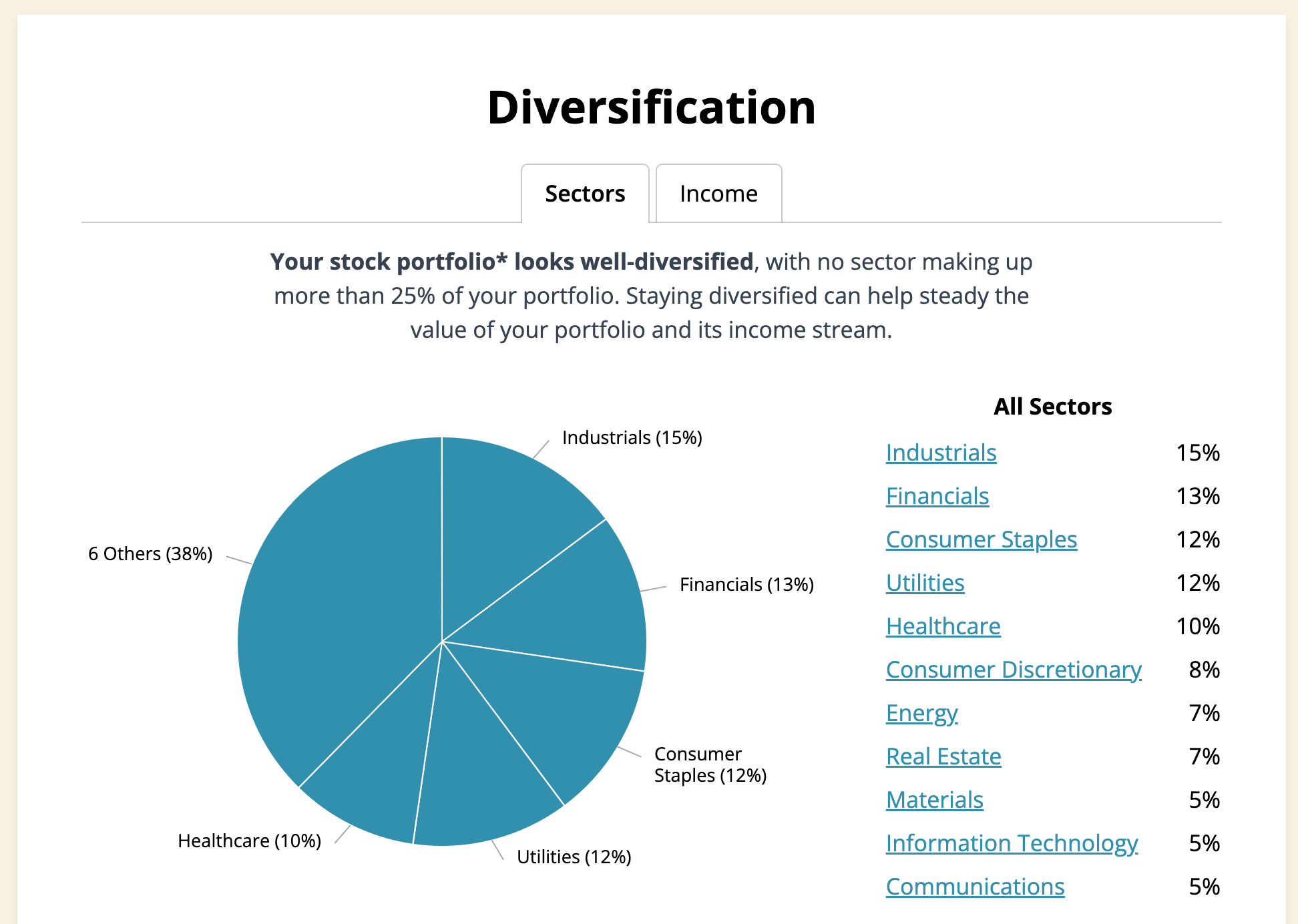

Turing to diversification, the 40 stocks we own are spread nicely across different sectors, with none accounting for more than 15% of the portfolio's value. We are not overly exposed to any area of the market.

Source: Simply Safe Dividends

And from an income perspective, no single stock accounts for more than around 5% of our portfolio's total dividend income.

With most of our holdings expected to continue growing their dividends, our income stream has a good chance of holding its ground even if we experienced a surprise dividend cut or two during the next downturn.

Source: Simply Safe Dividends

This sample dividend portfolio checks all of the primary guidelines we like to follow when getting started.

From here we monitor the performance of our holdings, keeping an eye on the shifting weights of our positions and any material developments that could impact their dividend safety or long-term outlooks.

You Can Build a Dividend Portfolio for Regular Income

Whether you want to live off dividends today or are investing for the long haul, the best way to build a dividend portfolio for steady income is to follow a simple set of risk management principles:

Hold between 20 and 60 stocks to reduce company-specific risk

Roughly equal-weight each position

Invest no more than 25% of your portfolio in any one sector

Target companies with Safe or Very Safe Dividend Safety Scores™

We built Simply Safe Dividends to help investors keep their retirement portfolios between the guardrails. If you are interested in seeing how your portfolio stacks up, you might like to try our online product, which lets you track your portfolio's income, dividend safety, and more.

You can learn more about our suite of portfolio tools and research for dividend investors by clicking here.