However, there are a number of pros and cons of preferred stock, including important differences between preferred shares and common dividend stocks and bonds.

Let’s take a closer look at preferred shares to help you determine if preferred stock could be an appropriate part of your conservative dividend portfolio.

What are Preferred Stocks?

Debt and equity markets exist to provide companies with access to capital to help them meet their financial needs. Preferred shares are a form of equity that makes up a company's "capital stack."

The capital stack is simply the priority by which debt and equity investors have claim over a company's assets. The order of priority, from highest to lowest priority, looks like this for all companies:

Senior Secured Bonds

Senior Unsecured Bonds

Junior Secured Bonds

Junior Unsecured Bonds

Preferred Equity (Stock)

Common Equity (Stock)

In a worst-case scenario, such as a company going bankrupt and dissolving, the above order indicates who gets paid off first. Senior bond holders are at the lowest risk of a permanent loss of their capital while common stockholders usually get wiped out. Thus another way to think about the capital stack is how risky an income investment is.

Preferred shares are a class of equity issued by companies for several reasons. The main one is that preferred stock allows them to raise capital without increasing their debt.

For example, suppose a company is worried that borrowing more will cause credit rating agencies to downgrade its bonds, which will raise its borrowing costs. By issuing preferred stock, the company can raise capital while lowering its debt-to-capital ratio and supporting or even improving the strength of its overall balance sheet.

Why issue preferred shares instead of common equity? If a company raises capital by issuing new common shares, then existing investors are diluted and the share price generally falls.

That’s because in order to sell enough new shares a company generally needs to entice investors by offering newly issued shares (what’s known as a secondary offering) at a discount to the current share price. However, because preferred shares trade separately from common shares, preferred stock offerings generally don’t cause the common share price to decrease.

In addition, preferred shares have fixed dividends which means that over time their dividend cost to the company doesn't increase, even if earnings and cash flow are growing over time.

Which brings us to the most important differences between preferred and common stock. Here's what investors need to know when deciding between these two types of equity investments.

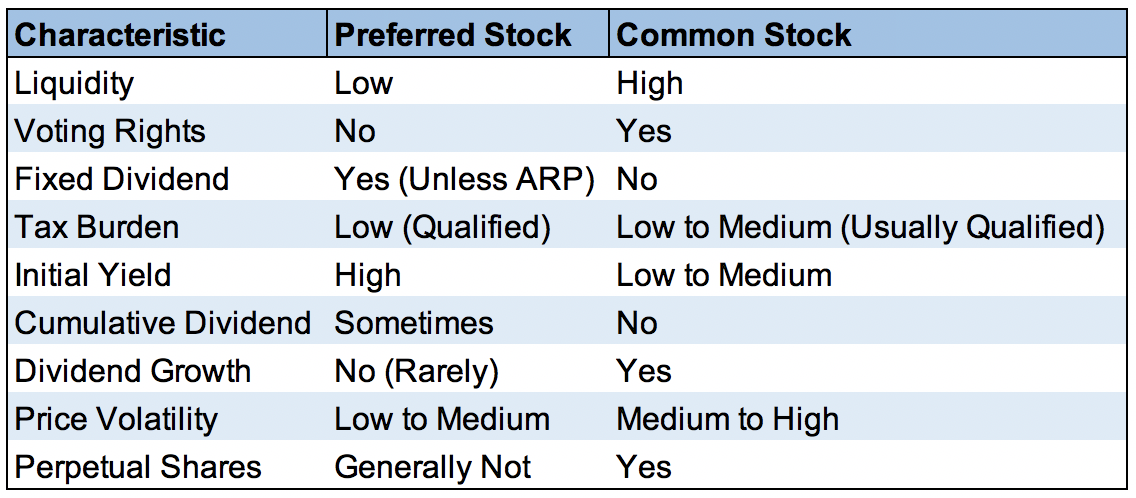

Preferred Stock vs. Common Stock

While both preferred and common stock are types of equity, there are important differences between them that can result in very different overall income, total return, and risk profiles over time.

The table below summarizes the key differences between preferred stock and common stock.

Sources: Simply Safe Dividends, Investopedia, Motley Fool, Seeking Alpha

Common shares are a stake in a business and represent ownership of a fraction of a company’s current and future profits. Common stock generally comes with voting rights and has historically appreciated the most over long periods of time, as a company’s earnings, free cash flow, and dividends experience growth.

Preferred shares, on the other hand, are a kind of debt/equity hybrid investment. They usually don’t have any voting rights and are issued with a stated dividend that typically doesn’t increase over time, which is similar to a fixed rate bond’s coupon.

Note that there is a special kind of preferred share called an Adjustable-Rate Preferred Share (ARPs) whose dividend is floating and generally tied to a set benchmark, such as the yield on Treasury bills. In addition, there are convertible preferred shares, which generally offer lower yields but have the option of being converted to common shares after a certain date.

Since a preferred dividend generally doesn’t grow, the yield on preferred shares when they are issued is generally higher than the common stock’s yield, in order to make up for a lack of dividend growth.

Furthermore, like common stock, preferred shares are generally more volatile than bonds in terms of how much their prices fluctuate. However, because of their fixed dividends and higher position in the capital stack, preferred shares generally aren’t as volatile as common shares.

The biggest reason for their lower volatility is the cumulative nature of some preferred shares. This means that if a company can’t financially pay a preferred dividend for a period of time, the preferred dividend obligation continues to accumulate as backpay.

If the company returns to financial health and resumes dividend payments, it must first pay off all of its accumulated preferred dividends. Common stock dividends are not allowed until preferred shareholders have been paid their accumulated dividends first.

In addition, common equity dividends are at the discretion of the board of directors each quarter, so if a company decides to cut or suspend its dividend investors have no recourse other than to sell their shares.

For many conservative investors this is one of the biggest pluses to preferred shares, especially for higher risk stocks such as REITs, MLPs, and BDCs.

While blue-chip corporations such as dividend aristocrats and dividend kings rarely fall into financial trouble and must suspend dividends, the high payout ratios and significant leverage employed by REITs, MLPs, and especially BDCs means they can be at greater risk of cutting or suspend their income payments to investors.

In other words, preferred shares are often a safer way to get a high yield, with lower income loss risk, for certain kinds of stocks.

Besides the risk of dividend suspensions, it's worth noting that most preferred stock, like bonds, has a maturity date after which the company has the right (but not the obligation) to buy back shares at par value (the initial issuing price, usually $25 per share).

This is known as the "call date" when a company calls back the shares and eliminates them. Their limited duration means preferred shares usually aren't "buy and hold forever" investments like common stock.

Due to their downsides (higher risk, lack of dividend growth, and lack of permanence), preferred shares are usually issued with higher yields than common stock to compensate investors for these risks. As a result, preferred shares are usually more attractive for investors who need immediate high income and are focused on capital preservation, such as retirees.

Alternatively, if you're primarily looking to grow your wealth over the course of many years and can handle somewhat greater volatility, building a diversified portfolio of quality dividend growth stocks will likely serve you better over the long term. Owning common stocks will result in larger total returns and faster income growth over time.

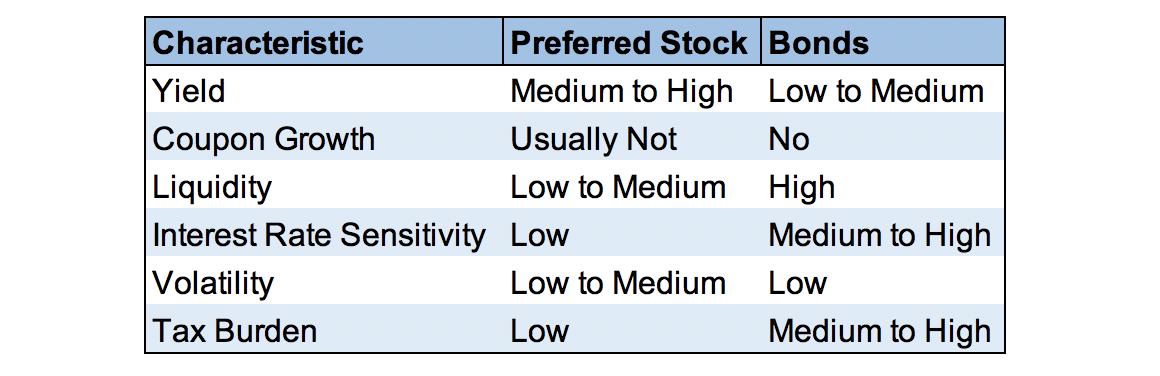

What about preferred stocks compared to bonds? Here, too, there are important pros and cons to consider.

Preferred Stock vs. Bonds

Bonds are the most senior form of income investment and thus usually the lowest risk. However, there are some downsides to their structure as well.

Sources: Simply Safe Dividends, Investopedia, Motley Fool, Seeking Alpha

Most notably, other than Treasury Inflation Protected Securities, or TIPs, bonds have no inflation protection. Their interest payments are fixed and they typically offer lower yields due to their reduced risk of capital loss. In addition, due to their fixed payments bonds have the highest interest rate sensitivity, meaning their value can rise or fall significantly based on interest rates.

That's because inflation eats away at the value of a bond's interest payments, reducing their inflation-adjusted or "real" returns. The longer the duration of a bond (how long until it matures), the more sensitive it is to interest rate fluctuations. For example, a 2-year Treasury bond has lower interest rate sensitivity than a 30-year Treasury bond because investors do not have their money tied up for nearly as long and can thus be more confident in the short-term outlook for inflation.

If interest rates rise, usually due to expectations for higher inflation, then a bond's price will decline so that its yield equals the prevailing yield on similar duration bonds.

For example, suppose you invest $10,000 into a 30-year Treasury bond at a yield of 3%. You'll get paid $150 every six months for 30 years, and at the end of the 30 years you'll get back your $10,000 principle. Note that assuming 2% inflation that $10,000 will only retain $5,500 in buying power using today's dollars.

While such an investment is "risk free" if you hold until maturity (the U.S. government will theoretically never default on its bond obligations), if you need to sell the bond earlier then you might very well take a substantial loss on it.

For instance, if interest rates rise after your purchase and a new 30-year Treasury bond now yields 4%, then the value of your 30-year bond will have declined by about 25% (actual price will factor in remaining duration and interest payments). The price decline is necessary so that the yield on your older bond now matches the 4% yield bond investors can get on freshly issued 30-year Treasurys.

Another thing to consider is that very few investors actually own individual bonds themselves. Rather most investors buy bond mutual funds or ETFs, which own large and diversified portfolios of bonds of various durations and maturities. Such funds have no actual maturity date (they are perpetual investments) which means that they carry larger risks of price losses should interest rates spike higher over a relatively short period of time.

In contrast, preferred shares usually have shorter durations since most are called within five or 10 years. As a result, preferred stock is less interest rate sensitive than most longer-term bonds. And while there are many preferred share mutual funds and ETFs available, it's usually easier to invest in individual preferred stock than it is in individual bonds (which usually come in denominations of $1,000 for corporate bonds and $10,000 for U.S. Treasurys).

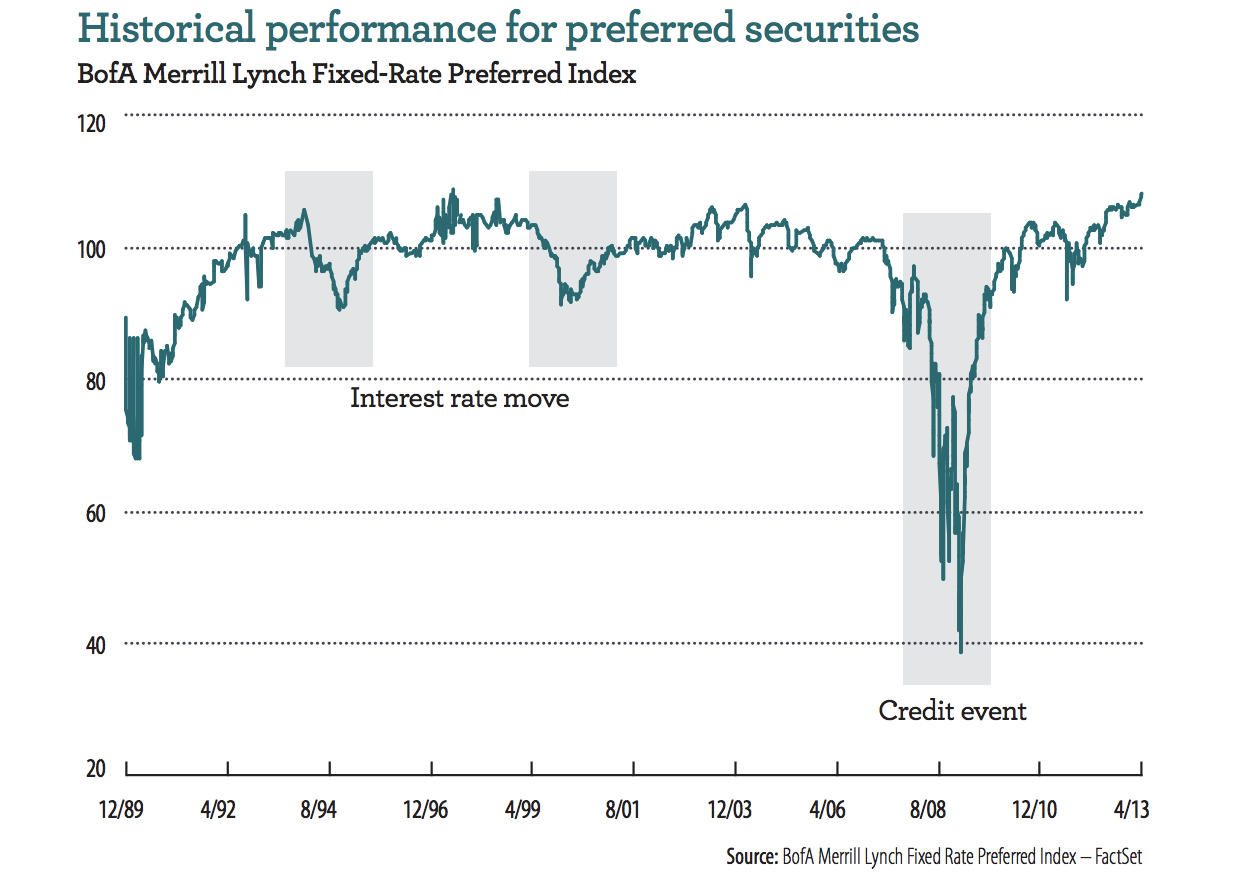

It's also worth nothing that despite their lower sensitivity to interest rate fluctuations, most preferred stock is still more volatile than bonds. Thanks to lower trading liquidity and greater credit risk, you can see that preferred securities tumbled during the financial crisis, with many losing as much as 50%. Meanwhile, in 2008 Treasurys gained 13.7%, corporate bonds were down just 4.9%, and even high yield (i.e. junk) bonds performed better with a 26.2% loss.

Source: Wells Fargo Advisors

Finally, investors should be aware that income from preferred stock is taxed more favorably than the coupon payments made by bonds. Let's take a look at the tax consequences of owning preferred stock.

Preferred Stock Tax Considerations

While most bond interest is taxed at your top marginal tax rate as ordinary income, preferred share dividends usually are taxed at the lower capital gains rate. That's because C-corp preferred dividends are qualified dividends.

However, investors should note that preferred shares issued by REITs and other pass-through entities such as business development companies do not enjoy qualified tax status, and their dividends are typically taxed at ordinary rates.

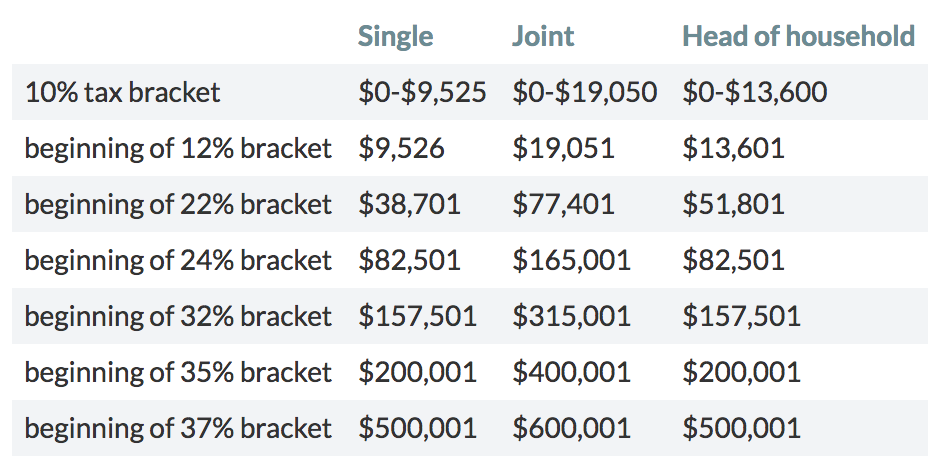

For unqualified income (including bond interest), your tax obligation will be based on the new marginal tax rates that went into effect after the 2017 Tax Cuts and Jobs Act.

Source: Marketwatch

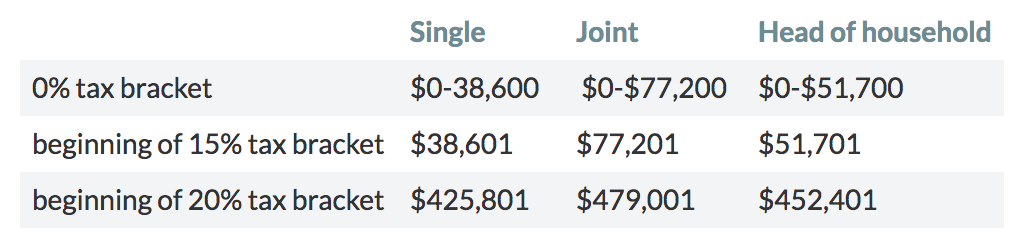

In contrast, the preferred dividends, being qualified income, are taxed at long-term capital gains rates which can be seen below.

Source: Marketwatch

Note that for those earning over $200,000 in adjusted gross income (singles) or $250,000 (couples), the 3.8% Affordable Care Act surcharge tax on capital gains and dividends still applies.

However, the point is that for most preferred dividends you get taxed at much lower rates than you would with bond interest payments. The exception is municipal bonds which are tax free at the Federal level and tax free at the state level if you live in the state that issues them.

Owning preferred shares in retirement accounts such as IRAs or 401(k)s will defer any tax liability until you make withdrawals, including for required minimum distributions, or RMDs. However, the downside to owning preferred shares in retirement accounts (other than Roth IRAs) is that all RMDs are taxed at your top marginal income tax rate. Thus you ultimately lose the beneficial lower tax rates on preferred shares by holding them in retirement accounts.

What about selling preferred shares? All capital gains are treated the same as with common equity, meaning they are taxed at the capital gains rate. If you own the shares for at least a year, then the tax rate will be the long-term capital gain rate. If you hold for less than a year, then the short-term capital gains rate applies, which is equal to your top marginal income tax rate.

How to Buy Preferred Stock

There are two ways to invest in preferred stock, and each has its own pros and cons. The first option is buying individual preferred shares via your broker, just as you would a common stock.

The upside is that you get direct visibility into what you own – the company's credit quality, the preferred stock's important terms such as the call date – and you control if and when you choose to sell your individual shares to minimize your tax liability.

The downside is that, depending on the rest of your retirement portfolio, you need to be mindful of your preferred stock diversification. If you buy preferred stock from just one company, your risk of income or capital loss increases if that business becomes financially distressed or goes bankrupt.

The other way to buy preferred stock is by purchasing shares of a preferred stock mutual fund or ETF. The benefit of this approach is that by owning a diversified mix of preferred shares you minimize the chances of losing your entire investment or having your dividend income stop entirely. After all, unless the fund or ETF you select is extremely concentrated in just one or two sectors, chances are that few of those companies will go bankrupt or suspend their preferred dividends at once.

However, the downside to owning preferred funds is that it effectively creates infinite duration risk, similar to bond fund risk. That means that as preferred shares are called, the fund will reinvest them into new preferred shares at prevailing prices and yields. As a result, these funds have increased interest rate risk in terms of share price volatility.

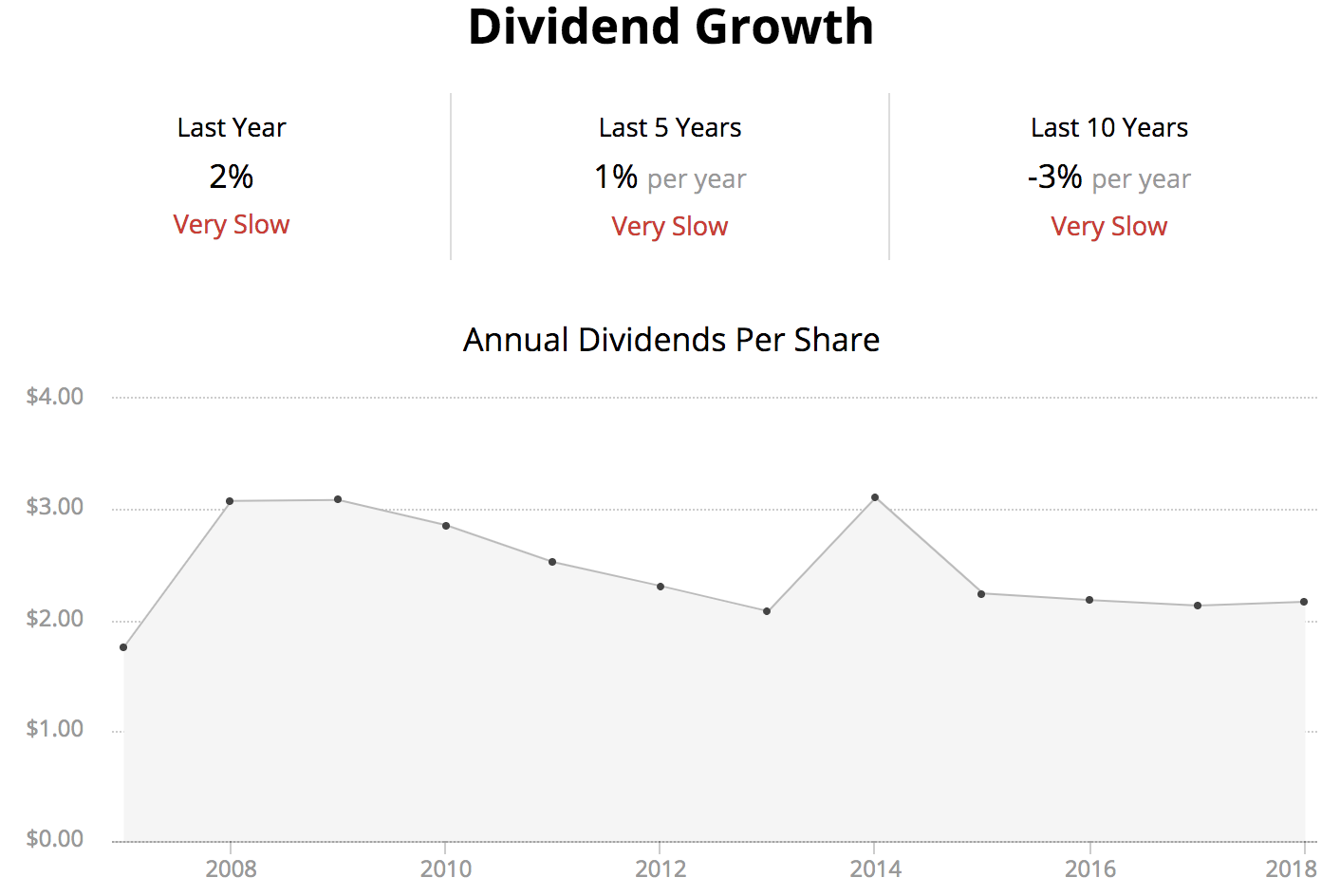

The other downside to such diversification is that because the mix of preferred shares changes over time as they become called and replaced with new issues, the income from such funds tends to be more variable. For example, the chart below shows the annual dividends paid by the iShares Preferred and Income Securities ETF (PFF), one of the largest preferred stock ETFs in the market that invests in hundreds of different holdings.

iShares Preferred and Income Securities ETF (PFF)

While such funds are likely to always offer relatively high yields, if your main concern is rock steady dividends than be aware that preferred funds or ETFs do have fluctuating payments over time. This is especially true over the long term as interest rates change and thus can drastically affect the yields most preferred stocks are issued at.

With that said, for those looking to buy preferred shares individually, be aware that there are some other important factors to consider.

Do Your Homework Before Investing In Preferred Shares

When you buy an individual preferred stock you need to make sure you understand the terms you are agreeing to. Preferredstockchannel.com is a good resource for looking up important information. Let's review a C-corp preferred share as an example of some of factors investors need to understand.

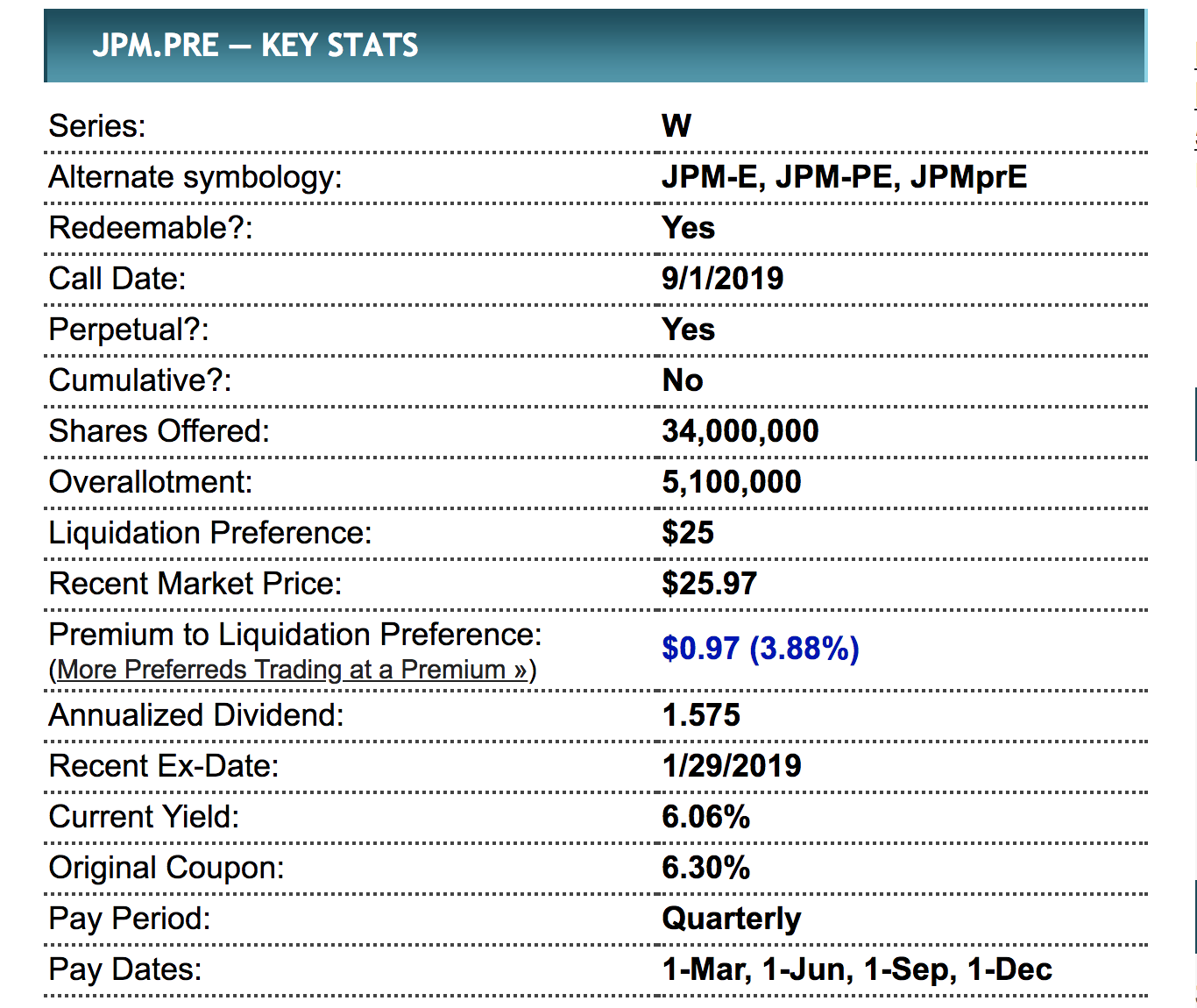

Using JPMorgan Chase Series W preferred shares, we can see that there are several factors that may make this class of stock more or less appealing than the company’s common equity.

Source: PreferredStockChannel.com

For example, the $1.575 per share dividend is fixed, meaning that even if the bank’s earnings soar thanks to rising interest rates (and its common dividend rises), your dividend payments won’t change.

However, with a 6.1% current yield, these shares offer attractive income. In addition, the shares are perpetual meaning that, theoretically, JPMorgan may allow them to continue existing indefinitely, which would be appealing to investors who need high immediate income for long periods of time, such as retirees.

But at the same time, the shares are callable past September 1, 2019. This means that JPMorgan has the right to buy each share back (and retire it) at the par value of $25 per share, 3.7% below the current share price. And given that the high yield on these preferred shares means a higher cost of capital than what JPMorgan might find in other capital markets, it is certainly possible that it will choose to buy back these shares.

This means that, with only $0.7875 in dividends per share guaranteed before the bank might call these shares, your effective cost basis is $25.97 (current price) minus $0.7875 (future dividends) = $25.18.

With the call price of $25 per share, that means that if you hold these shares until their call date and JPMorgan buys them back at $25, then you would actually incur a slight loss, despite holding a "safe" income investment from one of the highest quality banks in the world.

In addition, even if JPMorgan doesn’t buy these shares back, keep in mind that preferred shares aren’t necessarily guaranteed a dividend. They are merely the first shares in line to receive dividends first if a company decides to pays a dividend.

Now JPMorgan is a very strong company with an excellent balance sheet, reducing the chances of the company having to cut or eliminate its dividend. However, some preferred shares are issued by far less financially stable companies.

Simply put, anyone considering buying preferred stock needs to be willing to do a lot of homework.

First, you need to understand exactly how the preferred stock is structured (cumulative dividends or not, callable or not, perpetual or not). Next, you need to dig into the company’s fundamentals to make sure that the sales, earnings, cash flow, and balance sheet are strong enough for the company to survive and, most importantly, be able to pay a dividend at all (our Dividend Safety Scores can help).

In other words, you have to think like a bond investor, willing to put in the time to perform due diligence and determine whether or not a particular preferred share is worth buying based on your individual needs. Most investors don’t have the time or expertise to do this.

Given the number of risks involved, financial services firm Janney Montgomery Scott recommends an investor allocate no more than 10% of whatever amount they would put in fixed income securities in preferred shares.

Closing Thoughts on Preferred Stock Investing

While certain high-quality companies offer attractive preferred shares, successfully navigating the complexity of this asset class requires a great deal of time and research that most investors don’t have or are unwilling to devote to investing.

Compared to many long-term bonds, preferred stock offers a number of appeals, including higher yields, a more favorable tax treatment, and less interest rate sensitivity. For current income seekers looking for bond alternatives and additional portfolio diversification, certain high quality preferred stocks can make sense as part of a fixed income portfolio. However, be aware that they contain a number of unique risks – don’t let their “preferred” name trick you into thinking that your money is safe or guaranteed.

Alternatively, similar yields can be found in high-quality REITs, MLPs, utilities, and certain telecom common stocks. While regular dividend growth stocks are more volatile than preferred shares and typically offer lower starting yields, they can represent a more appealing opportunity for investors who prefer dividend growth and desire greater long-term capital appreciation potential.

.png)