AltaGas Signals Upcoming Change to Dividend Payout Policy

AltaGas (ATGFF) owns energy infrastructure assets across North America. The firm started in the midstream business and expanded into the power and utilities sectors over time.

While these are all capital-intensive businesses, they have mostly been steady cash flow generators as well. As a result, AltaGas enjoys an investment grade credit rating and has rewarded income investors with a generous, moderately growing dividend in recent years.

In January 2017, AltaGas announced a $9 billion deal to acquire WGL Holdings, a U.S. regulated natural gas utility. AltaGas took on substantial debt to finance this deal, which closed this past summer.

Unfortunately, a lot has changed in the midstream space since the deal was first announced. As a capital-intensive business, AltaGas historically relied on being able to issue equity and debt to fund its pipeline projects.

Investors today are rewarding midstream companies that move to a more conservative self-funding model while punishing those with more aggressive growth plans. With AltaGas's share price in the dumps, the company's financing options have become a lot more limited just as its balance sheet has been stretched.

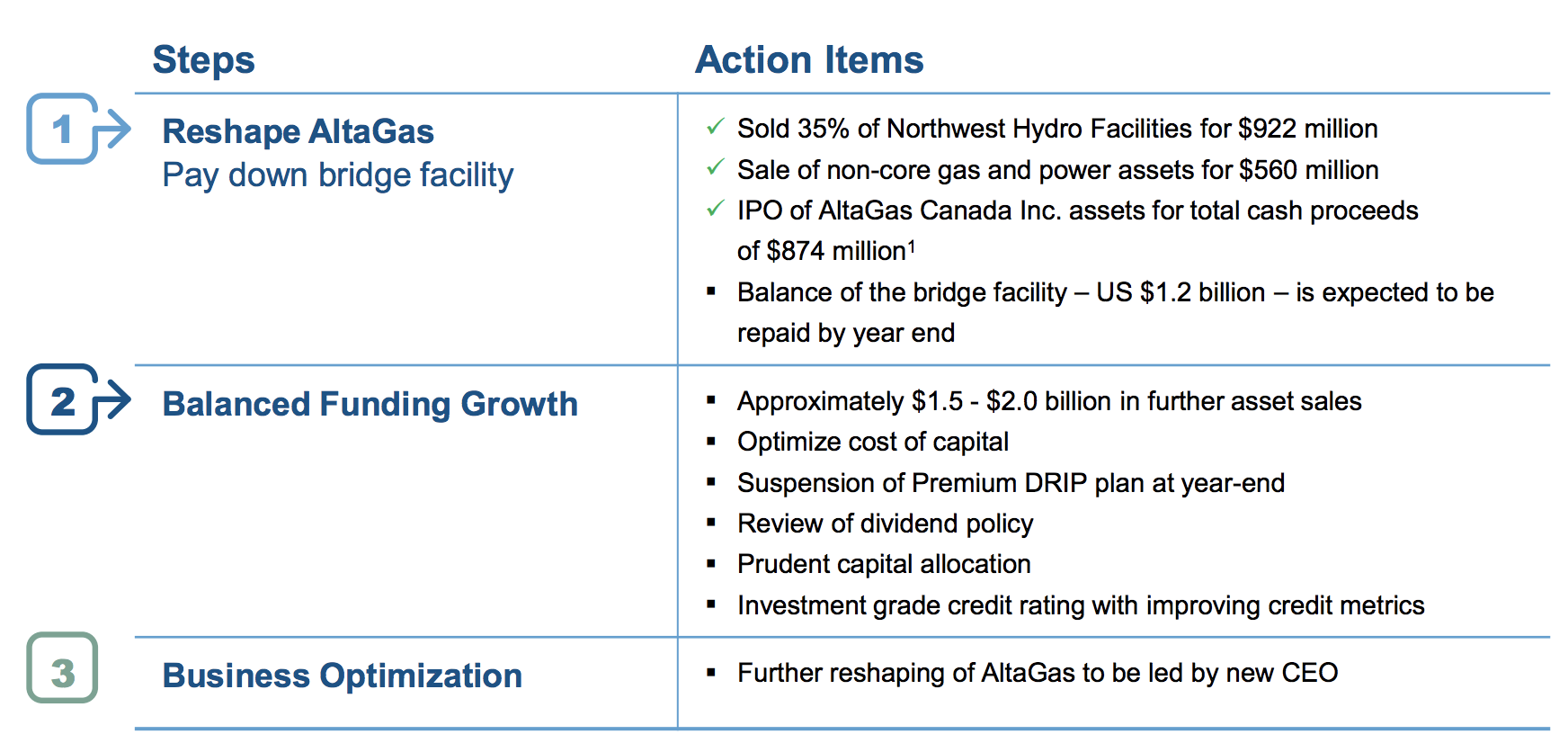

To help protect its investment grade credit rating and reduce leverage, AltaGas is selling more of its assets. Specifically, after already shedding over $2 billion of assets to help fund its acquisition of WGL Holdings, AltaGas announced plans to divest another $1.5 billion to $2 billion of "non-core" assets.

Management announced AltaGas would be suspending its "Premium DRIP" plan at the end of 2018 as well. This plan let shareholders receive shares at a discounted price, but with AltaGas's stock price in the dumps, it didn't make sense to continue the offer.

Source: AltaGas Investor Presentation

Meanwhile, the firm's third-quarter earnings came in lower than expected due to some seasonal and weather issues, as well as a later closing date with the WGL deal.

As the company continues selling off assets to protect its balance sheet, AltaGas's business mix will shift to derive at least half of its EBITDA from utilities.

While regulated utility operations are known for their stability and tend to be owned by dividend-friendly companies, AltaGas plans to use this opportunity to "adjust" its dividend payout policy to better reflect its business mix.

Here are management's comments from the firm's latest conference call:

"Turning to our dividend, this has been an area of focus by the capital markets lately, given where the stock is yielding. We have determined, not surprisingly, that growing the dividend at this time is not appropriate. What we need to assess now in the mix of other factors is what constitutes a sustainable and ultimately growing dividend for the reshaped AltaGas.

It's really a matter of short term yield versus long term growth. With our business mix changing significantly, including the higher contributions from utilities, an appropriate payout for our new longer term asset mix must be identified. A sustainable payout ratio provides additional funding flexibility and allows for long term dividend growth in line with earnings and cash flow per share growth....

I guess when I look at it, there's different appropriate payouts depending on the businesses. If you look at a hydro business can, with very low maintenance, would -- you could justify a long -- a higher payout ratio. I think it's pretty standard for most pure midstream or heavily midstream is kind of a mid payout ratio. And utilities have a lower payout ratio because of their need to invest to maintain the rate base to maintain earnings.

So I think we've become a -- you put those all together to determine what's the appropriate ratio for AltaGas. And if the business mix changes, I think the long term payout target should change appropriately to reflect the business that we're in.

I think in 2017 our largest segment from an EBITDA perspective was power, followed by utilities, followed by gas. And in '19, Tim was saying our largest will be utilities, 50% to 55%, gas at around 35%, and power the smallest at about 15%. So we've dramatically reshaped the company over the -- over this period of time. So I think the dividend payout would make sense to reflect the change in the business."

AltaGas will provide an official update on strategy, 2019 outlook, and capital plans prior to yearend. However, reading between the tea leaves it seems almost certain that management will announce a lower dividend when the time comes.

AltaGas is also searching for a new CEO after the company's former chief executive David Harris resigned abruptly in July following an unspecified "complaint." Harris spearheaded the WGL deal, so his absence puts even more uncertainty around AltaGas's future capital allocation plans.

As a result of these developments, AltaGas's Dividend Safety Score fell from 43 (the very low end of our "Borderline Safe" rating) to 5, signaling its payout appears to be a on very shaky ground. Investors depending on the firm's dividend may want to begin looking elsewhere for yield.