Interest Rates, Oil, and Coronavirus Shutdowns Create Some Uncertainty for Main Street

Main Street Capital (MAIN) was the only Safe-rated business development company, or BDC, prior to the coronavirus outbreak. Five other BDCs were rated Borderline Safe, and the remaining 30-plus companies have had Unsafe or Very Unsafe Dividend Safety Scores for several years.

Since the beginning of March, the VanEck Vectors BDC Income ETF (BIZD), which tracks the overall performance of publicly traded BDCs, has collapsed 46% while the S&P 500 Index has shed 21%.

Handing out loans with double-digit yields in a zero interest rate world is a dangerous game that's only magnified with the use of leverage. In 2018, Congress even increased the amount of leverage BDCs can use.

Making matters worse, most borrowers who take money from BDCs are relatively small, highly levered companies that aren't able to access traditional financing from banks.

The competition to win business is tremendous too with private funds awash in cheap capital and many investors hungry for yield.

In fact, total global private credit assets under management surged from $238 billion in 2008 to nearly $770 billion at the end of 2018, according to the Alternative Investment Management Association.

Simply put, this business model has always struck us as one akin to picking up pennies in front of a steamroller, which could arrive at any time and with little warning.

The Covid-19 pandemic, coupled with the oil-price war, has threatened to pop the BDC bubble and lead to wave of loan defaults as the American economy temporarily freezes to slow the spread of the virus.

High-yield default rates could spike to their highest level since the financial crisis if the coronavirus outbreak persists, according to Moody's.

Smaller companies with higher debt loads, more cyclical operations, and less access to financing find themselves especially in the crosshairs as their cash flow temporarily evaporates.

Given this backdrop, Main Street's (MAIN) lofty dividend yield near 14% may not come as a surprise. However, the company has never cut its monthly dividend since making its first payout in 2007, a stretch that includes the financial crisis.

Main Street's discipline has continued since then. For example, the firm wisely passed on the extra leverage the industry was granted in 2018 and maintains a BBB credit rating from S&P.

The big question is whether or not its investments (primarily first-lien secured loans) can hold up well enough in this unprecedented environment to keep the dividend safe. There are several areas of concern.

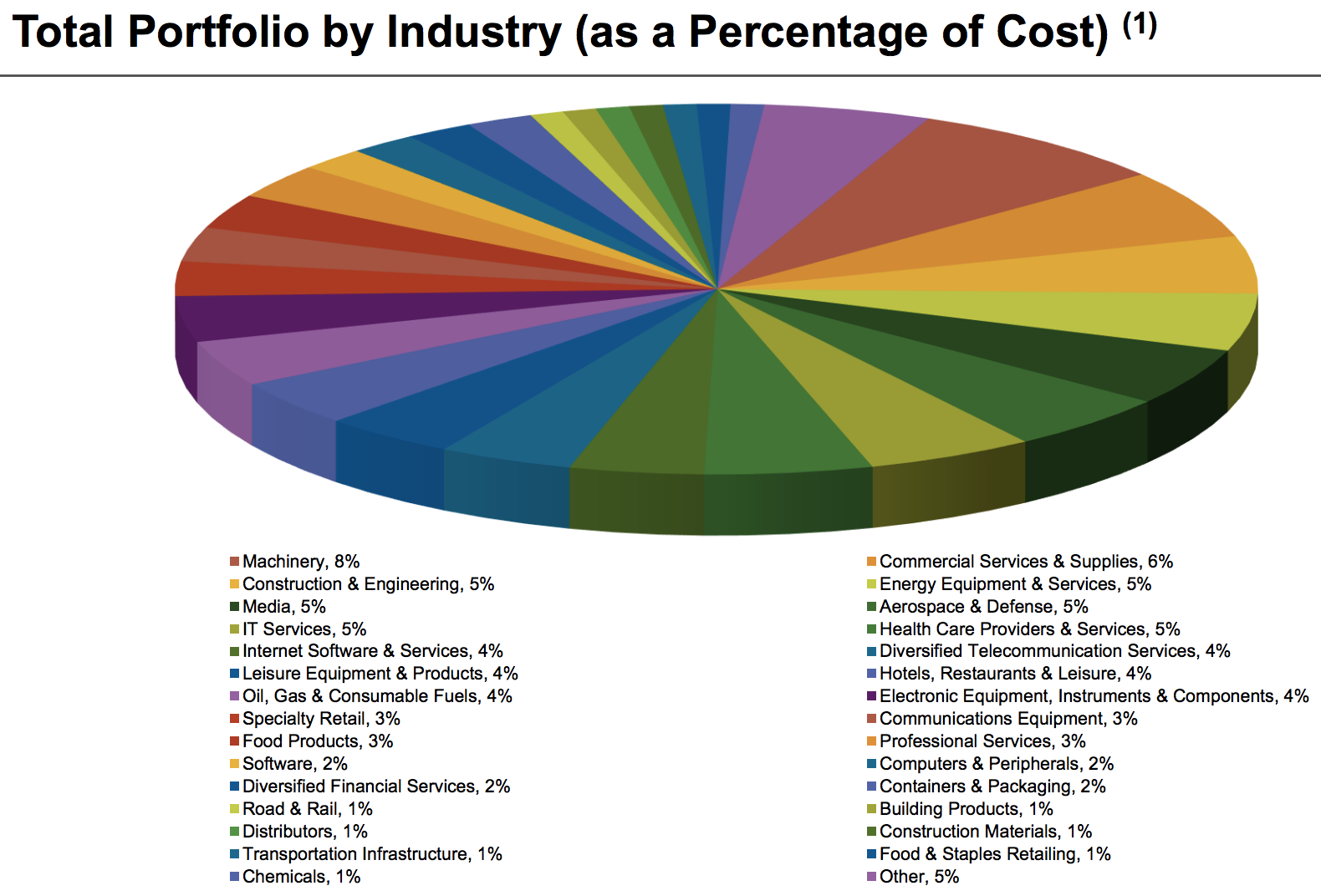

Main Street discloses that 5% of its portfolio is in the Energy Equipment & Services business, which is expected to be hit the hardest by the crash in oil prices as producers drastically reduce spending.

Another 4% of the portfolio is in Oil, Gas & Consumable Fuels which seems likely to feel pressure, too. Hotels, Restaurants & Leisure, industries under the most immediate pressure from coronavirus shutdowns, account for 4% of the portfolio.

Source: Main Street Capital Investor Presentation

It's too soon to say how able those firms will be to meet their debt obligations, and it may take several quarters to find out. Interest rates further complicate the picture.

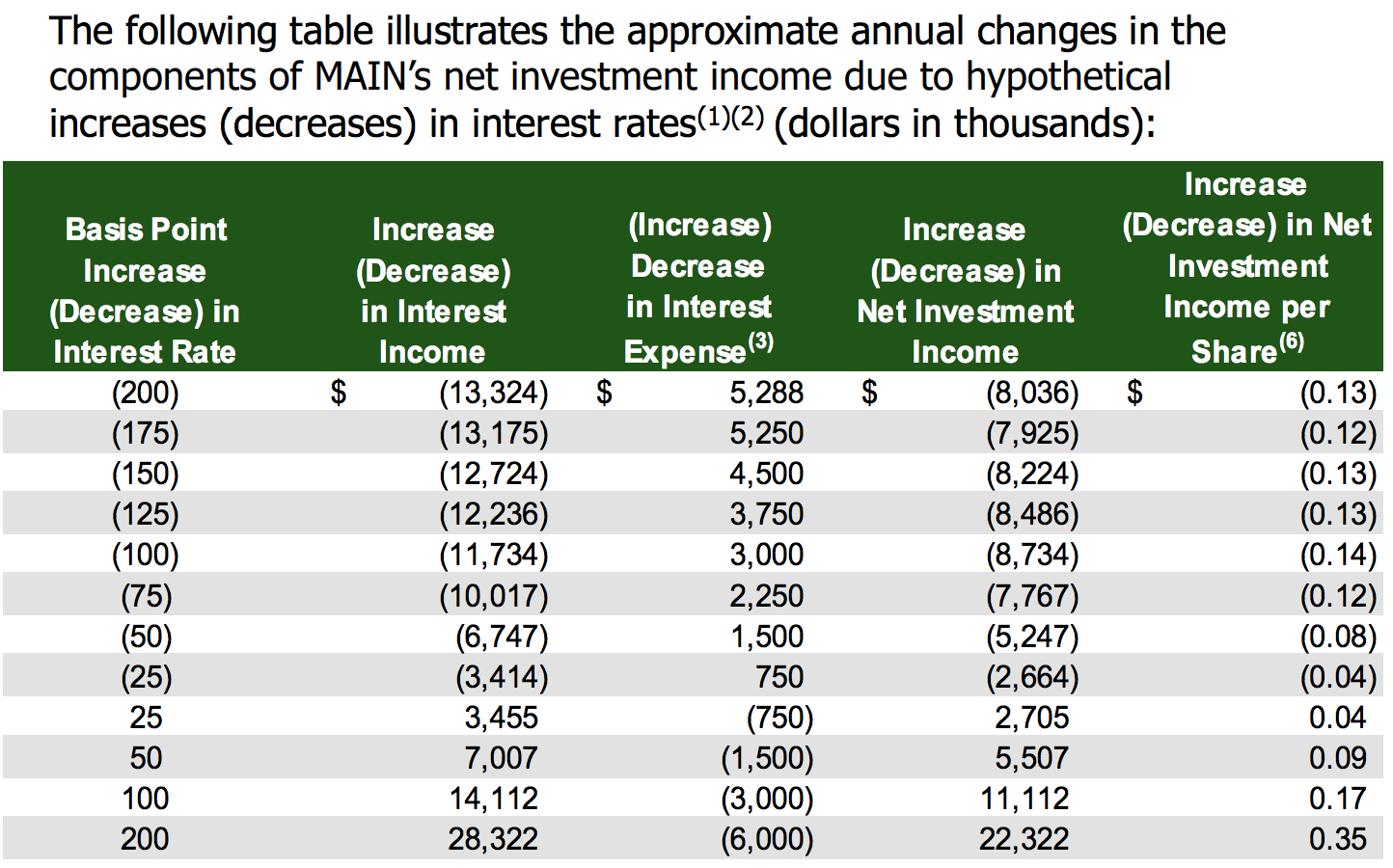

Approximately 73% of Main Street's debt carries fixed rates, but 74% of its debt investments bear interest at floating rates. When rates rise, this increases the firm's investment income.

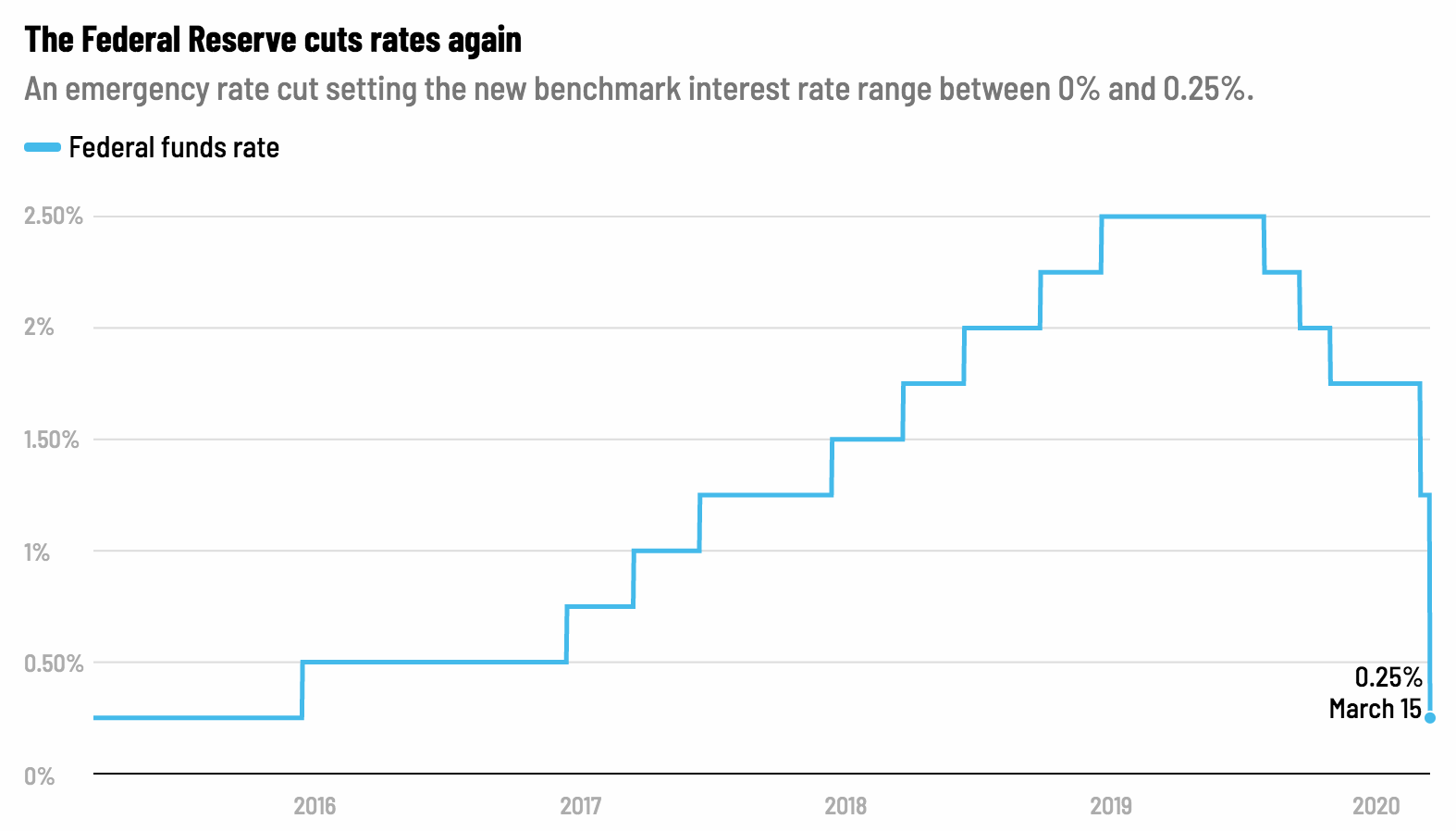

However, the Fed surprised investors last Sunday by announcing its second rate cut in less than two weeks with hopes of giving the economy a boost. As you can see, the Federal funds rate has plunged by 150 basis points since the start of the year.

Source: CNN

Main Street estimates that its annual net investment income per share would fall by 14 cents (about 6%) if interest rates fell 100 basis points.

Source: Main Street Investor Presentation

That's not a huge hit, but it reduces the margin of safety Main Street has to absorb a potentially elevated amount of non-performing loans in the year ahead.

In 2019, Main Street delivered distributable net investment income (DNII) of $2.66 per share, covering its dividend of $2.46. The plunge in interest rates could reduce its DNII to around $2.50 per share in 2020 for a payout ratio near 100%.

Should any material loan defaults occur, which seems likely given the disruption caused by the coronavirus and depressed energy markets, Main Street's DNII won't cover its dividend this year.

But the company has been here before. In 2009, Main Street paid $1.50 per share in dividends and generated $1.02 in distributable net investment income per share.

In 2013, when Main Street began paying supplemental dividends, management explained how the firm is able to cover such shortfalls:

"The significant amount of undistributed taxable income, or spillover, generated to date has allowed us to begin paying periodic special dividends in addition to our regular monthly dividends. The large spillover amount means that we have significantly out earned our dividends paid to date which gives us a lot of future flexibilities to support both regular, recurring, and special dividends.

The equity component of our lower middle market investment strategy remains a significant differentiating advantage for Main Street. It is the primary driver behind approximately $3.30 per share of gross net unrealized appreciation within our investment portfolio at March 31, as well as our cumulative NAV growth per share. These equity positions support growth in our taxable income and, therefore, our dividends paid, through current dividend income received and periodic realized gains harvested from the $3 plus per share of net unrealized appreciation.

Due to our spillover position and our appreciating equity portfolio, we are not solely reliant on growth or yield trends in our debt portfolio in order to grow and cover the dividends paid to shareholders. These factors also put us in the position to not have to reach for risk or make investments outside of our historical credit parameters to grow and cover our dividends.

This is differentiated from many other investment companies who are experiencing flat or declining earnings, and potentially dividends, based on the impact of market trends on yields and portfolio growth."

Essentially, Main Street invests in a mix of debt and equity and periodically realizes gains upon the exit of successful investments.

These gains and other undistributed taxable income (known as "spillover") provide an offset against the inevitable credit losses that will be experienced when making investments in non investment-grade debt securities.

In 2008, Main Street generated spillover income of $0.44 per share which plugged nearly all of the shortfall between its dividend ($1.50 per share) and distributable net investment income ($1.02 per share) in 2009.

Heading into 2020, Main Street estimated it had generated undistributed taxable income of $0.66 per share, or about 27% of its current dividend, that will be carried forward toward distributions to be paid this year.

That provides some cushion to absorb investment losses without sacrificing the dividend, as long as management believes future cash flow will recover.

If Main Street felt more pressure to maintain the dividend, its balance sheet has capacity to take on higher leverage, too. On a regulatory basis, Main Street's total debt-to-equity ratio is just over 0.5:1, well below the legal limit of 2:1.

The company also has $405 million of unused capacity under its revolving credit facility it can use to support its investment and operating activities. For context, the firm's dividend totals about $165 million annually.

Looking ahead, Main Street's stock closed at $17.82 per share on March 20, well below the company's net asset value (assets minus liabilities) of $23.91 per share. This type of discount doesn't happen often and suggests that the market expects the value of some of the firm's investments to be written down in the future.

The stock's depressed multiple also restricts management's ability to issue stock through Main Street's at-the-market program without costly dilution to shareholders.

In the past, Main Street has said that in an ideal world it would be able to issue enough equity to equal the dividends it paid out in order to have more capital to expand its portfolio.

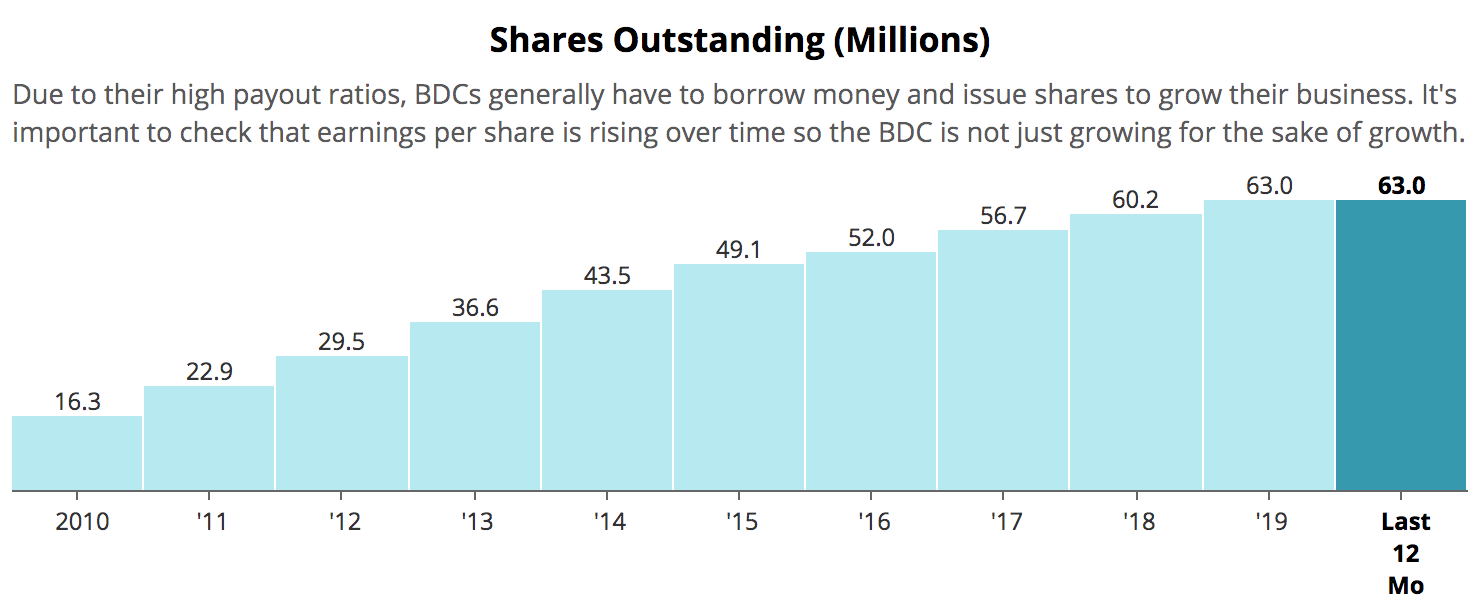

As you can see, the firm's shares outstanding have steadily increased over the years, providing permanent capital with which to support growth of its investment portfolio.

Source: Main Street Capital

That financing strategy won't work with a stock price trading below net asset value per share, but the company's been here before, too. During the financial crisis, Main Street's share price fell as low as $9.50 while its net asset value ended 2008 at $12.20 per share.

If Main Street's valuation never recovers and the firm desires to continue growing, management could eventually have to make a tough call between continuing the current dividend (which leaves little to no excess investment income today) or taking on more leverage.

With that said, management runs the business conservatively and with a patient long-term view. Barring an unprecedented wave of bankruptcies across its portfolio companies, a dividend cut would be surprising at this stage.

A lot of fear is in MAIN's stock price, and we will get a better feel for reality when the company reports earnings in May.