Required Minimum Distributions (RMDs) for Dividend Investors

Contributed by Dave Van Knapp

There can sometimes be a lot of angst about RMDs – Required Minimum Distributions – especially among investors approaching their RMD kick-in date.

The angst is based on having to pay taxes to retrieve your retirement funds. Taxes get on people’s nerves, and they make some individuals angry. Many folks will go to great lengths to avoid taxes.

On top of that, some people regard RMDs as mandatory sales, and they resent being obligated to liquidate investments that they want to keep, or to spend money unnecessarily. They don’t see how the RMD withdrawal rate aligns with their “4% rule” or other systematic approach to harvesting retirement funds.

But those are misconceptons.

You don’t have to liquidate anything if you don’t want to.

You don’t have to spend the money.

The RMD rate bears no relationship to any rule of thumb for harvesting.

RMDs simply require you to expose assets that were never taxed to taxation.

A few years ago, when I was approaching my first year of RMDs, I studied the laws and literature about them. I concluded that the overall system is fair.

RMDs In a Nutshell

When the U.S. created retirement accounts in the 1970s, it made them tax-deferred. That means that every dollar of wages that you steer into a retirement account goes untaxed at that time. All the gains in the account remain untaxed, too.

Traditional retirement accounts are not tax-free forever. They are tax-deferred. The taxation happens later, when you make withdrawals.

Until then, all contributions, plus gains made from them, can compound without taxation for years or decades in your 401(k), traditional IRA, or similar retirement account.

For a simple example, say that the tax deferral means that 20% more contribution money makes its way into your retirement account over the years. That extra 20% can work for you and earn significantly more money, because the taxes on all of it are deferred.

Ultimately, when you make withdrawals, the money is subject to taxation.

RMDs are taxed as ordinary income. It doesn't matter whether the money originated from your contributions, employer matches, short-term capital gains, long-term capital gains, interest, or dividends. It is all taxed as ordinary income when it leaves the IRA.

You must initiate RMDs beginning at age 73 under current law. You are required to annually distribute (remove) some of the value out of your retirement account.

At that point, the amount you withdraw is finally taxed.

How Much Do RMDs Require You to Remove?

Once RMDs start, the amount that you remove each year is based on actuarial principles, meaning life expectancy.

The RMD is calculated by dividing your account balance at the end of the preceding calendar year by what the IRS calls the distribution period, which is a projection of the remaining years you have to distribute from the account.

The distribution period is shown in three tables available from the IRS:

The “Uniform Lifetime Table” is used by most married taxpayers.

There is a different table if the sole beneficiary is the owner’s spouse, and that spouse is 10 or more years younger than the account owner.

And there is a third table if the beneficiary is not the spouse of the account owner.

As you get older, the remaining distribution period declines each year as you get older. That, in turn, increases a larger percentage of your account being distributed each year.

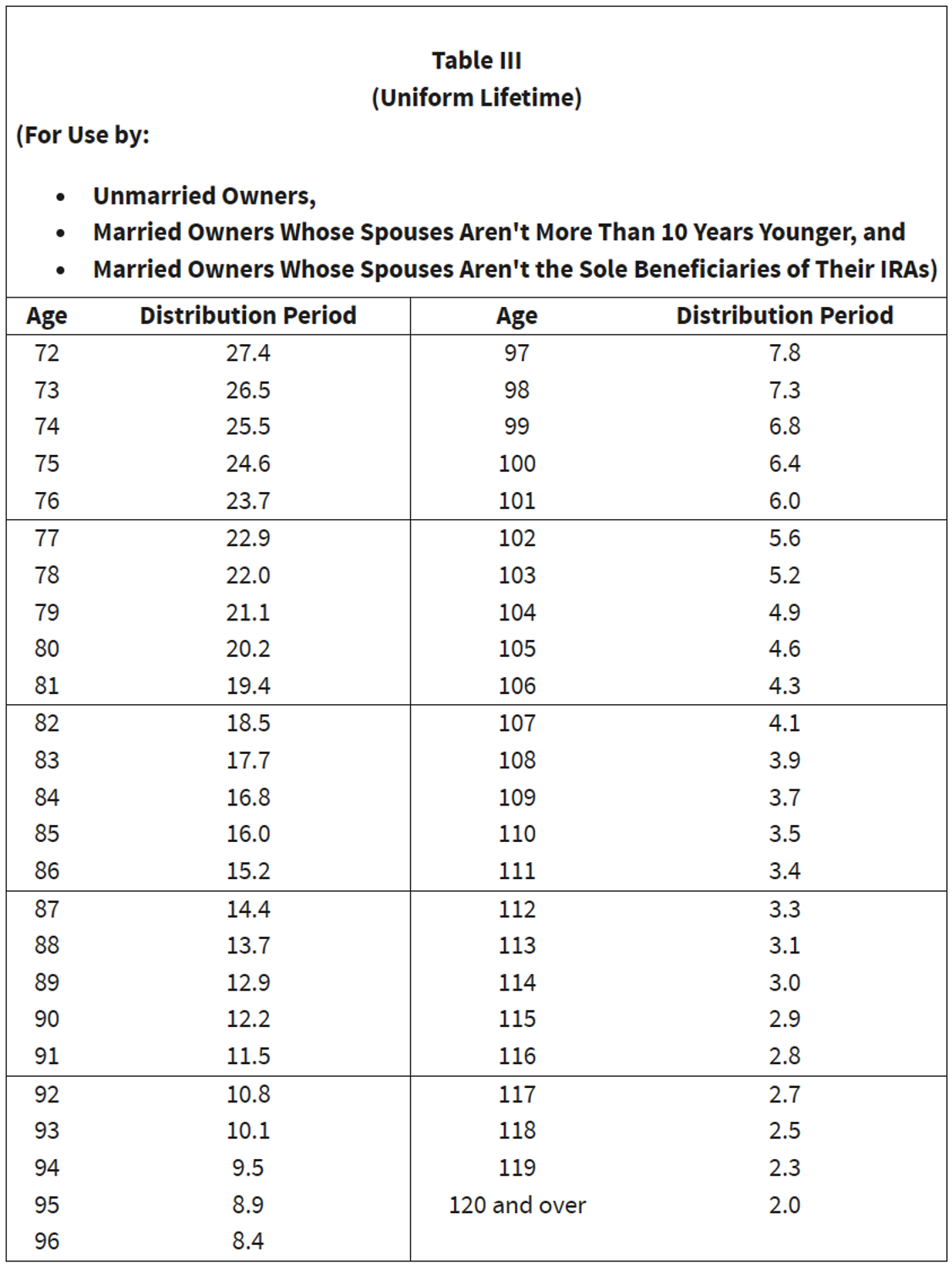

Here is the current Uniform Life Table from the IRS.

Source: IRS

Notice how the Distribution Period declines each year as you get older.

For example, at age 73, the period is 26.5 years, which means that your RMD would be about 3.8% of your account balance at the end of the previous year:

Account balance ÷ 26.5 = 3.6% of account balance must be distributed

By age 77, the divisor declines to 22.9, causing the distribution percentage to rise to almost 4.4% of your account.

Most brokerages calculate your RMD amount for you. For example, my IRA is held at Schwab. They compute my RMD each year and notify me several times throughout the year of my total RMD, how much I have already distributed, and how much remains to distribute by the end of the year.

Must the RMD Be Made in Cash?

RMDs do not have to be taken in cash, and as mentioned earlier, you are under no obligation to spend them.

"In kind" distributions allow you to transfer your investments to a taxable account rather than sell them. Your brokerage will be more than happy to facilitate that. You still owe taxes on the dollar value of the distribution.

Your original cost basis on whatever you distribute is irrelevant, because the distribution is taxed as ordinary income. If you transfer assets in-kind, their value establishes the cost basis in the new account.

Personally, I have never made in-kind transfers. I just take my RMDs in cash each year.

How Much Tax Do You Owe on RMDs?

The tax on your RMD depends on what tax bracket(s) it falls into.

Under our system of progressive taxation, the highest rate applies to your “last dollars” of income, which means your RMD.

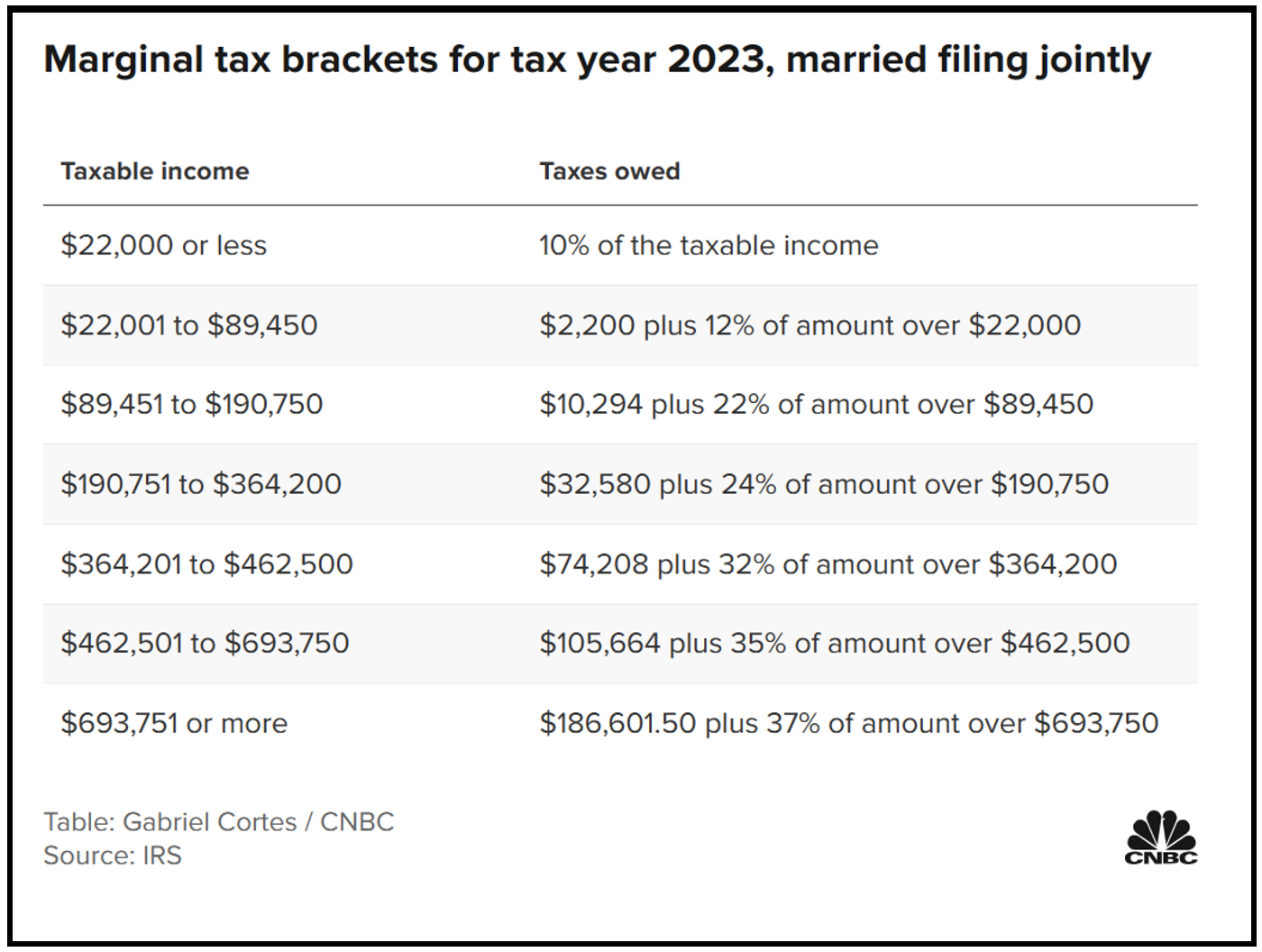

The IRS adjusts tax brackets every year for inflation. The following shows current tax brackets for married couples filing jointly, covering 2023 income for returns filed in 2024.

So, if your other income places you in the second bracket (12%), your RMD will be taxed at 12%, unless some of the RMD itself spills over into the next bracket (22%). In that case, the “excess” dollars will be taxed in the next bracket at 22%.

Again speaking personally, I view income taxes as a line item in our overall expense budget. They are not unlike other recurring obligations like real estate taxes or our cell-phone bill.

Viewed that way, the additional income taxes on my RMDs just become part of our annual budget. The amount is not negligible, but it does not explode our budget either.

The RMD itself always contains more than enough money to pay the tax on it, meaning that there is money left over to do with as you wish.

Reducing What You Owe

There are several ways to reduce how much you owe.

Qualified Charitable Distributions

One useful way to reduce what you owe is to make Qualified Charitable Distributions (QCD) as contributions directly from your retirement account.

The contribution must be direct: The money cannot stop over in your possession. It's not a QCD if you distribute funds to yourself and then donate them to a charity.

QCDs are a good deal for everyone. The charity of your choice gets your contribution. And you get to deduct the amount of the contribution, even if you do not itemize deductions. That deduction reduces your taxes.

My wife and I obtained a checkbook from Schwab for the specific purpose of making QCDs. It says “IRA ROLLOVER” on each check, which proves that the money is being contributed directly from my IRA. We use those checks for contributions to our church, my wife’s college, and other charitable donations that we make each year.

Smaller Retirement Account

Another way to reduce how much you owe is to have a smaller retirement account. Last year’s final account value is the numerator in this year’s RMD, so the smaller your account, the smaller will be your RMD.

No sane person roots for their account value drop in order to avoid taxes, but if your account value does drop, that will reduce your taxes the following year.

Roth Conversions

Another way to reduce the size of your retirement account is to remove distributions earlier than the law requires. Many do this by moving money into Roth IRAs, which went into effect in 1998.

Unlike its 1970s-era predecessors (with their RMDs), Roths are truly tax-free once the money gets into the account. Roth contributions are made with money that has already been taxed.

After that, the Roth never gets taxed, including gains made within it. There are no RMDs from Roth accounts during the lifetime of the original owner.

The key question therefore becomes:

Is it a good idea to distribute money “early” from a traditional retirement account, pay the resultant tax earlier than the law requires, and then move it into a Roth, in order to reduce future taxes owed?

The answer to that question is not simple.

Downsides of “prematurely” converting money into a Roth include:

You must pay taxes on the conversion amount earlier than the law requires.

Tax-free compounding is interrupted on the conversion amount, although of course those gains were subject to future taxation.

The distribution may spill over into a higher tax bracket.

Upsides include:

The reduced (taxed) amount transferred to your Roth re-starts compounding tax-free from its new (lower) starting point.

Money in the Roth – contributions, conversions, and investment gains – will never be taxed again.

You assume control over when distributions are made, rather than following the government’s schedule.

If you expect to be subject to higher tax brackets in retirement, converting “early” makes more mathematical sense than waiting.

There is no one-size-fits-all answer for everyone.

Under current law, tax rates are scheduled to rise with the 2025 expiration of the 2017 Tax Cuts and Jobs Act. Unless the law is changed, tax rates will increase by several percentage points within each bracket.

Some investors carefully convert just enough in earlier years to keep all of their taxable dollars contained within their marginal tax bracket, but not one dollar more than that.

Because no one knows what tax brackets will look like in the future, there is guesswork involved. Plus, rules and restrictions on Roth withdrawals may be disadvantageous if you convert.

Other factors, such as your age, your spouse’s age, health, spending needs, and estate planning can all play into conversion decisions.

For these reasons, it is usually recommended that anyone contemplating “early” Roth conversions should consult a qualified financial planner or tax professional to work out scenarios and decide what to do.

For myself, the question is moot. I retired shortly after Roths were invented, so I never had one. My highest earning years were at the end of my career, so I had no expectation of higher tax rates after I retired.

Therefore, I simply follow the RMD table applicable to my traditional IRA.

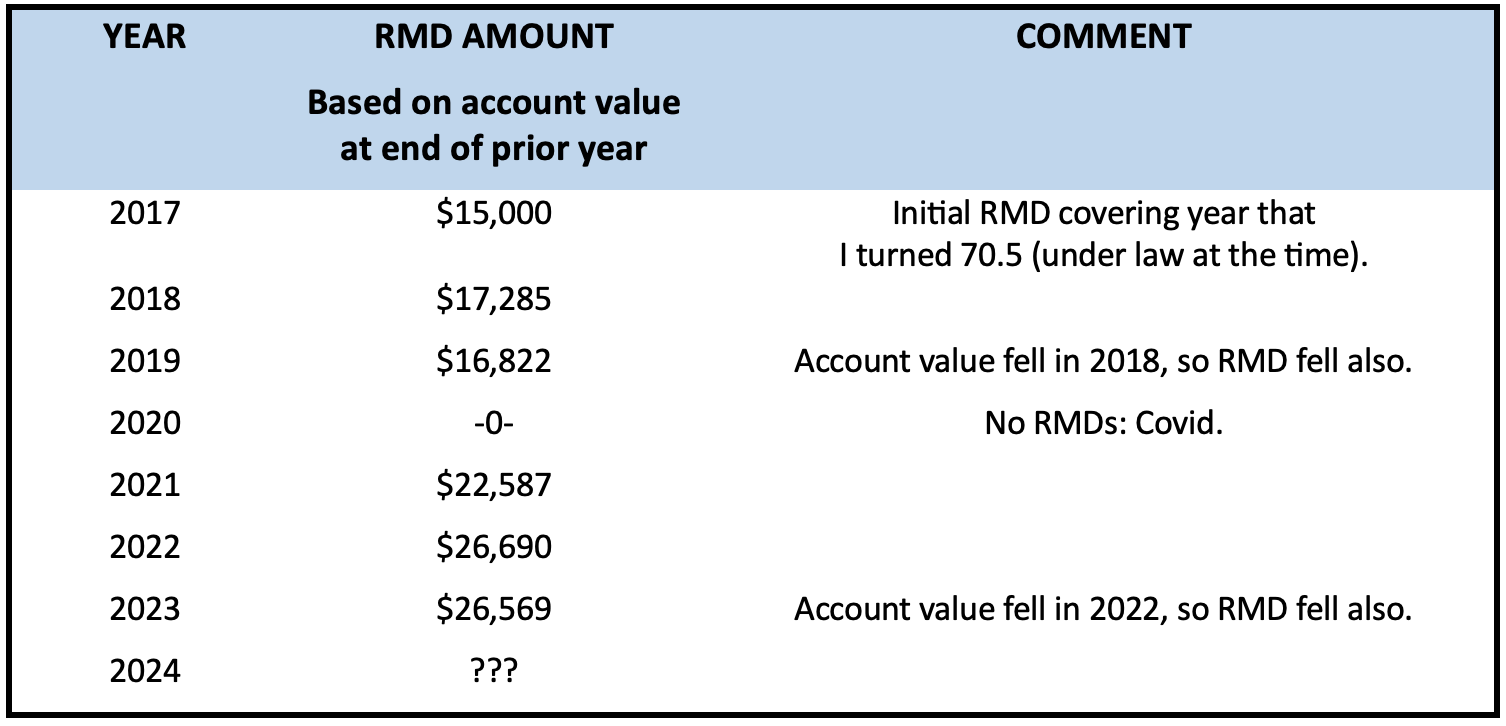

Here are the RMDs that I have made. (I have altered the first amount to protect my privacy, but each one after that changes by the same percentage as my actual RMD.)

Source: Author

I chose to take my first RMD in the year I turned 70.5, which was the required age at that time. (Since I retired, the age when RMDs begin has risen to 73.)

By law, I could have waited until the next year, but then I would have needed to make two RMDs in the same calendar year, because the grace period only applies to your first year.

That grace period still exists, but double RMDs in a single year can push some money into the next higher tax bracket as well as trigger higher taxes on your Social Security benefit.

That was my original goal too. I even started about a year early, holding dividends in cash, so that they would be available for my first RMDs.

But within a couple years, I discarded the goal for these reasons:

I did not want to manage my IRA to ensure that it would generate enough dividends to satisfy each year’s RMD.

I did not want the self-imposed goal of funding RMDs with dividends to seduce me into making bad investment decisions.

I did not want RMDs to cause me to “chase yield” by gradually overweighting my portfolio with ever-higher-yielding investments.

I wanted to keep reinvesting dividends to compound, rather than let them accumulate in cash to fund future RMDs.

Summary and Conclusion

Contributions to traditional retirement accounts are not taxed, becausethey are deductible in the year made. Employer matches and gains generated within the accounts are also not taxed at the time.

Therefore, traditional retirement accounts allow tax-free wealth-building and compounding until you make distributions.

RMD rules require distributions from such accounts when you hit a certain age (currently 73), to allow the government to collect taxes on retirement savings and related gains that were never taxed before.

The IRS does not care what you do with RMD withdrawals beyond requiring that you pay taxes on them. You are not required to spend them.

RMDs simply require you to move value out of the retirement account to allow it to be taxed as ordinary income.

You may find that your RMD, even after taxation, is larger than you need to cover living expenses. When that happens, there are several things you can do with the money:

Use Qualified Charitable Distributions (QCD) to make or enlarge your charitable giving. This has the additional advantage of lowering the tax on your RMD.

Strengthen your finances by starting or bolstering an emergency fund, or paying down debt.

Invest the money. You can take your RMD in-kind by moving investments into a taxable account. Or you can sell investments from your retirement account, use part of the cash to pay the tax, and reinvest the rest.

Fund 529 educational accounts for your grandkids.

Use the money (or some of it) to fund a vacation or improve your standard of living in a way that pleases you.

Some individuals convert assets from traditional retirement accounts into Roth IRAs by withdrawing money before it is subject to RMDs. They do this to reduce the amount of taxes owed in the future.

This can work very well, especially if you think you will be in a higher tax bracket after you retire. It is advisable to consult an expert before embarking on such conversions.