Oxy's Safe Dividend Safety Score Remains Fragile Due to Debt, Oil Risks

Shares of Occidental Petroleum (OXY) are down more than 30% since early April 2019 when Oxy emerged as the high bidder for Anadarko. As a result, Oxy's dividend yield topped 7% last month, reaching an all-time high.

Source: Simply Safe Dividends

Although Oxy's dividend continues to look sustainable based on the price of oil today, investors clearly remain concerned about the company's risk profile following its purchase of Anadarako, which closed on August 8.

For more background on this major acquisition, please review the in-depth note we published in April 2019 reviewing the deal's strategic merit and dividend implications for Oxy. Here was my conclusion:

"An acquisition of this size increases both executional and financial risks. Oxy's debt load will balloon to riskier levels, making the company more dependent on a favorable oil price environment as it looks to divest assets and improve its free cash flow generation to rapidly reduce leverage.

Due to the firm's higher expected leverage, Oxy's Dividend Safety Score could be downgraded if the company does not quickly improve its balance sheet and cash flow generation as management expects. While Oxy's payout should remain on stable ground if everything goes as planned, another untimely crash in the price of oil could create uncertainty."

Those statements remain true today. Oxy's risk profile will remain elevated the next several years until it can make significant progress deleveraging, divest non-core assets at reasonable valuations, and deliver on its synergy targets after integrating Anadarko.

The success of each of these priorities depends on a favorable oil price. If the price of oil falls and remains below $45 per barrel (currently $59) during the next few years, then Oxy's cash flow and credit metrics would remain pressured, and its Dividend Safety Score could be downgraded to a potentially unsafe level.

If the price of oil remains at or above its current level, then Oxy should have the breathing room it needs to improve its balance sheet and the coverage of its dividend. Management remains strongly committed to the payout as well.

While Oxy's dividend risk profile hasn't changed materially since our note was published in April, several other factors have weighed on the company, resulting in Oxy's high dividend yield.

First, shareholders have lost some trust in management. At the time of our April note, Oxy planned on financing the transaction with a combination of 50% stock and 50% cash. However, this level of equity issuance would have triggered a shareholder vote to approve the Anadarko acquisition.

With several major shareholders such as T. Rowe Price expressing concern about the deal, in early May the firm revised its buyout offer to be 78% cash and 22% stock. While this move increased the amount of leverage Oxy used to acquire Anadarko, the bigger issue was the message it sent to shareholders.

The New York Stock Exchange (NYSE) requires shareholder approval prior to issuing common stock if the common stock will equal or exceed 20% of a firm's shares outstanding.

By reducing the amount of common stock issued to fund the deal, Oxy remained under this threshold and thus avoided a shareholder vote on the transaction. For a deal this significant (effectively a merger of equals), shutting out shareholders represents a major corporate governance concern.

Activist investor Carl Icahn, who owns more than 30 million Oxy shares (about 5% of the company, or $1.5 billion), has ripped the deal, stating Oxy paid "way too much to complete a transformational transaction without a stockholder vote."

He believes Oxy's management may have pursued Anadarko at any cost to ensure they would stay in power. Loading up the balance sheet with debt is a good way to ward off potential acquirers of Oxy, whose performance struggles and weak stock price might otherwise attract a buyer.

Icahn is hoping to remove and replace several of Oxy's board members. Further frustrating shareholders, management financed part of the deal by issuing $10 billion in preferred stock paying an 8% annual dividend to Warren Buffett's Berkshire Hathaway.

If the 8% dividend wasn't generous enough, the preferred stock also came with warrants giving Buffett the option to buy up to 80 million Oxy shares at a price of $62.50 per share.

With the yield on Oxy's newly issued debt sitting around 3%, issuing costly preferred stock looks like a questionable move. Oxy might have pursued this path to help protect its credit rating since preferred stock is usually not fully counted as debt when calculating leverage ratios.

Source: Oxy Investor Presentation

Besides taking on higher effective leverage, ignoring the voice of major shareholders, and tapping suboptimal financing to get the deal to the finish line, Oxy's stock performance has also been hurt by the weakening energy environment.

The price of West Texas Intermediate (WTI) oil fell from $66.30 per barrel in late April 2019 (when Oxy placed the highest bid to acquire Anadarko) to $54.85 last week, nearly a 20% slump.

Even after the pop in global oil prices yesterday following an attack on Saudi Arabia's oil infrastructure, which sidelined around 5% of the world's total supply, prices sit near $59 per barrel, or 11% below their level when the Anadarko deal was announced.

While $59 per barrel oil remains well above management's projected 2020 breakeven price in the "low $40" range, investors are losing faith in shale oil companies. (Anadarko has a strong presence in some of the country's most prolific shale regions, and the Permian basin accounts for about 40% of the combined company's energy production.)

In August 2019, the Institute for Energy Economics and Financial Analysis (IEEFA) published a study of 29 fracking-focused oil and gas companies following their second quarter results, stating that U.S. shale should be viewed as a "speculative enterprise with a weak outlook and an unproven business model."

OilPrice.com summarized the report's findings, which showed the industry continues struggling to generate positive free cash flow:

"By and large it was another period of disappointment for a sector that has underwhelmed for years...Fracking, horizontal drilling and mountains of cash from Wall Street have succeeded in producing wave after wave of oil and gas, continuously pushing output to record highs. But the profits have never really materialized. In fact, rapid production growth crashed prices for both oil and gas, undercutting the industry’s ability to make any money."

Fracking companies continue bleeding cash (Anadarko recorded negative free cash flow of $526 million in the second quarter), and investors are losing faith that these businesses will ever be able to turn a profit.

Given this backdrop, Oxy's pricey deal to double down on the Permian basin has investors feeling skeptical about management's ability to deliver on their promised synergies. There's a lot of fear in the stock price, and some of it is understandable.

As expected, Oxy was also hit with credit rating downgrades once the deal became official. On August 8, Standard & Poor's downgraded Oxy's credit rating from A to BBB. Moody's issued a similar downgrade, writing:

"OXY's acquisition of Anadarko is a significantly leveraging transaction, adding over $40 billion of debt to OXY's capital structure at its outset. While the acquisition will strengthen and diversify OXY's upstream and midstream asset base, adding further scale to its already large position in the Permian Basin, the significant increase in debt leaves the company with less flexibility to confront commodity price volatility.

Moreover, OXY could be challenged to deliver the full complement of asset sales, capital and operating cost synergies and execution on the acquired assets to fund the debt reduction required to improve its materially weakened credit metrics." – Andrew Brooks, Moody's Vice President

Sometimes companies with high debt loads choose to reduce their dividends to accelerate deleveraging, even if their payouts are covered by cash flow. Kraft Heinz (KHC) is one recent example.

This seems unlikely in the case of Oxy, unless the oil price environment weakens significantly. The company's common stock dividend is one of the few remaining pieces of credibility Oxy has with its shareholders, and management appears very committed to maintaining it.

For example, Oxy has not historically hedged its production often, but the company began a new hedging program for 2020 to strengthen its cash flow in a low oil price environment.

On its second quarter earnings call, management said these hedges "provide additional assurance that our dividend is safe while we are deleveraging."

Management also vowed to "protect our dividend in the event of any potential commodity price pressures, including during the transition phase of our integration."

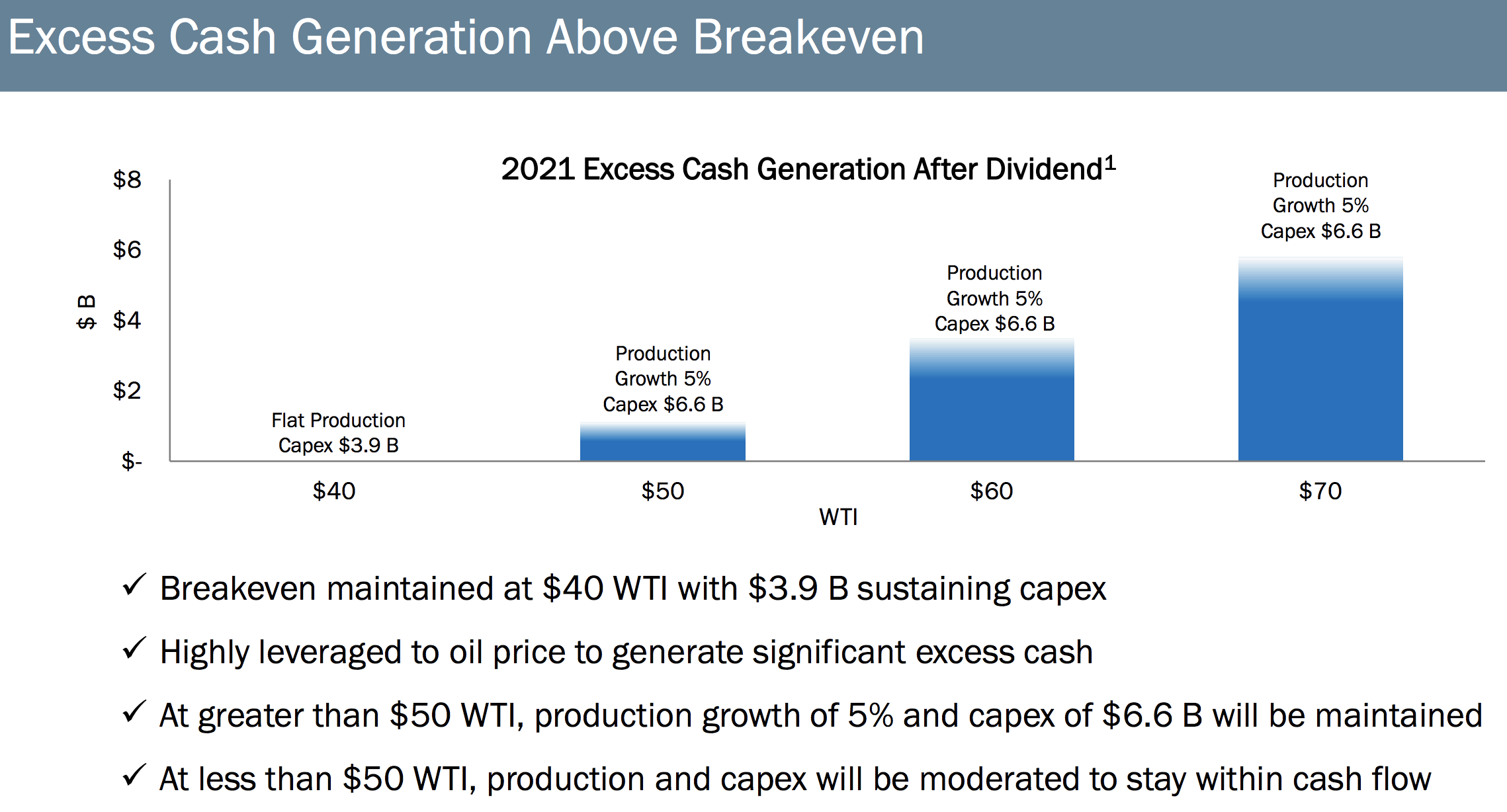

Next year Oxy believes it can keep production flat, cover its dividend, and remain cash flow neutral "in a low $40 dollar WTI price environment." As you can see below, Oxy expects its breakeven position to get back down to $40 per barrel oil with an unhedged position in 2021.

Source: Oxy Investor Presentation

Oxy emphasized that its two highest priorities are to maintain its low-cost production base and to sustainably grow its dividend per share, which it has done since 1991 (including a 1.3% increase in July).

Deleveraging is the next priority, with management targeting at least $10 billion to $15 billion of asset sales over the next two years for debt reduction.

It's hard to imagine Oxy receiving favorable terms on the assets it divests given the firm's desperation to deleverage, but there aren't great alternatives if the dividend is to be preserved.

Oxy already struck a deal to divest Anadarko's Africa assets for $8.8 billion, giving the firm a good start on its objective. However, management assured investors it would shift cash from its capital program to debt reduction if the firm was unable to meet its internal divestiture targets.

As we discussed in April, Oxy is somewhat unique in that the vast majority of its targeted growth projects are short-cycle investments with payback periods of less than three years at $50 per barrel oil. Management has also claimed Oxy can reduce capital from its growth plan to sustaining capital levels within six months.

Combined with Oxy's substantial asset base, which provides ongoing opportunities for the firm to improve its balance sheet through asset sales, this flexibility gives management another lever to pull to protect its dividend.

Overall, Oxy's weak performance since April appears to have been driven by shareholders' disappointment in management's actions (skirting a shareholder vote to approve the acquisition; issuing costly preferreds) and the continued volatility in the energy sector as a whole.

However, Oxy's dividend appears to remain supported by both the current oil price environment and management's strong desire to maintain the payout, which represents one of the firm's last remaining pieces of credibility with investors.

The next year is a critical one for Oxy. We will learn how quickly the company can deleverage via asset sales, whether or not the integration of Anadarko goes smoothly, and if the Permian basin can continue its impressive growth.

Oxy could be a great investment if the price of oil remains stable or increases, but it could also turn into a value trap due to its balance sheet if energy markets experience a significant and sustained decline in the next year or two.

Conservative investors may want to remain on the sidelines until Oxy has made more progress deleveraging and demonstrated that it can achieve its expected synergies from Anadarko. Until then, the stock faces a somewhat wide range of potential outcomes based largely on the price of oil.