J&J's Dividend Remains Safe Despite Top Court's Refusal to Hear Baby Powder Appeal

The U.S. Supreme Court on Tuesday denied Johnson & Johnson's request to appeal a 2018 ruling in Missouri that its talc-based baby powders helped cause ovarian cancer, keeping the healthcare giant on the hook to pay $2.1 billion to 22 women.

This eye-popping payout may seem especially alarming since J&J at the end of 2020 faced claims from 25,000 other plaintiffs (up from 17,900 in 2019) making similar allegations about the firm's body powders.

Coupled with an expected liability of around $5 billion to settle litigation related to Johnson & Johnson's role in the opioid crisis, some investors wonder if these legal costs could balloon enough to threaten the dividend.

Despite this week's setback, which highlights the wide range of liability outcomes attached to the claims against the company, we expect Johnson & Johnson's dividend to remain safe and growing.

J&J's scale and vast financial resources provide a comfortable margin of safety for the firm to address a variety of liability scenarios without jeopardizing the dividend.

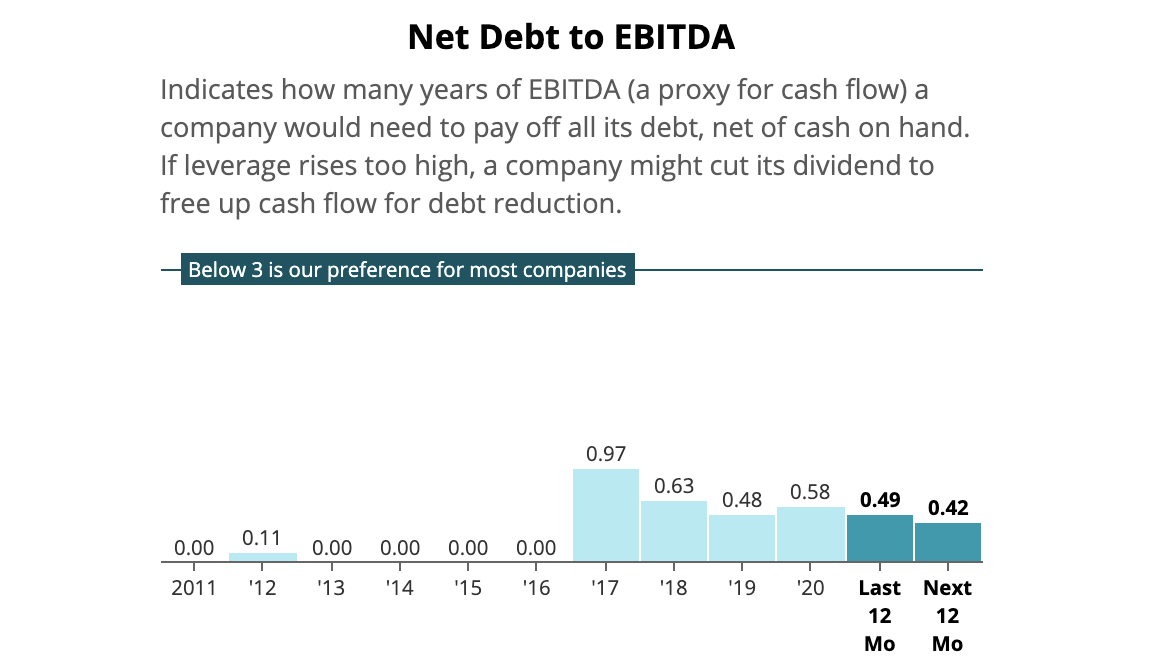

Johnson & Johnson generates nearly $10 billion of annual cash flow after paying dividends and holds approximately $25 billion of cash (compared to $34 billion of debt), earning the company a stellar AAA credit rating from S&P.

This sturdy foundation, plus continued access to low-cost capital, positions J&J to absorb substantial liabilities without impairing its balance sheet or ability to generate plenty of excess cash flow after paying dividends.

For example, if talc powder and opioid litigation triggered a $20 billion liability that the firm financed with debt, we estimate J&J's net debt to EBITDA leverage ratio would increase by just 0.6x.

This could cause Johnson & Johnson's credit rating to drop a couple notches. However, the company's leverage would remain at low levels that provide flexibility for acquisitions and continued returns of capital to shareholders.

Source: Simply Safe Dividends

But how large could the talc liabilities reach, especially in light of Johnson & Johnson's recent rejection by the U.S. Supreme Court?

While acknowledging there is a fairly wide range of outcomes, we would guess $10 billion to $15 billion is a reasonably conservative estimate (and would come in below the $20 billion combined liability for talc and opioids we used in our leverage example above).

There aren't many great precedents to review. The closest might be Bayer's ongoing efforts to settle 125,000 claims (five times as many as J&J faces) alleging the company's Roundup weedkiller product causes cancer.

The German manufacturer of chemicals and pharmaceuticals has agreed to settle existing claims for roughly $10 billion and proposed another $2 billion to cover future claims, but a deal is not yet finalized.

Meanwhile, the largest drug settlement of all time was $3 billion in 2012. And across all industries, only three settlements have ever topped $8 billion (major tobacco companies in 1998, BP's 2016 oil spill, and Volkswagen's emissions scandal in 2016).

This makes J&J's $2.1 billion loss in Missouri all the more startling, but its steep cost per plaintiff (22 women) shouldn't be scaled across the other 25,000 powder-related claims against the company.

Roughly $1.5 billion of this reward was for punitive (rather than compensatory) damages, which can differ in application from state to state and have occurred in just 6% of civil cases that result in monetary award.

J&J probably won't face these damages in most of its other cases, especially as it works to settle cases to avoid going to court. In fact, the firm in October 2020 reached its first major settlement to resolve over 1,000 other baby powder cases for more than $100 million.

This works out to a settlement of about $100,000 per case and implies a total liability of $2.5 billion if all 25,000 existing claims were resolved at this rate.

Several years ago, Wells Fargo analyst Larry Biegelsen wrote a note to clients stating the highest per-case settlement the firm has seen was $280,000 each. Applying this rate across all 25,000 existing claims would suggest a total liability of $7 billion.

Throwing out another projection, Bloomberg in July 2020 estimated that settling all the outstanding talc cases could cost J&J as much as $10 billion.

This week's news cementing J&J's $2.1 billion loss in Missouri could push talc liabilities somewhat above that range, but Bloomberg's estimate still seems in the right ballpark as long as the number of claims does not increase significantly from here.

Overall, J&J's scale, predictable cash flow, and strong balance sheet, plus the size of historical settlements, suggest the firm's talc liability is unlikely to threaten the dividend, which management raised by 5% in April.

Directing billions of dollars towards legal matters could restrict some firms from investing in initiatives to increase their long-term earning power, but J&J's solid financial health should allow it to continue plowing forward with its capital priorities.

We will continue monitoring Johnson & Johnson's legal developments and provide updates as needed.