Franklin's Dividend Continues to Look Safe But Growth Challenges Seem Likely to Persist

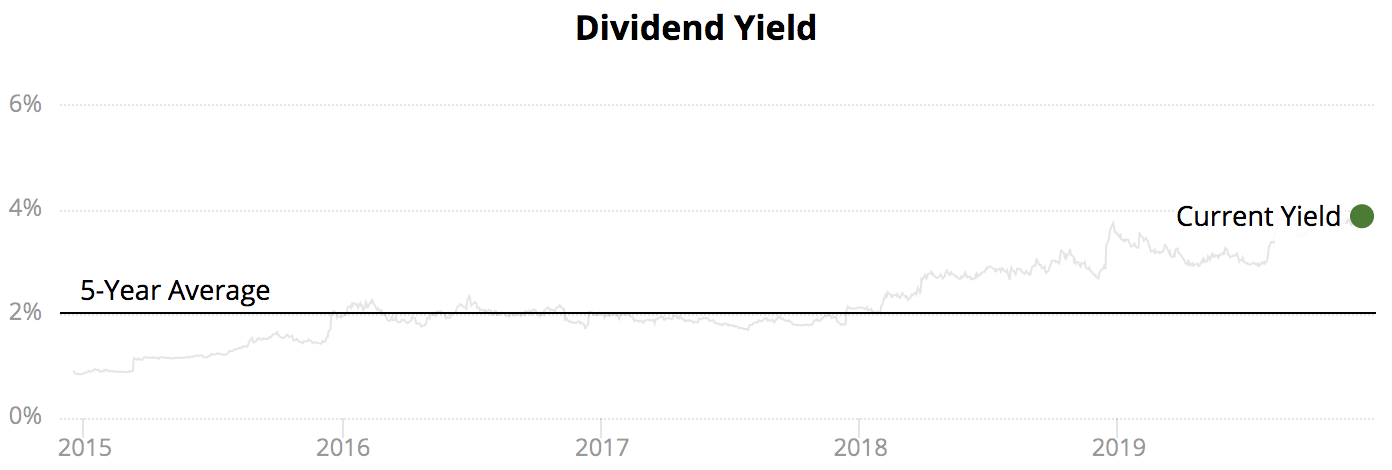

Franklin Resources (BEN) has raised its dividend every year since 1981 and offers a 4% dividend yield, an all-time high for the stock. While the asset manager's payout continues to look safe, Franklin faces several headwinds that could weigh on its future performance and pace of dividend growth.

Source: Simply Safe Dividends

Actively managed funds have been under pressure for most of the past decade. Lackluster performance and relatively high fees have persuaded many investors to move their money into cheaper index funds that simply track a benchmark rather than try to outperform it.

In fact, for the first time ever, in August 2019 passive U.S. equity assets passed active U.S. equity assets, according to Morningstar. Unfortunately, Franklin finds itself on the wrong side of this trend.

The investment manager offers actively managed funds across fixed income (40% of assets under management, or AUM), equity (39%), and multi-asset / balanced strategies (20%). Franklin also provides cash management services (1%).

ETFs account for less than 1% of the firm's AUM, and alternative assets represent only about 6%. In other words, Franklin depends heavily on the types of traditional active funds that are under the most performance and fee pressure.

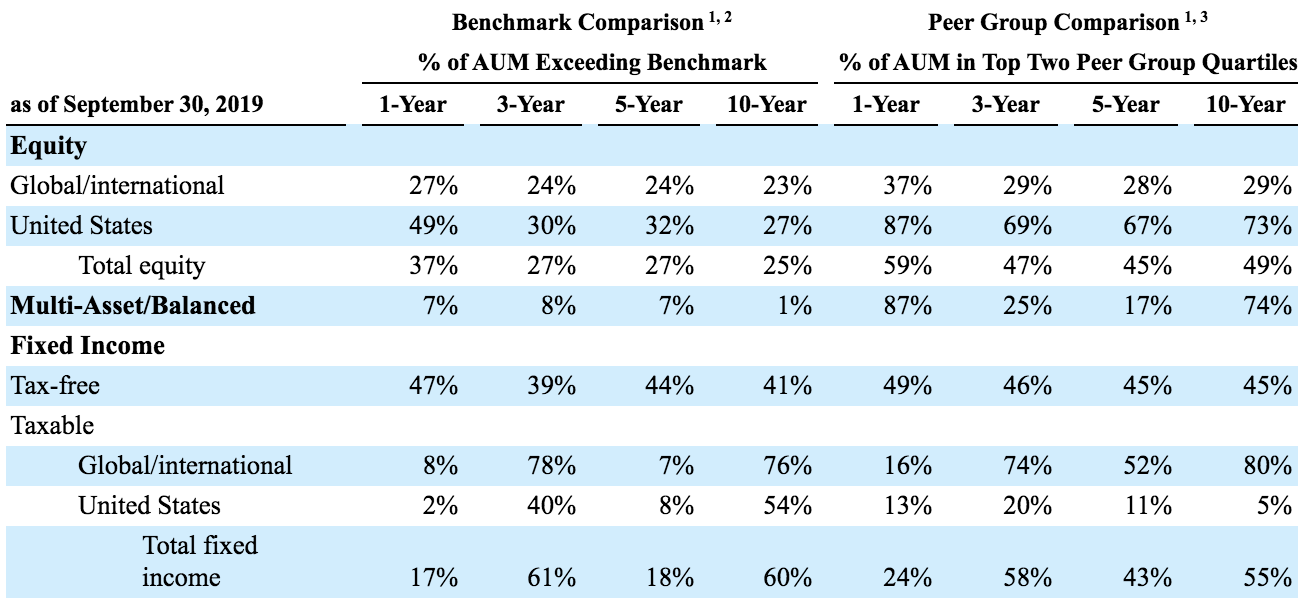

That's not necessarily a problem if Franklin's funds were holding their own. However, as you can see below, only 25% of the assets invested in Franklin's equity strategies have outperformed their benchmarks over the past decade.

These important products represent about 40% of firm-wide assets and generate higher management fees compared to Franklin's fixed income products. The company's global/international equity funds (23% of AUM) earn the highest fees but have consistently turned in some of the weakest relative performance.

Source: Franklin 10-K

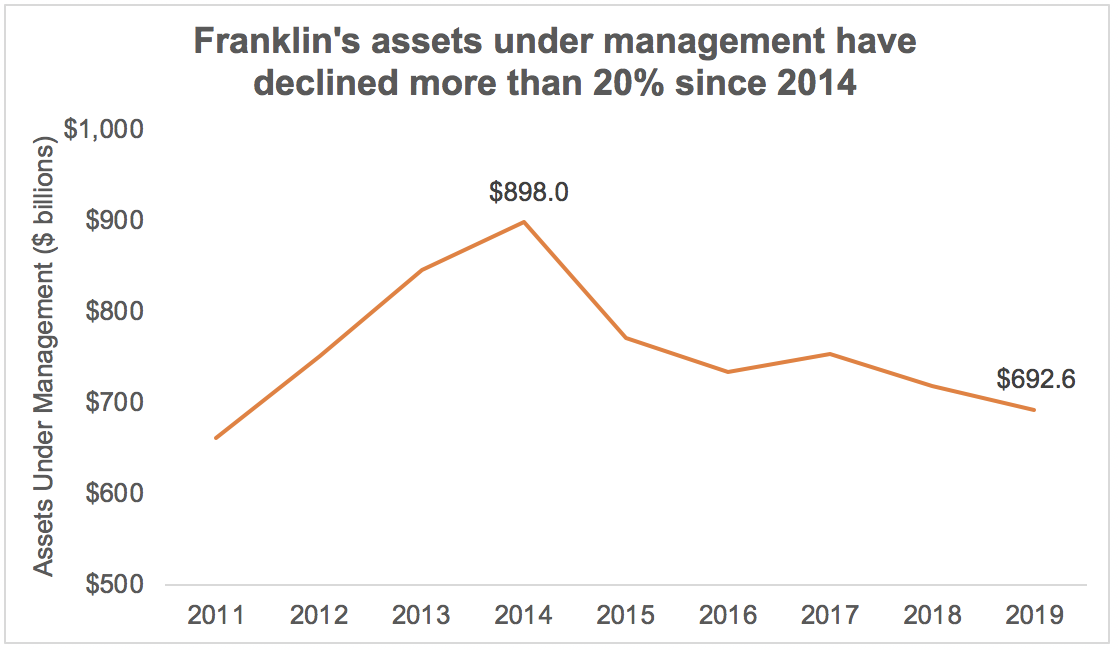

Investors have responded by pulling their money from many of Franklin's funds. The company's AUM has fallen from a peak of $898 billion in 2014 to under $700 million today, representing a 23% slump.

When you consider that global markets have appreciated significantly during this period and Franklin has made several acquisitions, helping offset some of the net outflows, the firm's performance is even more disappointing.

Source: Franklin, Simply Safe Dividends

Adding insult to injury, Franklin's effective investment management fee has also declined from 62.7 basis points in 2014 to 56.4 basis points in 2019, a 10% drop. In its annual 10-K filing, Franklin blames the decline in the industry's management fees on increased investor demand for lower-fee passive funds.

Investment management fees, which generate the bulk of Franklin's revenues, are determined based on a percentage of AUM each month. As a result of the decline in Franklin's AUM (especially in its higher-fee international equities business), plus the general downward pressure on fees industrywide, the firm's annual revenue has fallen more than 30% since 2014.

Source: Simply Safe Dividends

Franklin's operating income declined about 50% during this period, sliding from $3.2 billion in 2014 to approximately $1.6 billion in fiscal 2019. The company's earnings per share haven't fallen as much thanks to aggressive buybacks reducing Franklin's shares outstanding by roughly 20% during this period, but there's no mistaking the downward trend in profitability.

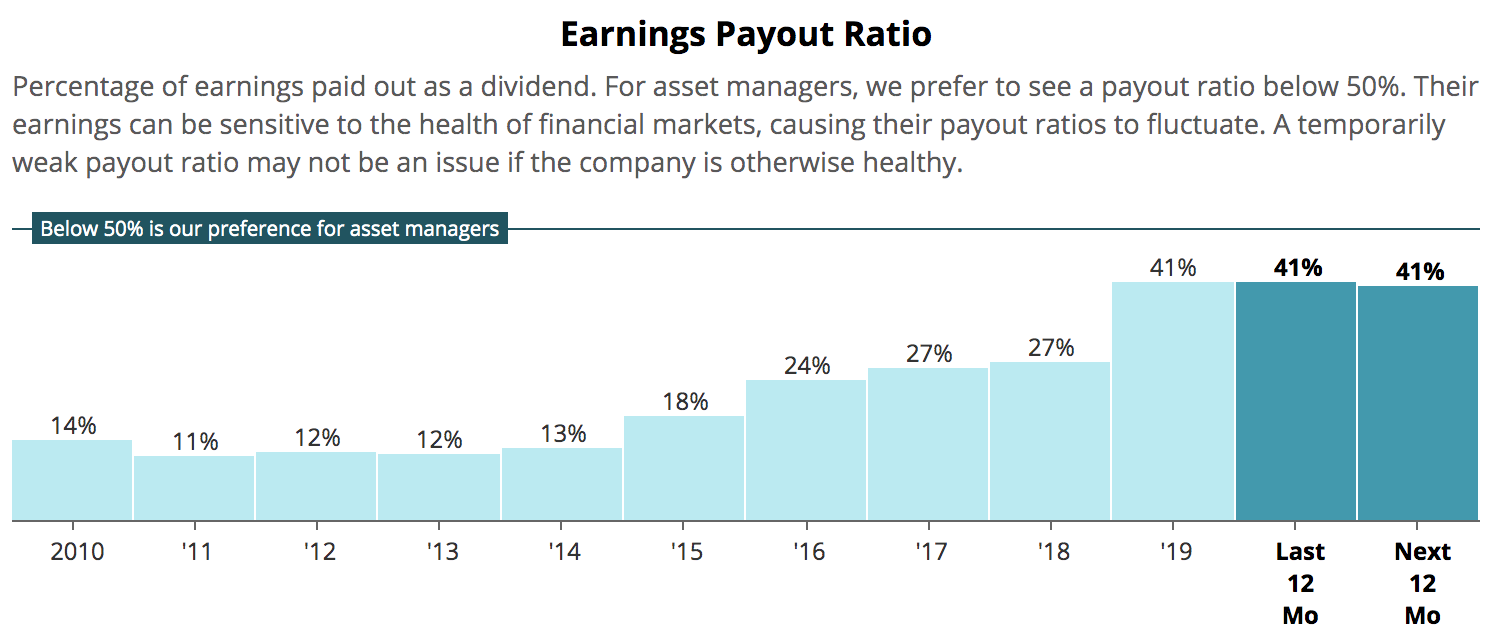

Despite these challenges, Franklin's dividend appears likely to remain safe for the foreseeable future. The dividend consumes about $500 million annually, representing a payout ratio near 40%.

While that's about twice as high as Franklin's historical norm, it still represents a reasonable level that provides some cushion in the event that global financial markets fall and hurt the firm's short-term earnings.

Source: Simply Safe Dividends

As importantly, Franklin maintains an excellent balance sheet with $5.8 billion in cash and about $2 billion in liquid investments compared to just $700 million in debt. Standard & Poor's awards the firm an A+ credit rating, although it has a negative outlook in light of potential further net outflows and fee pressure.

The dividend carries extra importance to Franklin, too. Founder Rupert Johnson Sr.'s family members own about 40% of the firm's shares and three of 10 board seats. They undoubtedly enjoy receiving their dividends and would like Franklin to maintain its status as a dividend aristocrat.

Three Johnson family members collectively hold the important titles of CEO, Vice Chairman, President, and Chairman of the Board of Directors. Given their influence on the company, it would likely take severe financial distress for management to consider reducing the dividend.

With that said, weak performance and fading interest in an asset class are powerful headwinds that could intensify in future years. The big question is whether or not Franklin can improve its relative investment performance to reverse investor redemptions, especially across its international equity products.

Besides several contrarian bets that haven't played out, management places some of the underperformance blame on the market's multiyear rotation into growth stocks since some of Franklin's strategies are focused on deep value.

Regardless, it's very difficult to forecast if or when more of Franklin's strategies will turn performance around. What's more clear is that the longer performance headwinds persist, the more likely it is that Franklin will lose its reputation with investors for delivering solid long-term results.

Franklin's impressive distribution capabilities for its funds and its diversification by geography and product seem likely to help keep the pace of AUM erosion manageable for now, but the clock is ticking.

Franklin is responding to these challenges by getting its funds on new distribution platforms and diversifying further into growth areas such as ETFs and alternative products, though these businesses combine for less than 10% of the firm's AUM today.

Management has also expressed increased willingness to use Franklin's conservative balance sheet to pursue larger (but not "mega") acquisitions, which would potentially help fill product gaps, bring scale to the firm's smaller products, and increase its distribution capabilities.

Franklin emphasized that any deal would need to allow the firm to continue operating with low leverage and strong financial flexibility, but it's clear that pressure is building for the company to take more significant action to stop its bleeding.

It's hard to have much confidence in the family-led executive team, which has been slow in responding to the industry's shifts. If Franklin's investment performance remains weak or the firm makes a regrettable large acquisition, the stock seems likely to turn into an even greater value trap.

Until results improve, income investors should expect relatively slow dividend growth. In fact, after raising its dividend by 13% in 2018, Franklin announced this week a 4% dividend increase.

Overall, we prefer to invest in businesses that have similarly strong financial health but clearer paths to profitable long-term growth. Franklin's uninspiring investment performance keeps many of its funds in the crosshairs of index funds, which could lead to additional investor redemptions and lower cash flow going forward.

Combined with slowing dividend growth, a management team with questionable skill, and the potential for a cyclical downturn in financial markets that could exacerbate net outflow challenges, long-term income investors may want to consider alternative ideas.