Merck's Spin-off Plan Has Tradeoffs But Dividend Expected to Remain Safe and Growing

On February 5, Merck (MRK) announced plans to spin off its Women's Health and Biosimilar divisions, as well as various legacy branded drugs. Combined, these businesses ("NewCo") account for nearly 15% of Merck's revenue.

Source: Merck Investor Presentation

The spin-off transaction is expected to be completed in the first half of 2021 and will take the form of a tax-free distribution to Merck shareholders of a new publicly traded stock in the new company.

Whenever a company spins off part of its business and shrinks its remaining earnings base, one of the first questions many income investors have is what will happen to the dividend.

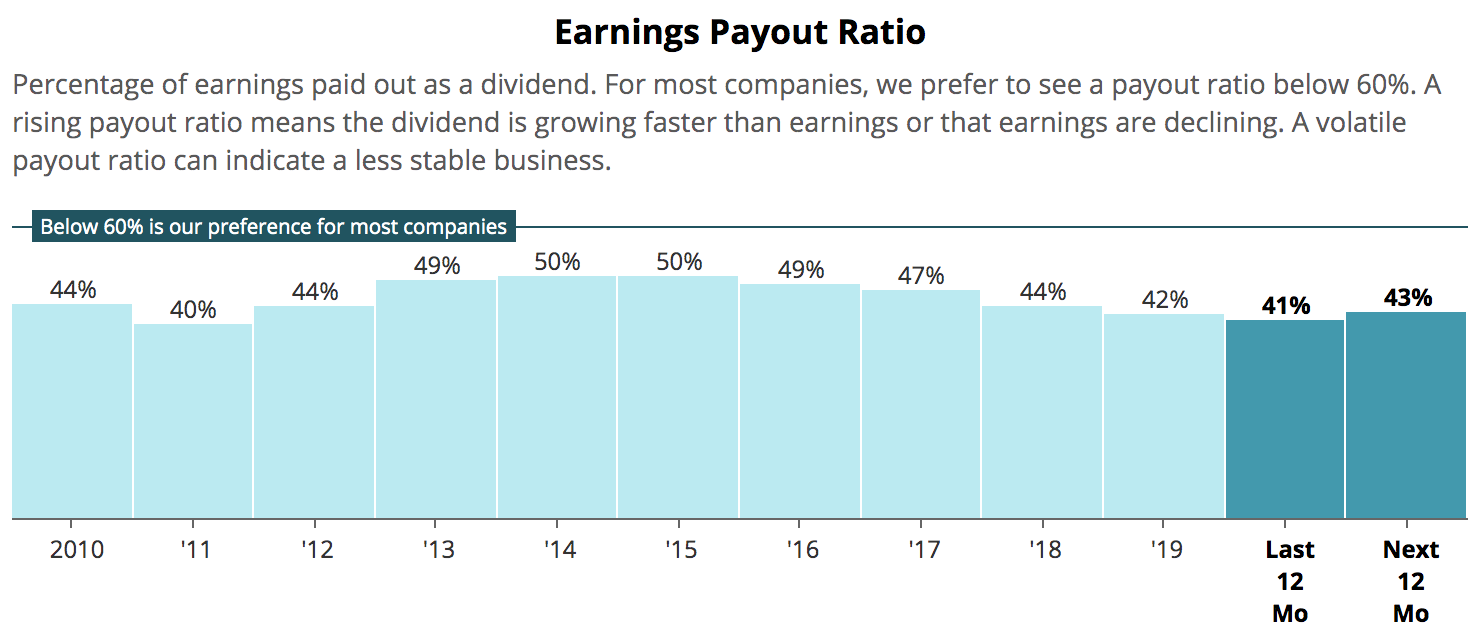

Merck has paid uninterrupted dividends for more than two decades, and that trend will continue. Management has committed to maintain the firm's current $2.44 per share dividend (with growth expected in 2021 and beyond) and targets a 47% to 50% payout ratio going forward.

We estimate the spin-off will reduce Merck's earnings per share by about 10% to 15% once the transaction is completed. Using Merck's pre-spin-off 2020 earnings guidance, that would put Merck's payout ratio right in management's target range this year and only slightly above its current level near 43%.

Source: Simply Safe Dividends

As a result, Merck's dividend will likely grow at about the same pace as its earnings in 2021 and beyond, probably at a mid- to upper single-digit pace.

In addition to Merck's current dividend, shareholders can expect to receive incremental income from the new spin-off, which intends to pay a "meaningful dividend."

Here's what management said on the earnings call:

"We are not lowering the dividend as a result of the spinout of NewCo. We're going to hold our dividend to $2.44, which it is in 2020, and then grow it off of that base, with the goal to get to 47% to 50% as a payout ratio.

So you're actually going to see a maintained dividend growing over time, and then you have the benefit of the incremental dividend that NewCo is going to have. So all in all, you should have overall more dividends if you hold those stocks than we do today."

However, as with many spin-offs, the business units Merck is shedding don't appear to be the most desirable assets.

Management expects NewCo's revenue to be flat to down 8% in 2021, driven by loss of exclusivities of cardiovascular drug Zetia in Japan (10% of NewCo's revenue) and Women's Health product NuvaRing in the U.S. (14% of NewCo's revenue).

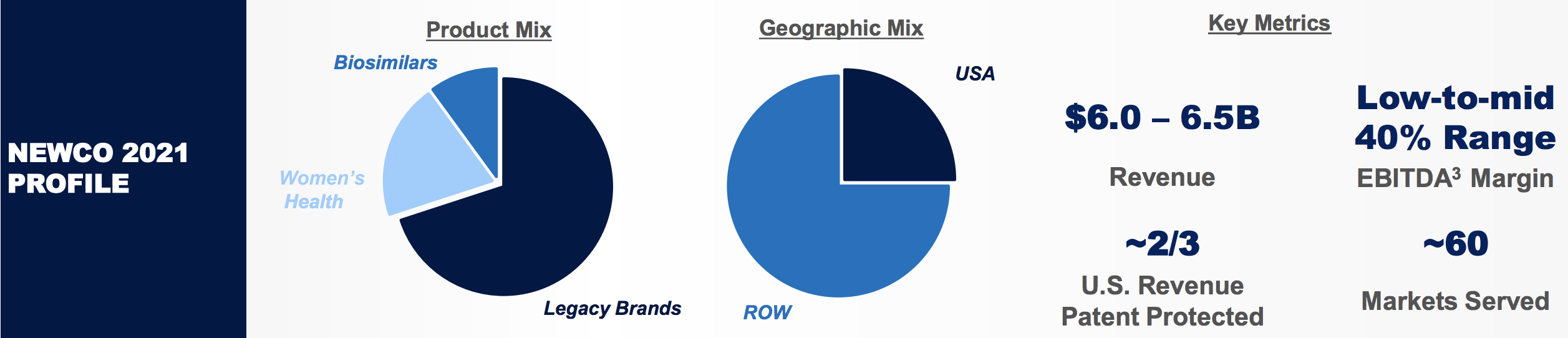

NewCo hopes to achieve low single-digit annual revenue growth thereafter. However, it's hard to have much confidence forecasting a business like this since about 70% of NewCo's revenue will come from Merck's legacy brands.

Most of these legacy branded drugs (in areas such as pain, dermatology, and cardiovascular) are characterized by low rates of growth, and some are set to lose patent protection.

Source: Merck Investor Presentation

Merck talks up growth opportunities in Women's Health (contraceptives and fertility businesses; $40 billion fragmented market) and Biosimilars (similar copies of prescription drugs sold by rivals), but these areas will only account for 30% of NewCo's revenue (with hopes of exceeding 50% by 2024).

Further muddying NewCo's outlook, Merck expects to receive $8 billion to $9 billion through a special tax-free dividend from the new company, adding a pile of debt to NewCo's balance sheet.

We estimate this will cause NewCo's net debt to EBITDA leverage ratio to sit at an elevated level between 3x and 3.5x, limiting the spin-off's financial flexibility and weakening its dividend safety profile.

Finally, it's worth noting that while NewCo generates 15% of Merck's revenue, its operations account for 25% of Merck's manufacturing footprint and 50% of its products and markets. As a standalone business, NewCo's margins will initially fall, and improving its efficiency could be difficult.

As for Merck, management expects the remaining business to improve its revenue growth by up to 1 percentage point annually through 2024. Combined with its leaner operating model, Merck also expects to achieve operating margins of greater than 40% in 2024 (up from 32% in 2019).

The main downside is that Merck's outlook becomes even more dependent on only several drugs. In 2019, Merck's three largest drugs accounted for 39% of its revenue. Without NewCo's revenue, this figure would increase to 45%.

Merck's fast-growing Keytruda drug (used to treat lung cancer, as well as melanoma, head and neck, bladder, and other types of cancer) grew 58% in 2019 to represent 24% of the company's total sales (27% excluding NewCo's revenue).

For better or worse, Keytruda will drive Merck's growth for the foreseeable future. A mega-blockbuster drug like this is great on the ride up. However, Keytruda will eventually be a tough act to follow once it loses patent protection in 2028 and sees its sales erode due to generic and biosimilar competition.

Replacing a product that has potential to generate over $20 billion in annual revenue (representing the industry's top-selling drug and upwards of 40% of Merck's total sales) is no small task.

Merck will need to continue building its pipeline of drugs in the years ahead to help soften the eventual blow. In addition to internal research and development work, the $8 billion to $9 billion of cash proceeds from NewCo provide Merck with optionality to acquire promising drugs for its portfolio.

However, spinning off many of its legacy drugs removes a source of funding. In fact, management acknowledged that NewCo's businesses provided Merck with cash flow which helped fund the development of Keytruda, which is now funding itself (helping justify the spin-off decision).

Generally speaking, we prefer to own pharma companies which have diversified sources of funding and don't overly depend on the success of any single drug. These traits usually result in a slower pace of growth, but they also reduce risk.

With that said, Merck's major brands enjoy favorable patent profiles, providing solid cash flow visibility for the foreseeable future.

Most importantly, Keytruda (24% of 2019 revenue) is protected until 2028. Vaccine Gardasil (8%) doesn't lose exclusivity until 2028 in the U.S. and 2025 in the European Union. Merck's third-largest drug, diabetes treatment Januvia (7%), loses protection in 2022, but that still provides for a couple of years of growth across Merck's other medications to more than offset revenue losses.

Overall, Merck should remain a fundamentally solid business with a safe dividend following its planned spin-off in 2021. The company's drug portfolio will become more concentrated, especially as Keytruda's growth remains strong, but the drug maker's patent situation is favorable, and its financial strength remains excellent (including an AA- credit rating from Standard & Poor's).

If the firm's leverage ticks up following the transaction (management mentioned using the spin-off's tax-free dividend for buybacks rather than acquiring more cash flow), it's possible Merck's Very Safe Dividend Safety Score will be downgraded slightly to the high end of our Safe category. However, we expect Merck's dividend profile to remain suitable for conservative income investors.

The new company that will be spun off appears less attractive (as is often the case) due to its elevated leverage profile and branded drugs that face growth challenges but dominate its portfolio. Merck will disclose more information about this business in the future, but based on what we know today, conservative investors may want to eventually consider cashing out their shares in the spin-off.