20 Best Recession-Proof Dividend Stocks for a 2025 Downturn

The best recession-proof stocks can withstand persistent inflation, high interest rates, trade wars, and the potential popping of a bubble in AI stocks that could tip the economy into a downturn as soon as 2025.

The top dividend stocks for a recession have pricing power to pass through rising costs, low debt to protect from higher interest rates, and essential products that generate steady cash flow in all types of environments.

We analyzed 20 recession-proof stocks that possess these traits and have:

A dividend yield near 3% or higher

Paid uninterrupted dividends for at least 20 years (including 7 stocks with 100-plus-year streaks)

Outperformed the S&P 500 during the 2007-09 financial crisis

The recession-resistant stocks below are ordered by how many consecutive years they have maintained or increased their dividends, starting with the shortest streaks.

2007-09 Recession Return: -38% vs. -55% for S&P 500 Uninterrupted Dividend Streak: 41 years

Verizon (VZ) was formed in 2000 when telecom giants Bell Atlantic and GTE merged, but its predecessors' roots trace back to the late 19th century when Alexander Graham Bell patented the telephone and founded AT&T.

As one of the largest wireless providers in the U.S., Verizon operates in an industry that is critical to modern life. Whether during economic booms or downturns, consumers and businesses continue relying on mobile and internet connectivity. This makes Verizon's services highly resilient to recessions, providing the company with steady revenues in all environments.

What reinforces Verizon's defensive profile is its recurring, subscription-based business model. With over 90% of its profits tied to wireless services—used daily by tens of millions of customers—Verizon enjoys a cash flow stream that is not only predictable but also difficult to disrupt. Even when budgets tighten, most households prioritize their mobile service, given how vital smartphones have become for work, school, and social life.

In fact, Verizon's sales edged lower by just 1% during the 2008 financial crisis, and its stock outperformed the S&P 500's loss of 55% by nearly 20%.

Verizon's dividend continued rising during that period, too. The company and its predecessors have paid uninterrupted dividends since Bell Atlantic's formation in 1984 and should be able to continue that streak thanks to Verizon's resilient cash flow, BBB+ credit rating, and healthy payout ratio below 60%.

Source: Simply Safe Dividends

2007-09 Recession Return: -18% vs. -55% for S&P 500 Uninterrupted Dividend Streak: 23 years

With roots tracing back to 1896, WEC Energy (WEC) has grown through a handful of major acquisitions to become one of the nation’s biggest utilities, with electric and natural gas activities in Wisconsin, Illinois, Michigan, and Minnesota.

Regulated utilities are among the most dependable businesses investors can own during a recession. This reflects the lack of competition in their service territories, the reasonable returns on capital investments they are allowed to earn by regulators, and the non-discretionary nature of their services.

WEC's predictability is especially impressive as it is the only regulated utility to beat guidance every year since 2004.

The company's track record reflects management's conservatism running the business, as well as Wisconsin's solid economy and the supportive relationships WEC has maintained with state regulators.

Looking ahead, management expects earnings to grow by 6% to 7% per year as WEC's rate base and regulated renewables continue expanding. This should fuel a similar pace of dividend growth, giving WEC one of best combinations of dividend income and growth in the sector.

Coupled with a healthy A- credit rating, WEC Energy appears poised to weather a recession and come out stronger on the other side.

Source: Simply Safe Dividends

Sector: Energy – Oil and Gas Storage and Transportation Dividend Yield: 7.1%

2007-09Recession Return: -37% vs -55% for S&P 500

Uninterrupted Dividend Streak: 26 years

Enterprise Products Partners (EPD), a master limited partnership, has paid uninterrupted distributions since going public in 1998.

With roots tracing back to 1968, Enterprise has grown to become one of the largest midstream service providers in America with a network of assets connected to nearly every major U.S. shale basin and throughout the Gulf Coast.

Enterprise's pipelines, storage facilities, and other infrastructure help raw fossil fuels get from a producer's wellhead to the end consumer in a ready-to-use state, generating fees at almost each step of the way.

Despite handling a mix of crude oil, natural gas, petrochemicals, natural gas liquids, the firm's cash flow has minimal direct exposure to commodity prices. Instead, Enterprise enjoys stability from long-term, fixed-fee contracts with minimum volume commitments and annual rate escalators to offset inflation.

Coupled with a BBB+ credit rating and conservative payout ratio that supports a self-funding business model (i.e. expansion projects funded by cash flow and debt rather than equity), Enterprise represents one of the lower-risk choices in the midstream energy space.

The partnership has survived past recessions with its dividend intact and even outperformed during the 2008 financial crisis, losing 37% compared to the S&P 500's -55% total return.

Source: Simply Safe Dividends

Recession-Proof Stock #17: Lockheed Martin

Sector: Industrials – Aerospace and Defense Dividend Yield: 2.8%

2007-09Recession Return: -46% vs. -55% for S&P 500

Uninterrupted Dividend Streak: 32 years

Lockheed Martin (LMT) commenced operations in 1912 during the dawn of flight and is now the world's largest defense contractor and supplier of fighter aircraft.

Most of Lockheed's business is with the U.S. government and spans combat aircraft such as the F-35 joint strike fighter, missile defense systems, military helicopters, and satellite systems.

Military might has always played a major role in human affairs, making the need to defend territory and wield power a timeless, expensive problem for governments.

Lockheed's scale and time-tested reputation make the firm an ideal partner for the U.S. government, resulting in a large backlog of work that provides multiyear revenue visibility.

While defense budgets ebb and flow, a high baseline of spending and diversified mix of projects help Lockheed generate a consistent level of profits detached from the vagaries of the economic cycle.

The business enjoys protection from inflation as well, with 40% of revenue tied to cost-plus contracts that pass higher costs through to the end customer.

The other 60% of sales have fixed-price contracts, but Lockheed requires its suppliers to enter fixed-price arrangements over the entire duration of a project, pushing inflation risk lower down in the supply chain.

With relatively low debt levels and an A- credit rating, Lockheed is insulated from rising interest rates, too. Along with a conservative payout ratio near 50%, Lockheed appears primed to continue growing its dividend and remain a recession-proof stock for income.

Source: Simply Safe Dividends

Recession-Proof Stock #16: Public Storage

Sector: Real Estate –Specialized REITs Dividend Yield: 4.0%

2007-09Recession Return: -38% vs. -55% for S&P 500 Uninterrupted Dividend Streak: 44 years

Public Storage (PSA) went into business in 1972 and is the largest U.S. self-storage REIT with over 3,000 facilities serving more than 1 million customers.

Self-storage has proven to be a sticky business since moving is such a headache.

In fact, the self-storage industry’s free cash flow per share fell by less than 5% during the financial crisis, according to Bank of America Merrill Lynch.

While consumers spend less during recessions, they still need a place to store their stuff. As long as people continue experiencing major life events such as an unexpected move or divorce, there will be demand for self-storage warehouses.

This results in a stable and predictable industry with a slow pace of change – all good things for dividend growth investors worried about the next economic slowdown.

Public Storage is particularly advantaged since it is much larger than its rivals and locates many of its facilities in close proximity to each other.

This allows the REIT to leverage its costs (property management, maintenance, and advertising) across the company to achieve better profitability during the good times and the bad.

As population density increases, flexible work encourages consumers to free up more space at home, and downsizing activity rises alongside an aging population, demand for storage properties should rise over the long term, providing a nice tailwind for Public Storage.

Public Storage has paid uninterrupted quarterly dividends since 1981 and last raised its dividend by 50% in 2023 following a nearly 7-year freeze, giving it a yield that makes the REIT an interesting high dividend stock.

The company also has a conservative balance sheet, earning it an A credit rating, and should remain a cash cow given the lack of capital required to maintain this business.

Coupled with ownership of real property and month-to-month leases with prices that are more flexible to adjust, Public Storage represents a solid inflation hedge in addition to a quality recession-proof stock to consider.

Source: Simply Safe Dividends

Read More:Guide to Investing in REITs for Income

Consumers cut back on discretionary spending to save money during economic downturns, so restaurants are usually not the best dividend stocks for a recession. Higher labor and food costs further add to the industry's challenges in an inflationary environment.

But McDonald's (MCD) is different. Almost all of the fast-food chain's restaurants are franchised, meaning the stores are owned and operated by independent business owners.

Under a typical franchise arrangement, McDonald's owns the land and building while the franchisee pays for the equipment, signs, seating, décor, labor, food, and other supplies.

Franchisees generate the bulk of McDonald's profits by paying the company high-margin rent and royalties based upon a percent of sales.

This model helps shield McDonald's from a restaurant's operating costs, and the firm's underlying real estate ownership serves as another inflation hedge.

"We (McDonald's) are not technically in the food business. We are in the real estate business. The only reason we sell fifteen-cent hamburgers is that they are the greatest producer of revenue, from which our tenants can pay us our rent."

– Harry Sonneborn, McDonald's former president and chief executive

That said, McDonald's has historically supported franchisees by co-investing to improve restaurants. This has helped the firm maintain consistency between locations with fast service, convenient ordering options, hot food, and predictable quality.

Along with an affordable menu, generous advertising budget, and BBB+ credit rating, McDonald's should remain a durable cash cow with a safe dividend that has been paid without interruption since 1976.

Source: Simply Safe Dividends

2007-09Recession Return: -26% vs. -55% for S&P 500

UninterruptedDividend Streak: 50 years

Founded in 1823 as the New York Gas Light company, utility Consolidated Edison (ED) provides energy for the 10 million people who live in and around New York City. Almost all of the firm's earnings are generated from regulated activities involving the transmission and distribution of electric and gas power.

The company's focus on regulated utilities, combined with the industry’s slow pace of change and recession-resistant services, has resulted in a predictable earnings stream enabling Con Edison to increase its dividend every year since 1975, the longest streak of any S&P 500 utility company.

Con Edison's dividend has grown at a low single-digit pace over the past decade, reflecting some of New York City's challenges.

While Manhattan needs reliable power, the city has experienced several years of population losses as residents seek cheaper options. Regulators have also been less agreeable to raising electricity and gas rates given the city's high cost of living and already pricey power.

Still, Con Edison has lots of work to maintain New City's infrastructure, which requires substantial investment being located in such a dense, congested area.

From strengthening the grid to participating in the clean energy transition with efficiency projects and electric vehicle charging stations, A- rated Con Edison should continue to enjoy predictable earnings and pay a secure dividend in all manner of economic environments.

Source: Simply Safe Dividends

Recession-Proof Stock #13: Bristol-Myers Squibb

Sector: Healthcare – Pharmaceuticals

Dividend Yield: 5.0%

2007-09Recession Return: -32% vs. -55% for S&P 500

UninterruptedDividend Streak: 54 years

Bristol-Myers Squibb (BMY) traces its roots back to 1858 and is one of the world's largest biopharmaceutical businesses with more than $40 billion in annual sales.

Bristol is focused almost exclusively on branded drugs, an industry with high barriers to entry and excellent profitability. Major pharma players invest billions of dollars and years of time in research and development to commercialize breakthrough drugs.

While the success rate is low, a commercialized drug can generate billions of dollars in monopolistic profits that are protected for many years thanks to the intellectual property owned by the manufacturer.

Medications are also recession-resistant products because consumers need them regardless of how the economy is doing. This helped Bristol's stock only fall 32% during the 2007-09 financial crisis while the S&P lost over 50%.

Coupled with Bristol's A credit rating, which supports the firm's ability to make acquisitions to keep its drug pipeline full, the biopharma giant should remain a reliable income payer in almost any environment.

Source: Simply Safe Dividends

Recession-Proof Stock #12: Realty Income

Sector: Real Estate – Retail REITs Dividend Yield: 5.7%

2007-09Recession Return: -43% vs. -55% for S&P 500

UninterruptedDividend Streak: 56 years

Realty Income (O) is among the best monthly dividend stocks with a track record of paying uninterrupted dividends since its founding in 1969.

The REIT owns over 15,000 properties focused on freestanding, single-tenant retail. Realty's properties are leased to more than 1,000 tenants operating in around 90 different industries, creating a diversified rental income stream.

The firm's long-term leases provide predictable cash flow during downturns and insulate Realty from inflation. As a triple net lease REIT, Realty's clients cover taxes, insurance, and other operating expenses. As prices rise, clients pass the incremental cost burden on to their customers or suppliers.

Realty also generates most of its rent from recession-resistant tenants that have a service, non-discretionary, or low price point element to their business. Nearly half of the REIT's tenants have investment-grade credit ratings, too.

The quality of Realty's properties and underwriting is reflected in the company's occupancy rate, which has never dipped below 96%, even during the 2007-09 financial crisis and 2020 pandemic.

Along with an A- credit rating, which provides some fundamental protection against rising interest rates and tighter financial conditions, Realty Income should remain one of the most reliable dividend stocks to ride out a recession.

Source: Simply Safe Dividends

2007-09Recession Return: -35% vs. -55% for S&P 500

UninterruptedDividend Streak: 60 years

With roots tracing back to 1898, PepsiCo (PEP) is one of the oldest and largest drink and snack makers in the world.

The firm's balanced portfolio includes over 20 iconic brands that generate more than $1 billion each in annual sales, including Lay's and Doritos chips, Gatorade sports drinks, Quaker oatmeal, and Mountain Dew soda.

PepsiCo's products are recession-resistant since people need to eat and drink no matter how the economy performs. In fact, the company's sales dipped just 0.5% during the 2007-09 Great Recession, and revenue surged during the 2020 pandemic as at-home eating boomed.

Persistent inflation does create challenges since value-conscious consumers are more likely to trade down and the cost raw materials increases. But the firm's strong brands and dominant shelf space with retailers has helped it maintain solid margins.

PepsiCo's profits are insulated from higher interest rates as well since the company maintains low leverage and earns an A+ credit rating.

Overall, PepsiCo is one of the best recession-proof stocks in the market and appears positioned to extend its streak of paying higher dividends every year since 1971 regardless of the economic environment.

Source: Simply Safe Dividends

2007-09Recession Return: -46% vs. -55% for S&P 500

UninterruptedDividend Streak: 60 years

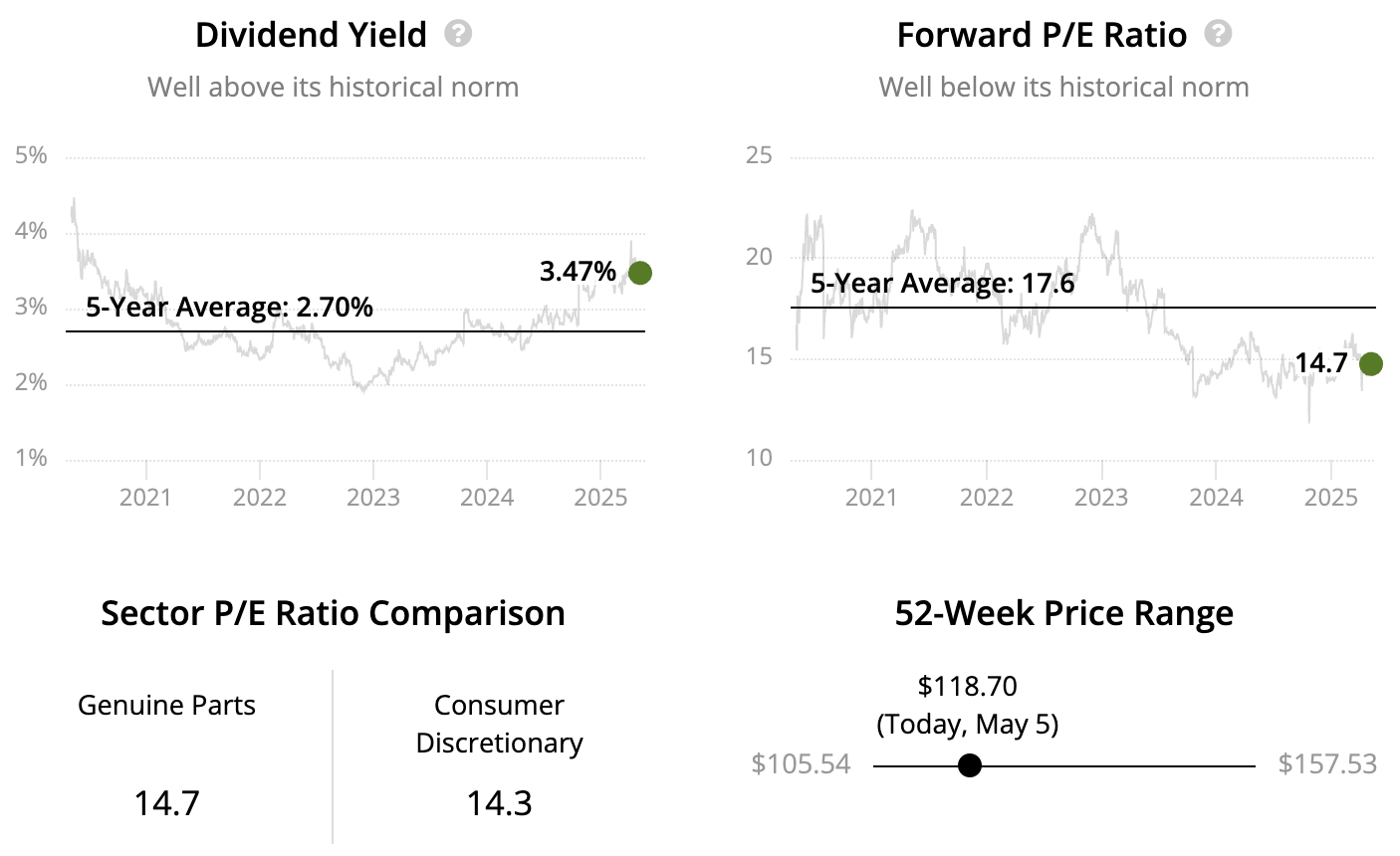

Founded in 1928, Genuine Parts (GPC) owns the largest global automotive replacement parts network and has a sizable industrial parts distribution business.

On the automotive side, which generates the majority of the company's sales, Genuine Parts markets its products through a network of distribution centers and retail outlets, including thousands of NAPA and Alliance auto parts stores.

The automotive aftermarket business does well even in challenging times because people still have a need to repair their aging vehicles as they break down over time.

High used car prices and limited availability of new vehicles due to pandemic-related supply chain disruptions further support maintenance demand for existing cars.

Auto and industrial parts are somewhat price inelastic, too. Customers value product reliability and delivery convenience more than getting the absolute lowest price. This is partially because professional clients tend to pass on higher prices to their customers, helping Genuine Parts maintain stable margins.

Overall, Genuine Parts operates in slow-changing industries and maintains leading market positions because of its extensive distribution networks (just-in-time delivery), wide range of products, brand recognition, and long-standing customer relationships.

Combined with a conservative payout ratio target near 50%, a BBB credit rating, and solid cash flow generation even during economic downturns, Genuine Parts should extend its streak of higher annual dividends since 1957 and remain one of the best dividend stocks for a recession.

Source: Simply Safe Dividends

2007-09Recession Return: -34% vs. -55% for S&P 500

UninterruptedDividend Streak: 90 years

Kimberly-Clark (KMB) has grown from humble roots as a simple paper mill founded in 1872 to a global leader in tissue and hygiene products, including five billion-dollar brands: Huggies, Kleenex, Cottonelle, Scott, and Kotex.

Demand for Kimberly-Clark's products remains fairly stable during recessions because there is not much discretionary use in categories such as diapers and toilet paper. While more consumers trade down when times get tough, Kimberly-Clark plays across all pricing tiers with value and premium offerings.

These qualities helped the firm's sales slip only 4% during the 2007-09 financial crisis, and management had confidence to continue raising the dividend as Kimberly-Clark has done every year since 1973.

Inflation does impact Kimberly-Clark's costs with key raw materials such as nonwoven fabrics and pulp facing upward pressure. However, the company has offset a significant amount of inflation with price increases and cost savings actions.

With a strong balance sheet, A credit rating, and portfolio of recession-resistant products, Kimberly-Clark should remain a durable income investment in all manner of environments.

Source: Simply Safe Dividends

Recession-Proof Stock #8: Duke Energy

Sector: Utilities –Diversified Utilities Dividend Yield: 3.5% 2007-09 Recession Return: -34% vs. -55% for S&P 500 Uninterrupted Dividend Streak: 97 years

Duke Energy (DUK) is one of the largest regulated utilities in America with operations spanning seven states across the Southeast and Midwest.

Electric utilities generate most of the firm's profits, with gas utilities, infrastructure, and renewables driving the remainder. Over 90% of cash flow is from regulated activities.

Due to the steep cost of infrastructure required to serve a limited pool of customers, many utility companies are essentially government regulated monopolies in the regions where they operate. Duke's utilities are no exception, acting as sole suppliers in most of their service territories.

However, the monopoly status of regulated utilities has a downside: the price they can charge for their services is controlled by state commissions to ensure rates remain reasonable for consumers.

Fortunately, Duke's utilities are concentrated in areas that have historically constructive regulation. Weighted by rate base, Duke operates in the top 20% of jurisdictions in the country, according to estimates made by activist investor Elliott Management.

Coupled with Duke's BBB+ credit rating, the firm should continue growing its earnings and defending its track record of paying safe dividends since 1927.

The other attribute conservative income investors might appreciate is the stock's low volatility. During the financial crisis, DUK's shares slumped just 34% while the S&P 500 lost 55%.

Overall, Duke's essential services, stable cash flow, and strong balance sheet make the stock a good choice for low-risk income investors during recessions and bear markets.

Source: Simply Safe Dividends

2007-09Recession Return: -31% vs. -55% for S&P 500

UninterruptedDividend Streak: 105 years

Coca-Cola (KO) began in 1886 when a pharmacist in Atlanta created a new "delicious and refreshing" drink. Today, the iconic beverage maker serves nearly 2 billion customers daily from its portfolio of over 200 drinks sold worldwide.

Beverage companies need to cultivate strong brands to drive high sales volumes of their low-priced products. Repeat business from consumers generates the steady cash flow streams that investors expect from this defensive sector.

Retailers, in turn, need to keep shelves stocked with brands that customers expect to find. For beverage manufacturers with in-demand products, like Coca-Cola, the more robust and diverse their portfolios, the more leverage they have when negotiating pricing, shelf space, and in-store promotions.

Coke's strong positioning, built on the back of tremendous advertising spending and distribution network investments, has historically helped the company raise prices at a pace similar to inflation, protecting margins.

With about 80% of the firm's sales volumes coming from outside the U.S., Coca-Cola's diversified footprint provides insulation from unfavorable economic environments in any single region, too.

Reflecting these defensive qualities, the beverage giant's sales only fell 5% during the 2007-09 Great Recession, and KO shares outperformed the S&P 500's -55% return with a loss of 31%.

Backed by an A+ credit rating and annual dividend growth streak dating back to 1963, Coca-Cola is one of the safest consumer staple stocks investors can own if the economy hits a downturn and brings on a prolonged bear market.

Source: Simply Safe Dividends

2007-09Recession Return: -27% vs. -55% for S&P 500

UninterruptedDividend Streak: 109 years

Formed in 1886 as a manufacturer of sterile surgical supplies following the Civil War, Johnson & Johnson (JNJ) is now one of the world's largest pharma companies and makers of medical devices.

Consumers dealing with arthritis, infectious diseases, mood disorders, cancer, diabetes, and other ailments need to continue receiving treatment during recessions, resulting in stable demand for J&J's branded medicines.

While drugs operate in boom-and-bust cycles due to the nature of their finite patent protection, J&J's portfolio is not overly concentrated in any single drug or treatment area. This reduces the firm's earnings volatility.

Demand for medical devices is more sensitive to recessions since elective surgeries can be deferred, but a healthy baseline of demand for many types of procedures helps stabilize J&J's performance.

These resilient cash flow sources and management's conservative use of debt have earned the firm a pristine AAA credit rating and enabled the firm to raise its dividend every year since 1963. Johnson & Johnson should stay relevant for decades to come regardless of recessions and bear markets.

Source: Simply Safe Dividends

Recession-Proof Stock #5: Chevron

Sector: Energy – Integrated Oil and Gas

Dividend Yield: 5.1%

2007-09Recession Return: -34% vs. -55% for S&P 500

UninterruptedDividend Streak: 113 years

A recession triggered by inflation could result in energy producers fairing relatively well as supply constraints keep oil and gas prices high. Chevron (CVX), one of the largest oil companies in the world, could perform well in an environment with sticky inflation.

But even if oil prices come down as a contracting economy better balances supply and demand, Chevron has an excellent track record of paying stable or higher dividends each year since 1912.

This resilient performance partly reflects Chevron's scale, capital efficiency, and vast resource base. Management believes the firm can cover its capital spending program and dividend with an oil price as low as $50 per barrel, providing a healthy margin of safety.

Oil prices have fallen below this threshold and might in the next downturn. But Chevron maintains ample balance sheet capacity so it can borrow debt to plug its cash flow deficit and defend its dividend until oil prices recover.

With Chevron's dividend costing about $12 billion annually and the firm able to reduce short-cycle capital during periods of extreme stress, we think Chevron's dividend could survive multiple years of oil prices as low as $30 per barrel.

Overall, Chevron should remain a cash cow paying a generous dividend even if the price of oil falls. For investors who believe fossil fuels will remain a core component of the world's energy mix, Chevron represents one of the best recession-proof stocks in the industry.

Source: Simply Safe Dividends

Recession-Proof Stock #4: General Mills

Sector: Consumer Staples – Packaged Foods and Meats

Dividend Yield: 4.4%

2007-09Recession Return: -12% vs. -55% for S&P 500

UninterruptedDividend Streak: 126 years

General Mills (GIS) has been in business since 1866 but did not focus entirely on consumer foods until 1995. Today, General Mills sells a wide variety of branded packaged meals, cereals, snacks, baking products, pet food, and more. No category tops 25% of sales.

The firm's core brands have been on the shelves for many decades, supported by hefty spending on advertising and product innovation. These investments have helped General Mills' foods reach over 95% of U.S. households and dominate their respective categories.

Consumers expect to find these brands when they shop, giving General Mills pricing power with retailers to combat inflation.

Demand generally remains stable during recessions as well because people stop eating away from home as much to save money. In fact, the firm's sales were flat during the 2007-09 financial crisis.

Ultimately, General Mills' large marketing budget, shelf space, distribution relationships, product diversity, entrenched brands, and BBB credit rating should help the business stay relevant and continue its streak of paying uninterrupted dividends since 1898.

Source: Simply Safe Dividends

Recession-Proof Stock #3: Colgate

Sector: Consumer Staples – Household Products

Dividend Yield: 2.3%

2007-09Recession Return: -22% vs. -55% for S&P 500

UninterruptedDividend Streak: 130 years

Founded in 1806 as a starch, soap, and candle business, Colgate (CL) is nowone of the world’s largest consumer products conglomerates. The company's brands span everything from toothpaste and mouthwash to shower gels, household cleaners, and specialty pet food.

During recessions, people still brush their teeth, take showers, wash their hands, and clean their homes. This limited Colgate's revenue decline during the 2007-09 financial crisis to less than 3%, helping the stock fall by less than half of the S&P 500's decline.

That said, more consumers still look to save money during economic downturns by trading down to cheaper products. Colgate mitigates this risk by having products available at all price points and in different package sizes to meet a wide variety of consumer needs.

Compared to other consumer product categories, oral care also faces less competition from lower-priced private label offerings. This reflects the more scientific nature of products such as toothpaste, as well as the importance of endorsements from dentists for Colgate's brands.

With stable cash flow, significant exposure to emerging markets for long-term growth, and a strong A+ credit rating, Colgate is one of the best dividend stocks during recessions and appears poised to extend its streak of paying uninterrupted dividends for more than 125 years.

Source: Simply Safe Dividends

Recession-Proof Stock #2: Procter & Gamble

Sector: Consumer Staples – Household Products

Dividend Yield: 2.7%

2007-09Recession Return: -36% vs -55% for S&P 500

UninterruptedDividend Streak: 134 years

Since its formation in 1837, Procter & Gamble (PG) has grown into one of the world’s largest manufacturers of laundry detergents, baby wipes, diapers, paper towels, cleaning products, shampoos, deodorants, toothpastes, and other consumer goods.

Following decades of high spending on advertising and innovation, most of the company's 20-plus billion-dollar brands boast No. 1 or No. 2 positions in their categories. Consumers expect to find these brands when they shop.

This strengthens P&G's bargaining power with retailers, helping the consumer products giant increase prices to offset rising costs in an inflationary environment. Higher interest rates pose little threat to the firm's earnings as well since P&G maintains low leverage and has a strong AA- credit rating.

While some consumers trade down to cheaper offerings during recessions, overall demand for most of the staples P&G sells remains steady since these products are used every day. The firm has also created different value tiers and pack sizes to meet shifting consumer priorities.

With management continuing to invest around $10 billion annually on R&D and advertising to maintain the company's entrenched market position, P&G should remain a recession-proof stock with dividends investors can rely on.

Source: Simply Safe Dividends

Recession-Proof Stock #1: Exxon Mobil

Sector: Energy – Integrated Oil and Gas

Dividend Yield: 3.8%

2007-09Recession Return: -28% vs. -55% for S&P 500

UninterruptedDividend Streak: 143 years

Exxon Mobil (XOM) and its predecessors have paid uninterrupted dividends since 1882, marking the longest streak of any recession-proof stock on our list.

The resilience of the oil major's dividend across dozens of recessions and energy price crashes reflects management's conservative approach to running the business, beginning with Exxon's integrated business model.

The energy behemoth controls all aspects of the fossil fuel business, from exploration and production to transportation, refining, and retail gasoline sales.

Falling oil prices reduce earnings in Exxon's upstream production segment, but the firm's refining and petrochemical businesses benefit from lower input costs. This diversification helps keep Exxon profitable in all manner of commodity price environments.

Exxon's relatively low leverage and AA- credit rating provide further insulation. When oil falls below around $40 per barrel, the level Exxon needs to cover its dividend and capital spending program, the firm can borrow debt to plug its cash flow deficit until the pricing environment improves.

We estimate that Exxon's balance sheet capacity would allow the the company to defend its dividend for at least a couple of years if oil prices averaged as low as $30 per barrel.

While oil demand falls during recessions, prices may not fall as far in the next downturn if persistent inflation caused by supply constraints keeps energy prices high.

Even if the price of oil crashes like it did in 2008, investors can take some comfort in knowing that XOM shares only lost 28% during the financial crisis compared to the S&P 500's -55% slump.

For income investors who share our belief that fossil fuels will remain a core component of the world's energy mix, Exxon seems like a good bet for reliable dividends whenever the next recession arrives.

Source: Simply Safe Dividends

Closing Thoughts on Recession-Proof Dividend Stocks

The best dividend stocks for recessions possess defensive qualities that appeal to conservative investors seeking safe income and capital preservation.

No one can predict with any consistency when the next downturn will hit or which industries will face the most pain. Maintaining a diversified portfolio can help, as can holding some of the of the companies we highlighted.

By the way, many of the people interested in recession-resistant stocks are retirees looking to generate safe income from dividend-paying stocks.

If that sounds like you, you might like to try our online product, which lets you track your portfolio’s income, dividend safety, and more.

You can learn more about our suite of portfolio tools and research for dividend investors by clicking here. Thanks for reading!