Digital Realty's Near-Term Outlook Clouded by Tighter Financing Markets

Higher interest rates and tightening lending standards spurred by stress in the banking sector are clouding the outlook of Digital Realty (DLR), one of the world's largest owners and operators of data centers.

Many current and prospective tenants, including well-known tech firms like Meta, are trying to cut costs and temper growth initiatives that may impact near-term demand for data centers.

For example, Amazon wrote on Thursday that growth is slowing at its cloud-computing business AWS as more companies scrutinize their costs. Cloud customers account for about 40% of DLR's revenue.

Additionally, DLR's attempts this year to finance $2.5 billion in development projects by selling non-core properties are complicated by this more constrained environment, making it harder for prospective buyers to arrange financing.

(The REIT only retains around $400 million of cash flow annually after maintenance capital expenditures and paying dividends – not enough to cover development costs alone.)

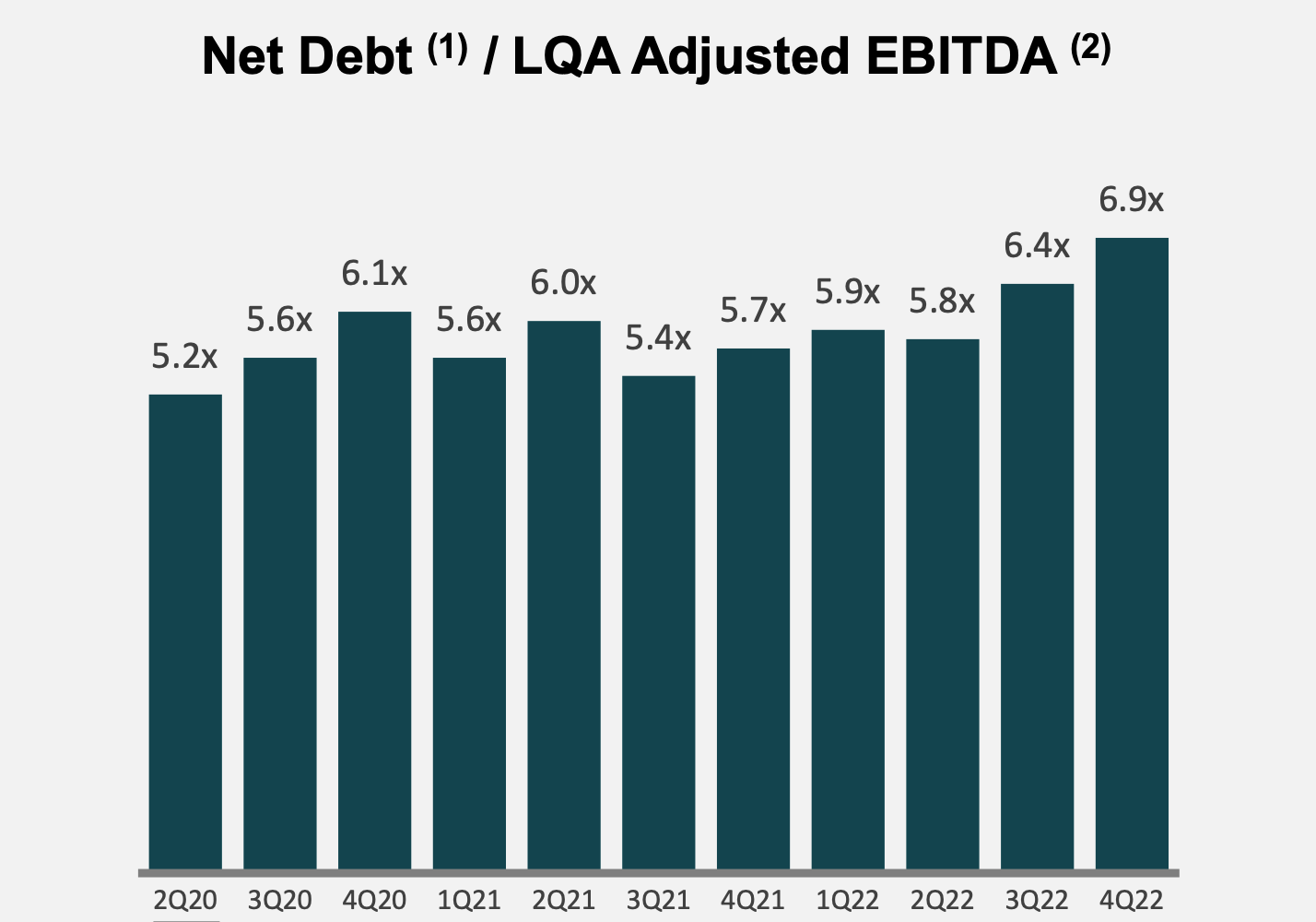

If fewer buyers emerge and DLR fails to raise enough capital through disposals, management may need to decide if it's comfortable adding more debt to the balance sheet, despite a desire to get leverage below 6x.

Source: Digital Realty Investor Presentation, March 2023

These latest challenges have proved frustrating for investors and management since rent prices were finally showing signs of stabilizing after nearly eight years of annual contraction, which we addressed in more detail in our last update.

We recommend investors refer back to that article for a bigger-picture outlook for DLR outside of the disruptions created by the currently challenged financing environment.

In reaction to these burgeoning headwinds, DLR elected to forgo raising the dividend in the first quarter of this year, as has been the REIT's cadence for over a decade.

While the data center landlord has several quarters ahead to raise the payout and preserve the firm's 18-year dividend growth streak, we've decided to follow management's lead and take a more tempered stance by downgrading DLR's Dividend Safety Score from Very Safe to Safe.

That said, DLR still provides an interesting consideration for conservative investors with long-term perspectives and the patience to endure some near-term uncertainties.

Data centers are likely to remain cash cows since they are critical to many industries in the modern economy, including financial services, technology, and manufacturing.

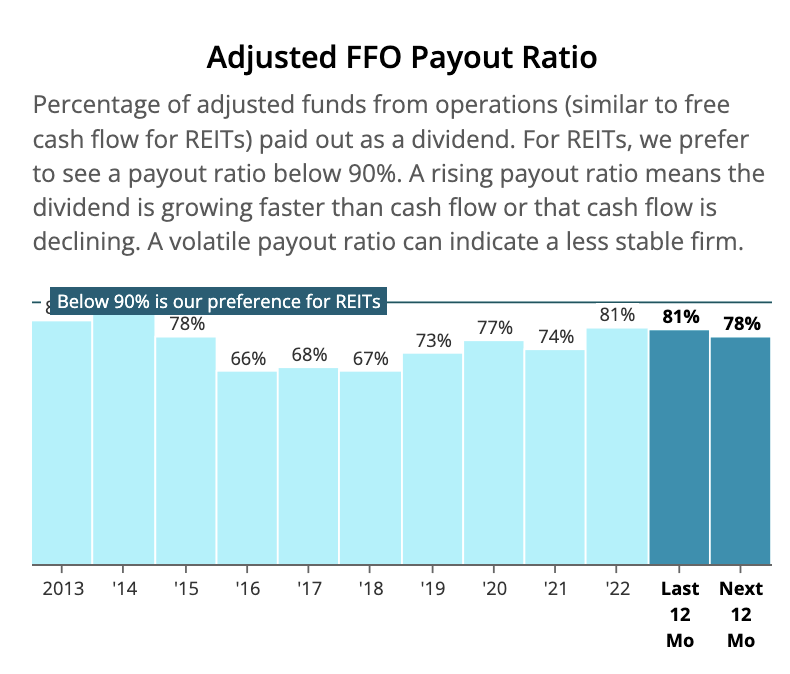

The firm's healthy payout ratio is another appeal, suggesting DLR has some flexibility to maintain the dividend while adapting to an evolving marketplace.

Source: Simply Safe Dividends

Even so, we would be more comfortable if the BBB-rated firm could make progress in reducing debt – which could happen if rising rent prices persist and the REIT's latest batch of development projects come online and start generating income.

Overall, despite the noted challenges, we feel confident in the REIT's dividend profile and ability to maintain its prominent role in the industry.

We will continue to monitor Digital Realty's non-core property dispositions and occupancy changes and provide updates as needed.