Softening Appliance Demand Not a Threat to Whirlpool's Dividend

Demand for refrigerators, dishwashers, laundry machines, and other big-ticket appliances seems likely to slow further in the months ahead following two pandemic-fueled bumper years.

Evidence is stacking up that consumers are shifting more of their spending from goods to services, with many households feeling pinched by persistent inflation and rising interest rates.

Big-box retailer Target in May warned that it had seen "a rapid slowdown" in discretionary merchandise categories such as apparel, home goods, and hardlines. This left the company with too much inventory, particularly in bulky categories such as kitchen appliances.

Whirlpool itself had even warned of slowing demand when it reported first-quarter earnings results in April. Management flagged that North American industry volumes remained 24% above 2019 levels but fell 4% from a year earlier, a trend that could accelerate in a recession.

Coupled with rampant inflation, Whirlpool appears poised for a period of lower revenue and falling margins. Fortunately, we expect the company to handle these headwinds with its dividend intact.

The home appliance market is very mature in developed countries where Whirlpool conducts most of its business because population growth rates there are very low.

As a result, we estimate Whirlpool generates at least half of its revenue from replacement sales as consumers often replace worn out appliances with the same brand in order to match the other appliances in their house.

As the world's largest appliance manufacturer, Whirlpool's large installed base can continue providing reliable cash flow during a downturn to keep the firm profitable even as discretionary purchases and appliance sales tied to new housing construction face sharper declines.

For now, Whirlpool expects to generate $1.25 billion of free cash flow this year, comfortably covering the company's $430 million dividend.

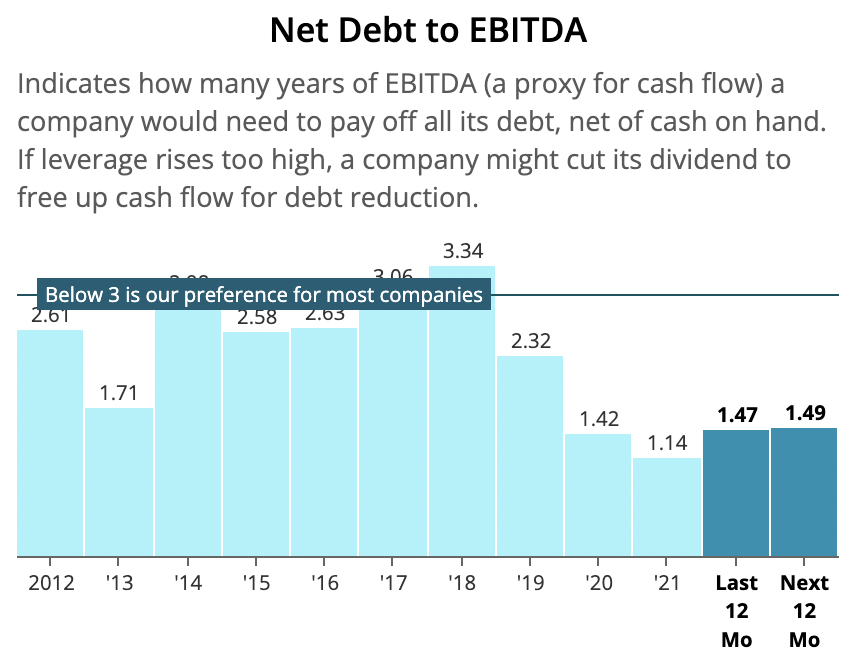

It's also worth noting that Whirlpool's leverage ratio sits below its pre-pandemic level and beneath management's long-term target. This provides support for Whirlpool's BBB credit rating and offers additional financial flexibility to defend the dividend.

Source: Simply Safe Dividends

No more than a few hundred million dollars of debt are set to mature in each of the next five years either, reducing refinancing risk. Whirlpool's liquidity is also strong with $2.1 billion of cash on hand.

Outside of Whirlpool's financial strength, it's worth mentioning that management is conducting a strategic review of the firm's Europe, the Middle East, and Africa (EMEA) division.

The review is expected to be completed by the third quarter and could result in Whirlpool deciding to divest the entire business. The EMEA segment accounted for 23% of sales last year but only 4% of adjusted operating income, so we would be surprised if a potential divestiture would necessitate a dividend cut.

Overall, Whirlpool heads into this period of slowing economic growth in excellent financial health. We expect the firm to continue its streak of paying uninterrupted dividends since 1972 despite its somewhat cyclical earnings profile.