Neither of these investment grade-rated firms paid dividends or were very popular holdings amongst income investors. But these events have caused bank investors to wonder if more dominoes will fall, and whether the banks they own remain on solid footing.

We reviewed 59 of the most relevant bank stocks to assess their exposure to the factors (high dependence on uninsured deposits, flighty base of depositors, large unrealized investment losses) that caused SVB and Signature to fail.

We also analyzed which banks could face the greatest headwinds if regulations become tougher at smaller banks to address these risk factors.

While visibility is admittedly low with no real-time data on deposit outflows, most of the 59 banks appear somewhat insulated from these issues, especially in light of policy makers' emergency measures to restore confidence in banks and soothe near-term liquidity strains.

Assuming the Fed's actions (more on that below) minimize the probability of widespread bank runs, we do not anticipate changing many Dividend Safety Scores in response to these events outside of the downgrades we issued this week for First Republic, Zions, and UMB Financial.

More downgrades are possible if new information on deposit trends, capital levels, and financial contagion emerges that suggests bigger problems at play.

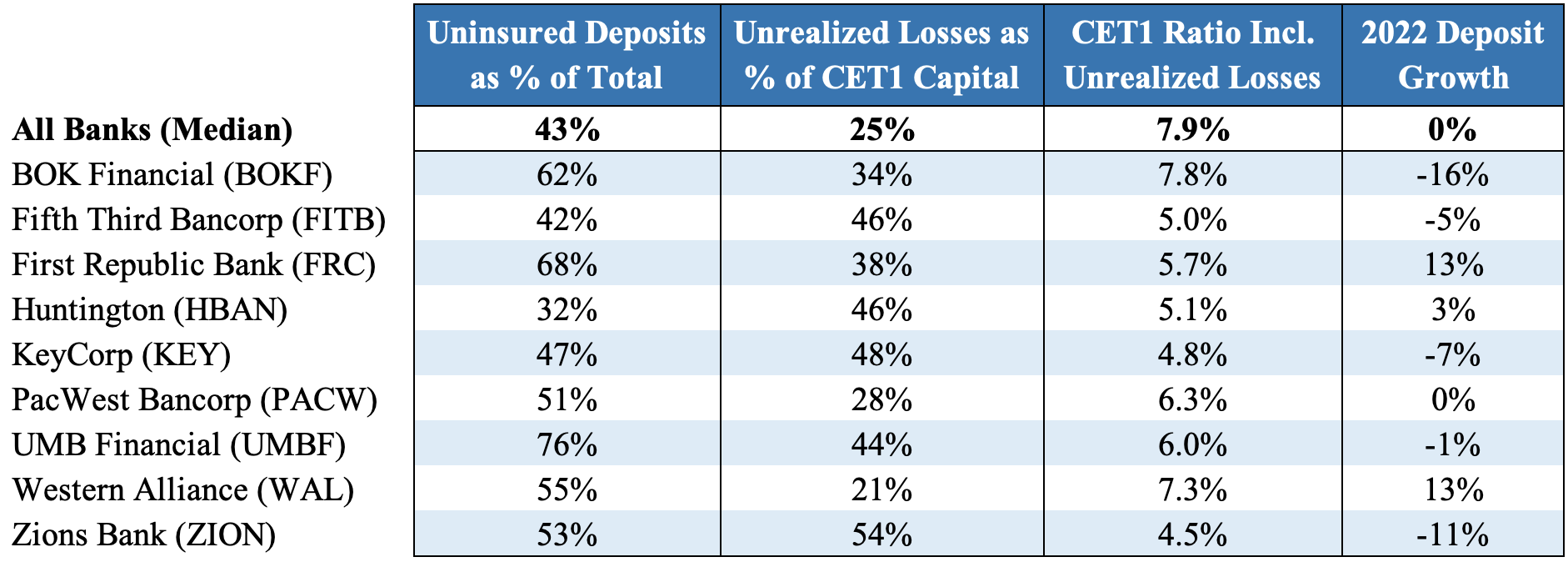

That said, these are the banks (in alphabetical order) that have a higher mix of uninsured deposits, larger unrealized investment losses, and/or more exposure to tougher regulations.

Note that due to data limitations, we didn't consider any hedges a bank might have in place to provide some protection against interest rate fluctuations (and the unrealized losses they have caused). This could give our analysis a conservative bent.

Ally Financial (ALLY)

BOK Financial (BOKF)

Fifth Third Bancorp (FITB)

First Republic Bank (FRC)

Huntington (HBAN)

KeyCorp (KEY)

PacWest Bancorp (PACW)

Synovus Financial (SNV)

UMB Financial (UMBF)

Western Alliance (WAL)

Zions Bank (ZION)

Conservative investors may want to avoid or limit their exposure to banks with higher exposure to these risk factors in case the Fed's stabilization efforts fall short or the shifting interest rate environment causes other unexpected challenges.

You can download all of our risk assessments, plus industry-specific data on each bank, in the spreadsheet below:

Bank investors can use this information to better align personal risk tolerances with their portfolios and position sizes.

This is a fluid situation. A lot could change in the coming weeks and months. Your guess is as good as ours, but we will provide future updates as needed.

Let's take a closer look at the issues rattling the banking sector.

Why SVB and Signature Bank Failed

The downfall of SVB and Signature Bank was not risky loans that soured but rather a mismatch in duration between short-term deposits (liabilities) and the longer-term loans and investments (assets) they fund.

SVB serves primarily tech, venture capital, and private equity companies. These businesses saw an influx of funding during the pandemic, causing the bank's deposits to nearly double in 2021.

Similarly, Signature Bank's deposits jumped about 70% in 2021 as deposits from crypto-related businesses (around 20% of total deposits) surged.

Unable to find enough loans to make with this funding, SVB and Signature stuffed a lot of this money into U.S. Treasuries and other government-backed debt securities with minimal credit risk but maturity dates years away, making their values more sensitive to changes in interest rates.

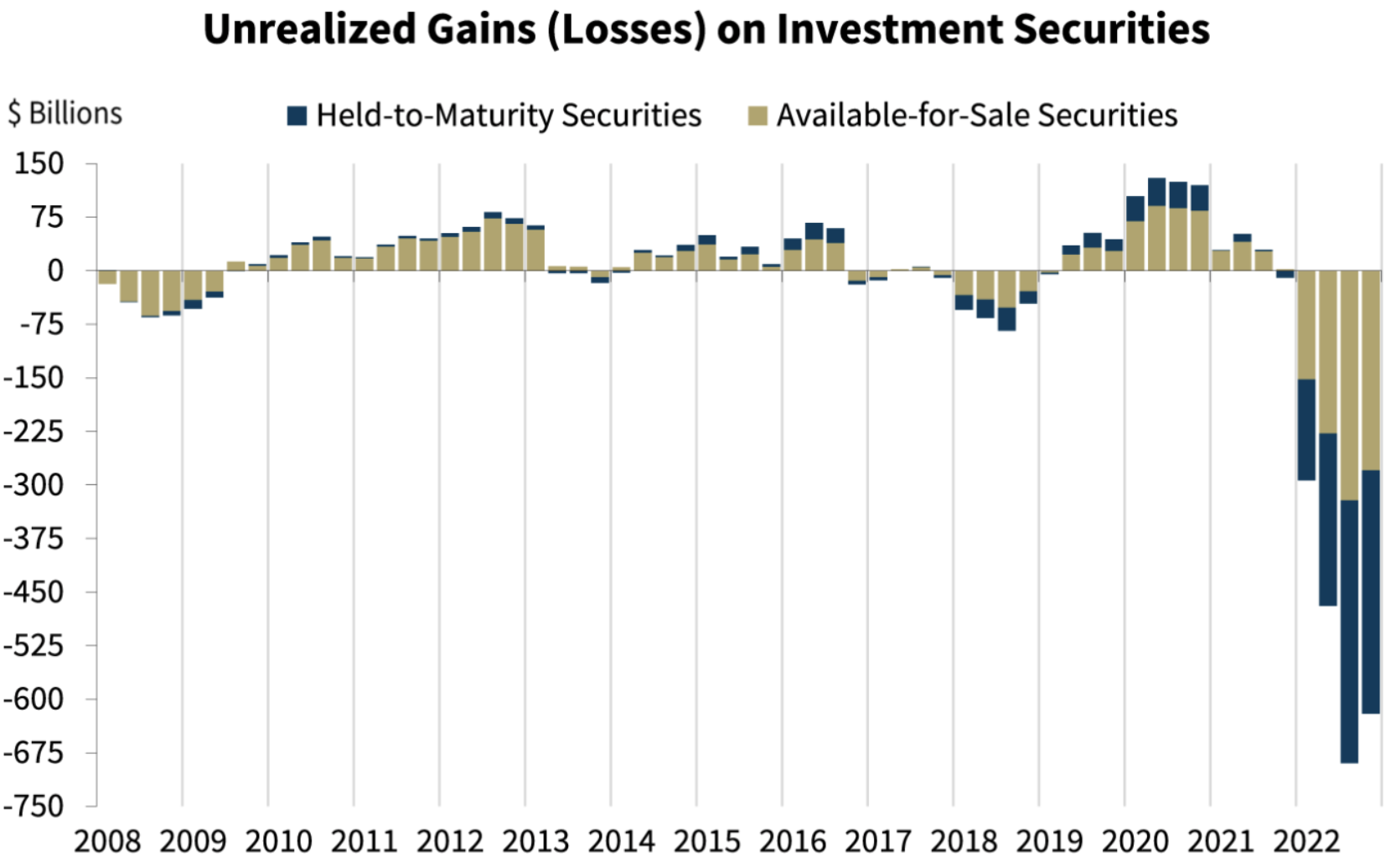

Shortly later, the Fed began its aggressive interest rate hikes to combat inflation, battering the value of longer-term bonds. The chart below from the FDIC shows the jump in unrealized losses on investment securities held across the banking industry due to higher rates.

Source: FDIC

These losses would never be realized if banks could hold their debt investments through maturity, when safe bonds get paid back in full. But they could be forced to sell at a loss if enough customers demand their deposits back at the same time.

In 2022, SVB's deposits fell around 10% and Signature's deposits dropped 17% as venture funding slowed and many tech-focused customers began drawing down cash deposits to finance their businesses.

This forced SVB to sell some of its investments on March 8, locking in a loss and leading the bank to try and raise capital to shore up its financial position.

Panic ensued since the unrealized losses of SVB's investment portfolio exceeded the firm's common equity (banks are highly leveraged by nature), creating a scenario that could wipe out the company if enough customers pulled their deposits at the same time.

This is exactly what happened since the FDIC only insures up to $250,000 per depositor per bank. Nearly 90% of deposits at SVB and Signature were uninsured, causing customers to run for the exits as they lost confidence in the safety of their banks and created a self-fulfilling prophecy.

The Fed, FDIC, and Treasury Department stepped in Sunday night, March 12, in an attempt to calm investors and prevent other bank runs this week.

Their announced emergency measures included the guarantee of all uninsured deposits of SVB and Signature and the ability for banks to take one-year loans from the Fed using their debt investments valued at par as collateral, reducing the need to sell investments at a loss.

That said, as noted earlier, visibility is low. A crisis in confidence that results in a run on deposits is enough to bring down most banks, especially those with a high mix of uninsured deposits from flightier clientele.

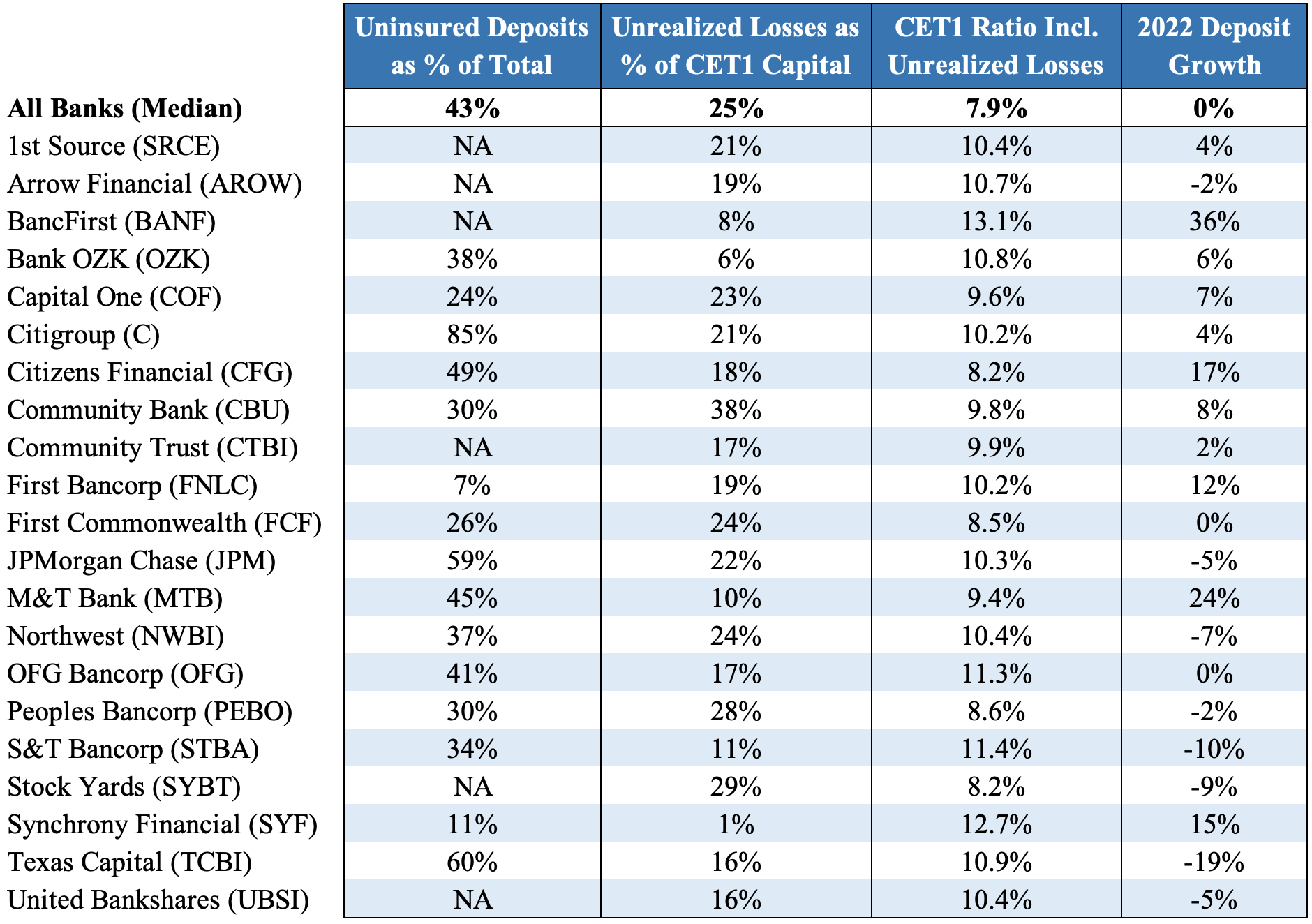

Exposure of Regional Banks to Uninsured Deposits and Unrealized Losses

Compared to other banks, SVB and Signature maintained the highest proportions of uninsured deposits (by far) and had more concentrated exposures to deposits from early-stage tech, crypto, and venture-backed businesses.

Deposit outflows from these more speculative commercial accounts started picking up in 2022, and both banks had unrealized investment losses that would eat into a significant share of their common equity tier 1 (CET1) capital if sales were forced to meet a run on deposits.

Source: Simply Safe Dividends, Bank Filings

CET1 capital is the most loss-absorbing form of capital since it primarily consists of a bank's common stock and retained earnings. Most regional banks are required to maintain a CET1 to risk-weighted assets ratio of at least 7% to ensure they can weather economic cycles.

Unrealized investment losses are not counted against regional banks' CET1 capital. But if they were, a change regulators may be keen to make, we estimate SVB and Signature would have had inadequate CET1 ratios.

These metrics (and others) are available for all other 59 banks in our spreadsheet:

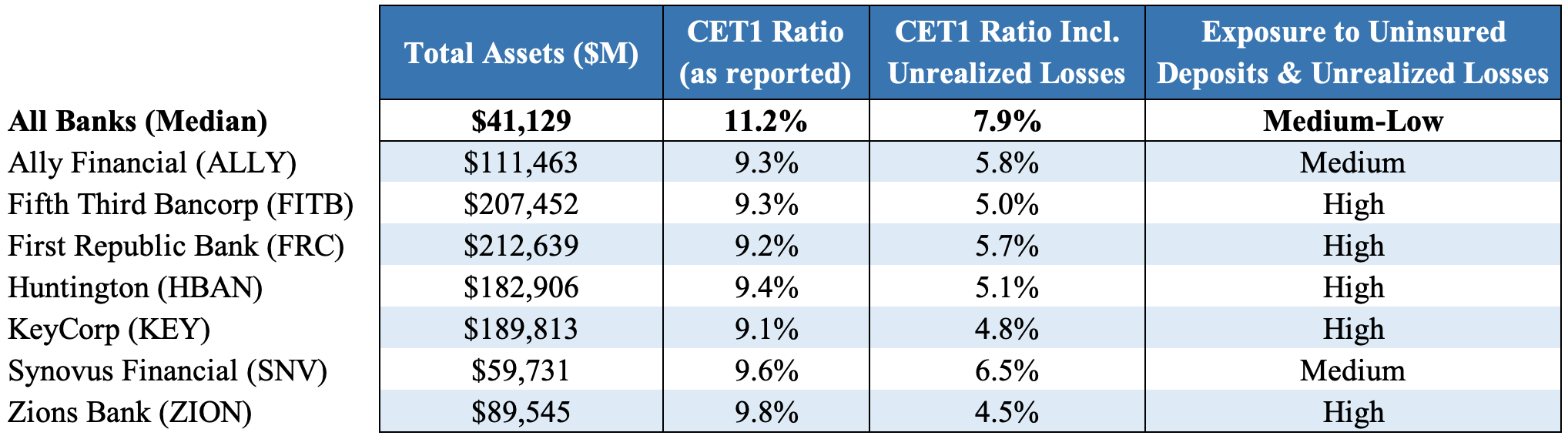

After reviewing capital levels, unrealized investment losses, deposit trends, and more, here's how we assessed the exposure levels of the 59 banks to the issues that brought down SVB and Signature.

Lists are ordered alphabetically by bank name.

High Mix of Uninsured Deposits and Unrealized Losses

Source: Simply Safe Dividends, Bank Filings

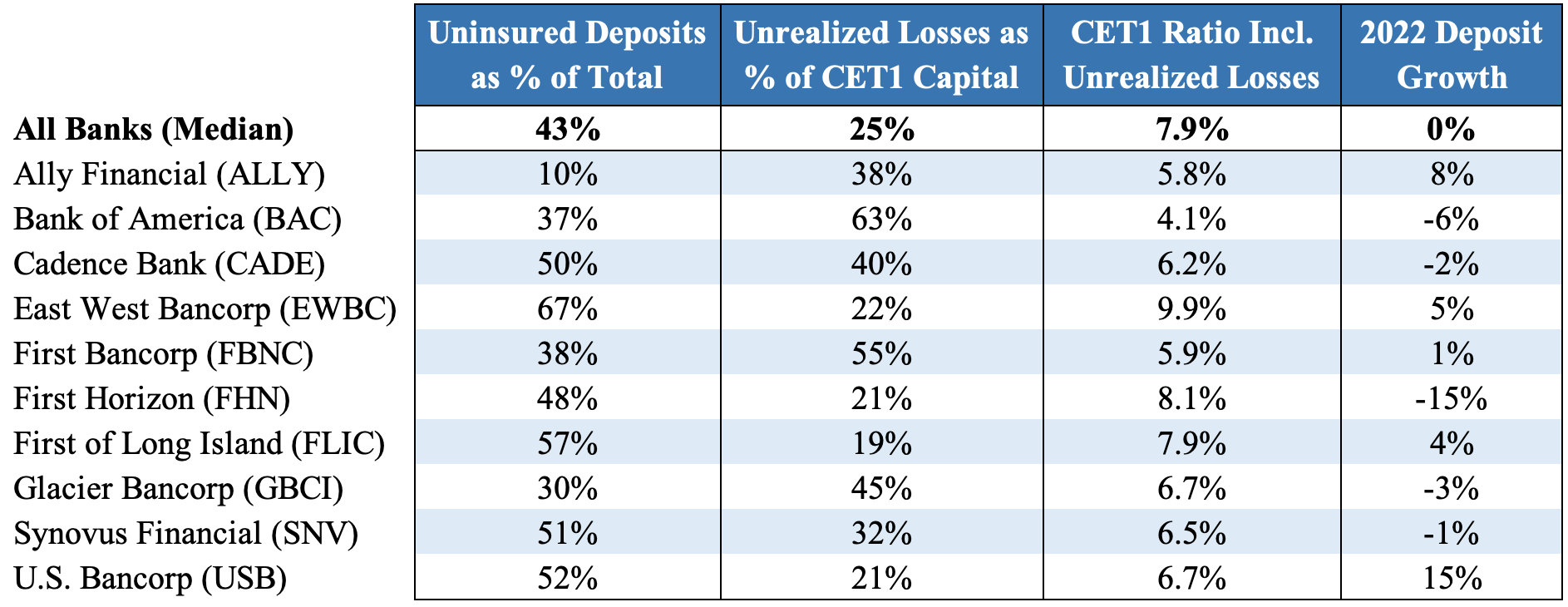

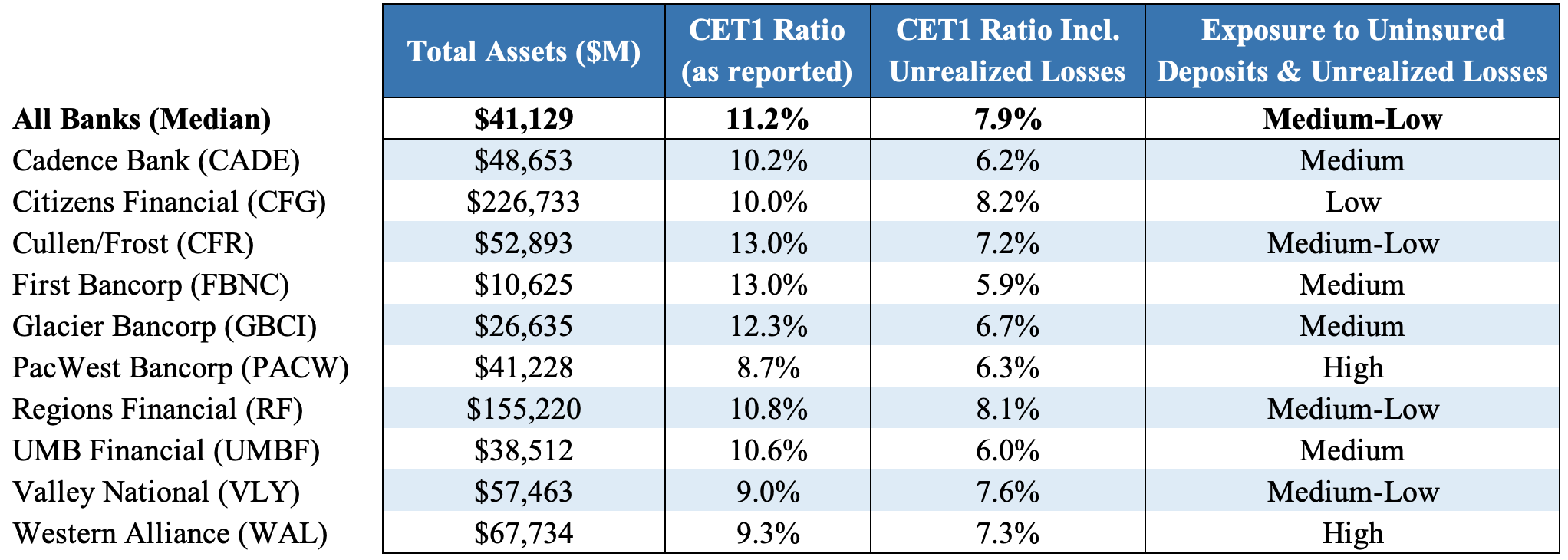

Medium Mix of Uninsured Deposits and Unrealized Losses

Source: Simply Safe Dividends, Bank Filings

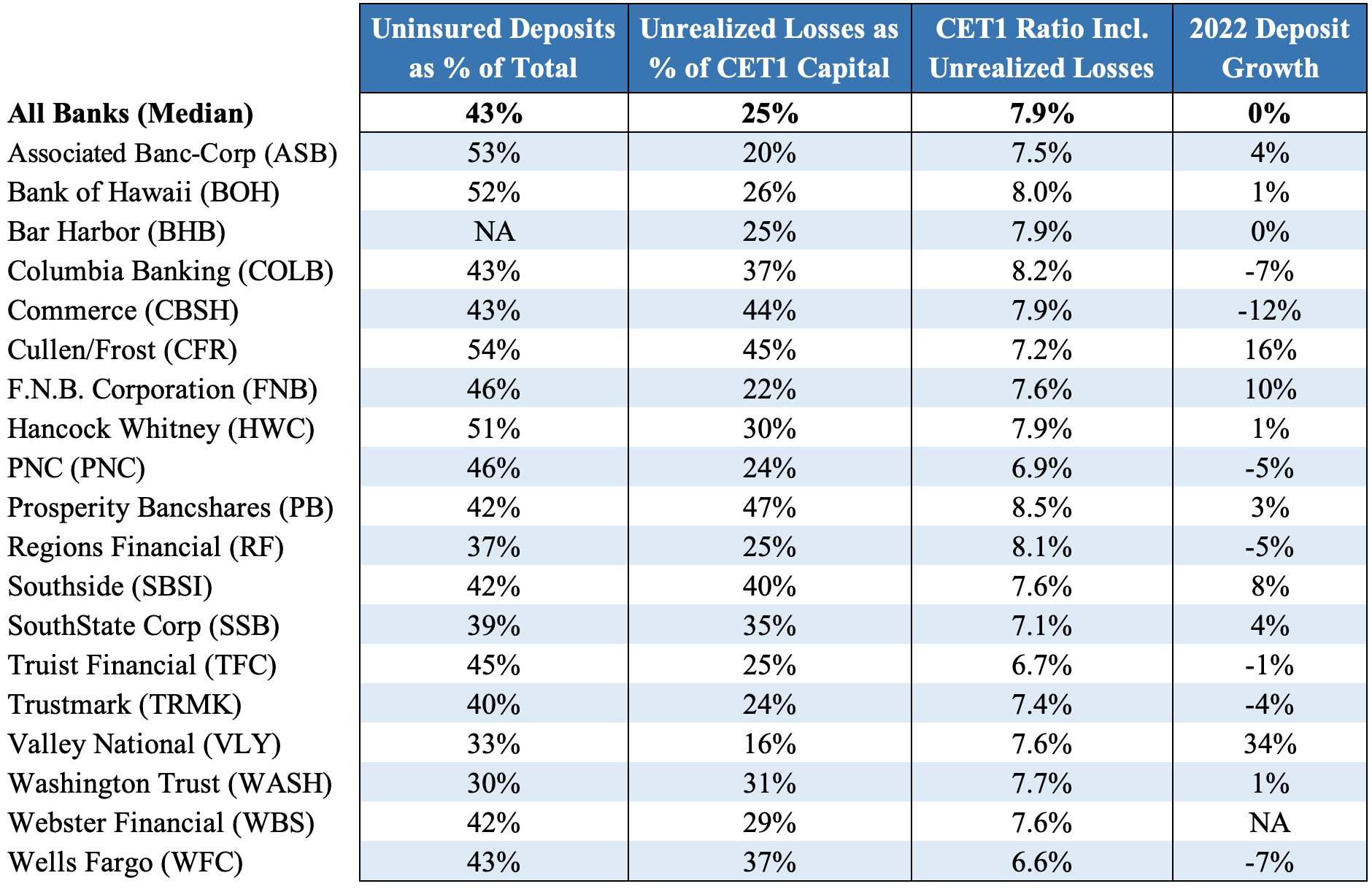

Medium-Low Mix of Uninsured Deposits and Unrealized Losses

Source: Simply Safe Dividends, Bank Filings

Low Mix of Uninsured Deposits and Unrealized Losses

Source: Simply Safe Dividends, Bank Filings

Looming Regulatory Risk and Higher Funding Costs May Reduce Earnings Power

The Wall Street Journal suspects banks with $100 billion to $250 billion in assets (SVB and Signature fall in this group) will be in the crosshairs as these firms currently escape some of the strictest requirements.

While this is all speculation right now, it would not surprise us to see the accounting for unrealized investment losses change to count at least some portion against a bank's capital. This would discourage the reach for yield that took place, albeit after the fact.

Moving the minimum CET1 ratio requirement higher for midsize banks could be another consideration. Major banks like Citigroup and JPMorgan in 2022 needed to maintain CET1 ratios above 11-12% compared to 7% for most regional banks.

If this played out, some regional banks would need to raise more capital and shrink their exposure to certain risk assets to comply, potentially diluting shareholders and reducing their earnings power. Compliance costs would presumably move higher as well.

Smaller banks may continue to fly under the radar, though. Across the 59 banks we analyzed, 36 had total assets near $50 billion or less, with 15 of them sitting below $10 billion in size.

These smaller, community-focused banks do not pose systemic risk and can hopefully continue to escape stricter regulatory requirements.

Looking at the size of each bank and its estimated CET1 capital ratios after including gross unrealized investment losses, here are the firms we think have higher exposure to tighter regulations.

The lists are ordered alphabetically by bank name.

High Exposure to Potentially Tougher Regulations

Source: Simply Safe Dividends, Bank Filings

Medium Exposure to Potentially Tougher Regulations Most of these banks may be small enough to avoid stricter regulations, but their lower CET1 ratios after accounting for unrealized investment losses create some uncertainty if the accounting rules used to measure CET1 capital change.

Source: Simply Safe Dividends, Bank Filings

The remaining 42 banks in our spreadsheet are deemed to have low exposure to future regulatory changes.

Again, you can view all of this data in our spreadsheet here:

In addition to increased regulatory risk, smaller banks may see higher costs as they fight to retain their deposits in a rising interest rate environment.

About one third of a typical bank's deposits are noninterest-bearing accounts. Clients may be more inclined to seek alternatives that provide some yield on their excess cash balances.

Depending on how long short-term rates remain elevated, and how competitive rival banks become in fighting for deposits, this shrinks the margin a bank earns as deposits represent the vast majority of funding for regional banks.

This isn't an overnight concern, but with many bank loans and securities carrying fixed interest rates, we will monitor trends in bank profitability.

Closing Thoughts on Bank Turmoil

Well-managed banks mint money by gathering low-cost deposits from consumers and businesses and lending them out at higher interest rates.

Sounds simple enough, but this leveraged model breaks down if deposit outflows become unmanageable. This can be driven by a loss of confidence in a bank's financial strength as SVB and Signature have reminded the industry.

The issues that hit SVB and Signature seem unique given the makeup of their largely uninsured, tech-oriented deposit bases.

But it is unsettling to see the average bank has racked up a gross unrealized investment loss equal to 25% of its common equity capital. And rates could keep climbing from here.

Most of those losses will hopefully never be realized as the Fed tries to calm anxious depositors. We will know a lot more over the next month as banks report earnings and disclose their latest deposit levels.

Focusing on banks with the strongest capital ratios and deposit bases can provide some protection for investors who seek opportunity in this complex industry and understand the risks, including the potential for more regulation and lower profitability across midsize banks.

We will continue monitoring the banking sector and provide updates as needed.