EQM Merger With Equitrans Results in Effective 68% Distribution Cut

EQM Midstream Partners, LP (EQM) announced plans to merge with its general partner Equitrans Midstream (ETRN) in an all-stock transaction, continuing the trend of MLP simplifications. Each unit of EQM would be exchanged for 2.44 shares of ETRN stock.

The exchange ratio represents only a 3% premium based on EQM's average price over the 20 days leading up to the deal's announcement. Making matters worse for income investors, it also means EQM unitholders will face an effective distribution cut of nearly 70%.

EQM paid annual distributions of $4.64 per unit, whereas ETRN's annual dividend was lowered to $0.60 per share. After receiving 2.44 shares of ETRN stock for every unit they hold, EQM investors will earn a comparable dividend of $1.464 per unit (a 68% cut), representing about an 8.5% yield today.

Whether investors sell now or wait for the merger to close in mid-2020, this transaction will be treated as a taxable event as well. If your cost basis is below the current $17.22 per unit deal value (which could change as it's tied to ETRN's price), then you will have to realize a capital gain.

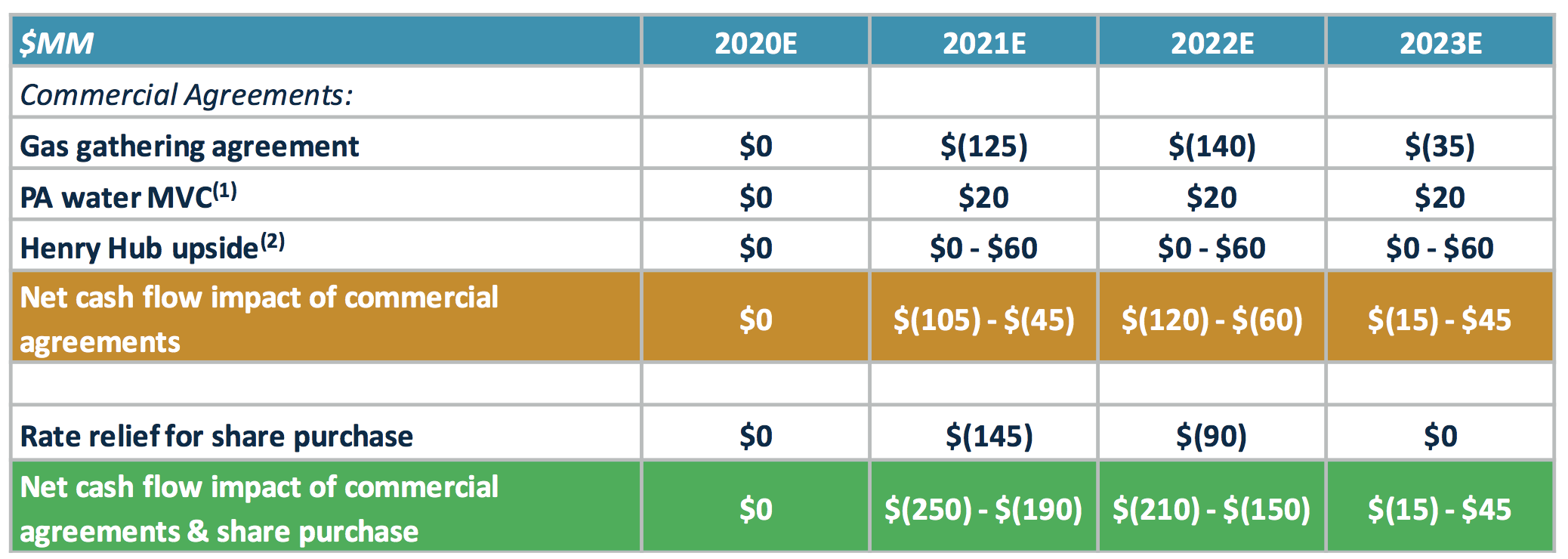

Making matters worse, EQM renegotiated its natural gas gathering contract with its upstream partner EQT Corporation (EQT), which accounts for roughly 70% of EQM's revenue and is struggling in today's weak natural gas price environment.

While the contract was extended to 15 years, improving long-term visibility, EQT will receive rate relief from 2021 through 2023. ETRN is also buying back some of its shares owned by EQT, providing cash and additional rate relief as compensation.

The combined hit could exceed $300 million in each of 2021 and 2022. For context, EQM's distributable cash flow totaled nearly $1 billion in 2019.

Source: EQM Earnings Presentation

The end result of this transaction is a combined company (ETRN and EQM) that will have a much higher leverage ratio of about 5.6x this year, prompting credit rating downgrades from Standard & Poor's and Moody's.

Source: EQM Earnings Release

The company's dividend coverage improved significantly to 2.2x following the dividend cut (EQM's coverage hovered near 1x in 2019), and there's a path to generate enough free cash flow to cover the dividend and all capital spending within a couple of years.

However, the firm's cash flow and deleveraging trajectories depend almost entirely on the beleaguered Mountain Valley Pipeline (MVP) project.

As we discussed in October 2019, this critical project has faced a number of regulatory challenges, delays, and cost increases, which supported the Unsafe Dividend Safety Score we had on the stock. EQM hopes the MVP will come online at the end of this year, and the company's financial health depends on it.

Overall, this merger announcement is obviously a big disappointment for EQM unitholders. ETRN has solid upside if the MVP project finally comes online and improves the firm's cash flow generation and leverage, but there's still plenty of execution risk. ETRN must also continue contending with EQT's poor cash flow outlook given today's weak natural gas prices.

Conservative investors who remain interested in the midstream space may want to consider moving on to other businesses that have greater basin and customer diversification, less project execution risk, and lower leverage. Enterprise Products Partners (EPD) is one such example and has a comparable 7.6% yield following the market's rout this week.