Founded in 1862, Union Pacific (UNP) owns and operates over 32,000 miles of railroads linking 23 states in the western two-thirds of the United States. The company also has about 8,600 locomotives and more than 64,000 rail cars.

The company’s railways connect with all of the major ports on the West Coast and Gulf Coast and serve many of the fastest-growing cities in the country. Union Pacific’s rail network also connects with some of Canada’s railways and all six of Mexico’s major gateways (the only U.S. rail network to do so).

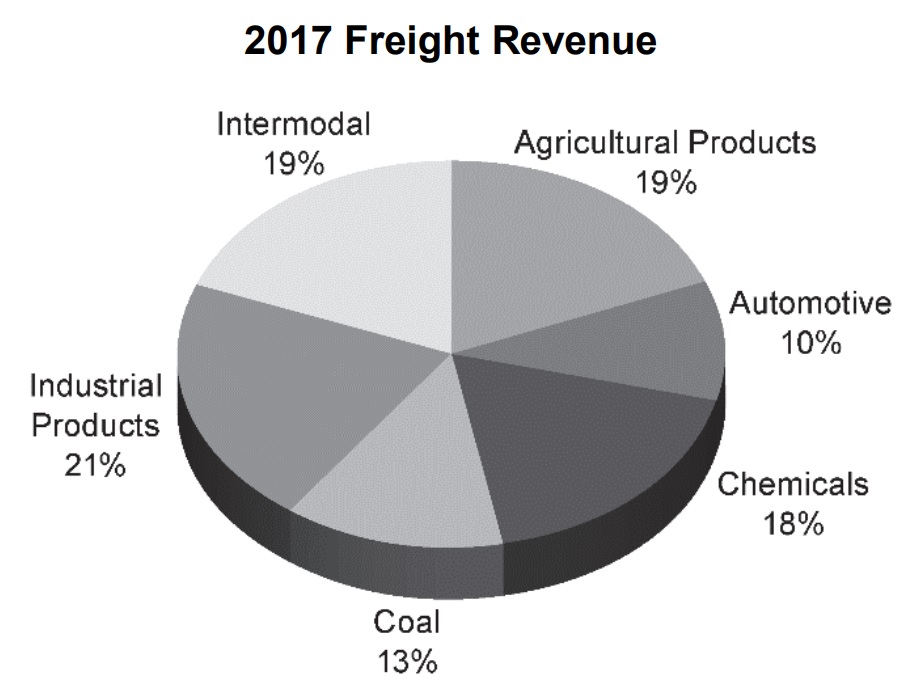

The company serves approximately 10,000 customers across a variety of industries, including agriculture, automotive, chemicals, coal, industrial, and intermodal (shipping containers).

Business Analysis

Railroads are the backbone of America’s economy, moving approximately 40% of U.S. freight as measured in ton-miles (the length freight travels), according to the Federal Railroad Administration. Without companies like Union Pacific, the country’s supply chain could not operate.

Perhaps it is no surprise why Warren Buffett acquired leading railroad company Burlington Northern Santa Fe (BNSF) in 2010 for $34 billion. Union Pacific shares a number of competitive advantages with BNSF, making it an interesting business for long-term dividend growth investors to consider.

First, railroads are by far the cheapest and most efficient way to move most types of goods over land in the regions they serve. In fact, moving freight by rail is four times more fuel efficient than moving freight on the highway, according to CSX.

Trains can move a ton of freight over 470 miles on just a single gallon of fuel, which allows them to charge lower rates compared to other types of transportation, such as highway trucking.

Thanks to the huge expense of building and maintaining rail networks, this is an industry with very high barriers to entry and relatively few major competitors.

For example, Union Pacific’s 32,000 miles of track represent approximately 23% of all rail lines in the U.S., and it’s just one of nine class 1 (revenue above $350 million per year) rail companies in the country.

Along with Burlington Northern Santa Fe (owned by Berkshire Hathaway) and Norfolk Southern (NSC), Union Pacific and its two major rivals control over 60% of America’s total rail miles, effectively making them an oligopoly.

The large incumbents have the scale and efficiencies needed to underprice potential new entrants and remain in control of their key markets. There are also only so many major transportation hubs and consumer markets, further limiting competition.

However, due to their importance to the country, U.S. railroads used to be some of the most regulated companies on earth. The companies were financially and operationally challenged under stringent government oversight until the Staggers Rail Act of 1980 deregulated the industry.

According to the Federal Railroad Administration, prior to 1980, railroads had little flexibility in pricing their services and restructuring their operations to become more efficient.

During periods of inflation, regulation slowed down rate adjustments that railroad operators could realize, crimping profits and causing a number of railways to declare bankruptcy.

In the 30 years leading up to 1980, railroads saw their share of revenue ton-miles plunge from 56% to 38%. The outlook was bleak.

The Staggers Rail Act of 1980 changed everything. Railroads implemented market-based pricing schemes on many routes, invested over $500 billion in capital improvements and maintenance to improve productivity, and train accident rates fell by 65% from 1981 to 2009.

Impressively, the lack of government oversight resulted in freight rates declining by 0.5% per year compared to an increase of nearly 3% per year in the five years leading up to act’s passage in 1980.

The industry’s market share also increased back to 40% of ton-miles and has remained stable. Today, about 20% of railway traffic is still regulated where competition is not deemed to be effective enough to protect shippers.

Throughout the last several decades, the railroad industry has significantly consolidated in an effort to further improve productivity, raise profit margins, and better combat alternative modes of transportation (e.g. trucking).

For example, in 1980 there were 40 class 1 railroads. That figure has fallen about 75% as companies strove to achieve economies of scale and minimize unit cost.

Union Pacific has leveraged its size by spending $34 billion over the last 10 years to maintain and upgrade its transportation network. The company invested $3.1 billion in 2017 (15% of revenue) and plans to spend another $3.3 billion in 2018.

While most types of businesses will spend between 2-4% of their total sales on capital expenditures to maintain and grow their operations, Union Pacific expects spending to average around 15% of revenue over the long term, reflecting the capital intensive nature of the railroad industry.

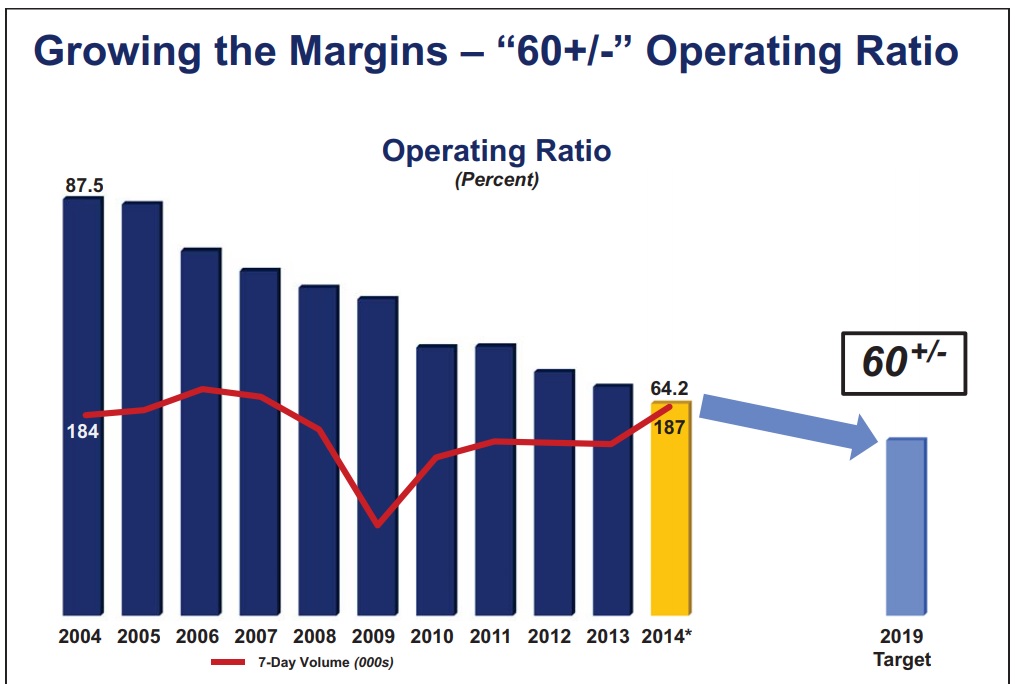

What’s most impressive is how successful management has been over the years in reducing costs despite Union Pacific’s heavy spending. For example, in 2004 the company’s operating ratio (operating costs/revenue) was 87.5%, and its return on invested capital was just 5%.

However, in 2017 Union Pacific’s operating ratio hit an all-time low of 62%, and over the past few years the company’s return on invested capital has been between 14% to 16%.

Management aims to get the operating ratio down to 60% by 2019 with a long-term target of 55%. The key to this steady decline in costs is the railroad’s impressive ability to adapt to fast-changing conditions as well as its “G55 + 0” initiative. This initiative is Union Pacific’s cost reduction plan (begun in late 2015) which aims to achieving a 55% operating ratio in the long run while maximizing safety (zero injuries).

Over the years Union Pacific has proven itself to be highly adaptable to changing industry and economic conditions, too. For example, in 2009 the Great Recession caused company-wide volumes to fall 16%. However, management was able to cut costs even faster and actually boost margins. The same actions occurred in 2015 when coal volumes fell 18%.

Thanks to such improved operating efficiencies, Union Pacific is still capable of generating very strong operating margins (close to 40%) and a double-digit free cash flow margin in 2017. Tax reform will also drop the company’s effective tax rate from 37% to about 25% in 2018, boosting free cash flow by approximately $1 billion.

Over the long term, Union Pacific has two primary growth catalysts. First, freight volumes generally follow population growth over long periods of time. A growing population is expected to result in 22% more rail traffic between 2010 and 2035, according to the Federal Railroad Administration. By 2060, the U.S. Census Bureau expects America’s population to grow to 420 million, 30% larger than today and supportive of higher rail demand over time.

However, the more powerful growth catalyst for all railroads is the potential for volume growth to outpace population growth in several key industries. For example, the U.S. energy boom has created substantial growth potential in shipping volumes for inputs like frack sand or end products such as petro chemicals.

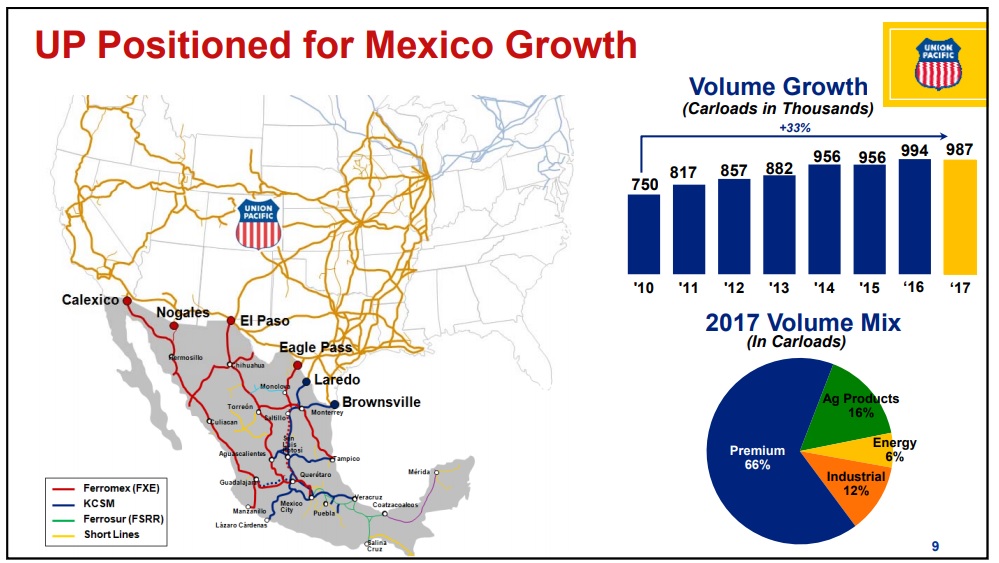

In addition, Union Pacific’s industry-leading connections to Mexico provide it with the best potential for increased trade with that fast-growing developing market.

Union Pacific has excellent growth potential in intermodal (shipping containers) volume growth as well thanks to its key access to West Coast ports. These areas could see strong demand due to increasing U.S. trade with fast-growing Asian markets.

Overall, there will always be a need to connect consumers with agricultural, industrial, manufacturing, and logistics centers across the country. As a best-in-class operator with hard-to-replicate assets, Union Pacific will be there to meet this major need.

Key Risks

There are several important factors to remember regarding Union Pacific’s business.

First, because its revenue and earnings are deeply tied to almost all aspects of the U.S. economy, Union Pacific’s growth and profits will be cyclical. For example, the company’s revenue fell 21% in 2009 and 9% each year in 2015 and 2016 as the price of oil crashed.

In addition, individual business unit volumes are also volatile. For instance, automotive volumes (10% of total) are likely to decline since U.S. auto sales peaked in 2015 and are expected to gradually fall through 2020.

Meanwhile, coal shipments (13% of total) are likely to be in permanent secular decline as natural gas and renewable energy replaces this form of highly polluting and increasingly non-cost competitive form of power.

In addition to having cyclical revenues, Union Pacific’s input costs can also be highly variable. For instance, its hybrid diesel locomotives (electric motors powered by diesel generators) consume a lot of fuel. Union Pacific reported diesel prices increased more than 20% in 2017. Should oil prices continue to rise, this could result in even higher fuel costs for the company that it will need to pass through to customers to avoid margin pressure.

Then there’s the issue of labor costs, which were up 4% in 2017. Approximately 85% of the company’s workforce is represented by more than a dozen unions. As a result, there is risk that future labor contract disputes might lead to a strike and significant business disruption.

And while the railroad industry is far less regulated than it used to be, Union Pacific still faces potential regulatory risks.

For example, the Surface Transportation Board (STB) has jurisdiction over rates charged on certain regulated rail traffic, common carrier service of regulated traffic, freight car compensation, transfer, extension, or abandonment of rail lines, and acquisition of control of rail common carriers.

And the STB is just one of many regulators that Union Pacific must deal with:

- Federal Railway Administration

- Department of Transportation

- The Occupational Safety and Health Administration (OSHA)

- The Pipeline and Hazardous Materials Safety Administration

- Department of Homeland Security

- Environmental Protection Agency

Sometimes these regulators can impose costly (though hopefully necessary) regulatory burdens. One example is the Positive Train Control (PTC) program. This is a collision avoidance technology intended to override engineer controlled locomotives and stop train-to-train and overspeed accidents. The program is expected to be fully implemented by the end of 2018. Union Pacific has spent $2.6 billion on PTC thus far and expects the full cost to be $2.9 billion when completed.

Another risk to consider is a U.S. trade war, which could potentially be triggered by the recently announced 25% and 10% tariffs on steel and aluminum imports, respectively. When combined with a potential U.S. withdrawal from NAFTA, U.S. trade growth could be reduced and dampen one of the company’s growth catalysts.

Most of the risks discussed above are short term in nature. Looking further out, competition from other modes of transportation could pose a threat to Union Pacific’s long-term earnings power if they take share away from railroads.

Trucks, barges, ships, planes, and pipelines all compete with railroads to efficiently and reliably transport goods. However, rail transportation has been, and will likely continue to be, the best option for shipping bulk commodities such as grain, construction materials, and energy products.

These materials have a high weight-to-price ratio and generally do not require time-sensitive deliveries. Railroads can transport these bulk materials using less fuel than trucks over long distances and are usually faster than using waterways, which face physical limitations. Rail’s market share of ton-miles seems likely to remain stable around 40% just like it has for a couple of decades.

Overall, barring a secular decline in commodity consumption, it’s hard to find many risks that could impair Union Pacific’s long-term earnings power.

Any given quarter could be somewhat rocky due to unpredictable fluctuations in various commodity, industrial, and consumer markets, but that has no bearing on Union Pacific’s long-term competitive advantages and excellent financial health (an “A” credit rating from S&P).

Closing Thoughts on Union Pacific

Union Pacific is a durable company that is sensitive to economic growth and a number of different commodity markets.

However, freight demand should continue to expand with population growth over the long term, and Union Pacific’s railroads will likely remain an essential component of our country’s supply chain for many years to come.

The company’s strong competitive advantages, predictable business model, and conservative management team have enabled the business to pay uninterrupted dividends since 1998 and increase its payout every year since 2007.

Union Pacific appears to be a reasonable business to consider for long-term dividend growth investors who are comfortable having exposure to industrial-sensitive stocks.

To learn more about Union Pacific’s dividend safety and growth profile, please click here.

Leave A Comment