Rising Funding Costs Squeeze First of Long Island's Dividend Coverage

With roots tracing back to 1927, First of Long Island has served the banking needs of businesses and consumers on Long Island and in New York City for nearly a century.

Despite its lengthy history, First of Long Island operates only around 40 branch locations. This focus reflects the bank's conservative management and disciplined growth, which has enabled the micro-cap stock to pay higher dividends for over 25 consecutive years.

While the community bank has maintained strong credit performance across its loan book and held onto its deposits (around 40% are uninsured) despite recent industry stress, the Fed's interest rate hikes have hurt First of Long Island's profitability.

Rising rates have pressured banks to pay deposit holders higher yields to retain their money. First of Long Island has felt a bigger pinch compared to the average bank because it depends more on lending activities (over 90% of net revenues) and leans more on variable-rate wholesale funding (in addition to core deposits) to finance its loans and investments.

Meanwhile, most of First of Long Island's loans and investment securities have fixed interest rates and do not mature or reprice for at least a few years. The result is a shrinking net interest margin, or spread between interest earned and interest paid as a percentage of assets.

First of Long Island's net interest margin fell from 2.74% in the fourth quarter of 2022 to 2.34%, one of the largest sequential declines we have seen across our coverage universe and reversing progress made in recent years.

Source: Simply Safe Dividends, Company Filings

First of Long Island recently entered into an interest rate swap and repositioned part of its investment portfolio to combat margin pressure by reducing the duration mismatch between its assets and liabilities. (The amount of loans and securities repricing within one year nearly doubled to 21% of the total.)

However, sustained margin improvement will take time and could remain elusive if the Fed keeps rates dialed up to combat persistent inflation.

Management said it best on First of Long Island's April 28th earnings call:

The margins of community and small regional banks generally do not respond well to a 475 basis point rate shock and big yield curve inversions. Add concerns over recent bank failures and the cost of interest-bearing liabilities is escalating rapidly, and margin compression is generally beyond analyst expectations...

Reversing the decline in net interest income and margin will take time for assets repricing to catch up to liability repricing or until the Federal Reserve Bank reduces short term rates.

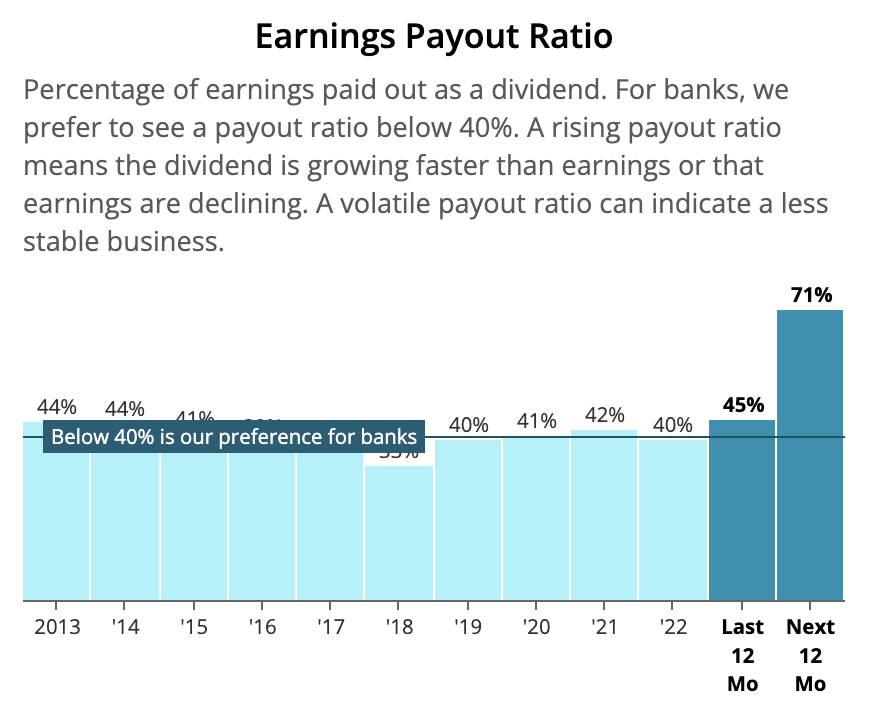

For now, higher funding costs and lower margins are expected to result in enough earnings pressure to send First of Long Island's payout ratio north of 70% in the year ahead, marking its highest level in at least a decade.

Source: Simply Safe Dividends

Fortunately, the bank continues to maintain healthy capital levels (even after accounting for unrealized investment losses), so the dividend seems unlikely to face the chopping block at this time. Management even kept the door open for potential buybacks this quarter.

That said, we are downgrading First of Long Island's Dividend Safety Score from Safe to Borderline Safe until the bank's net interest margin and payout ratio improve.

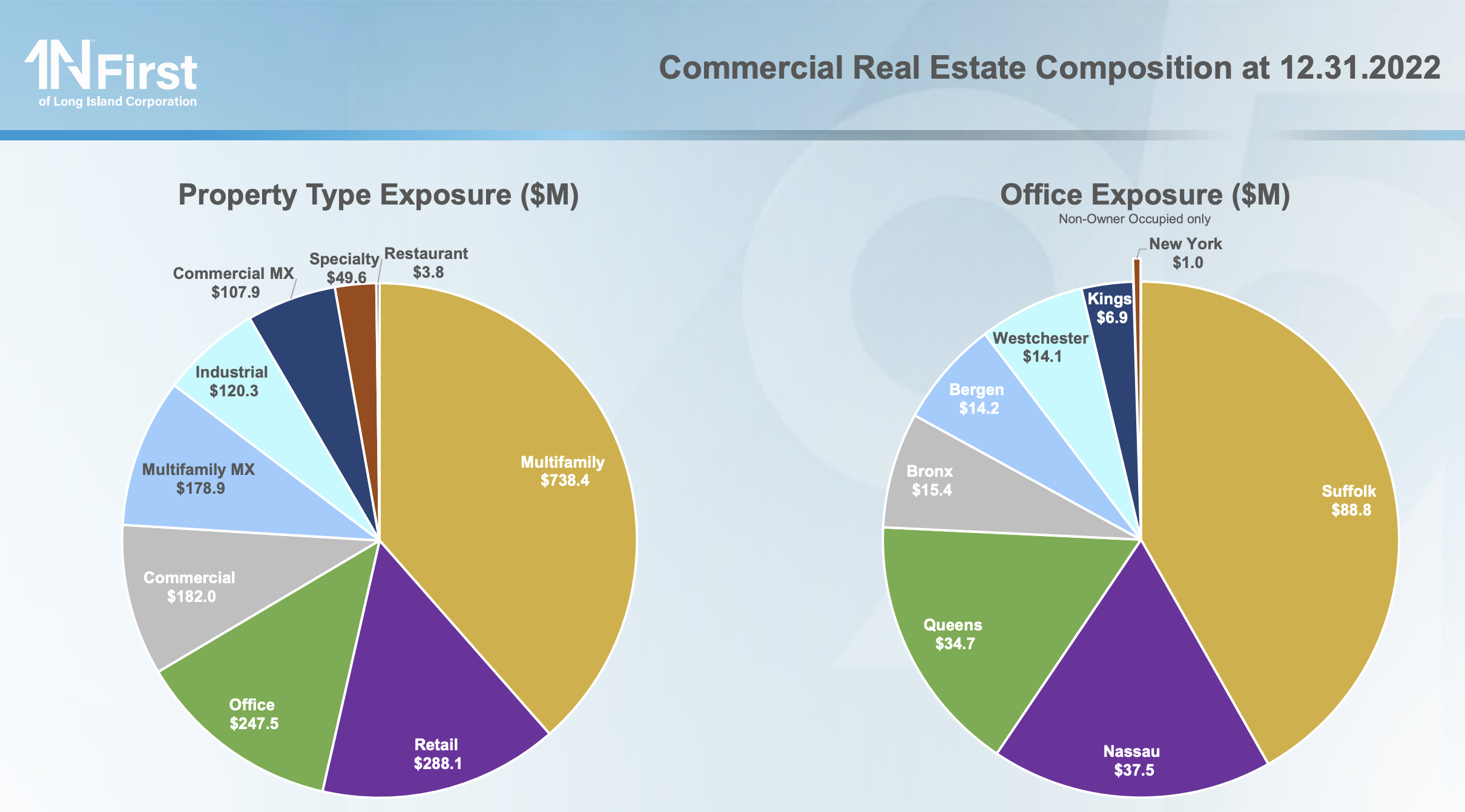

The funding cost outlook becomes fuzzier with each passing month that inflation remains above the Fed's long-term target. Should higher-for-longer interest rates coincide with a recession that weighs on commercial real estate (around 60% of FLIC's loans; minimal Manhattan office exposure), management could feel pressure to retain more capital.

Source: First of Long Island Investor Presentation

If we held shares of First of Long Island, we would probably maintain our position. Importantly, the bank's deposit base has remained steady (management even noted $15 million of new deposits from Signature Bank and First Republic), and the yield curve won't remain unfavorable forever.

However, investors considering First of Long Island need to be comfortable with the firm's less diversified business mix, geographic concentration in Long Island (especially commercial real estate), and higher funding cost sensitivity to the Fed's future interest rate changes.

We will continue monitoring First of Long Island's performance, providing updates as needed.