MLP Simplifications: How Times are Changing for MLPs

Master limited partnerships, or MLPs, are a kind of pass-through stock that are favored by many income investors looking for high yields and fast growth.

However, over the past five years, the midstream space (dominated by oil & gas transportation infrastructure) has experienced a painful and prolonged bear market.

The Alerian MLP index, a proxy for the industry, hasn't come close to recovering from its nearly 60% decline from August 2014 to February 2016, which coincided with the 75% plunge in oil prices.

Even factoring in distributions, from August 2014 through May 2019 the Alerian MLP index's has registered a -25% total return while the S&P 500 has gained over 50%.

Despite the price of oil nearly doubling since its February 2016 low, plus the broader stock market continuing to rally, most MLPs have seen their unit prices stagnate, too.

Understandably this has resulted in a lot of frustrated income investors who are wondering whether or not the midstream MLP industry can ever recover.

Let's take a closer look at how this high-yield industry is changing, especially with the number of MLP simplification transactions announced, and what it could mean for the future distribution safety and growth profile of MLPs.

MLP Simplifications Don't Mean The Midstream MLP Industry Is Dying, But Evolving

A five-year bear market might leave some investors fearing the midstream industry faces a secular decline in long-term cash flow. In reality, the industry's growth prospects appear to remain solid, thanks to advanced fracking techniques which continue driving a boom in American oil and gas production.

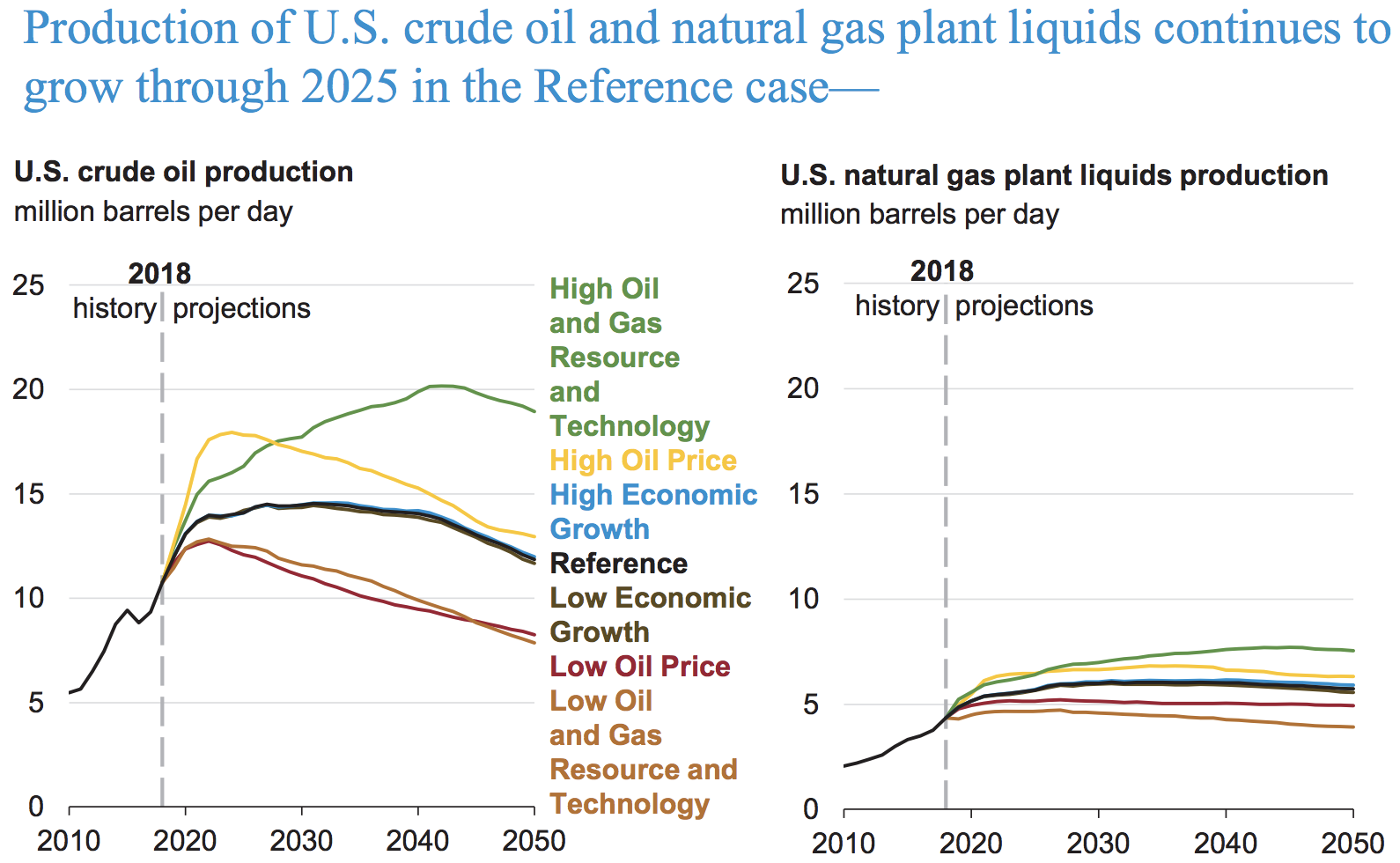

The U.S. Energy Information Administration expects domestic oil and natural gas liquids (NGL) production to grow through at least 2025, and possibly through 2040. Natural gas production is expected to grow steadily through at least 2050, driven by higher NGL export demand from emerging markets like China and India, as well as developed markets such as Japan and the European Union.

Overall, about 33% growth is expected in U.S. oil and natural gas production from 2017 to 2025.

Source: U.S. Energy Information Administration

As a result of growing energy production, consulting services firm ICF believes $800 billion in new North American midstream infrastructure will be needed by 2035, and through 2050 new infrastructure demand could exceed $1 trillion.

Simply put, the MLP industry's fundamentals don't appear to be dying, but the funding and growth model employed by these companies is shifting to a more conservative one that emphasizes financial independence and lower risk.

The classic MLP business model (created in the 1980s by Congress) was characterized by:

Rapid distribution growth (often double-digits)

Low distribution coverage ratios (paying out almost all distributable cash flow)

Substantial equity and debt funding for growth projects (little cash flow was retained due to aggressive payout ratios)

High leverage levels (debt/adjusted EBITDA)

Complex corporate structures (including costly incentive distribution rights paid to the general partner)

However, that business model appears to have been permanently broken by the 2014-16 oil crash. As oil prices plunged, over 300 energy producers, oil field service companies, and pipeline operators in North America went bankrupt.

This created fear in the bond and stock markets about the safety of the long-term contracts underpinning MLP cash flow and distributions. While most contracts were never at high risk, a few MLPs were indeed forced to renegotiate their contracts for less favorable terms.

Meanwhile, the unit prices of MLPs, like those of most energy stocks, crashed, resulting in an unsustainably high cost of equity.

Unit prices plunged again in March 2018 when the Federal Energy Regulatory Commission (FERC), which has the ability to set rates for pipelines, revised a 2005 tax policy to no longer allow interstate pipelines owned by MLPs to recover an income tax allowance in the cost of service customers previously paid for.

As pass-through entities, MLPs do not pay any federal taxes. In other words, they were essentially getting a double benefit on taxes, which was now going to be taken away and thus significantly reduce distributable cash flow for certain MLPs. FERC has since revised its rule change to lessen the negative effect on the industry, but MLP valuations have remained low.

With unit prices crashing and failing to recover, most MLPs were unable to issue new units to fund their capital-intensive growth projects. They had also run their businesses with very high amounts of leverage, limiting their ability to borrow more. Therefore, many MLPs were forced to choose between executing on their backlogs or maintaining their distributions.

Numerous MLPs cut their payouts to retain more cash flow for growth and deleveraging, losing the trust of their core base of income investors who primarily owned MLPs for their stable payouts.

The industry has had to adapt to these challenges, which mainly centered around the struggle to raise affordable growth capital. Many MLPs have responded by taking on substantial corporate restructuring activities including:

Elimination of incentive distribution rights (which sent up to 50% of incremental cash flow to the general partner and greatly increased an MLP's cost of capital) in stock funded buyouts.

General partners acquiring their MLPs (as seen with Kinder Morgan, Enbridge, ONEOK, Tallgrass Energy, Energy Transfer, Valero Energy, and Dominion Energy).

Stock-based mergers between MLPs (which sometimes involves effective distribution cuts) such as MPLX (MPLX) acquiring Andeavor Logistics Partners (ANDX) in a $14 billion deal.

Corporate conversions, in which an MLP converts from a partnership to a corporation with hopes of simplifying its business structure and reducing its cost of capital. In March 2019 Antero Midstream Corporation (AM) changed its tax structure after the general partner acquired its MLP.

Private equity acquiring entire MLPs (typically after a steep payout cut that caused the stock price to trade at extremely low valuations) as seen with Buckeye Partners (BPL) being taken private in a $10.3 billion deal announced in May 2019.

In response to increasing pressure over the past five years, driven by the crash in oil prices, regulatory changes, and U.S. tax reform, the MLP industry continues to shrink and consolidate. Firms are especially focused on reducing their long-term cost of capital and reliance on equity markets for growth funding.

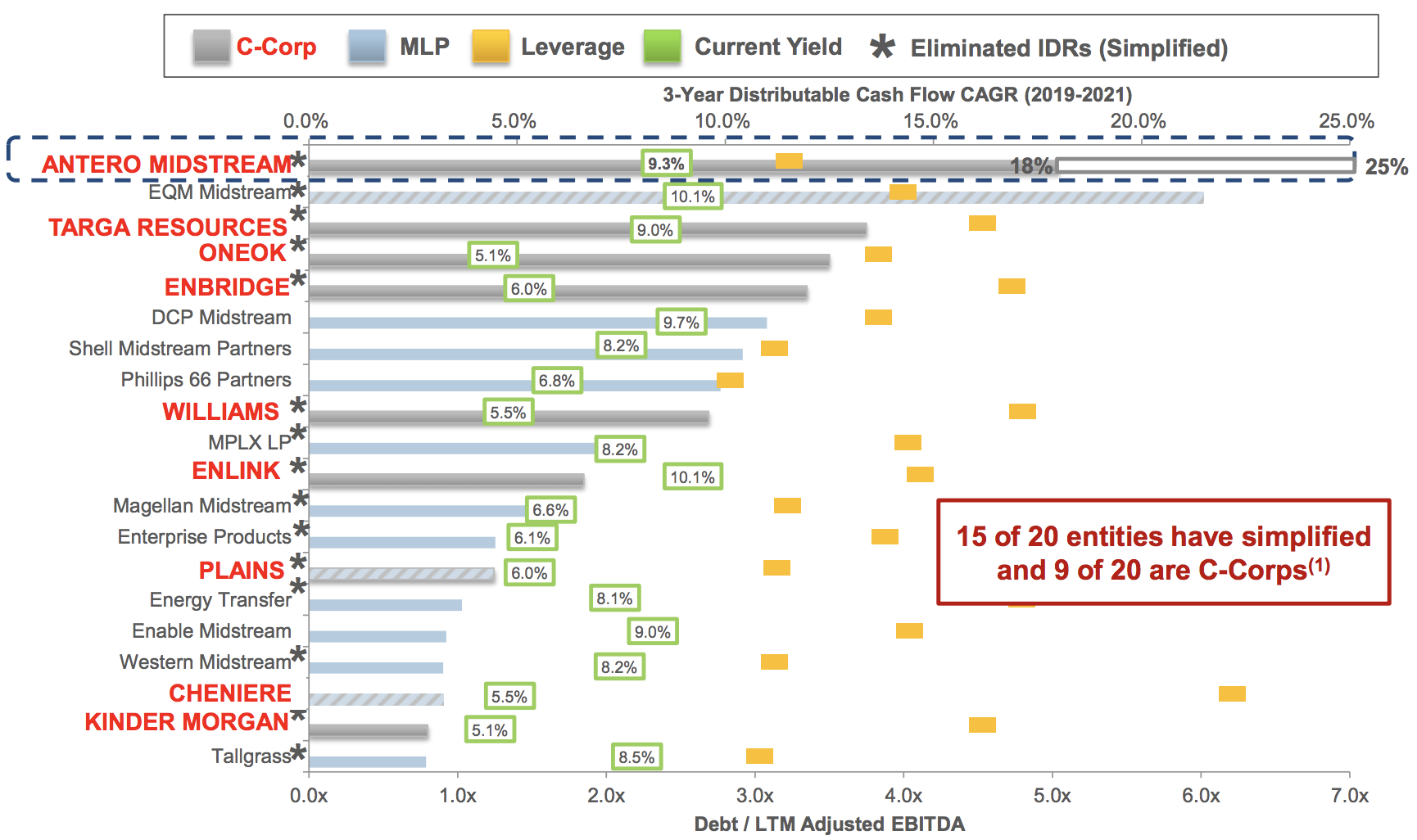

In fact, of the 20 largest midstream stocks by market cap, 15 have eliminated their incentive distribution rights in recent years (and Magellan Midstream Partners did so back in 2010). Nine of these stocks are now corporations paying qualified dividends (1099 tax forms but no deferred tax benefits on payouts) rather than partnerships paying distributions (K-1 tax forms).

Source: Antero Midstream Investor Presentation

Most of the C-Corp conversions are from corporate sponsors buying out their MLPs. The sponsors had used their MLPs as financing vehicles, selling them completed midstream assets in exchange for cash proceeds which could be reinvested into the next growth project or used for deleveraging.

The MLPs would pay for these midstream assets by issuing equity and debt. However, continued weakness in MLP capital markets no longer made this financing strategy viable – the MLP model failed provide the growth capital needed to expand North America's energy infrastructure.

Other C-Corp conversions were executed due to management's belief that a conversion to a corporation might boost the firm's share price.

The theory goes that K-1 tax forms are unpopular with many investors (due to greater tax complexity), and since most ETFs can't own MLPs and the S&P 500 specifically excludes MLPs, greater investor interest and higher share prices could be obtained via such a conversion.

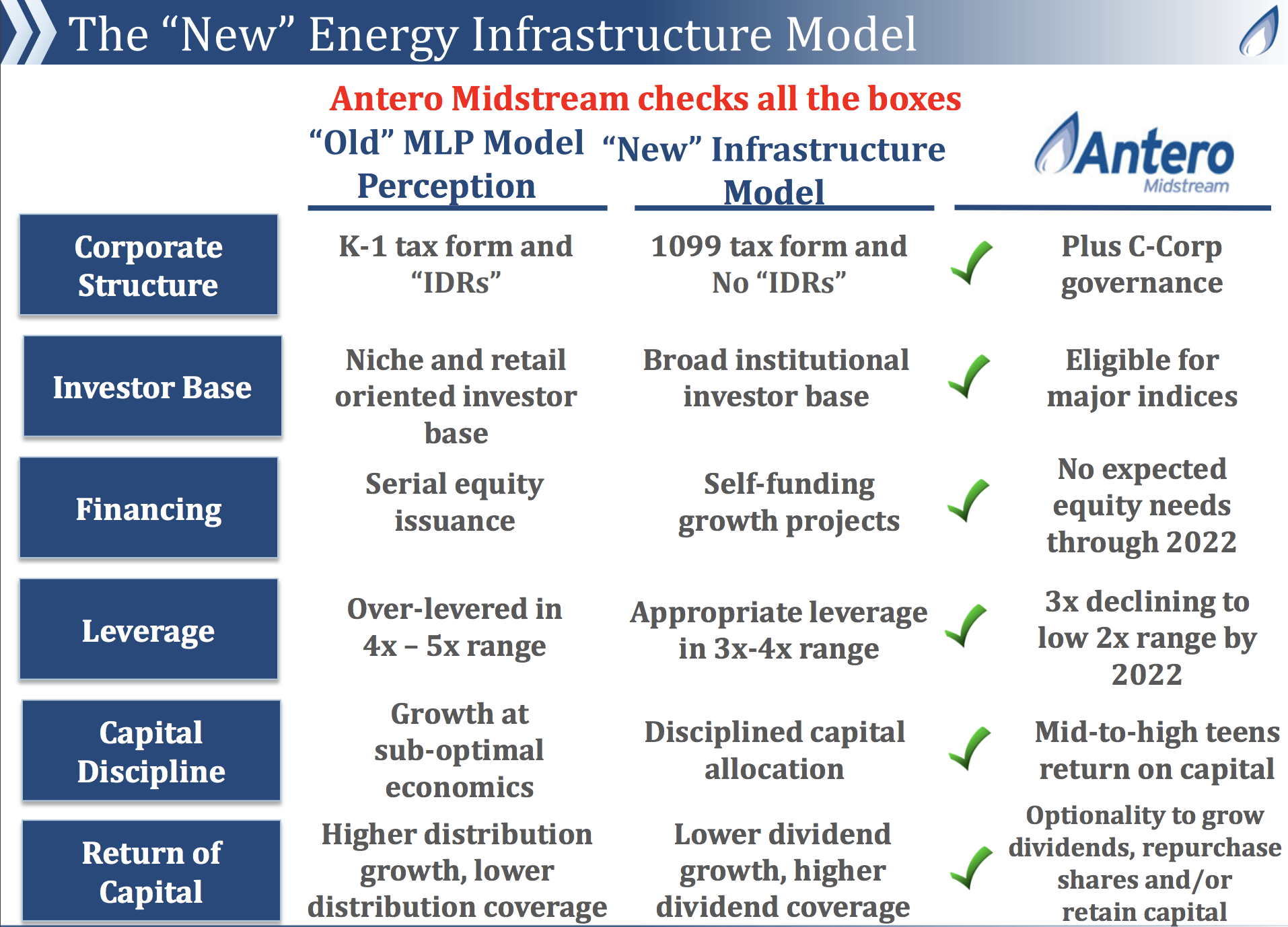

Antero Midstream provided a helpful slide highlighting the benefits it expects to recognize from its recent C-Corp conversion. By simplifying its business structure, the firm hopes to expand its investor base, reduce its long-term tax burden, de-risk its growth financing, and enhance governance and shareholder rights compared to the MLP structure.

Source: Antero Midstream Investor Presentation

The downside to such buyout conversions (which has likely weighed on industry stock prices over the years) is that they often trigger a deferred tax liability. In addition, as Kinder Morgan's 2014 conversion (one of the first of the modern era) showed, cash flow multiples and share prices don't necessarily benefit if investor sentiment remains bearish enough.

This shift in corporate and funding structures, combined with ongoing weak stock prices, has an important implication for midstream investors interested in both MLPs and corporations.

Slower Midstream Payout Growth is Likely Here to Stay

The age of rapid payout growth is likely ending for good, with small and fast-growing midstream firms like Antero Midstream Corporation now guiding for single-digit dividend growth going forward (down from 20+% just last year).

Similarly, EQM Midstream Partners (EQM) was guiding for 15% long-term distribution growth in early 2018. However, after a complex restructuring (that eliminated its IDRs in an expensive stock-based transaction) the firm's guidance was reduced to 6% to 8% long-term payout growth and has now been lowered to just 6%.

Small MLPs like Oasis Midstream Partners (OMP) and Noble Midstream Partners which expect to continue delivering 20% annual distribution growth through 2022 are still seeing weak stock prices and yields frequently above 8%.

The market appears to be signaling its skepticism that management will deliver on its promised 20% long-term payout growth, despite strong balance sheets (leverage of 4.0 or less) and coverage ratios approaching 2.0 (50% distributable cash flow payout ratio, which is strong for this industry).

Skepticism seems justified due to the need for such small MLPs to eventually eliminate their incentive distribution rights through stock funded deals that will significantly dilute existing investors and result in much smaller (though likely still safe) coverage ratios.

The industry's slowdown in payout growth was to be expected given that the drop-down business model, in which MLPs sell new shares to buy assets from their corporate sponsors, isn't possible in a protracted industry bear market where costs of equity are frequently in the double-digits.

Even larger blue-chip MLPs have resorted to slowing their payout growth. A key reason for this, as expressed by management teams at the largest MLPs, is frustration that the equity market isn't rewarding fast distribution and dividend growth as it has in the past.

In recent years well-run MLPs that avoided distribution cuts have succeeded in significantly growing their cash flow and payouts but stubbornly low unit prices have persisted.

These firms have responded by shifting their capital allocation strategy to focus more on self-funded organic growth and even potentially initiate share repurchase plans given the high cash flow yields of their stock.

Self-funding means no longer issuing new stock to fund organic growth projects, but relying entirely on retained cash flow (distributable cash flow minus payouts) and modest amounts of low-cost debt. This strategy allows a midstream company's growth to become independent of its stock price.

For example, ONEOK previously guided for 9% to 11% dividend growth between 2018 and 2021 but management recently pulled back on that guidance. The CFO told analysts on the firm's fourth-quarter 2018 conference call that (emphasis added):

"We acknowledge that many investors and some research analysts have expressed the view that prudent capital allocation in the midstream space is more valuable. Accordingly, many investors do not require as high a dividend growth rate as they did in the past and that alternative approaches to returning capital may be appropriate at some point in the future."

While ONEOK hasn't officially retracted its previous fast dividend growth guidance, it has left itself open to slowing its payout growth so that it too can adopt a self-funding business model (OKE was one of the few large midstream operators that was still open to equity growth funding). That's something that many large MLPs and midstream corporations have done.

For example, since its 2012 IPO, MPLX has grown its distribution every quarter and at over 15% annualized rates. However, it's now growing the payout at 6% in 2019 and focusing on increasing its distribution coverage ratio to allow it to fund organic growth with retained cash flow and reduce its leverage ratio to even lower levels.

Enterprise Products Partners announced plans to shift to a self-funding business model in 2017, which meant a reduction in distribution growth to about 2% (half its historical 4% to 5% rate). Management said its target coverage ratio was 1.5 (allowing it to retain 33% of cash flow to fund growth), which it hit a year early.

In the first quarter of 2019 Enterprise recorded 18% growth in distributable cash flow and a coverage ratio of 1.7, allowing the firm to retain $665 million for funding its growth plans ($2.6 billion annualized retained cash flow).

Enterprise is currently spending about $5 billion per year on capex, meaning that it's far ahead of its goal of funding 33% of growth with retained cash flow. Yet rather than accelerate distribution growth back to historical levels, management authorized a $2 billion long-term buyback authorization.

Similarly, Energy Transfer LP (ET) initially told investors that the 2018 merger of Energy Transfer Equity (the general partner) with Energy Transfer Partners would lead to a much stronger MLP. One with a long-term goal of 4.0 to 4.5 leverage and coverage ratio of 1.7 to 1.9 which would help it retain $2.5 billion to $3 billion per year for growth investments.

The distribution would be frozen until the MLP could reduce its leverage to target levels and obtain an upgrade to its credit rating (currently BBB-, just one notch above junk).

In the first quarter of 2019 Energy Transfer's cash flow grew 36%, its coverage hit 2.07, and it retained $856 million ($3.6 billion annualized) in cash flow after paying its distribution.

However, despite also being well ahead of its self-funding goals, Energy Transfer's distribution has remained frozen for six quarters. Management has said it will consider buybacks instead of large payout hikes in the future, should the market continue to value its units at such a low cash flow multiple.

In other words, the entire midstream industry has been adapting to the new realities of a still bearish market not appreciating improving fundamentals (falling leverage, rising cash flow, stronger distribution coverage).

What does all this mean for income investors interested in the space?

How Income Investors Should Approach Midstream MLPs Going Forward

The traditional midstream MLP structure proved to be inadequate for raising growth capital for many firms. MLPs with the largest backlogs of growth projects, most costly incentive distribution rights, highest leverage, and weakest distribution coverage ratios have had to rethink their business models. Some of them have yet to take their medicine.

That's not necessarily reason to write off the entire midstream MLP industry. Conservative income investors interested in the space just need to focus on firms that have been adapting their business structures and strengthening their fundamentals. Here are some important factors to look for:

Strong distribution coverage ratios (preferably 1.2 or higher)

Healthy balance sheets and investment-grade credit ratings

No incentive distribution rights

Self-funded business models (no dependence on equity markets)

Diversified businesses, large customer bases, and good contract profiles (not too much concentration with one customer and low commodity price sensitivity due to long-term contracts with minimum volume commitments)

Examples of quality MLPs include Enterprise Products Partners and Magellan Midstream Partners. These businesses are run conservatively and do not need access to much external growth capital. As a result, potentially weak MLP valuations do not fundamentally affect their ability to execute, and they seem likely to retain their existing business structures for the foreseeable future.

For investors seeking the same exposure to growing energy production and stable cash flow but without the K-1 tax forms, midstream corporations such as ONEOK, Enbridge, and TC Energy (TRP) are all potentially attractive long-term income investments at the right price.

While slower payout growth might be disappointing to some, it's important to remember that the industry's shift towards a lower-risk, self-funding business model characterized by higher coverage ratios and lower leverage is ultimately a good thing for conservative income investors.