Founded in 1961, Lancaster sells branded frozen dinner rolls and garlic bread, croutons, salad dressings, bottled sauces, and other specialty food products to retailers and restaurants.

Source: Lancaster Investor Presentation

Compared to its peers, Lancaster has been hit harder by commodity cost inflation due to its higher exposure to dressings, which we estimate account for at least one-third of sales.

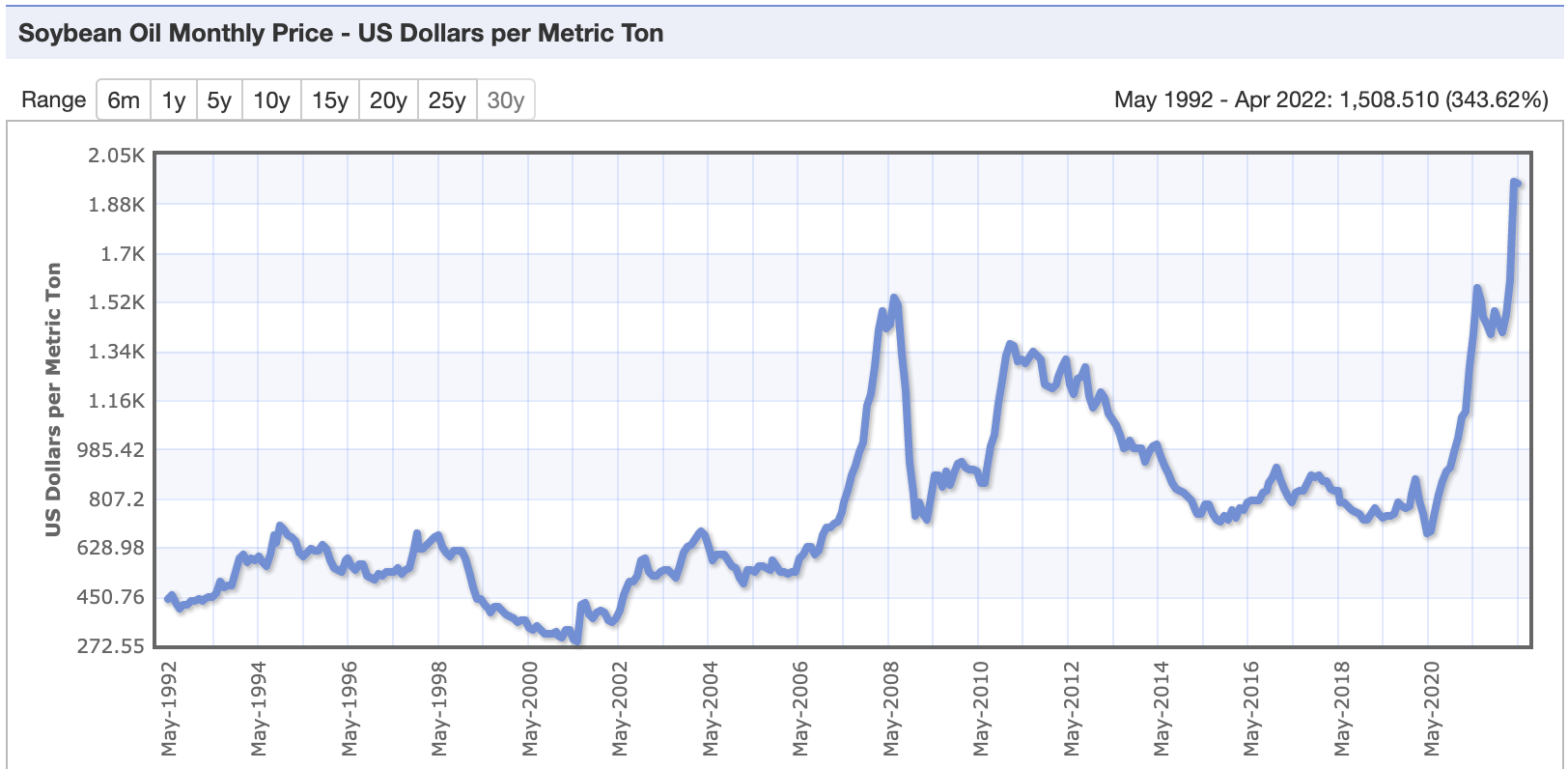

Soybean oil is used in most salad dressings, and prices have surged this year due to drought conditions hurting crops and the Russian invasion of Ukraine, a leading exporter of certain edible oils.

Source: Index Mundi

The price of wheat, a key ingredient in Lancaster's bread products, also increased as much as 50% earlier this year as war-ravaged Ukraine is unable to deliver its historical 10% share of global exports for this essential commodity.

Overall, edible oils and wheat are driving about two-thirds of the total inflation Lancaster is seeing. Across raw materials, packaging, and freight, Lancaster experienced nearly 30% inflation last quarter, well ahead of management's expectations.

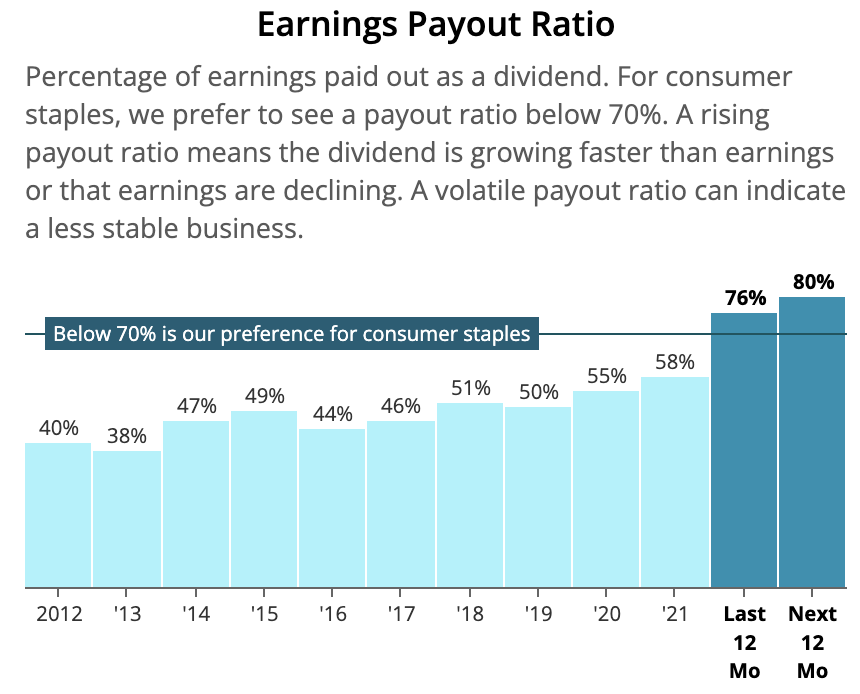

With margins under pressure, Lancaster's adjusted earnings per share have fallen roughly 20% over the past year despite 15% sales growth. The slump in profits has pushed Lancaster's payout ratio towards 80%, marking the company's highest level in at least a decade.

Source: Simply Safe Dividends

We expect Lancaster's profitability and dividend coverage to eventually return to historical levels. The majority of commodities used by the firm sit at or near 10-year highs, incentivizing more production and potentially marking a cyclical peak as harvests improve.

Meanwhile, management is implementing additional price increases, investing in cost efficiency projects such as more factory automation, and reducing dependence on higher-cost co-manufacturers, which have supported Lancaster's growing relationship with Chik-fil-A (21% of sales last year).

Lancaster's financial position will remain strong as it waits for profitability to improve. The company maintains a debt-free balance sheet and holds $67 million of cash – nearly enough on its own to cover the firm's roughly $90 million dividend for a year.

Overall, we expect Lancaster to remain a cash cow and defend its track record of paying higher dividends each year since 1963, a streak matched by only 12 other U.S. companies.

Trading at a relatively high dividend yield compared to its historical norm, Lancaster's stock may appeal to dividend growth investors looking for a well-run business that can endure the challenging inflationary environment with its long-term outlook intact.