Magellan Remains Positioned to Preserve Distribution Despite Disappointing Guidance

Magellan on Tuesday reported earnings, closing out a year which management described as having "the most challenging industry and economic conditions experienced in our 20-year history as a public company."

Magellan's units slumped more than 4% on the update after management's guidance indicated that this year may not be much better.

The firm's distributable cash flow (DCF) fell 20% in 2020, and Magellan's guidance called for DCF to decline another 2% this year.

A gradual recovery in fuel demand and the recent completion of various expansion projects will help buoy cash flow, but these factors aren't expected to fully offset continued weakness in crude oil transportation and blending profits.

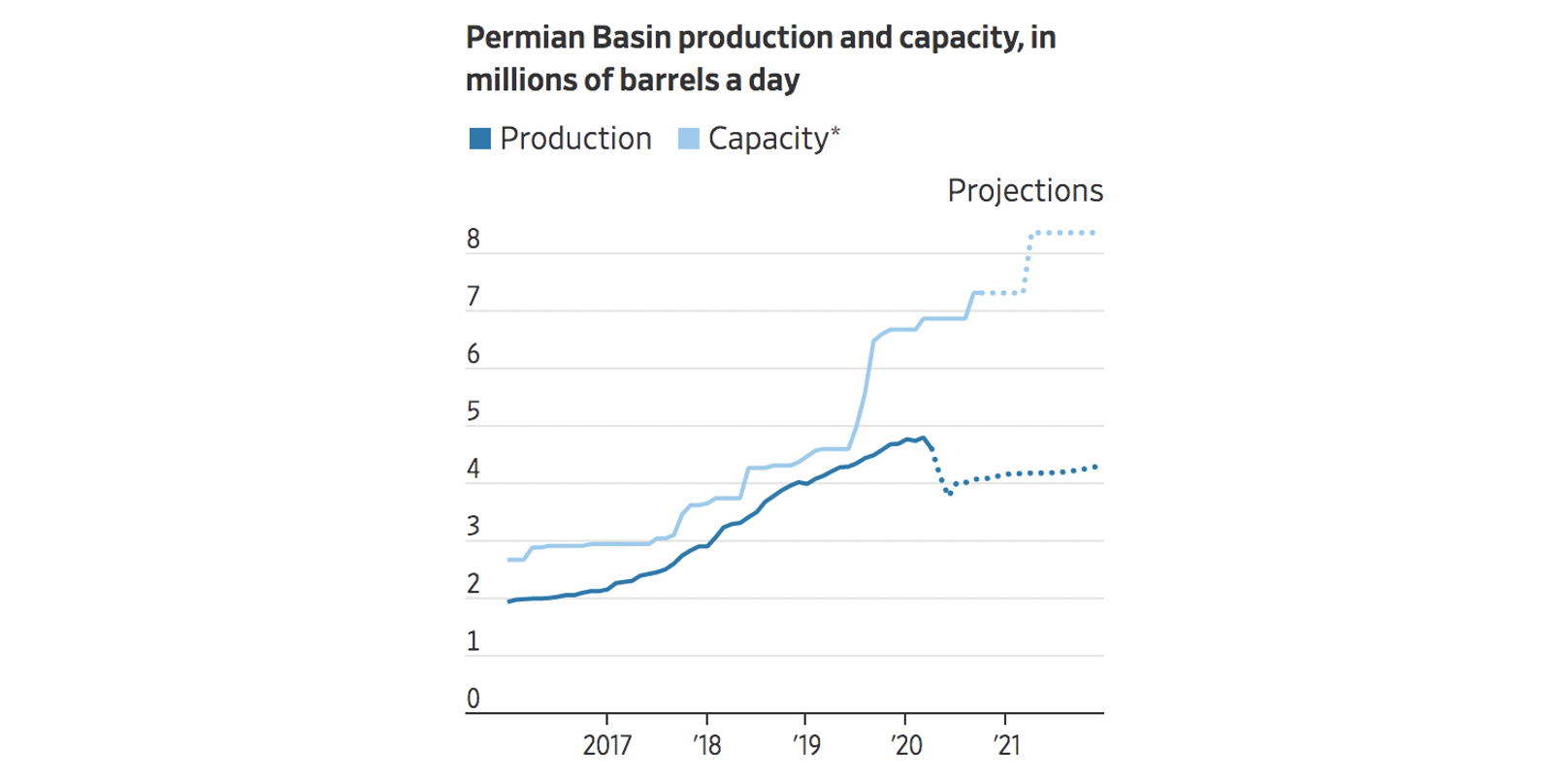

Magellan's crude oil segment (34% of operating income) consists mostly of long-haul pipelines providing outlets for production in the Permian Basin.

While these assets are generally secured by long-term take-or-pay commitments, low oil prices have triggered a decline in drilling activity. This has hurt higher-priced spot shipments and pressured volumes and rates as contracts come up for renewal.

Magellan's crude oil segment saw operating profits plunge 28% in the fourth quarter, and investors remain anxious about excess supply denting the economics of pipelines going forward, especially in the Permian.

Pipeline operators aggressively added capacity in America's largest oil basin in anticipation of many years of strong production growth. The pandemic flipped that thesis upside down as drillers slashed their capital spending to the lowest level seen in 15 years.

Producers are now estimated to be using only about half of the available pipeline capacity for Permian oil, according to sources cited by The Wall Street Journal. That's down from utilization as high as 96% in early 2018.

Source: The Wall Street Journal

If oil production in the Permian fails to return to much higher levels, Magellan could struggle to retain sufficient shipping volumes at fair rates as more contracts expire over the next five years.

For now, management expects lower volumes and rates to cause the crude oil segment's profits to fall by $60 million in 2021, representing a decline of around 12%.

Magellan's blending business accounted for only around 5% of profits prior to the pandemic but has also delivered a big hit to the firm's DCF.

This commodity business earns a margin based on the price of gasoline versus the price of butane. The pandemic-driven plunge in fuel prices caused margins to be cut in half from 2019 through the fourth quarter of 2020.

Management expects blending margins to be at a historical low in 2021, which will result in a nearly $50 million decline in profits compared to 2020. Until gasoline demand moves higher, driven by an increase in travel, this business could remain weak.

Magellan will bank on a continued recovery in its refined products segment (66% of operating income) to help offset these pressure points.

This core business transports and stores refined petroleum products such as gasoline and diesel fuel. The pandemic hurt this historically stable segment by reducing non-essential travel, causing fuel demand to plunge.

After refined product volumes fell 9% in 2020, Magellan expects shipments to rise 13% this year. Increased availability of vaccines should help travel and economic activity rebound, and the firm put new pipelines into service the last two years which should see their volumes ramp.

While the company's short-term outlook is admittedly murky, management believes Magellan's distribution will remain covered by cash flow in 2021.

Distribution coverage for 2021 is expected to be 1.1x, little changed from 1.13x in 2020 and representing a DCF payout ratio of about 90%.

If all goes according to plan, Magellan will generate excess cash of $100 million after paying distributions. That's enough to cover Magellan's expansion capital spending, so the firm does not need to issue any debt or equity to fund its growth.

Management also believes DCF will increase over the next few years as the economy strengthens and as the firm's recent expansion projects increase their gasoline volumes.

As refined products demand rebounds and blending margins return to more historical levels, Magellan expects to return to its target distribution coverage of at least 1.2x.

The firm's balance sheet and liquidity should help protect the distribution too.

Magellan's leverage ratio ended the year at 3.5x, well below management's long-stated limit of 4x and supportive of the firm's BBB+ investment-grade credit rating.

With no debt due until 2025 and $1 billion available under its untapped credit facility, Magellan has solid financial flexibility to wait for a recovery to take hold.

Based on what we know today, we are maintaining Magellan's Safe Dividend Safety Score.

That said, the firm obviously has less margin for error going forward. Magellan's DCF payout ratio has increased from around 80% in recent years to a projected 91% in 2021. Leverage has also risen from 2.8x in 2019 to 3.5x today.

Given some of the challenges that could continue pressuring its crude oil segment, it's especially important that demand for refined products continues rebounding this year. We would consider downgrading Magellan's rating if the firm encountered any material setbacks which could cause its distribution to no longer be covered by DCF.

Looking further out, the energy transition to cleaner fuels creates uncertainty across each of Magellan's businesses as well. Demand for refined products is expected to gradually decline over the course of decades, but we would also revisit Magellan's Dividend Safety Score if this transition appeared to be playing out more rapidly.

Finally, it's worth noting that Magellan announced it does not plan to convert from a master limited partnership to a corporation. While a larger pool of investors can own stakes in corporations, management believes that any valuation upside would be more than offset by the corporate income taxes the firm would owe.

This news could have disappointed some investors who believed it was in Magellan's best interest to expand its investor base, but remaining a partnership provides more support for the distribution. You can review Magellan's corporate conversion analysis here.

Overall, Magellan's latest results and guidance highlight that the pandemic continues to weigh on the energy sector. The firm's cash flow and balance sheet still support the current distribution this year, and we will continue monitoring today's headwinds to ensure that also remains the case further out.