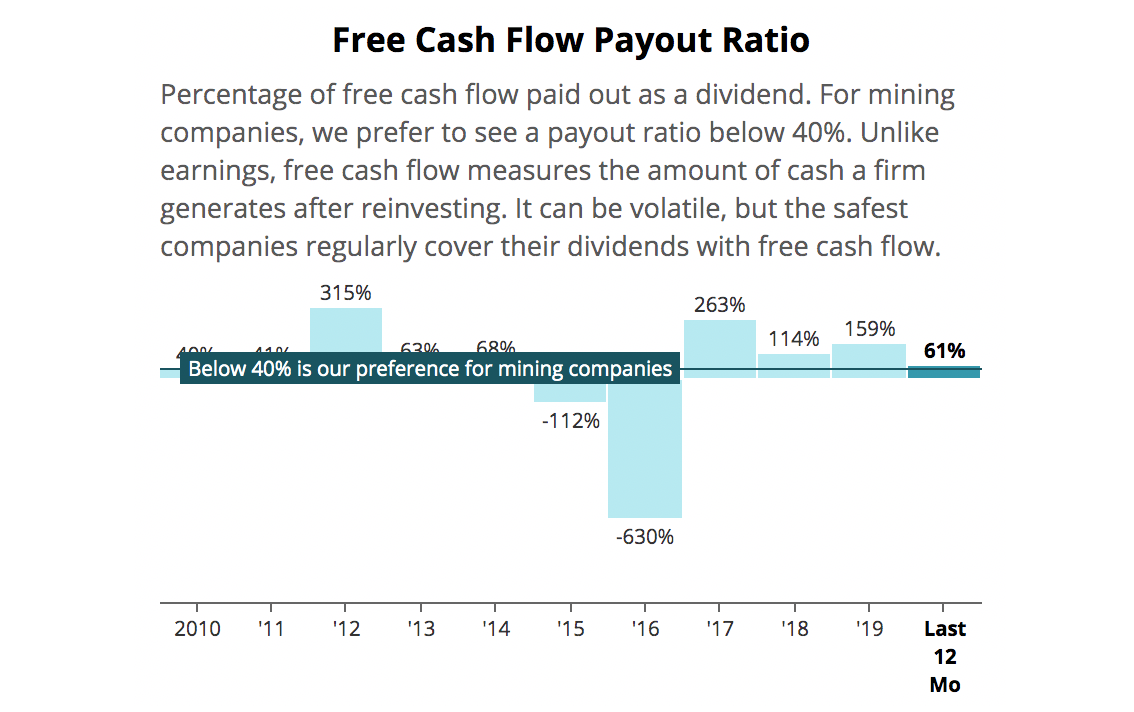

Compass Minerals' Free Cash Flow Returns to Covering Dividend for First Time Since 2014

Compass Minerals has had a speculative Dividend Safety Score since 2017, reflecting the firm's poor dividend coverage, elevated leverage, and various operational missteps.

Management has kept the dividend frozen since early 2017. During this period, shares of Compass Minerals have lost 5%, including dividends, while the S&P 500 has gained more than 70%.

But under a new CEO since May 2019, Compass Minerals has made progress on several fronts.

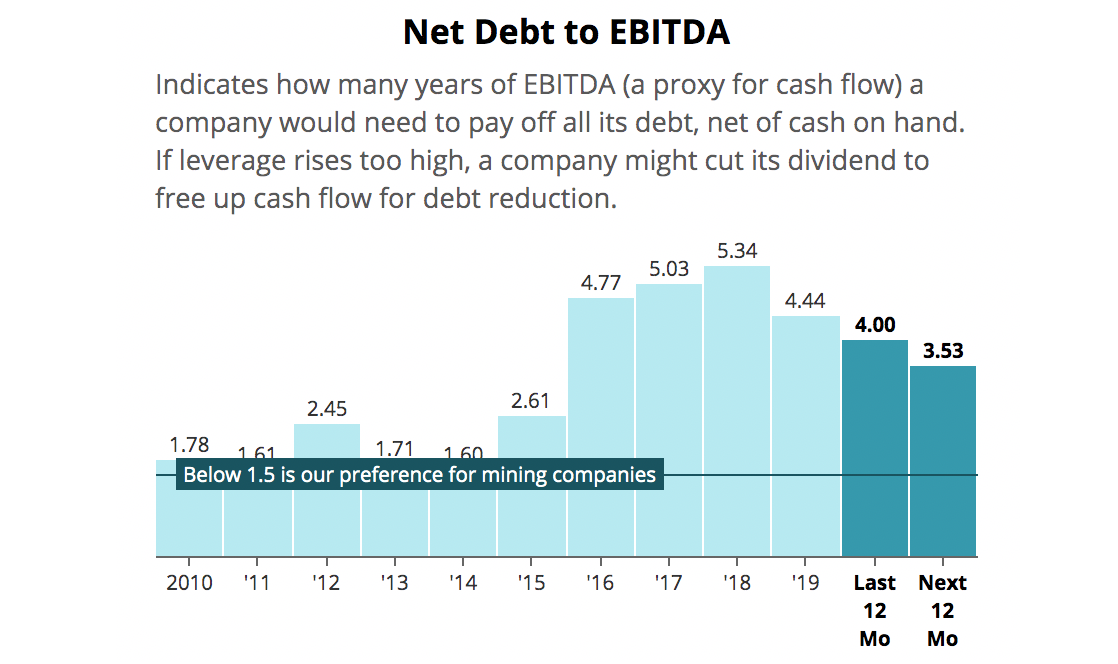

With free cash flow now covering the dividend for the first time since 2014 and leverage falling to its lowest level since 2015, we are upgrading Compass Minerals' Dividend Safety Score to Borderline Safe.

Compass Minerals boasts an operating history dating back to 1844 and is a leading producer of salt (used for deicing highways and in various consumer and industrial applications) and specialty fertilizer (improves the quality and yield of crops).

Compass Minerals has paid reliable dividends since going public in 2003. This track record was built around the company's ownership of the largest and lowest cost salt mine in the world, as well as an extensive logistics network that gave it transportation advantages in its core Midwest region.

Road salt is also an essential business, and demand is generally insulated from economic cycles. But salt, which accounts for the majority of firm-wide revenue, is also a slow-growing business and experiences demand volatility depending on winter weather.

In 2013, Fran Malecha joined Compass Minerals as its CEO. Mr. Malecha came from the agriculture business and launched the firm on an ambitious growth plan composed of two strategies.

The first was diversifying away from salt and into plant nutrition in order to reduce the firm's dependence on cold winter weather and improve long-term growth opportunities.

This was achieved through a roughly $600 million acquisition of Produquímica, a Brazilian specialty plant nutrition and chemical company, in 2016. The company also bought Wolf Trax, a micronutrients supplier, for $85 million in 2014.

These deals reduced Compass Minerals' salt business mix to around 60% of sales, down from 80% in 2015.

Mr. Malecha's other major growth initiative was a four-year, $500 million investment program. This included expanding its potash business (fertilizer), which benefited some of the lowest production costs in the industry.

The plan also included spending $225 million to improve its mining capacity (which was expected to lower operating costs 25%) with a specific focus on its biggest salt mine.

For context, Compass Minerals' market cap sits around $2 billion today. These were transformative investments for the company.

As luck would have it, Compass Minerals encountered numerous challenges in the years that followed.

The firm's largest salt mine, which generates over 60% of its production, experienced a ceiling collapse in late 2017. Coupled with a labor strike, Compass Minerals dealt with production issues for about a year.

Meanwhile, mild winter weather, falling crop prices, and foreign currency exchange rate volatility further weighed on earnings and hurt the firm's agriculture business.

Coupled with new debt Compass Minerals took on to fund Malecha's growth plans, the company's leverage ratio more than tripled compared to 2014 and earned it a junk credit rating.

Source: Simply Safe Dividends

As pressure mounted on the business, Mr. Malecha abruptly stepped down in November 2018 and was replaced in May 2019 by Kevin Crutchfield, who has over 30 years of mining experience (though mostly in the coal industry).

Mr. Crutchfield has refocused Compass Minerals on strengthening the reliability of its operations and enhancing the productivity of its existing assets.

With capital investments now easing and management focused on taking costs out of the business, Compass Minerals' leverage is slowly returning to healthier levels.

Free cash flow this year has also returned to covering the dividend for the first time since 2014. Management expects to generate $125 million of free cash flow in 2020, compared to total dividends of about $100 million (an 80% payout ratio).

Source: Simply Safe Dividends

Compass Minerals still has a long ways to go to restore credibility with investors after the ill-timed, debt-funded investment plans of its former CEO.

But improving trends in leverage and cash flow are a good start to restoring the firm's image as a good operator and allocator of capital.

Keeping the dividend intact is perhaps an especially important priority given this backdrop.

Management has said surprisingly little about the dividend, mentioning it just once on a conference call since June 2019. However, Compass Minerals expects dividend coverage to remain healthy going forward as it continues deleveraging.

"We're performing well from an operation standpoint. We're going to generate more cash. So I think from a dividend coverage standpoint, we feel very comfortable about that...In terms of leverage...I think longer term, we want to get aimed at sort of 2.5 turns through kind of average conditions."

– CEO Kevin Crutchfield, 9/15/20 Investor Conference

Management expects leverage to sit at 3.8x at the end of this year, well above their 2.5x target.

Until the balance sheet has strengthened more, we expect Compass Minerals to hold its dividend flat, and another Dividend Safety Score upgrade is unlikely.

Overall, Compass Minerals' willingness to stick with the dividend this far is a good sign that management intends to remain committed to the payout going forward.

While the company's businesses are relatively simple to understand and appear durable thanks to their unique assets and essential nature, Compass Minerals seems likely to remain a volatile stock.

Besides its elevated debt load, Compass Minerals' plant nutrition and salt businesses remain at the mercy of uncontrollable weather patterns and global agricultural markets any given year.

The dividend's outlook has improved, but investors still need to be comfortable with these risks as Compass Minerals continues its turnaround effort.