Reviewing Oxy's Dividend Safety After $38 Billion Bid for Anadarko

Shortly after Anadarko (APC) agreed to be acquired by Chevron (CVX), Occidental Petroleum (OXY) offered $38 billion to buy Anadarko in a deal valued 20% higher than Chevron's agreement.

Oxy has now made a total of three acquisition proposals to Anadarko since late March, and each was higher than the deal announced with Chevron on April 12, according to a letter written by the company to Anadarko.

For whatever reason, Anadarko appears to prefer teaming up with Chevron and even agreed to pay the company a break up fee of $1 billion (about $2 per share) if their deal were to fall through. However, Oxy's significantly higher offer could finally be enough to sway Anadarko's board.

While Chevron could step back in with a higher bid, let's review Oxy's potential transaction with Anadarko to evaluate how it could affect the firm's dividend safety profile and long-term outlook.

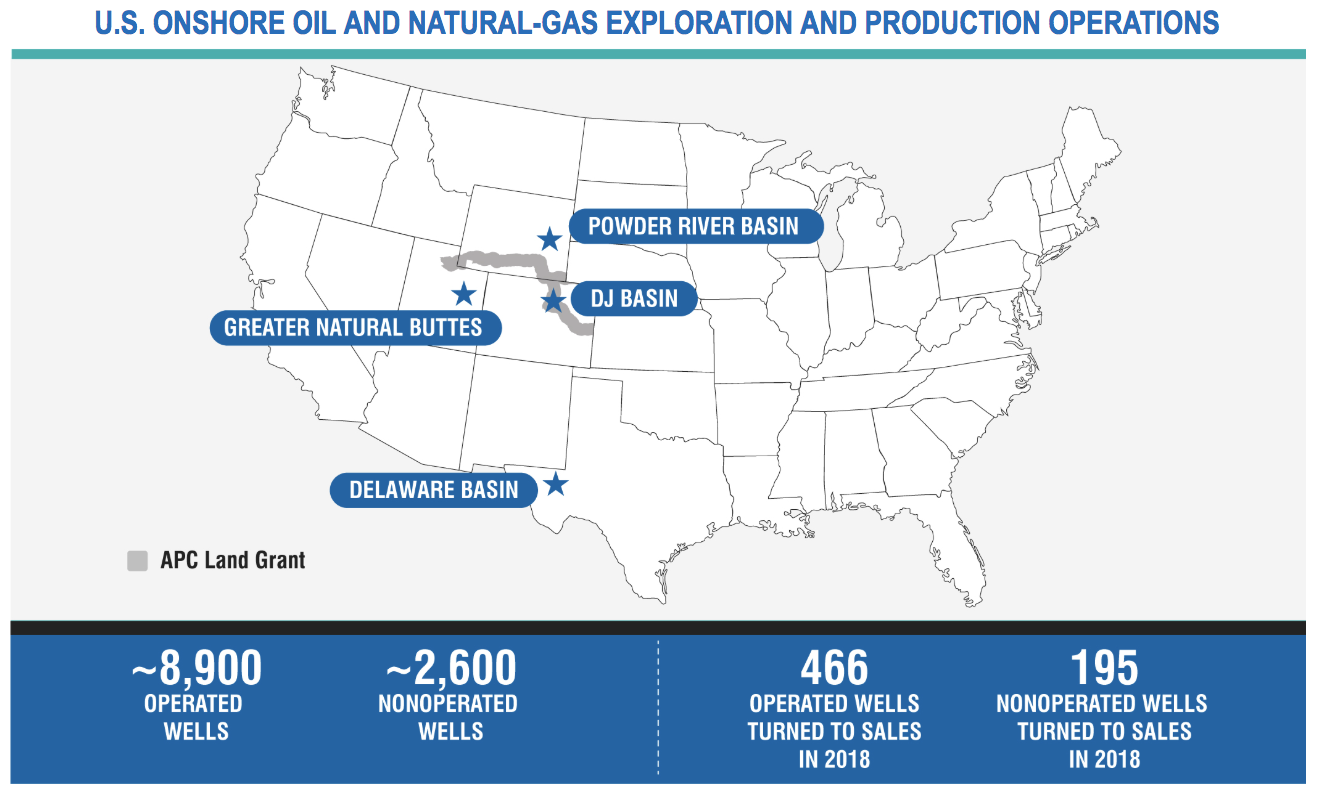

Why Oxy Wants to Buy Anadarko Anadarko is one of the biggest independent oil and gas production companies in America. The firm's U.S. operations account for 86% of its sales volume and 90% of its proved reserves. Importantly, Anadarko has a strong presence in some of the country's most prolific shale regions.

Source: Anadarko Annual Report

Thanks to advances in fracking technology, extracting oil and natural gas from large shale deposits has become increasingly economical over the past two decades, unlocking exponential production growth in America.

For example, in 2000 shale gas accounted for just 2% of U.S. natural gas production but makes up over 40% of production today, according to the Global Energy Institute. And in oil, the U.S. is now the world's top producer.

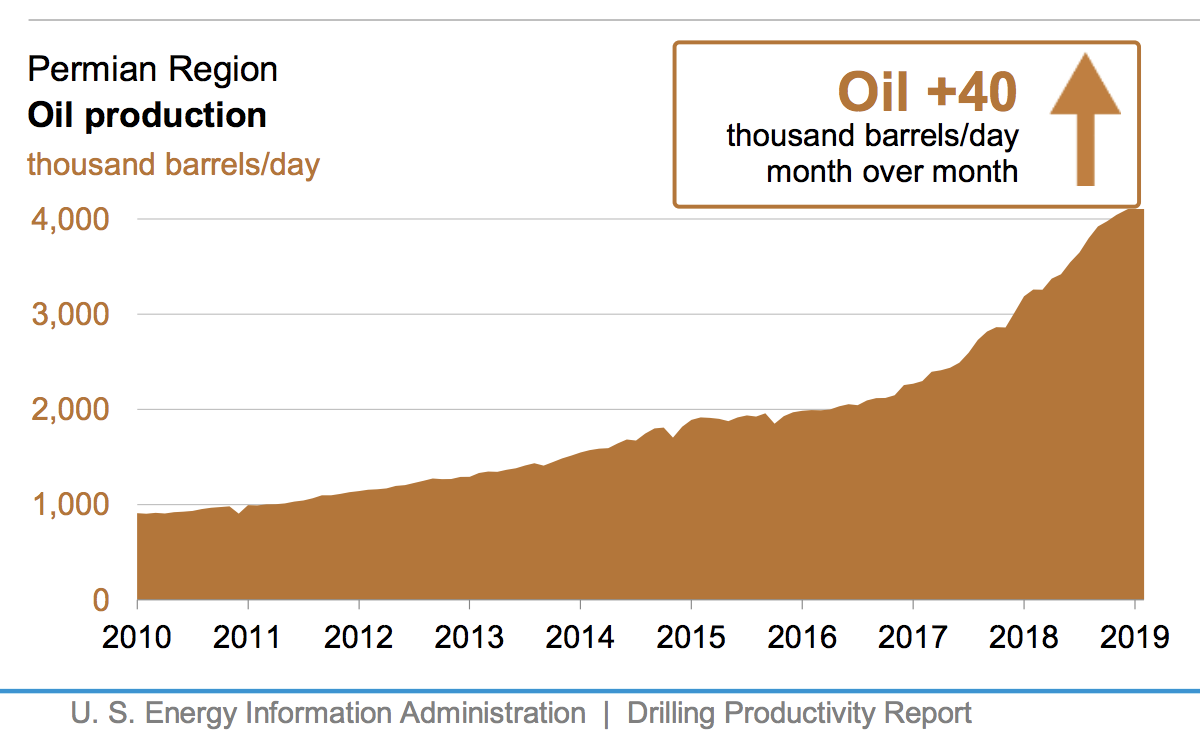

Anadarko is one of the largest shale drillers in the Permian basin in Texas, which is the second-most-productive oil field in the world. As you can see, oil production in this region has increased from less than 1 million barrels per day in 2010 to more than 4 million today.

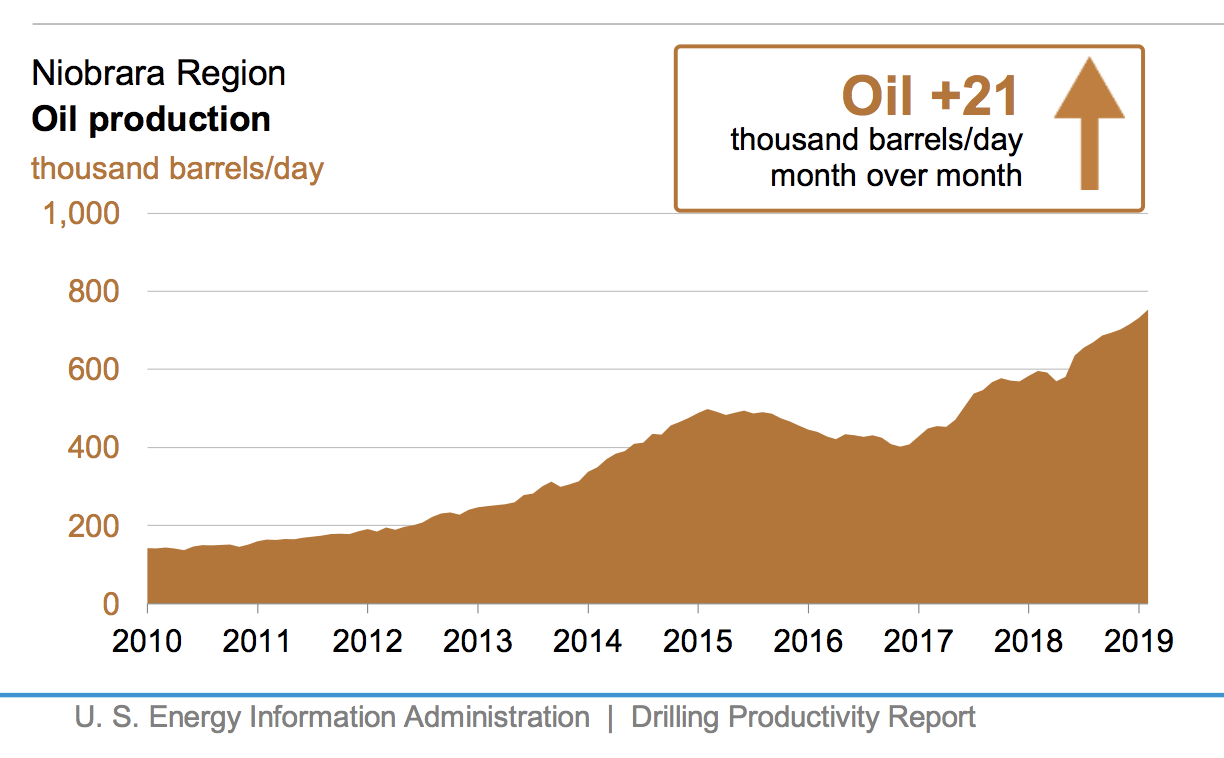

In the Niobrara-DJ region, which runs through Colorado and parts of Wyoming and is another critical region for Anadarko, oil production has increased from less than 200,000 barrels per day to nearly 800,000 today.

But despite this boom in output and the bounce in the price of oil, independent energy producers were struggling. Prior to agreeing to Chevron's offer earlier this month, Anadarko's stock was down nearly 60% since August 2014 and off over 35% since early July 2018.

Smaller producers were under pressure from rising drilling costs and volatile energy prices. Travis Stice, CEO of Diamondback Energy, remarked, "Realized pricing in the Permian Basin is near levels not seen since the end of 2016 while service costs have increased by about 35 percent during the same time period."

Investors punished most of these companies and wanted to see them cut costs, reduce their spending, and improve their cash flow. Like Chevron, Oxy presumably viewed Anadarko as an opportunistic purchase it could make to further expand its asset base in some of America's most important energy production regions.

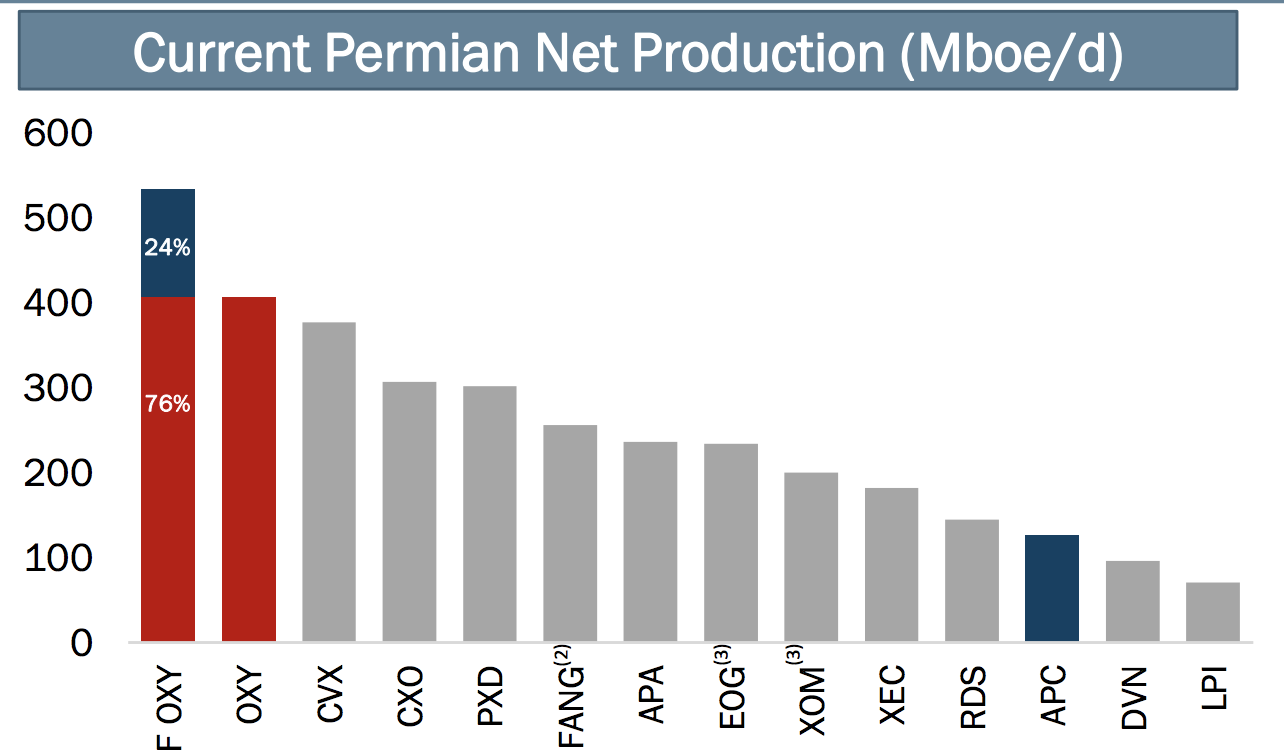

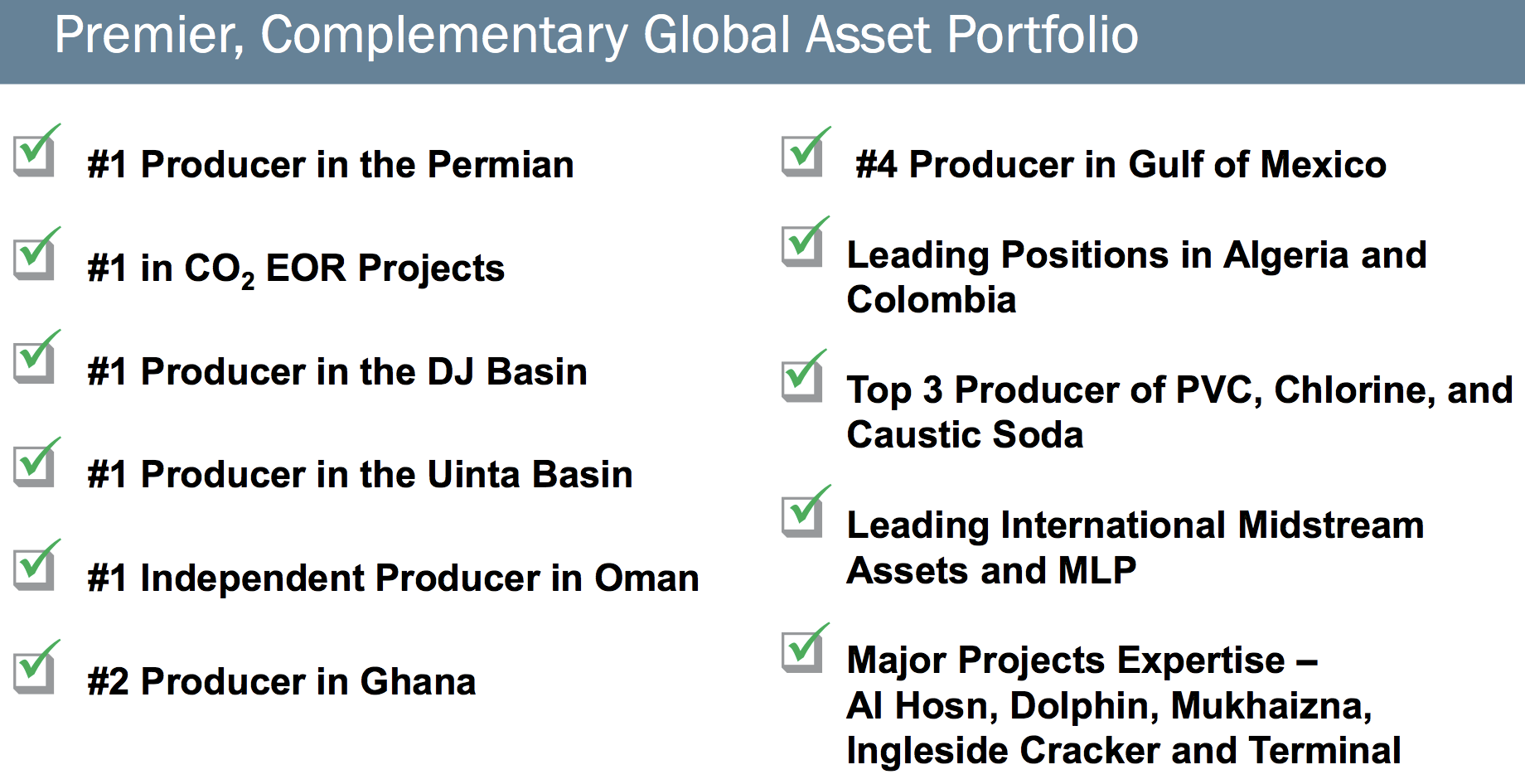

As you can see below, Oxy already enjoys very strong positions in shale oil producing formations. In fact, Oxy's current Permian net production is the largest in the industry and accounts for about a third of the company's total oil & gas production.

In recent years Oxy has divested higher production cost assets located in areas such as North Dakota and Iraq to focus more of its resources on the Permian. The company has one of the best logistics systems set up in the basin, and combining forces with Anadarko would further bolster its status as the largest producer in this important region.

Soure: Oxy Investor Presentation

Oxy expects to be the largest producer in the DJ basin as well, another important region for Anadarko, while also continuing to boast impressive scale in various other production fields and its chemical and midstream businesses.

Source: Oxy Investor Presentation

Thanks to its superior size and integrated operations, an Oxy-Anadarko company appears to be better positioned to handle the challenges that have weighed on independent oil and gas producers. The firm could put more pressure on contractors to achieve cheaper drilling rates and also afford to use the best technologies to improve well operating performance, for example.

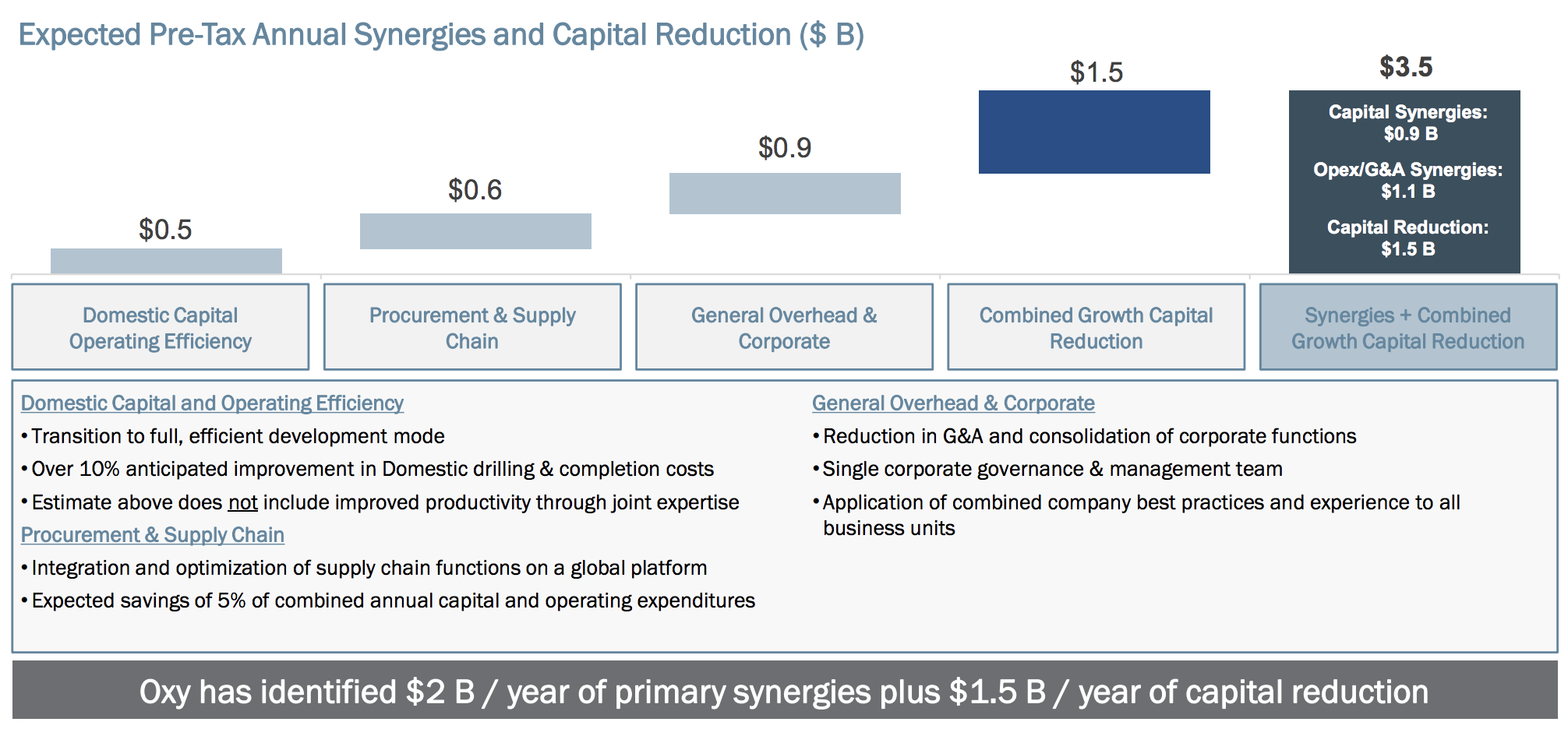

While Chevron identified $2 billion in annual synergies, balanced between reduced capital expenditures and cost savings, Occidental's management team sees potential to realize $3.5 billion in annual free cash flow improvements by 2021.

For perspective, in 2018 Anadarko and Oxy collectively generated $13.6 billion in cash flow from operations and invested $11.2 billion in capital expenditures, resulting in about $2.4 billion in free cash flow. While cash flow can be volatile any given year in the energy sector, a $3.5 billion synergy target is a really big number for these companies, representing over 20% of their combined forward EBITDA.

Approximately $2 billion of management's identified synergies is expected to come from cost savings, with another $1.5 billion of capital reduction. The cost synergies are expected to be realized from greater capital and operating efficiency, procurement and supply chain savings, and consolidating overlapping corporate functions.

The reduction in capital expenditures is expected to be delivered in the first year, causing Oxy's short-term production growth to moderate from 10% to 5% on a combined basis. Management also reduced the combined company's long-term production growth guidance from 5-8% to 5%, reflecting a more moderate level of spending focused on higher-margin opportunities.

Source: Oxy Investor Presentation

If Anadarko and Oxy tie the knot, based on 2018 results Anadarko would account for around 45% of the combined company's cash flow from operations. The overall business would have even greater exposure to the Permian and DJ shale basins, though this higher long-term production growth potential would come at the expense of a business (and stock price) that's even more sensitive to the price of oil.

Let's take a look at the financial implications of this deal.

How Buying Anadarko Could Affect Oxy's Dividend Safety While Chevron's transaction would be funded with 75% stock and 25% cash, Oxy's stock-and-cash offer calls for a 50-50 split. The company would issue 309 million shares, representing about a 40% increase in its shares outstanding, and pay $19 billion in cash for Anadarko.

Large acquisitions can imperil a company's dividend if they result in too much leverage, especially in a cyclical sector like energy. Impressively, Oxy has either maintained or grown its dividend each year since 1991, including throughout the 2014-16 oil crash when many other producers axed their payouts.

An excellent credit rating and conservative balance sheet are the ultimate dividend safety buffers in this volatile industry. When times get tough, causing payout ratios to temporarily exceed 100% or even turn negative if an oil producer operates at a loss, businesses committed to their payouts can safely borrow for a few lean years to maintain their dividends.

The company's disciplined capital allocation helped it navigate the sector's latest downturn. Management historically avoided debt-funded growth and focused instead on maintaining a pristine balance sheet. As a result, Oxy earns an A credit rating from Standard & Poor's, which is the third highest of any U.S. oil company (behind only Exxon Mobil and Chevron).

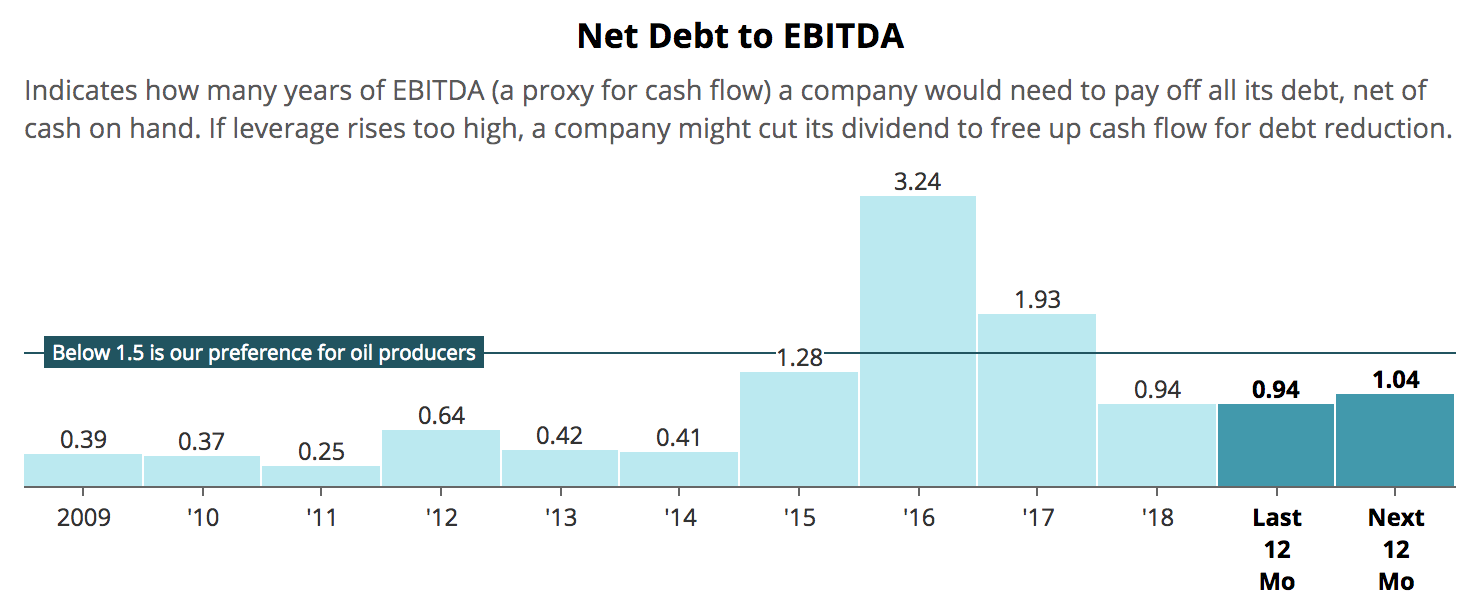

Oxy's net debt to EBITDA leverage ratio has remained very low for more than a decade, excluding the oil crash which temporarily suppressed the firm's profitability. However, taking on Anadarko's net debt, which exceeds $15 billion, and adding another $19 billion of net debt to fund the transaction will push the combined company's forward net debt to EBITDA ratio up to about 2.9, according to our analysis. That's nearly as high as Oxy's peak leverage during the oil crash.

Source: Simply Safe Dividends

Oxy says it is committed to maintaining an investment grade credit rating, with ambitions to return to its current credit rating or better, and targets less than 2.0 times leverage by 2021.

The firm plans to execute $10 billion to $15 billion of asset sales in the next 12 to 24 months to begin paying down debt. This alone would bring down the company's leverage ratio to about 2.0 using 2019 EBITDA estimates for the combined company, per our analysis.

If EBITDA grows 20% over the next two years thanks to synergies and production growth, Oxy's leverage ratio could fall closer to 1.5 with healthy asset sales.

However, the bottom line is that Oxy's balance sheet won't be as strong as it used to be for at least a couple of years. If this deal moves forward, Oxy is banking on energy markets remaining favorable enough for it to receive fair value for these assets to speed up deleveraging.

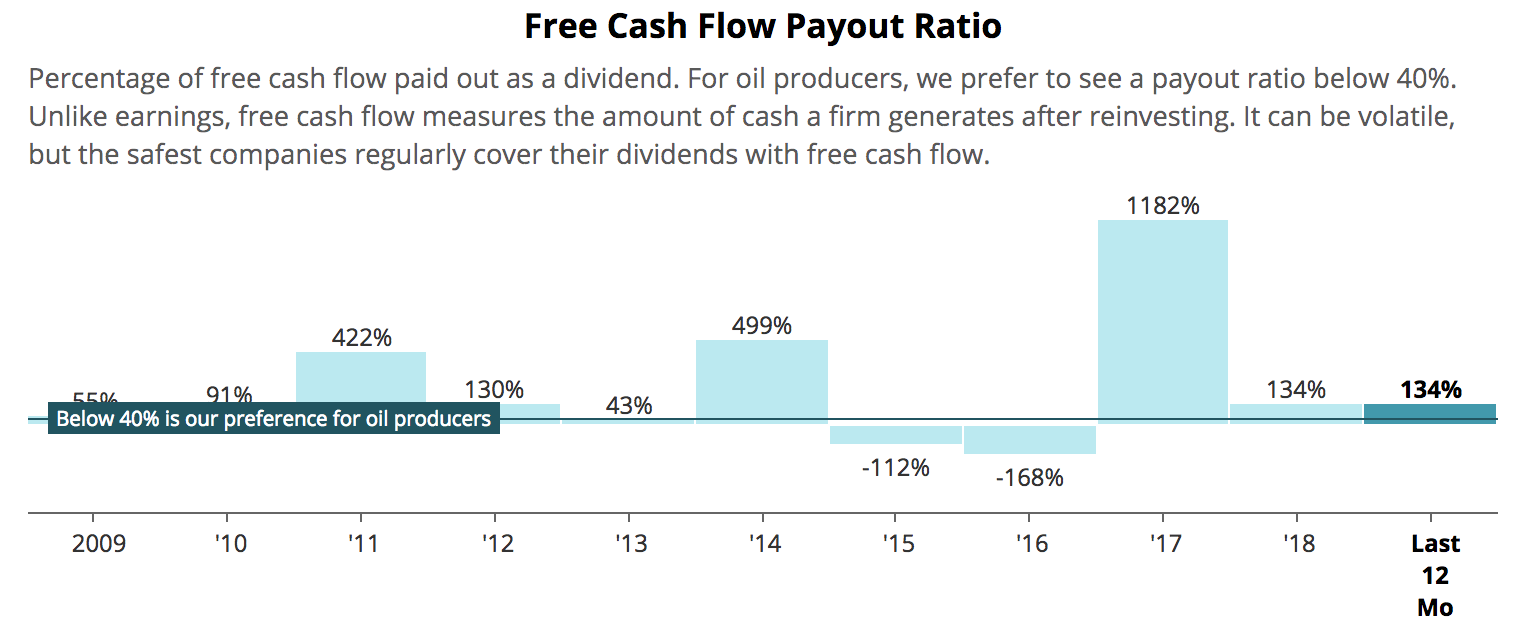

A high debt load is easier to manage if a company's payout ratio is low, providing a healthy amount of internally generated cash flow that can be used to reduce leverage.

Unfortunately, as previously discussed, Anadarko and Oxy generated $2.4 billion in combined free cash flow last year. After accounting for the 309 million shares Oxy expects to issue to fund the deal, the combined company's annual dividend obligation will total about $3.3 billion.

In other words, without accounting for any integration costs, synergies, higher interest expenses, or future asset divestitures, the combined company's 2018 free cash flow payout ratio would have remained well above 100%. With a weaker balance sheet, does this spell trouble for Oxy's dividend? Not necessarily.

Oxy Payout Ratio – Source: Simply Safe Dividends

Oxy is somewhat unique in that the vast majority of its targeted growth projects are short-cycle investments. In fact, approximately 80% of the $4.5 billion of projects management previously targeted for 2019 were expected to have payback periods of less than three years at $50 per barrel oil.

Management also claimed Oxy can reduce capital from its growth plan to sustaining capital levels (about $2.5 billion, or just over half of its targeted spending this year) within six months.

Thanks to this greater flexibility, the company expects its planned $1.5 billion reduction in capital spending will be delivered in the first year of the deal closing. All else equal, that move alone would boost the combined company's free cash flow enough to cover the dividend, even after higher interest expenses.

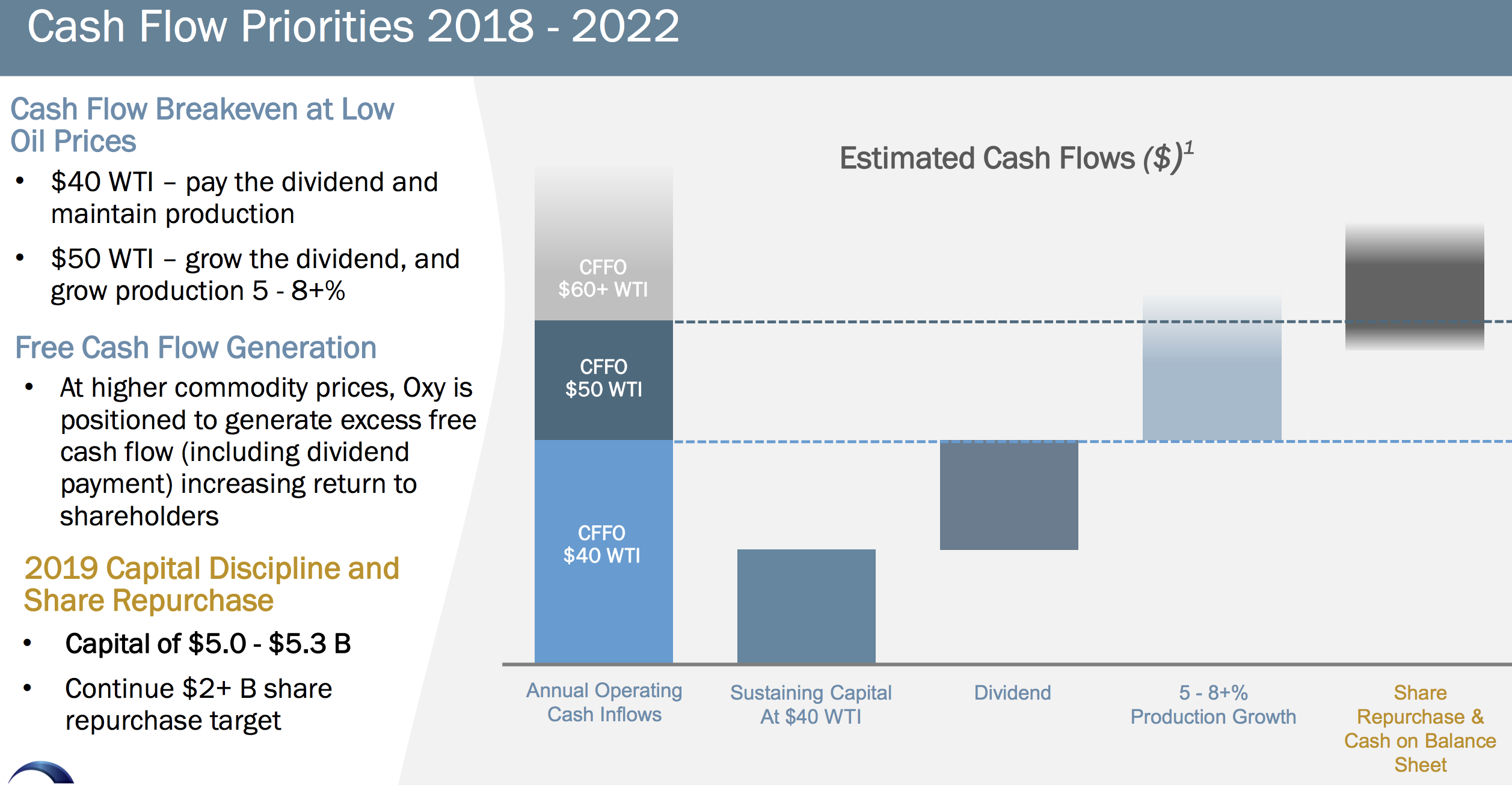

Oxy also previously stated that even if oil averages just $40 per barrel, the company's cash flow from operations would cover the costs required to maintain the firm's operations while also keeping the current dividend sustainable. For context, in January 2016 oil bottomed at $26 per barrel.

Source: Oxy Investor Presentation

In its presentation overviewing its offer for Anadarko, Oxy essentially reaffirmed this analysis, stating that its dividend is expected to remain sustainable at an oil price of $40 per barrel (current price is $65 per barrel). The company voiced further support for its dividend in the presentation, noting it "is firmly committed to maintaining its current dividend growth strategy."

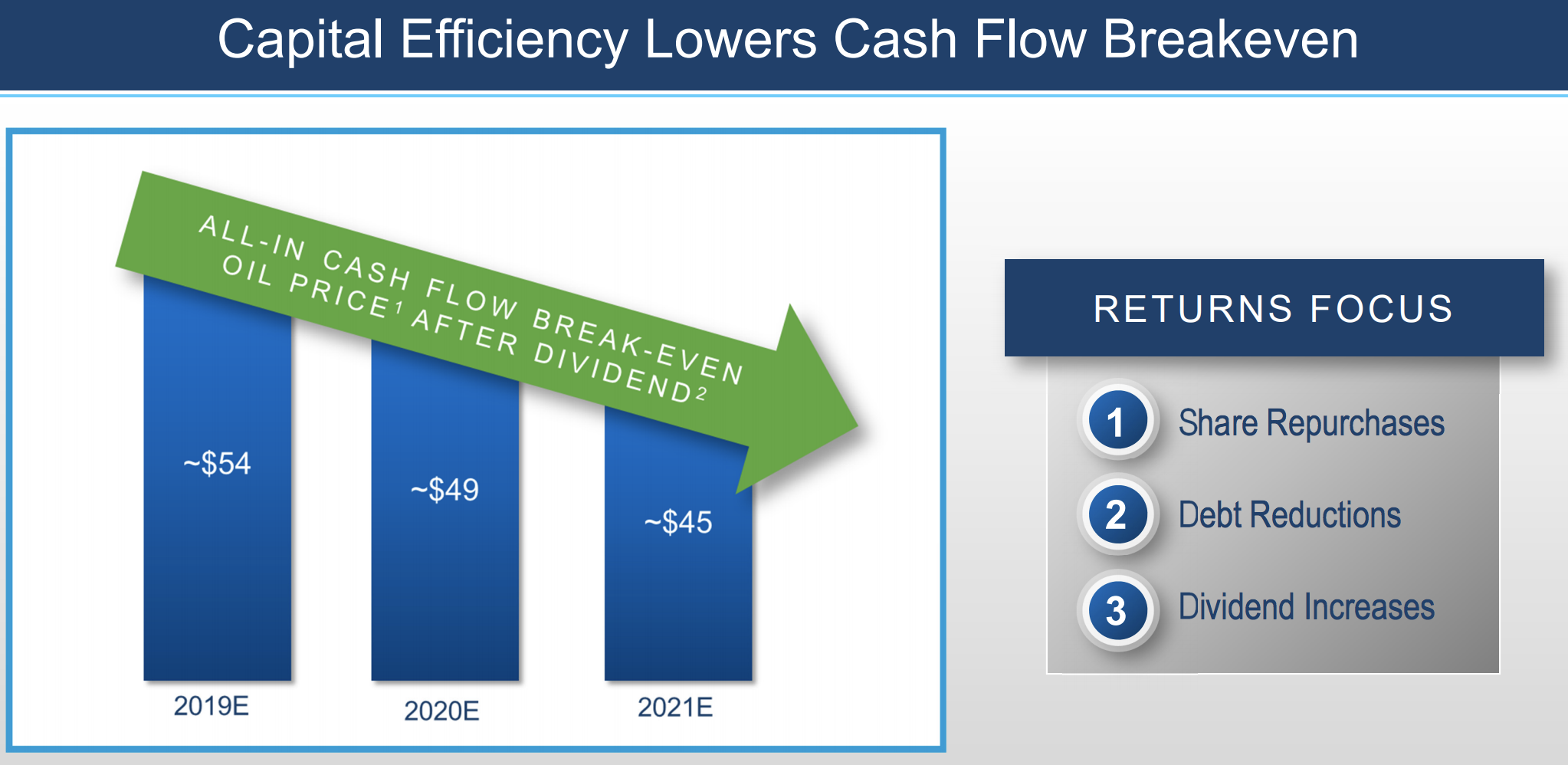

Anadarko has also put more emphasis on its all-in cash flow breakeven level, bringing it down to $54 per barrel this year with ambitions of hitting $45 per barrel by the end of 2021.

Source: Anadarko Investor Presentation

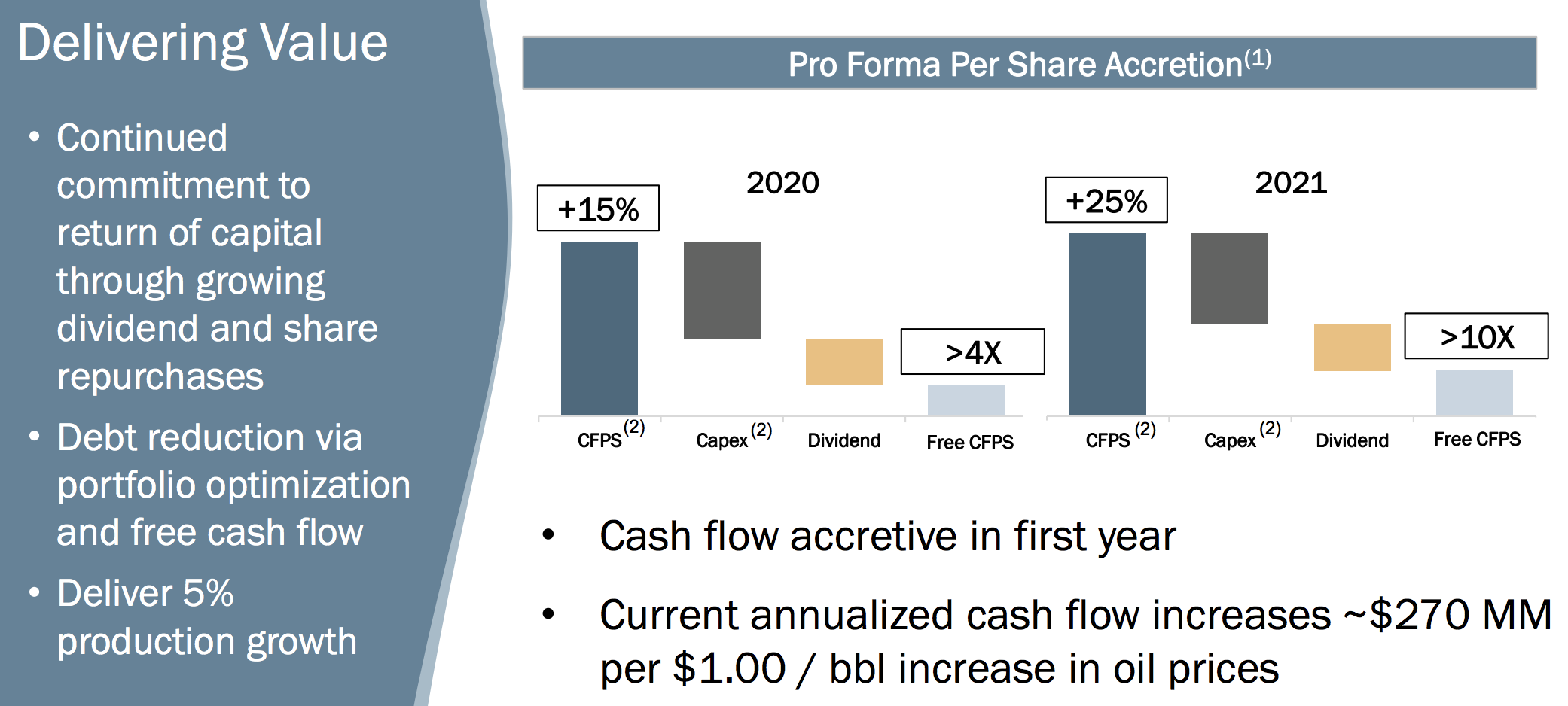

If management delivers on its target of $3.5 billion in annual free cash flow improvements by 2021, Oxy's free cash flow payout ratio would fall to around 60%. Incremental production growth (management now targets 5% annually) would further put Oxy's payout ratio on sustainable ground.

Higher oil prices would provide further upside, but even in today's environment management expects the deal to be significantly accretive to cash flow (CFPS) and free cash flow (Free CFPS), on a per share basis and after dividends in 2020 and beyond. This would improve Oxy's dividend safety and growth outlook.

Source: Oxy Investor Presentation

Overall, from a dividend safety perspective, Oxy's payout appears to remain sustainable. The company has several reasonable levers it can pull to improve free cash flow and begin paying down debt. While talk can be cheap, management has also voiced strong support for maintaining Oxy's dividend.

With that said, an acquisition of this size still increases both executional and financial risks. Oxy's debt load will balloon to riskier levels, making the company more dependent on a favorable oil price environment as it looks to divest assets and improve its free cash flow generation to rapidly reduce leverage.

Due to the firm's higher expected leverage, Oxy's Dividend Safety Score could be downgraded if the company does not quickly improve its balance sheet and cash flow generation as management expects. While Oxy's payout should remain on stable ground if everything goes as planned, another untimely crash in the price of oil could create uncertainty. For now, the firm deserves the benefit of the doubt.

Investors should also remember that Oxy's acquisition offer has not yet been accepted by Anadarko, nor does it have an expiration date. Chevron might come in with a counteroffer, so this situation could remain fluid until the bidding war comes to an end. If Oxy ultimately wins but the terms of the deal materially change, we will provide another update.