Retirement Planning Strategies: 4% Rule vs. Dividend Stocks

Contributed by Dave Van Knapp

I have been retired for more than 22 years. Based on my experience, as well as most literature about the subject, funding retirement is primarily about being able to pay your regular, predictable expenses.To do that, you need income.

Most retirement financial planning comes down to generating enough income without running out of money.

That goal breaks down into two factors.

1. How much retirement income will you need?

Many conventional rules of thumb, like “You will need 70% of your final year’s working income,” are worthless. The obvious flaw is that rarely does your final working income exactly match your expenses, so your final paycheck is not a good proxy for how much you need in retirement.

Another flaw in basing retirement needs on your final working income is that your expenses will change significantly. Pre-retirement categories like business travel, certain kinds of clothes, Social Security taxes, and saving for retirement all disappear.

On the other hand, new categories come up, like travel, hobbies, leisure activities, and spoiling your grandkids.

The bottom line is that you need to develop a sensible budget to know your income needs.

2. Where will your retirement money come from?

This question gets at the crux of this article, because we are going to compare two different strategies for generating retirement income: The 4% Rule vs. dividend streams.

Of course, you will have other sources of income, such as Social Security and maybe a pension.

But here, we will focus on income from your investments. For most investors, this is a significant factor in retirement happiness.

Retirement Income Strategy #1: The 4% Rule

The 4% Rule is the most recognizable principle in retirement planning. I Googled “4% rule” and got more than 10 billion results.

Bengen’s recommendations, based on data available when he published, have proven remarkably durable.

Bengen devised safe withdrawal rates (SWR), meaning how much a retiree can withdraw from assets each year and be confident of not running out of money.

Horrible periods for investors are not uncommon. Bengen’s data included 1973-1974, when the stock market crashed by 37% while inflation rose 22% simultaneously. More recently, retirees who lost 50% in the stock market in 2008-09 were catastrophically affected if they were just about to retire.

Bengen found that, for a 50-50 portfolio (50% stocks, 50% bonds), a 4% initial withdrawal rate, raised 3% for inflation each year, had always been safe for at least 35 years, and most of his historical portfolios actually lasted 50 years.

Bengen also suggested that advisors try to persuade their clients to own more stocks than bonds, “as close to 75 percent as possible.” That went against the still-common view that older people should decrease stocks and increase bonds as they age.

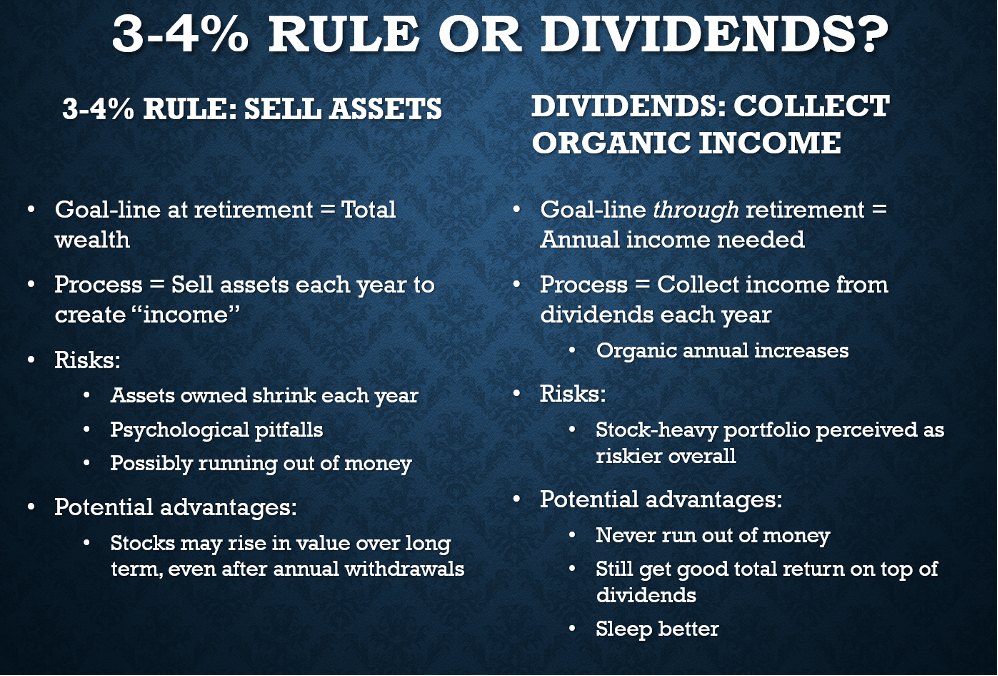

Let’s summarize the 4% Rule:

The 4% Rule is a withdrawal or decumulation strategy: It depends on selling assets to convert capital into “income.”

4% is a benchmark representing a safe withdrawal rate.

4% refers to the first year’s withdrawal. Withdrawals in subsequent years are increased for inflation at 3% each year.

Here’s a simple example. If you have $1 million in savings at the beginning of retirement, you can withdraw 4% ($40,000) to fund Year 1. In Year 2, you would augment that by 3% (to $41,200), and so on through Year 30.

Bengen’s work has been updated countless times with newer and broader data, including by Bengen himself. In the years since his original work, interest rates have gone up and down, stocks have waxed and waned, and the costs of advisor and fund fees have been added for realism.

The later studies have produced inconsistent results, but they are often close to the 4% original. At the extremes, I have seen studies that put the “new” SWR as low as 1.7% and as high as 5% or more.

The initial withdrawal percentage is important, because it impacts the amount that the individual must have saved to achieve their income goal in Year 1 of retirement.

If the SWR is 3% instead of 4%, the $1 million needed to generate $40,000 jumps to $1.3 million. At 1.7%, it jumps to $2.4 million.

The following chart is a typical presentation of the likelihood of 30-year success rates for withdrawing from retirement portfolios without running out of money.

As a retiree, you want to be in a green area, where you can have a high degree of confidence that your withdrawal plan will be safe – that you will not run out of money.

From the table, that puts your maximum safe withdrawal rate in the 3-4% range. Lower withdrawals always improve portfolio safety.

Source: J.P. Morgan Asset Management

The final topic for the 4% Rule is sequence of returns risk.

Even though the overall direction of the stock market has been upwards for decades, the year-to-year path is a roller coaster. Some years are really bad, while others are excellent.

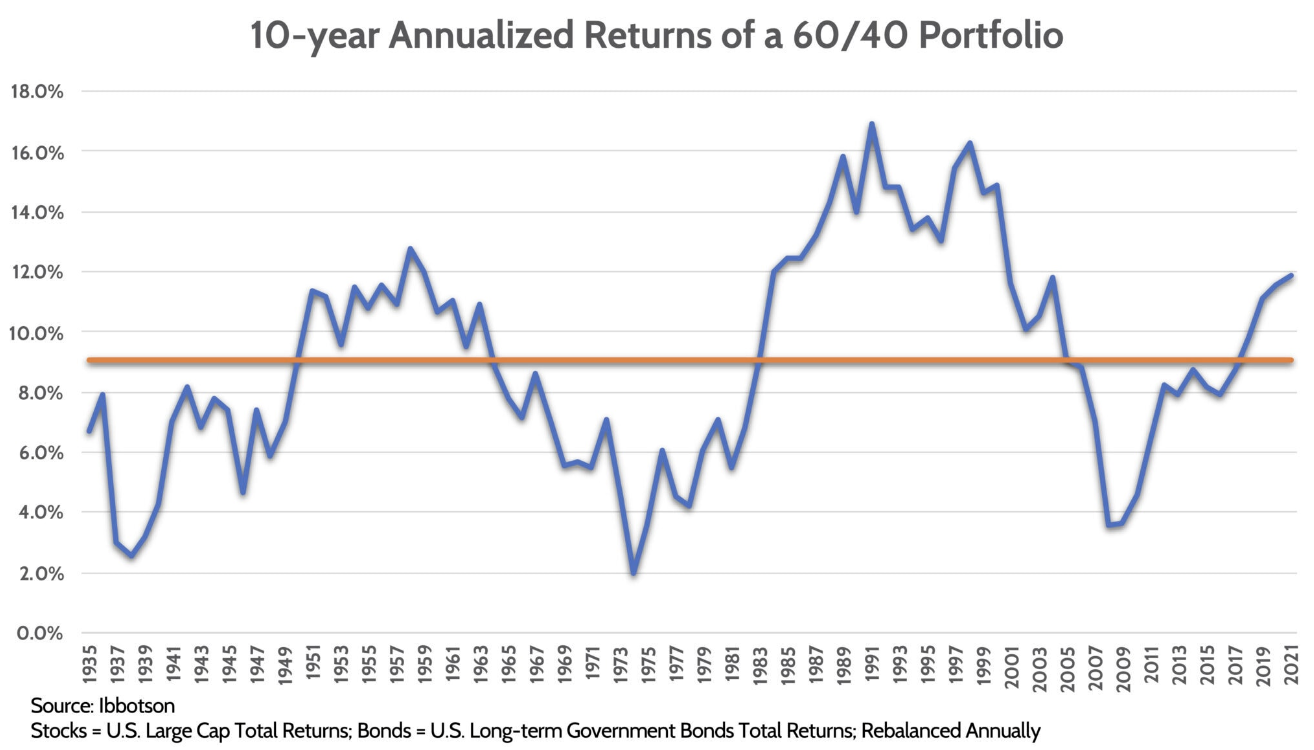

The following chart uses a 60-40 portfolio, 10-year averages, and rebalancing to smooth out the annual variances, but it is still a roller coaster. The gold line through the middle is the overall average from 1935 through 2021 (which means that the data started in 1926, so it includes the Great Depression).

Source: Financial Design Studio

The volatility of annual returns is important, because under the 4% Rule, your annual withdrawals go relentlessly up.

Poor returns in the first few years of retirement, amplified by rising withdrawals, may create a deficit that cannot be recovered by higher returns later.

A withdrawal strategy means that you may find yourself in one of the worst situations in investing: Being a forced seller when asset values are declining.

And even short-run bad returns can cause psychological problems. Besides sleepless nights, a bad year or two may cause the investor to panic and move more money into “safer” bonds.

But over the long haul, a higher percentage in “riskier” stocks generally enhances portfolio life. Moving into bonds too early may be self-defeating, even if it provides emotional relief in the moment.

For the rest of this article, I will posit that a 3-4% initial withdrawal rate, augmented 3% each year for inflation, is a decent benchmark for a safe withdrawal rate from most balanced portfolios.

So in one corner, we have the 3-4% Rule.

Source: Author, using Bing Chat

Living Off Dividends in Retirement

In the other corner is a dividend stock retirement strategy.

Whereas the success of the 3-4% Rule depends on total returns and the sheer luck of return sequence, dividend strategies depend on reliable and growing dividend income.

Growing income streams come from stocks with consistently rising dividends, known as Dividend Growth (DG) stocks.

A strategy based on using dividends for retirement means that your retirement day is not a finish line by which you must reach a certain level of wealth to sustain withdrawals in retirement.

Rather, retirement just becomes an inflection point in how dividends are deployed. Instead of being reinvested to build the annual income stream leading up to retirement, the dividends can be the income itself.

Many dividend investors amass considerable wealth anyway, because they carefully select DG stocks and funds of high-quality companies.

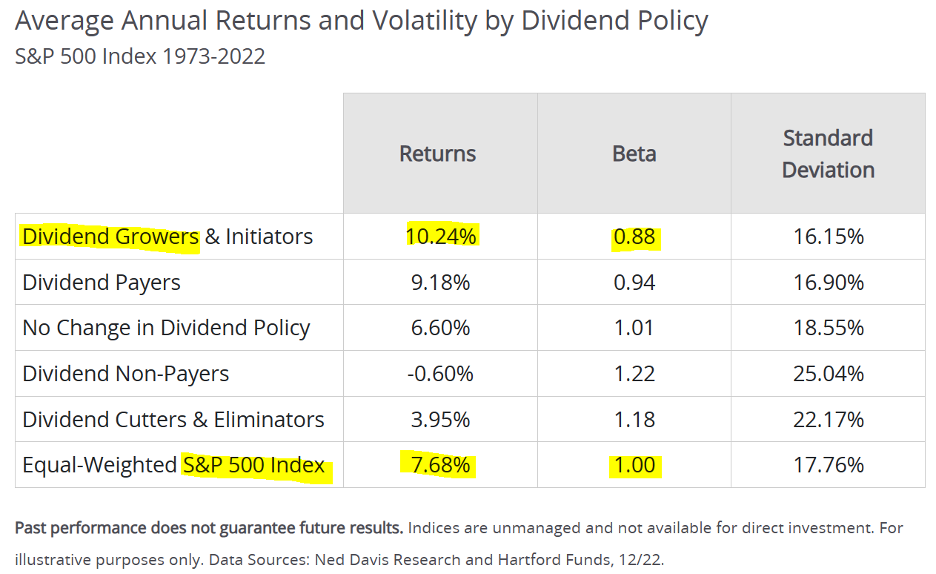

Studies such as the following from Hartford Funds show that dividend growth stocks have the best total returns, and lowest volatility, of all categories of stock when sorted by dividend production.

Source: Hartford Funds

High-quality DG stocks not only have more stable prices, but they usually keep raising their dividends even when the market as a whole is falling. Our Dividend Safety Scores™ help you find such stocks.

My wife’s and my DG portfolios have delivered annual income increases every year since 2010, when we completed our switch to DG investing. We are so confident in the approach that our nest egg is about 85% stocks. The rest are liquid assets. We own no bonds.

Consider the equilibrium between DG investing’s typical 3-4% current yield and the 3-4% Rule itself. They are the same number!

In other words, if you have saved $1,000,000 for retirement, then withdrawing 3-4% of it in Year 1 delivers the same income as a 3-4% yield: $30,000 to $40,000.

And if your assets are dividend growers, the annual inflation adjustment embedded in the 3-4% Rule will usually happen automatically, often with money left over.

In my wife’s and my portfolios, the past 5-year organic dividend growth rate has been 7% per year. I know this from the summary on Simply Safe Dividends’ Portfolio Tracker, which I use to track our portfolios.

Our overall yield is 3.5%, right in the heart of the 3-4% Rule.

Comparing the Two Retirement Funding Methods

In a withdrawal scheme, you must liquidate assets to fund retirement. But if you use growing dividends for retirement, you may not need to sell any assets, ever.

Not needing to sell to generate income can be important.

You remove Mr. Market’s ADHD behavior from your retirement income.

The sequence of market returns does not matter much.

You don’t have to sell more assets each year to cover the annual inflation adjustment. Your income rises automatically.

You will not get caught as a forced seller when markets are tanking.

In the literature, you will see unequivocal statements that one can create their own dividend simply by selling a few shares.

That notion is simplistic and false. The fact is, when you sell assets, they are gone. They won’t be around to help you next year or ever.

Obviously, those who state that selling a few shares is the same as receiving a dividend are presuming that the dollar value of the remaining shares will go up enough to recover the dollar value of the shares that were sold.

But that does not describe the real world. Look again at the roller-coaster chart earlier. Share prices do not increase every year.

Conclusion

Everyone must decide for themselves how they want to finance retirement. There is no single correct answer for every retiree.

I have a clear favorite, which is to build stock-heavy portfolios that generate growing income organically.

My comfort with such portfolios comes from (1) caring mostly about the income they provide rather than prices, and (2) appreciating the predictability, reliability, and natural growth of that income.

If you have a portfolio of DG stocks that yields 3-4% and whose income rises 5% or so every year due to dividend increases, you have the 3-4% Rule covered right there.

And you don’t need to sell anything. You will never outlive your savings.

Source: Author

In the real world, most retirees end up with a hybrid approach. They get some income from selling stuff, some from dividends and interest, and some from other sources.

Even if you do not own enough DG stocks to provide all the income that you need or want, every dollar you generate from dividend stocks is one less dollar that you will need to generate by selling assets.

One last thought: Everyone adapts to their financial reality as they approach retirement. Retirement-funding strategies become dynamic and flexible.

Tools in the toolkit include:

Delay retirement for a year or two, not only to gather more assets, but also to reduce the number of years that your investments must support you.

Cut back on spending in the last few years before retirement in order to save more.

Pay off your mortgage and all long-term debt.

Adjust investments from growth-oriented to income-oriented.

Maintain an emergency/fun fund of assets not subject to market risk (savings account, money-market fund, certificates of deposit).

Get a part-time job or gig work in retirement.

Do not mechanically raise withdrawals each year. Instead, adjust them according to actual inflation, spending, and investment performance.

Strive for good health to keep medical costs down.

We all end up making things work one way or another. You will too.