Reviewing Chevron's Dividend Safety Following $33 Billion Acquisition

Chevron (CVX) shares fell 5% on Friday after management announced a $33 billion deal to buy Anadarko Petroleum (APC).

As a result of this cash-and-stock acquisition, Chevron's debt load will increase and its payout ratio will rise. Let's take a closer look at why the company wants to buy Anadarko and how the transaction affects Chevron's dividend safety profile.

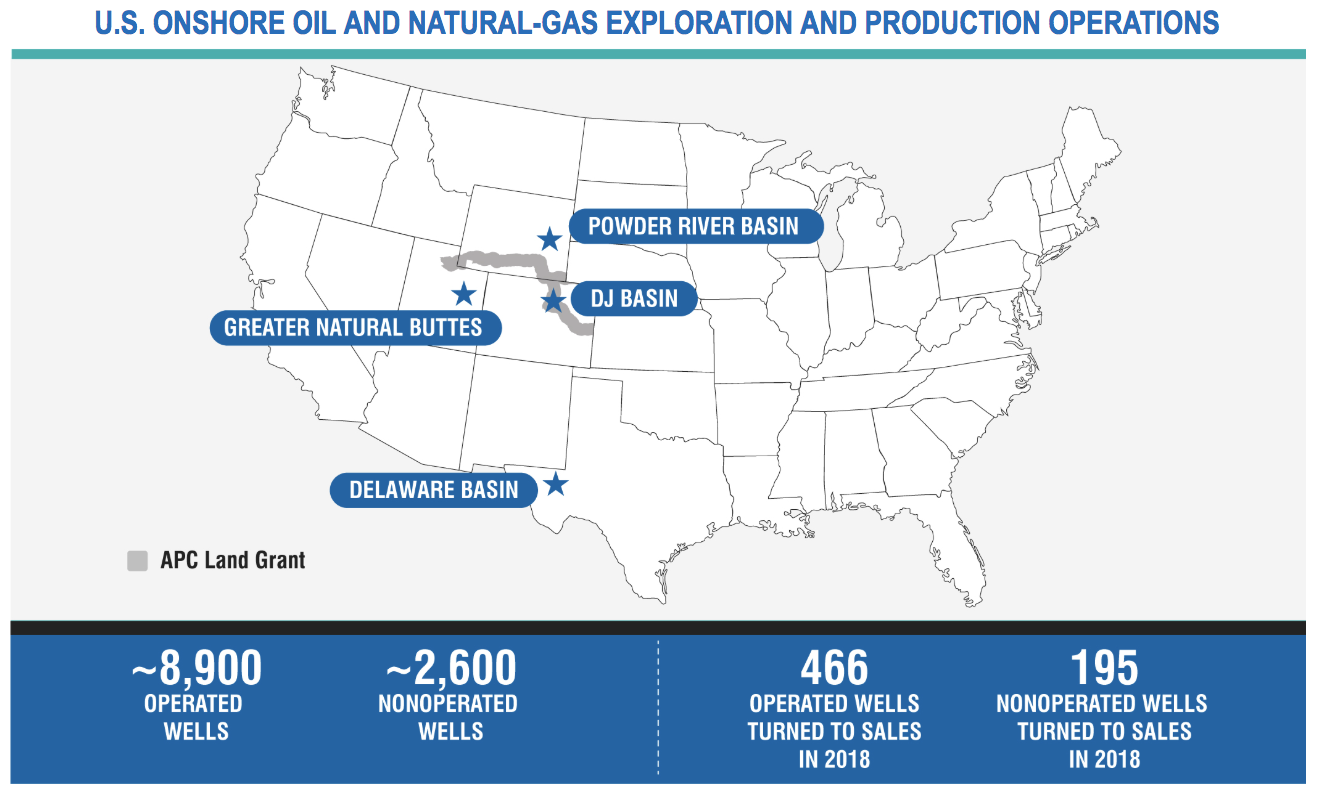

Why Chevron is Buying Anadarko Anadarko is one of the biggest independent oil and gas production companies in America. The firm's U.S. operations account for 86% of its sales volume and 90% of its proved reserves. Importantly, Anadarko has a strong presence in some of the country's most prolific shale regions.

Source: Anadarko Annual Report

Thanks to advances in fracking technology, extracting oil and natural gas from large shale deposits has become increasingly economical over the past two decades, unlocking exponential production growth in America.

For example, in 2000 shale gas accounted for just 2% of U.S. natural gas production but makes up over 40% of production today, according to the Global Energy Institute. And in oil, the U.S. is now the world's top producer.

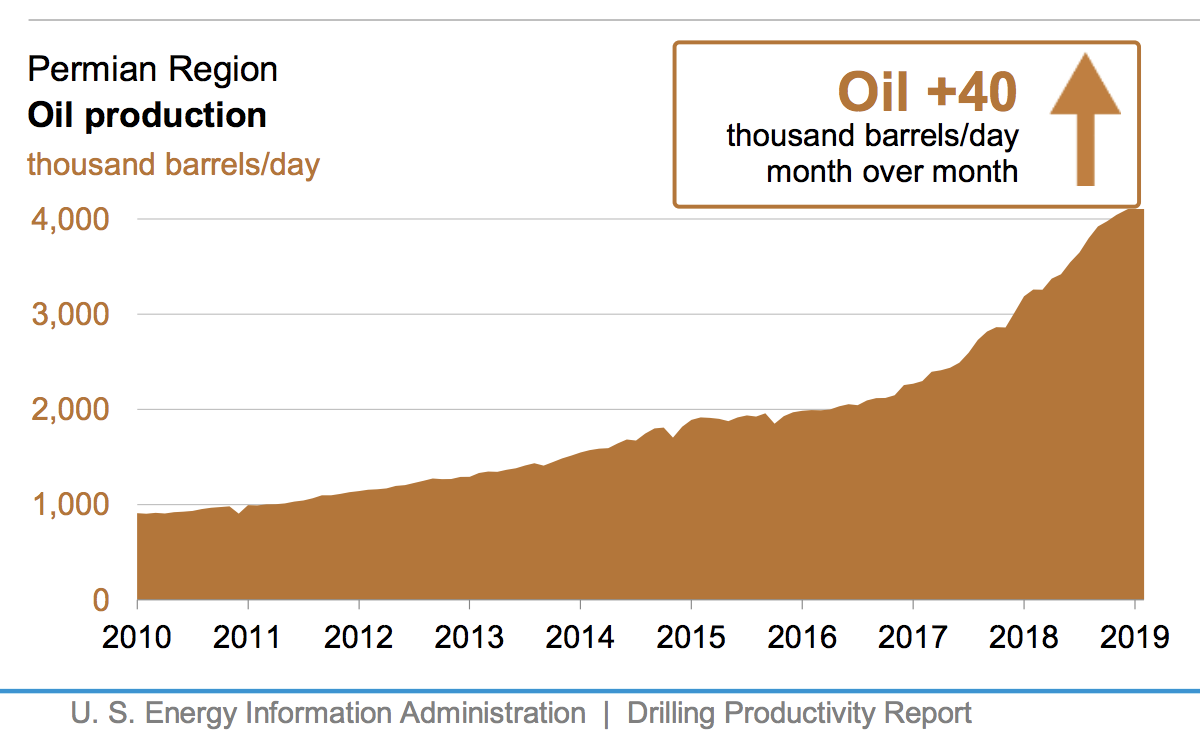

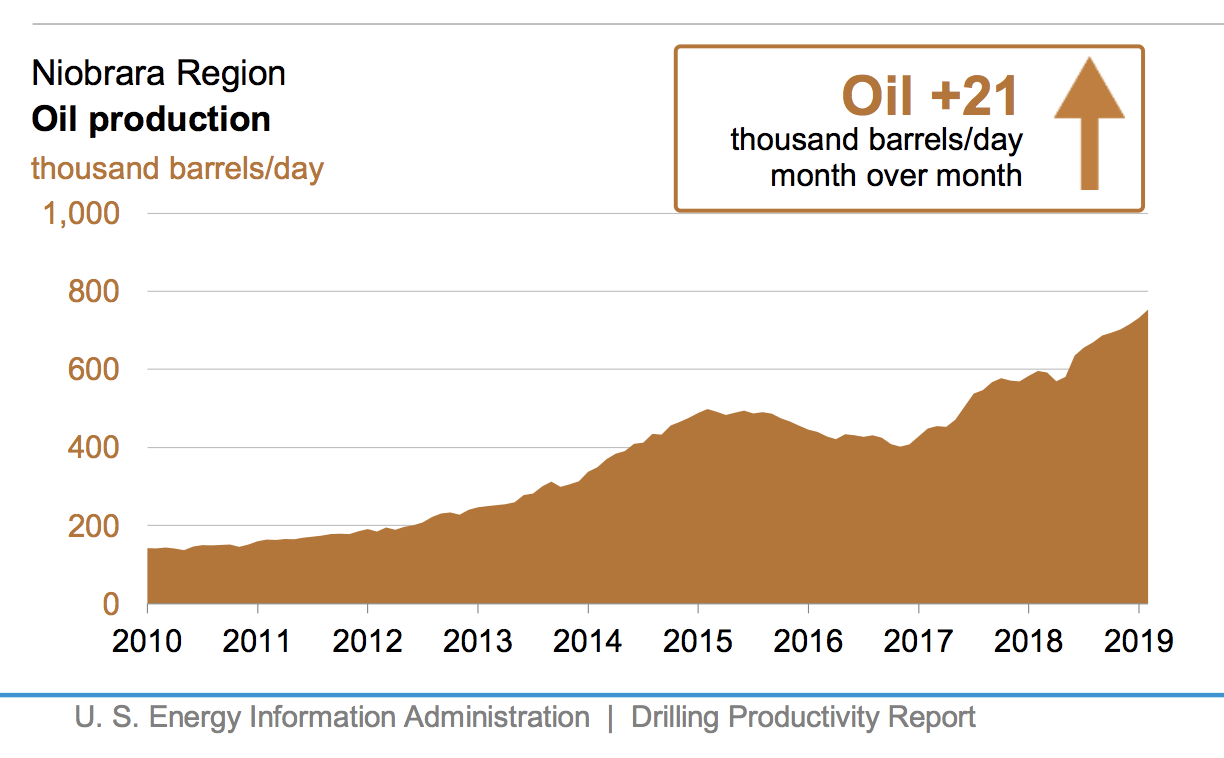

Anadarko is one of the largest shale drillers in the Permian basin in Texas, which is the second-most-productive oil field in the world. As you can see, oil production in this region has increased from less than 1 million barrels per day in 2010 to more than 4 million today. In the Niobrara-DJ region, which runs through Colorado and parts of Wyoming, oil production has increased from less than 200,000 barrels per day to nearly 800,000 today. But despite this boom in output and the bounce in the price of oil, independent energy producers were struggling. Prior to Chevron's offer, Anadarko's stock was down nearly 60% since August 2014 and off over 35% since early July 2018.

Smaller producers were under pressure from rising drilling costs and volatile energy prices. Travis Stice, CEO of Diamondback Energy, remarked, "Realized pricing in the Permian Basin is near levels not seen since the end of 2016 while service costs have increased by about 35 percent during the same time period."

Investors punished most of these companies and wanted to see them cut costs, reduce their spending, and improve their cash flow. Chevron presumably viewed Anadarko as an opportunistic purchase it could make to expand its asset base in some of America's most important energy production regions.

In fact, citing data from analytics firm Rystad Energy, The Wall Street Journal notedthat the "value of Chevron and Anadarko's fracking prospects exceeds $100 billion, more than double the nearest rivals."

Thanks to its large size and integrated operations, Chevron appears to be better positioned to handle the challenges that have weighed on independent oil and gas producers. The company can put more pressure on contractors to achieve cheaper drilling rates and also afford to use the best technologies, for example. Synergies from the deal should also help.

While management expects to accelerate spending in Anadarko's Permian acreage, the combined company's capital expenditures are expected to be reduced by $1 billion per year though eliminating overlap, rationalizing exploration spend, and funding only the most economic projects.

Chevron also sees opportunity to streamline the combined organization. The firm believes it can capture efficiencies and other cost synergies to generate $1 billion per year in cost savings.

Besides its quality shale assets, Anadarko is also working on a major liquefied natural gas export plant in Mozambique, has several deepwater assets around the world, and owns a stake in a midstream business.

Overall, assuming the deal closes as expected later this year, Anadarko increases Chevron's exposure to strategic parts of America's energy production. Anadarko would account for approximately 16% of the combined company's annual operating cash flow generation, and Chevron expects the combined company's production growth rate during the next five years to be consistent with its prior guidance, 3% to 4% per year.

Let's review how the deal could affect Chevron's dividend safety.

Chevron's Dividend Expected to Remain Safe and Growing Thanks to Chevron's solid financial health and the stock-heavy nature of this deal (funded with 75% stock, 25% cash), the company's dividend should remain safe. Chevron will issue approximately 200 million shares (about a 10.5% increase) and pay $8 billion in cash for Anadarko.

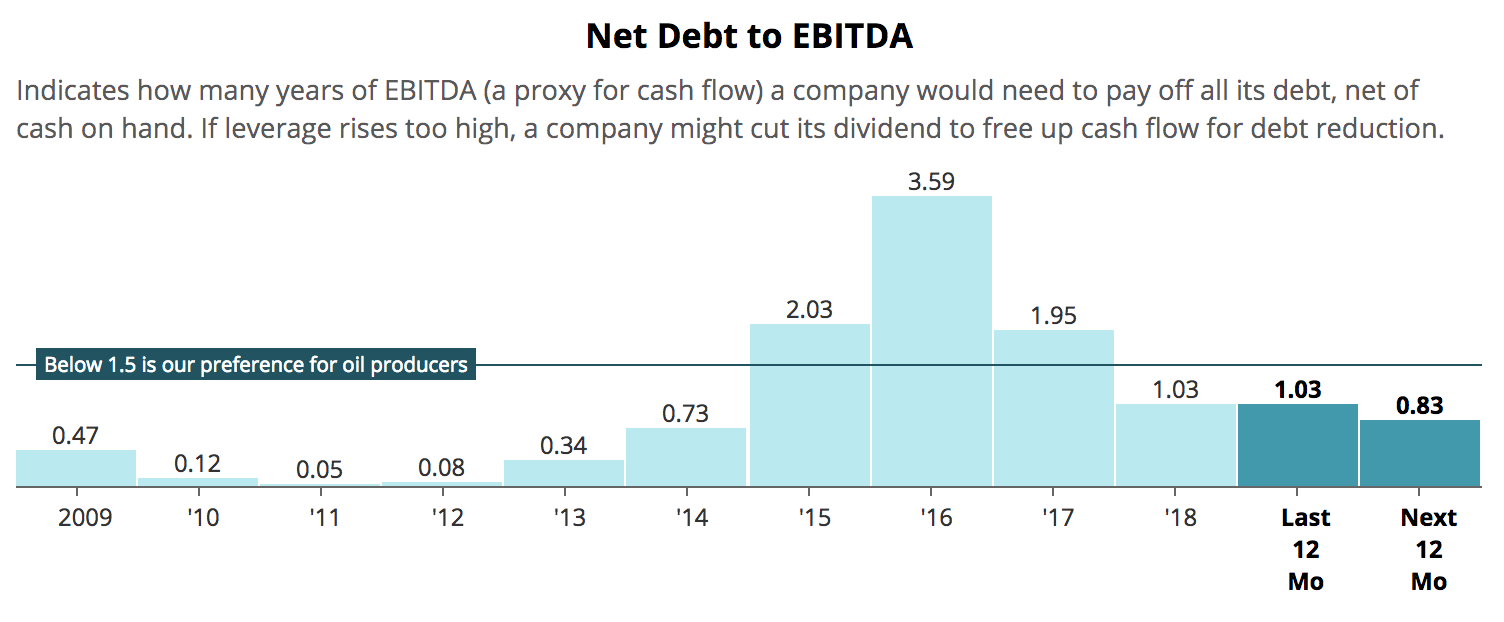

Large acquisitions can imperil a company's dividend if they result in too much leverage, especially in a cyclical sector like energy. Fortunately, according to our analysis, Chevron's forward net debt to EBITDA ratio will increase from 0.83 to about 1.25, which continues to represent a healthy level for oil producers.

Source: Simply Safe Dividends

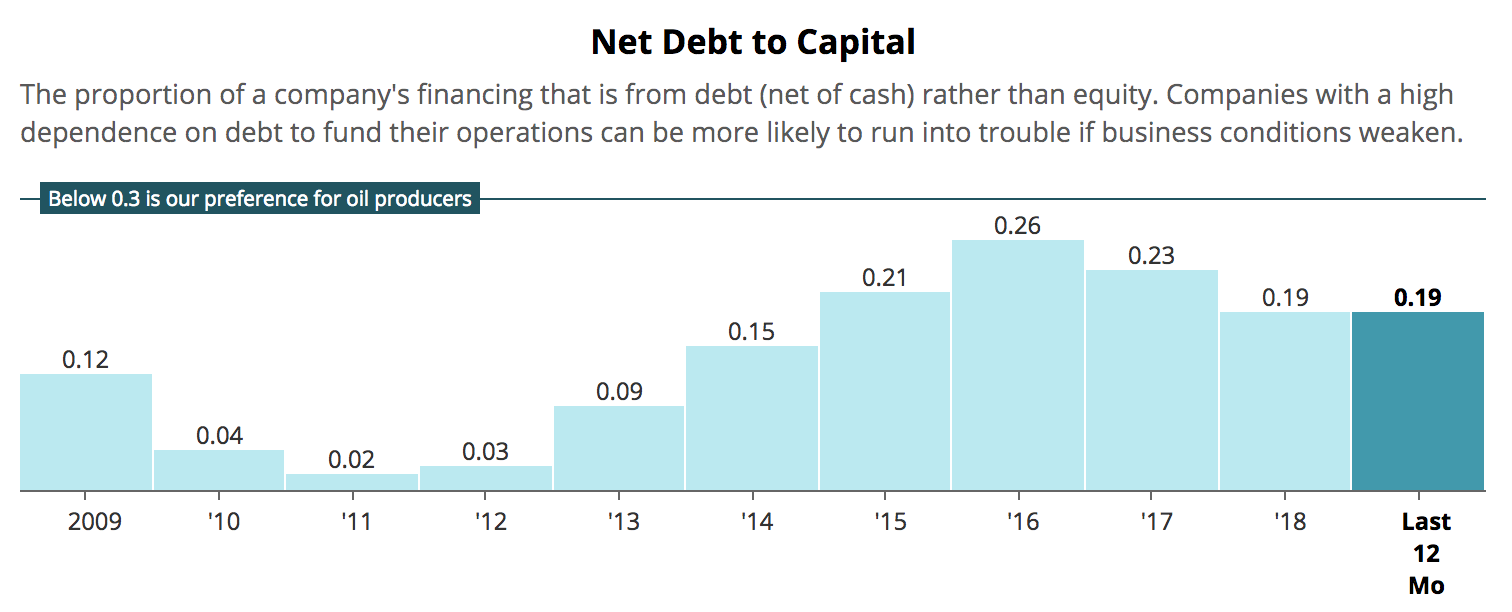

Similarly, Chevron's net debt to capital ratio will likely rise from 19% today to 25% or slightly higher once the deal closes. Once again, that's a reasonably strong level.

Source: Simply Safe Dividends

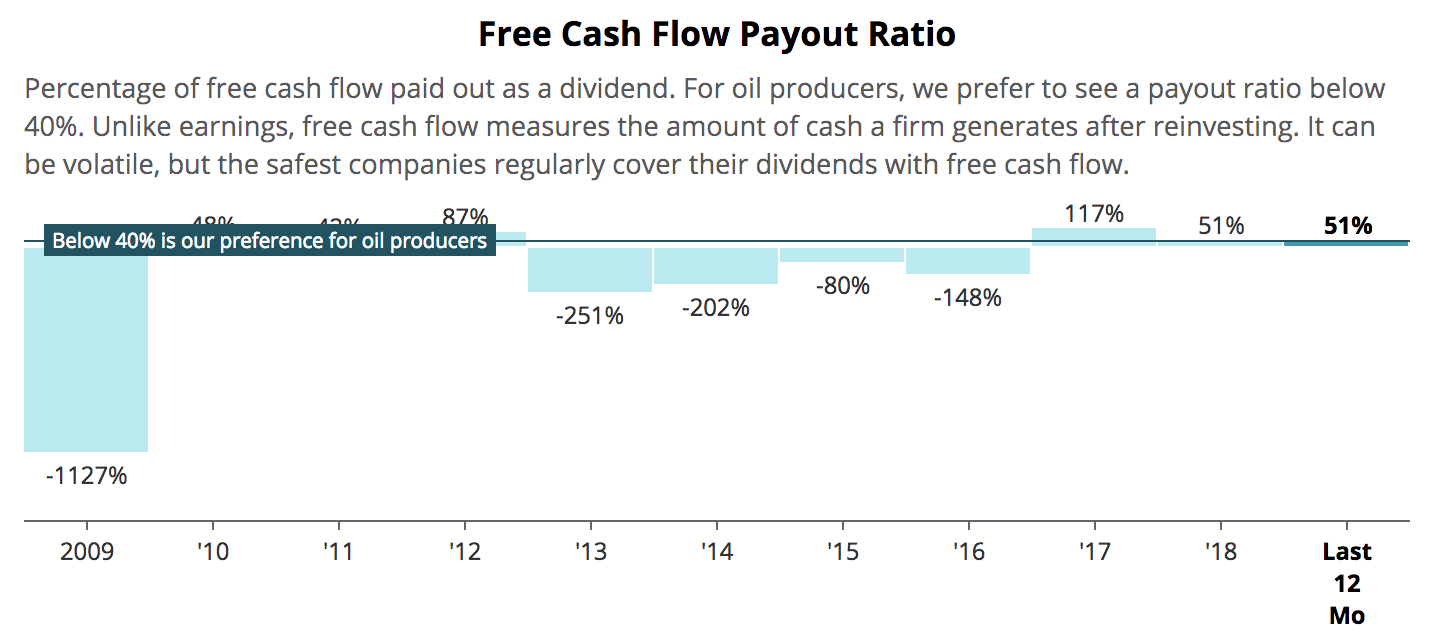

From a payout ratio perspective, in 2018 Anadarko and Chevron generated a combined $36.5 billion of operating cash flow while racking up $20 billion of capital expenditures, resulting in $16.5 billion of free cash flow. After accounting for the 200 million shares Chevron will issue, the combined company's annual dividend obligation will total about $10 billion.

In other words, without accounting for any integration costs, synergies, higher interest expenses, or future asset divestitures, the combined company's 2018 free cash flow payout ratio would have been approximately 61%. That's higher than the 51% level Chevron recorded but not unreasonable for a large integrated energy company.

Source: Simply Safe Dividends

After paying dividends, Chevron will likely generate at least $6 billion per year in excess free cash flow it can use to reduce the $61 billion net debt burden we project for the firm.

Assuming management hits on its $2 billion synergy target and delivers low single-digit production growth, Chevron's retained cash flow has good potential to increase, further solidifying the company's strong financial profile.

In fact, within a year of the deal closing, Chevron's annual retained cash flow could equal the entire amount of net debt ($8 billion) it needed to complete this transaction.

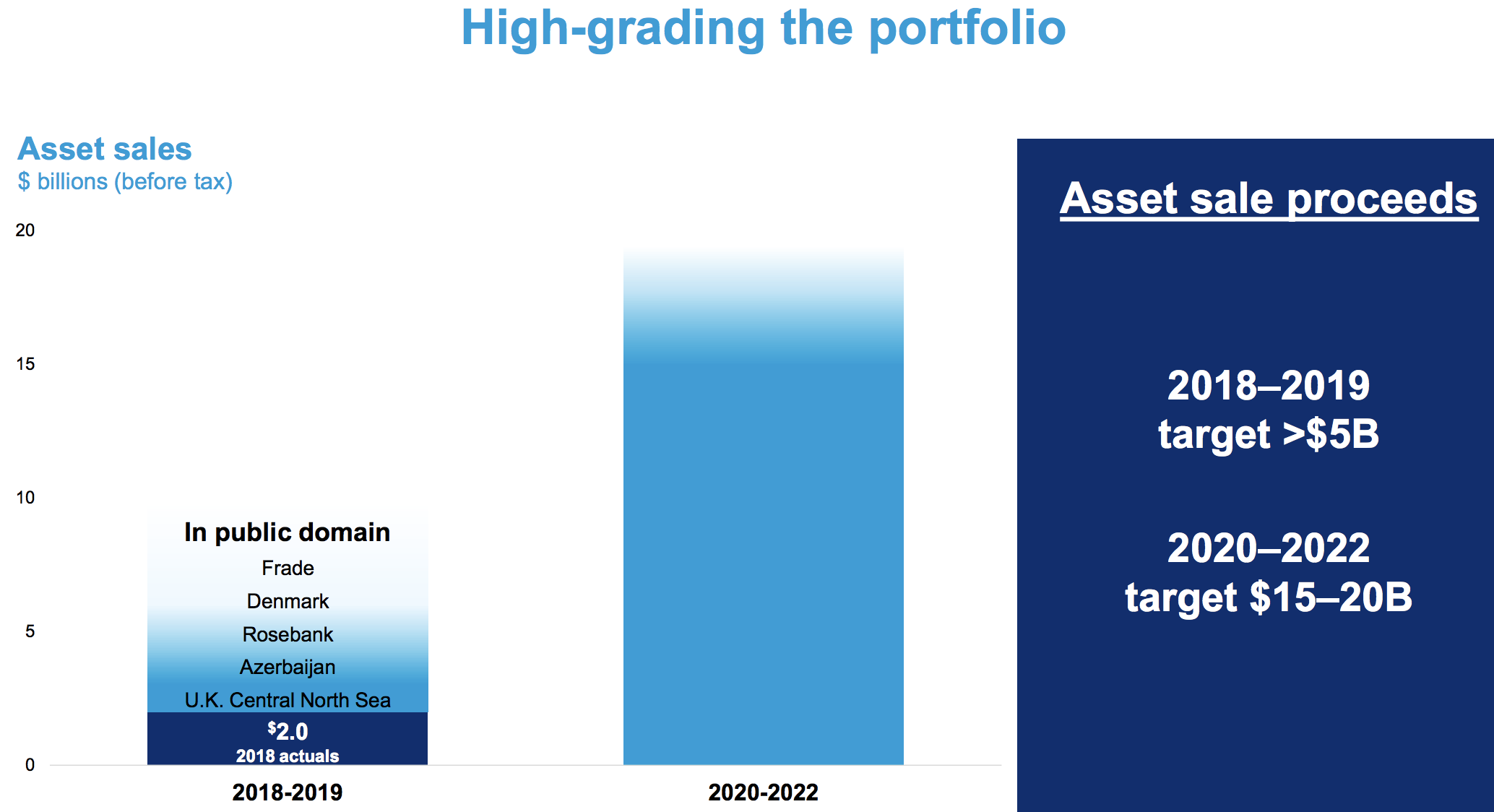

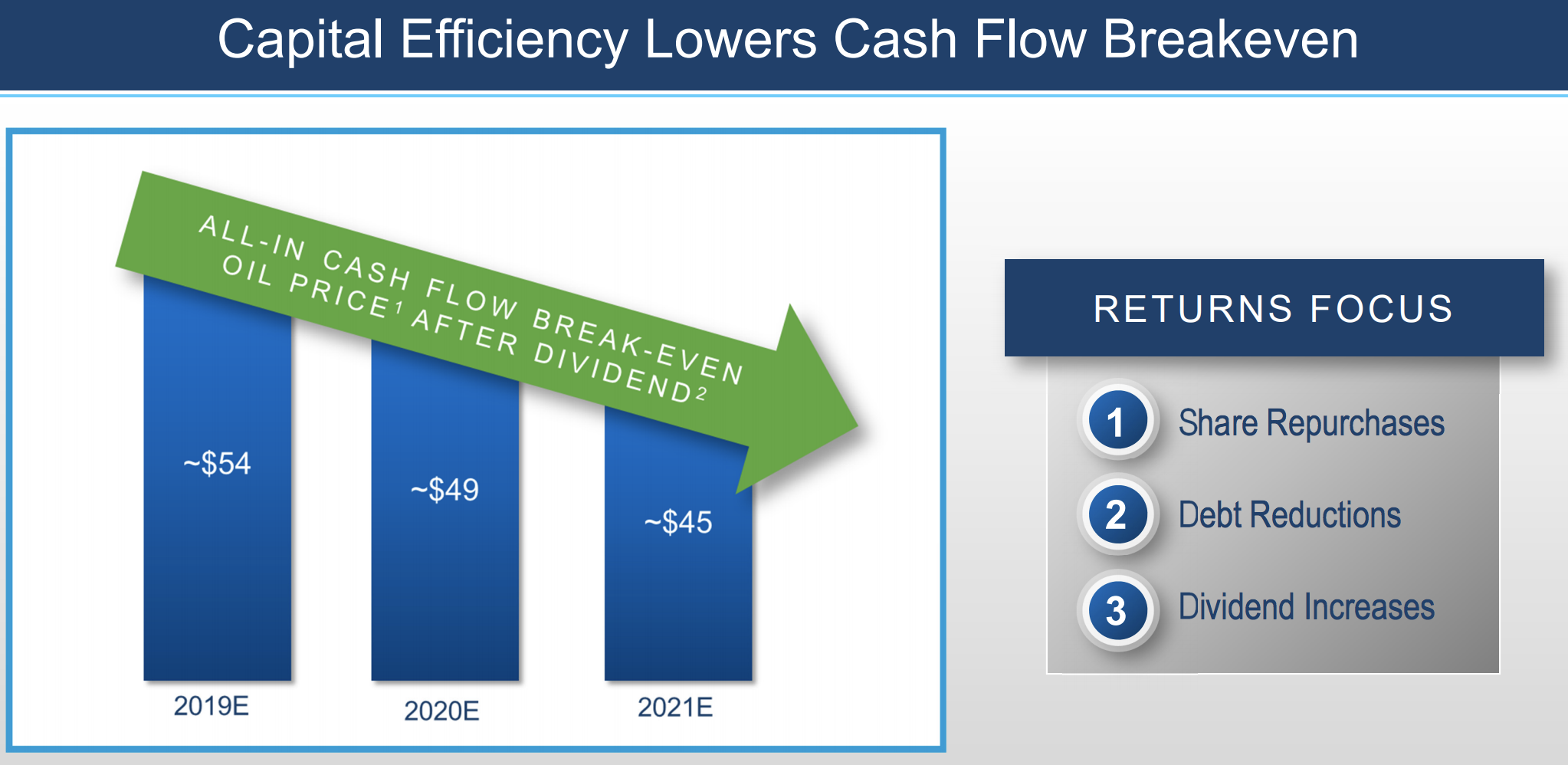

Management also expects non-core asset sales to help Chevron reduce debt and maintain healthy financial flexibility. The company targets $15 billion to $20 billion of asset divestitures between 2020 and 2022.

Source: Chevron Investor Presentation

The bottom line is that acquiring Anadarko does not appear to threaten Chevron's dividend safety. The firm's payout ratio and leverage metrics should remain on solid ground, and the combined company has several levers it can pull to reduce its debt load in a timely fashion.

With that said, Chevron is acquiring a more volatile business. While Chevron's integrated operations continued generating profits during the 2014-16 oil crash, Anadarko's more concentrated business racked up heavy losses (see below).

Source: Simply Safe Dividends

As a result, Anadarko slashed its dividend by 81%, marking its first cut in company history. Since Anadarko will account for around 16% of the combined company's cash flow going forward and management has planned significant asset divestitures which could be affected by energy prices, Chevron's overall performance will likely become more sensitive to the price of oil.

Fortunately, Chevron remains conservatively managed and in solid financial health, so its somewhat higher dependence on oil seems unlikely to imperil the dividend during the next downturn in energy markets.

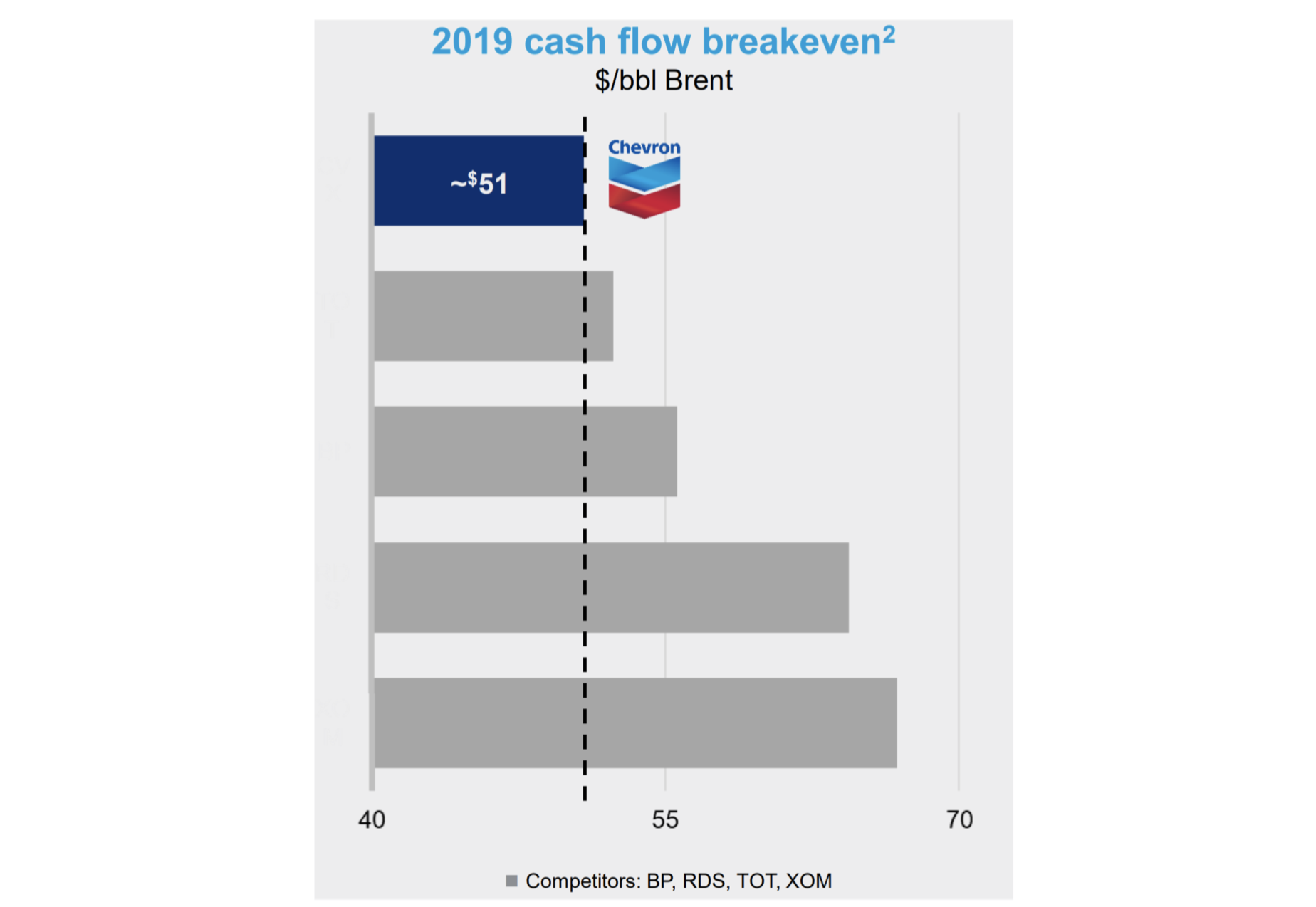

Both companies have worked hard to lower their breakeven prices for cash flow after dividends, too. Chevron boasts the lowest 2019 cash flow breakeven point in the industry at $51 per barrel, for example.

Source: Chevron Investor Presentation

And Anadarko expects to reduce its all-in cash flow breakeven level down to $54 per barrel this year, with ambitions of hitting $45 per barrel by the end of 2021.

Source: Anadarko Investor Presentation

Thanks to these improved efficiencies, plus expected synergies, Chevron expects the transaction to be accretive to (i.e. increase) its free cash flow and earnings per share one year after closing, at a Brent oil price of $60 per barrel (currently at $71 per barrel).

Outside of the financials, Chevron CEO Mike Wirth voiced his ongoing commitment to the company's dividend on the conference call as well:

"Our financial priorities haven’t changed. The dividend is priority one and sustaining and growing that dividend is job one. The second is to reinvest in the business and that can be organic or inorganic reinvestment to ensure we’ve got good strong cash flow generation capabilities well into the future. The third is to maintain a strong balance sheet. And then the fourth is to return cash to shareholders through share repurchases."

Overall, assuming its acquisition of Anadarko closes, Chevron's strong dividend safety profile appears to remain intact. While the company's payout ratio and leverage metrics will tick up, the combined company remains financially healthy and continues to have a low breakeven point for cash flow after paying dividends.

Chevron's dividend seems likely to continue growing as well (probably at a low single-digit rate), aided by the firm's increased exposure to the fast-growing Permian basin and the accretive nature of the deal one year after closing.

Simply put, for investors who are comfortable with the company's sensitivity to the price of oil, Chevron appears to remain one of the few dividend stocks worth considering as a long-term income investment in the energy sector.