Kraft Heinz (KHC) has roots dating back to 1869. The company was formed by the $45 billion merger of Heinz and Kraft in 2015 which created the fifth largest food maker in the world, and the third largest in the U.S. with more than $25 billion in revenue.

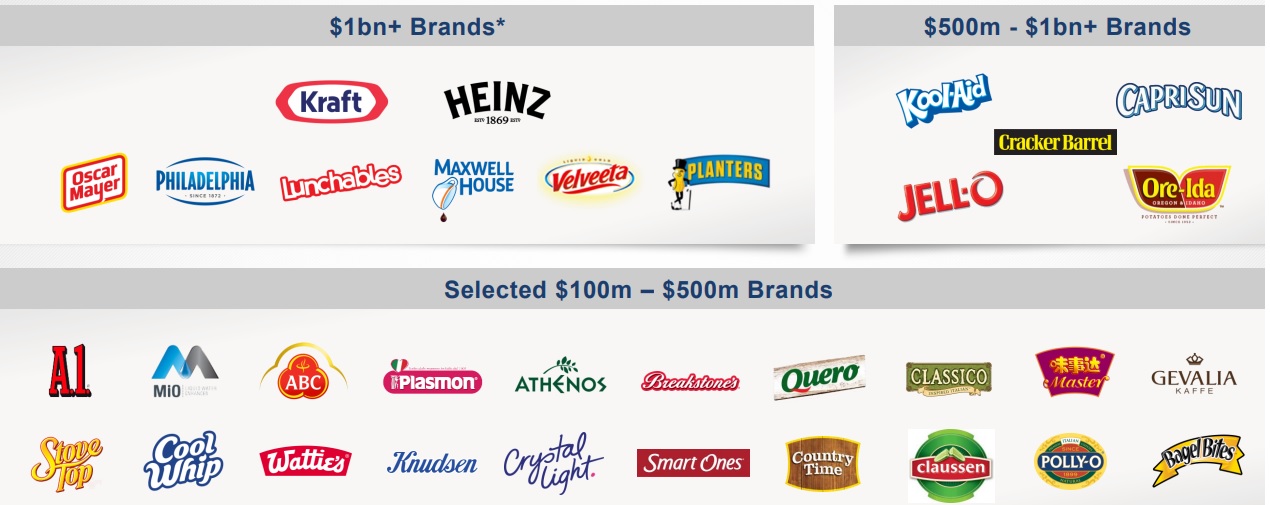

Today Kraft Heinz operates 83 manufacturing facilities around the world. The company sells products in over 190 countries under numerous household brand names such as: Heinz, Kraft, Oscar Mayer, Philadelphia, Velveeta, Lunchables, Planters, Maxwell House, Capri Sun, Ore-Ida, Kool-Aid, Jell-O.

Kraft Heniz’s sales are highly diversified by food type:

- Condiments and sauces: 25% of revenue

- Cheese & dairy: 21%

- Frozen meals: 10%

- Meats & seafood: 10%

- Shelf-stable meals: 9%

The company’s sales are highly concentrated with its largest wholesale clients. For example, Walmart (WMT) accounted for 21% of company sales in 2017. Kraft Heinz’s top five customers in the U.S. represent 48% of sales, and in Canada the top five buyers drove 72% of revenue last year.

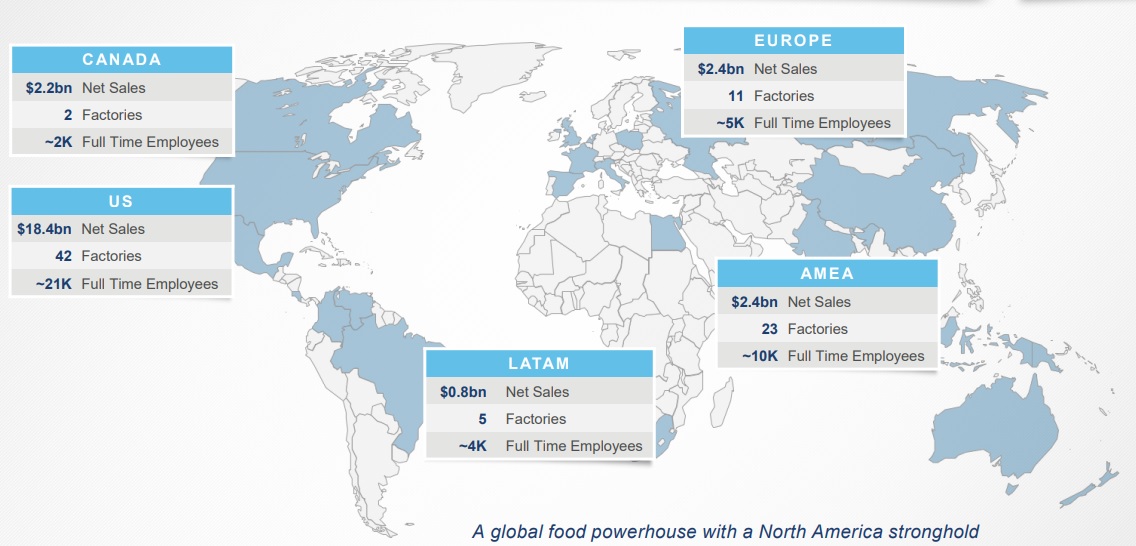

Geographically, Kraft Heinz remains heavily concentrated in the U.S., which accounts for approximately 70% of sales. Canada, Europe, and the rest of the world account for 8%, 9%, and 13% of revenue, respectively.

Business Analysis

Consumer staples companies such as Kraft Heinz enjoy several qualities that potentially make them solid income investments. For one thing, these businesses tend to have stable sales and recession-resistant cash flow.

That’s largely thanks to people’s constant need to eat, as well as Kraft Heinz large portfolio of well-known brands, including eight that generate over $1 billion in sales each year.

Over their corporate lives, Kraft and Heinz have spent billions of dollars on marketing to favorably alter consumers’ awareness and perceptions of their products. As a result, the company has historically been able to raise prices without seeing a major impact on demand.

With products in virtually every U.S. household (management estimates that Kraft’s household brands account for about 5% of all U.S. grocery sales) and leading market share positions across most core product categories, Kraft and Heinz are key vendors for the retailers that sell their products. They can also afford to invest in in-store displays, coupons, and rebates to help consumers buy more products.

As a result, it’s hard for new entrants to take shelf space from these giants and convince consumers and retailers that they are better. They lack the capital for marketing, and building brand awareness takes a very long time.

Kraft Heinz’s extensive distribution channels are another competitive advantage. As the company develops new products or acquires other brands, it can sell these new offerings to existing customers while improving their cost profile as they quickly scale. This helps the business respond to evolving consumer tastes to remain relevant.

The company also enjoys large economies of scale thanks to the integration of its own manufacturing, supply, and logistics chain with that of Heinz, which keeps its costs very competitive. The seed was planted to eventually combine Kraft and Heinz around five years ago.

In 2013, Warren Buffett’s Berkshire Hathaway (BRK.B) partnered with Brazilian private equity firm 3G capital to buy Heinz for $23 billion. The deal left Berkshire and 3G with 50% ownership in one of the largest food companies in the world, with nearly $12 billion in 2012 sales. About 60% of revenue was generated outside the U.S., with most from Europe, but about 25% from fast-growing emerging markets.

Then, in 2015, Heinz bought Kraft in a $45 billion deal that would combine Kraft’s dominant position in the U.S. with Heinz’s stronger global presence. Today Berkshire and 3G own 27% and 24% of Kraft Heinz, respectively. 3G, famous for its cost-cutting prowess, said it would help the combined company slash $1.5 billion in annual costs within three years.

Thanks to a strong focus on synergistic cost savings, closures of less efficient production facilities (and opening new ones in lower cost countries), and efforts to streamline supply and logistics chains, Kraft Heinz managed to achieve $1.7 billion in cost savings by the end of 2017. Management believes more cost savings can be obtained, and analysts estimate that within two years another $300 million in cost savings are realistic.

Kraft Heinz’s focus on economies of scale and cost savings is why the company’s operating margin hit 27.1% in the fourth quarter of 2017, which is far above the industry average below 10%. However, cost savings can only grow a company’s earnings and cash flow so far which is why management is focused on a multipronged approach to achieve strong top and bottom line growth in the years ahead.

The first part of the plan is to expand Kraft Heinz’s existing brands in existing sales channels. Since the food service market is a $665 billion global business, Kraft Heinz believes it can achieve significant long-term growth, both domestically and worldwide, by increasing the presence of its well-known brands. The main targets are Heinz condiments, Kraft snack foods, and Planters peanuts to sales of bars, hotels, restaurants, and institutions.

The second part of the growth plan includes expanding its brands into related categories. For example, Heinz was best known for ketchup and mustard, but in recent years the brand has found big success in launching mayo and barbecue sauces.

The company’s extensions in these categories have been especially big hits in Europe, Australia, and Latin America. Overall, Heinz sales have grown 5% annually since 2015, or 17% in total over the past two years. And in its “rest of the world” segment, which includes fast-growing emerging markets, organic sales rose 7% in the fourth quarter of 2017.

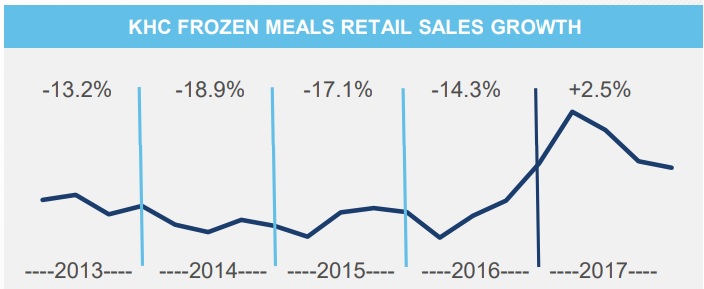

Importantly, Kraft Heinz is very focused on adapting its portfolio to changing consumer tastes, including preferences for healthier foods, organic products, and less processed selections. For example, Kraft eliminated artificial preservatives, coloring, and flavoring from its famous macaroni and cheese. Kraft has also launched new brands in frozen foods, including the successful Devour (frozen snacks) and SmartMade (frozen meals) offerings.

In addition, Kraft Heinz is constantly experimenting with new brands, including highly portable and convenient adult snacks to support an on-the-go lifestyle. These offerings include its new portable protein packs which have helped make Kraft the number one player in the adult meal combo space.

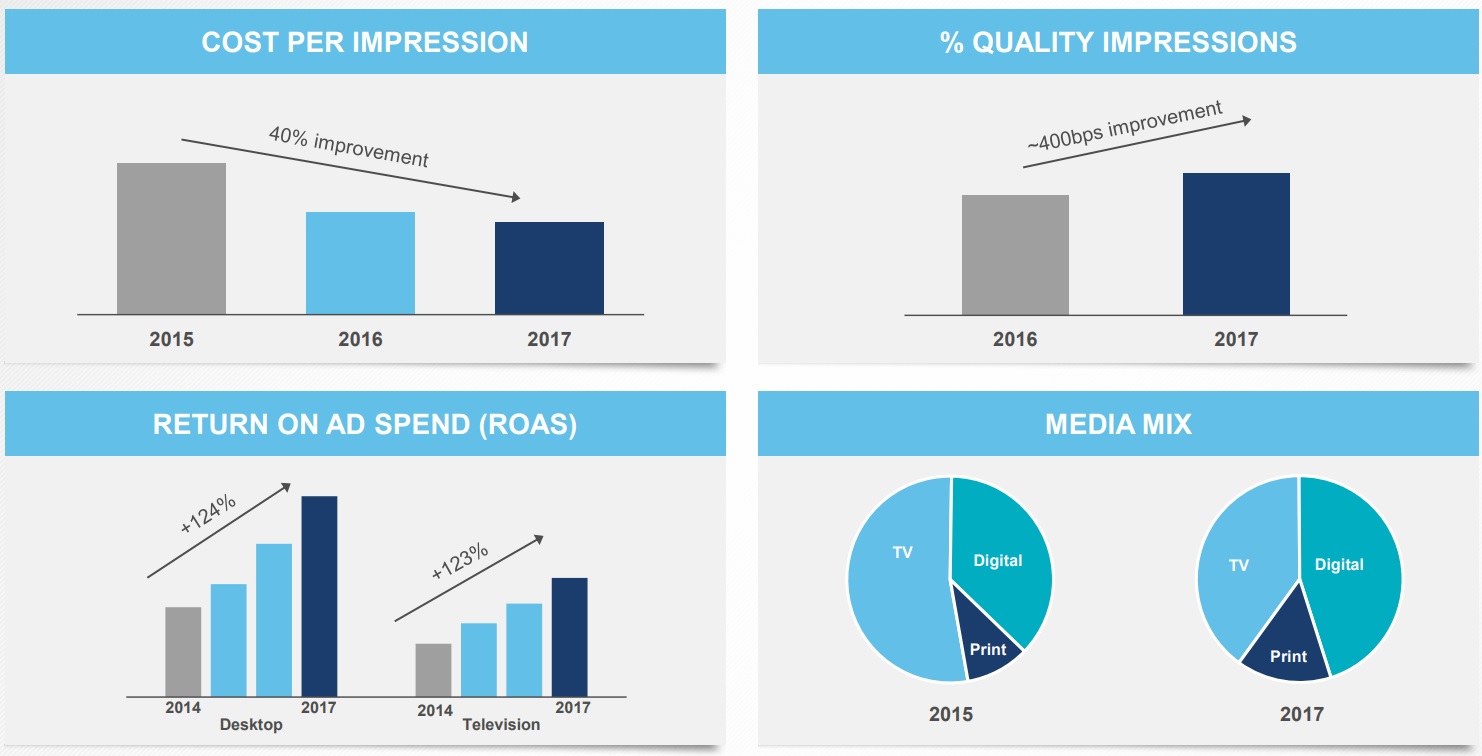

Meanwhile, to keep up its brand equity and pricing power, Kraft Heinz has been investing heavily into digital data analysis, particularly in regards to its marketing efforts. The goal is to spend marketing dollars most cost effectively and with the greatest positive effect on sales.

Kraft Heinz is trying to ensure that it adapts to changing consumer tastes, not just in what people consume, but also how they interact with media. For example, Kraft Heinz has now reached over 1 billion unique people on social media, and its website offers 50,000 professional recipes and more than 700 instructional videos for how to cook with its products.

Going forward, the company hopes that this kind of data-driven, more targeted advertising will help to cement brand loyalty with Millennials, who are now starting families and will only represent a growing share of overall food spending.

The company’s ultimate goal is to pivot its famous brands (and launch new ones) that are “on trend” with global consumers’ greater emphasis on healthier, less processed, but super convenient packaged foods.

Kraft Heinz then wants to plug these into Heinz’s well developed international supply chain and become the number one or number two snack/packaged food brand in 80% of the markets in which it operates by 2023.

For context, Kraft Heinz had the number one or number two market share position in just 10% of its operating countries in 2016, the company clearly has its work cut out for it.

Over the long term, it’s hard to imagine Kraft Heinz’s revenue growing at more than a low single-digit pace, driven by moderate global population growth, inflationary price increases, and efforts to expand its brand portfolio across channels, food categories, and geographic regions.

However, when combined with ongoing cost savings and share repurchases, Kraft Heinz’s earnings per share and free cash flow (as well as its dividend) have potential to grow at a faster rate. Perhaps at a mid to upper single-digit clip annually.

However, the company has encountered several challenges that could continue jeopardizing its rosy growth ambitions.

Key Risks

Kraft Heinz faces numerous threats to management’s efforts to profitable expand the business.

First and foremost is the fact that the vast majority of its sales are derived from mature markets, where sluggish population growth means that the size of the food market in these regions doesn’t change by much each year. Instead, the dollars spent by consumers largely shift between rivals and ultimately gravitate towards the companies offering the most in-demand products.

Unfortunately, Kraft Heinz has been on the losing end in recent years. In fact, nearly 80% of the company’s sales are from North America, where its organic growth has been falling for two years now.

U.S. organic sales declined 1.5% in 2017, for example, resulting in Kraft Heinz’s overall organic revenue for the year to slip 1%. In 2016, U.S. organic sales declined by 0.3%.

This disappointing growth can largely be attributed to two factors. First, 3G Capital’s strong cost-cutting efforts have likely come at the expense of investing enough in Kraft Heinz’s brands, specifically through advertising.

For example, in 2017 the company spent $629 million on advertising, or 2.4% of revenue. Most of its peers invest between 5% and 10% of their sales in marketing because maintaining branding power is essential in this highly competitive space.

That’s especially true when consumer tastes are increasingly shifting away from Kraft’s core products such as frozen meals, packaged meats, and shelf-stable foods. These product categories account for more than 20% of the company’s sales and are more susceptible to low-cost private label competition and share loss to new brands in healthier segments of the grocery store.

Increasing competition from store brand (i.e. generic) products are a legitimate threat to market share. This includes store-branded products from Kraft’s largest customers, including Walmart.

Store brands actually make more money for a retailer than branded products which means that Kraft faces severe pricing challenges when negotiating with its largest buyers. That might explain why Kraft was only able to achieve minor price increases that didn’t keep up with inflation in 2016 and 2017.

Combine intense private label competition with a secular shift away from packaged foods and towards healthier alternatives, and the result is that Kraft has started to see its competitive advantage in retail placement decrease.

For example, in Canada retailers are now reducing its prime shelf space and U.S. retailers may soon start to do the same. That can create a downward spiral in which decreased organic sales leads to an even less competitive position (less cash flow to invest in advertising and product innovation), which leads to further falling sales.

New products and brands, such as Devour frozen snacks and SmartMade frozen meals, appear to have stemmed the tide of plunging sales in the frozen foods unit, at least for now. But only time will tell whether such brands can actually sustain positive and profitable top line growth over time.

In addition, while Kraft recently launched its own brand incubator, Springboard, to help develop new healthier items, there is little reason to think that this will give the company a competitive advantage over rivals. That’s because many packaged goods companies also have similar in-house product development teams, most which were launched before Kraft’s effort.

In other words, Kraft Heinz is facing growing pressure to prove that it can turnaround its organic sales growth in its most important markets. Healthier food options and a larger presence in digital media are not unique advantages for Kraft. Those are merely table stakes in this highly competitive industry in which all its rivals are pursuing similar growth strategies.

If the company can’t stabilize its organic growth, than it’s possible that the brand equity Kraft Heinz has enjoyed for over a century has eroded. Potentially to the point that the business might not be able to drive sufficient earnings and cash flow growth to make it a good long-term dividend growth stock.

But top line sales are just one of several challenges facing Kraft Heinz. Another is that the company has only so much control over its short-term costs. For example, rising commodity and transportation costs in 2017 partially offset the impressive cost savings that management was able to achieve.

And even if Kraft can deliver success in emerging markets, foreign currency risk means that if the dollar appreciates relative to local currencies, reported sales and earnings growth from international markets will decrease. However, neither of these factors should affect Kraft Heinz’s long-term earnings power.

But Kraft Heinz does have a large amount of debt, about $32 billion worth. That gives the company a debt/EBITDA ratio of 4.0, compared to the industry average near 2.5. Management wants to reduce its leverage ratio to 3.0 in the long term.

Until then, Kraft Heinz will need to maintain its BBB credit rating, which is on the low side of its peers and suggests the company could have less financial flexibility when it comes to either investing in future growth or raising its dividend.

However, Kraft Heinz’s management has shown that it’s still eager for a big acquisition to buy its way back to growth. For example, the company attempted to buy Unilever (UL) for $143 billion in 2017. While that bid was rebuffeded by Unilever, such large-scale acquisitions are notoriously difficult to pull off well.

For one thing, they often result in the acquirer overpaying, which means that it can take many years for such a deal to actually increase earnings and free cash flow per share. Additionally, many of the cost synergies that such deals rely on to create value for shareholders can fail to materialize.

A large acquisition would also increase Kraft Heinz’s debt burden even more, potentially putting it at risk of a credit downgrade. The company does have Warren Buffett and 3G Capital backing it, but higher debt, especially during a time of rising interest rates, would have only hinder Kraft’s financial flexibility even more.

While Kraft Heinz has a large portfolio of well-known brands, some cost advantages, and good growth potential in overseas markets (especially emerging economies), those strengths have not been enough to lift the company to profitable growth in recent years.

For now, Kraft Heinz is left with stagnating top line sales growth, driven by falling pricing power in mature markets. Changing consumer tastes (and potentially excessive cost cutting) are driving the bulk of this pressure, and management has thus far had a hard time shifting the company’s massive product portfolio to be better aligned with consumers’ changing tastes.

Closing Thoughts on Kraft Heinz

Many of Warren Buffett’s holdings are characterized by strong brands, essential products, and dominant market share positions, so it’s no surprise why he was excited to own Heinz and Kraft.

While Kraft Heinz is likely to remain a dominant force in the food and beverage industry for many years to come, it’s also facing numerous growth headwinds that it has thus far been incapable of dealing with. Management’s stated plan for returning to stronger top line growth appears reasonable, and in the meantime investors are paid handsomely to wait.

That being said, given the major secular shifts in consumer eating habits in recent years, it may be a good idea to wait and see whether or not Kraft Heinz’s turnaround plan actually succeeds before investing in the company for the long term.

To learn more about Kraft Heinz’s dividend safety and growth profile, please click here.

Leave A Comment