The outlook for retail REITs continues to dim as the coronavirus pandemic drags on and fewer businesses are able to pay rent.

Nareit, a producer of REIT research, recently conducted a survey of 54 publicly-listed REITs and found that shopping center REITs have only collected 46% of their rent this month as of mid-April.

Rent collection rates will vary significantly between retail REITs depending on their mix of tenants and property locations, but Kimco's (KIM) exposure is concerning.

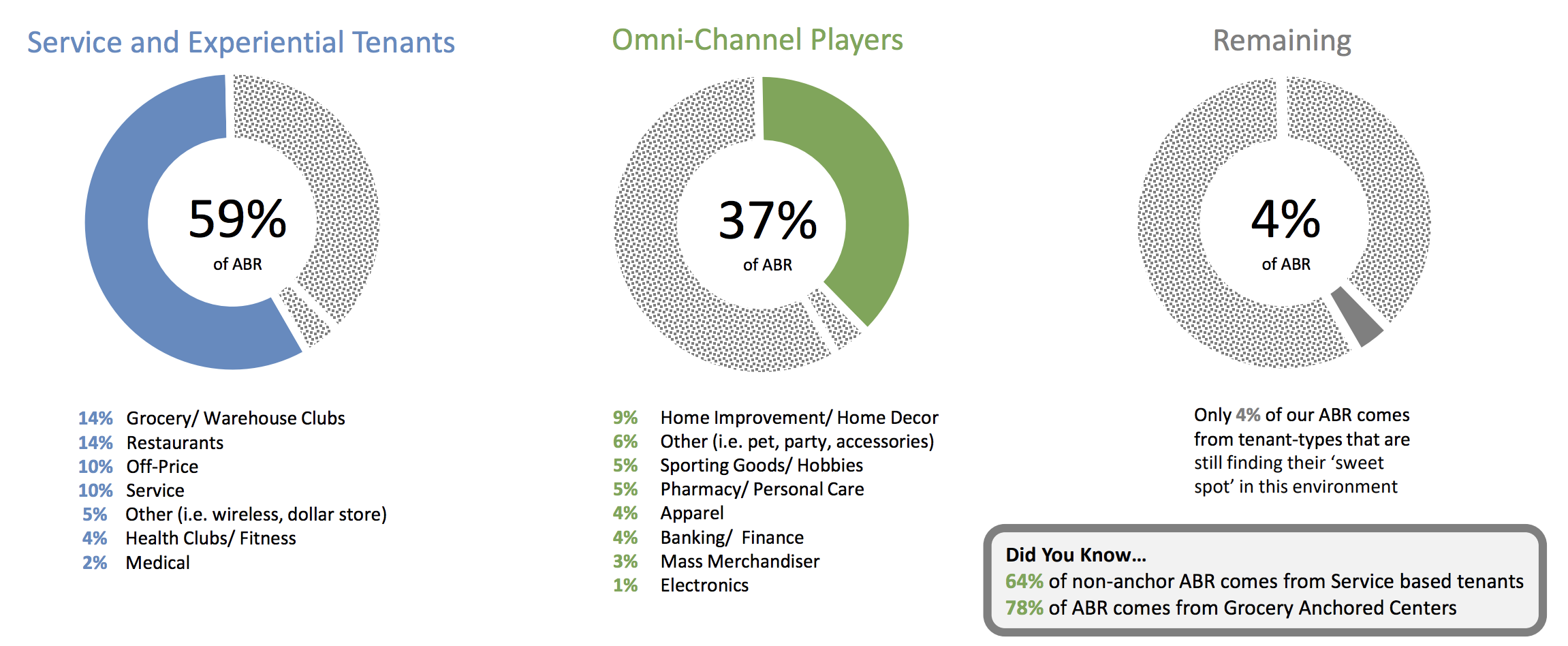

Kimco generates approximately 78% of its annual base rent from grocery-anchored shopping centers and has historically focused on service-based tenants, which face less pressure from e-commerce.

Unfortunately, this has also increased Kimco's exposure to "non-essential" businesses, many of which are temporarily closed and likely to struggle paying their rent for the foreseeable future.

Restaurants (14% of rent), off-price retailers (10%), pet / party / accessories (6%), sporting goods (5%), gyms (4%), and apparel (4%) are some of the stressed categories in Kimco's portfolio.

Source: Kimco Investor Presentation

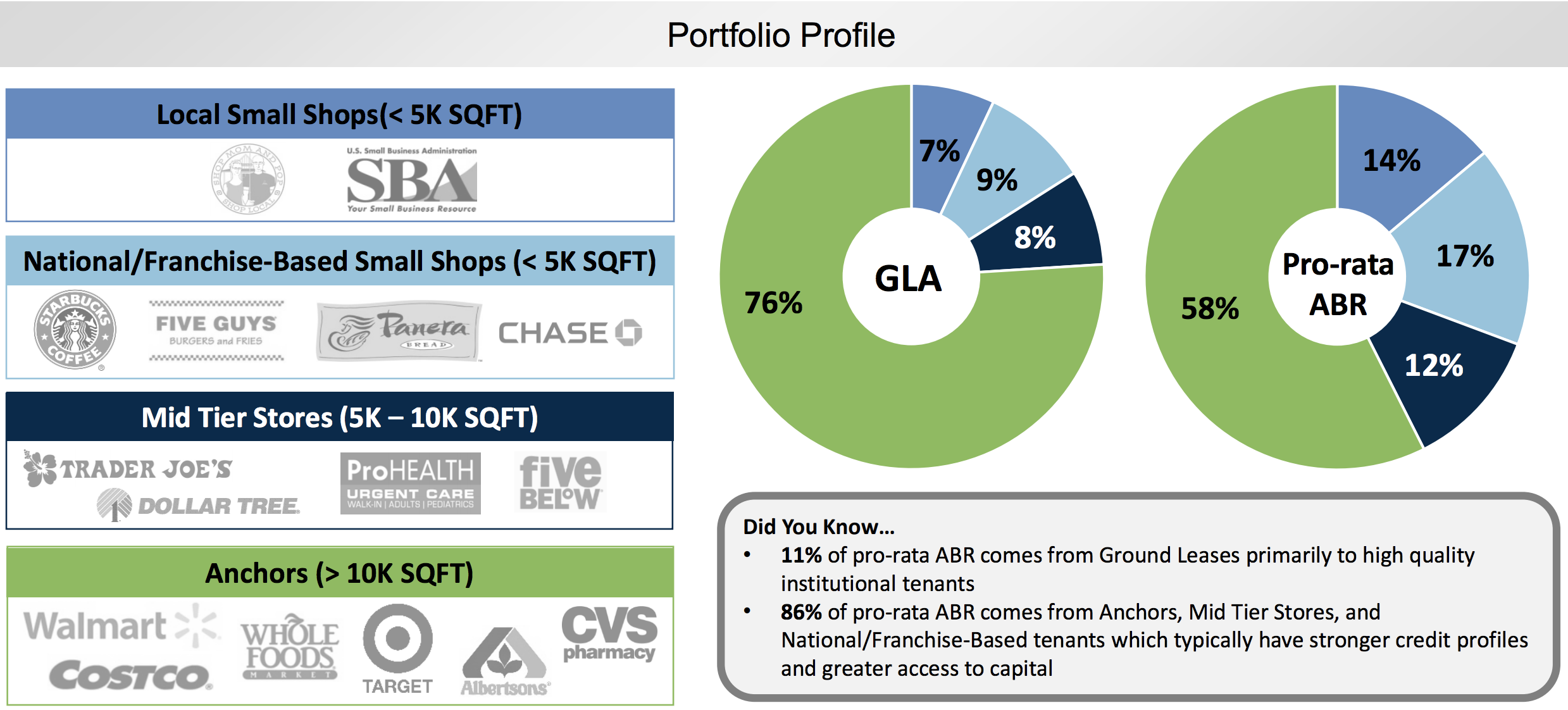

Local businesses are especially challenged in today's environment given their smaller scale and fewer financial resources compared to their national counterparts. Local small shops account for 14% of Kimco's rent.

Source: Kimco Investor Presentation

Some of Kimco's larger tenants were under financial pressure prior to the pandemic as well, including Petsmart (1.8% of rent), Bed Bath & Beyond (1.5%), Petco (1.1%), The Gap (0.9%), and Pier 1 (0.5%).

And while Kimco is diversified geographically, New York, the state hit hardest by the virus, is the REIT's largest market, accounting for about 13% of rent.

Overall, there's substantial uncertainty as to how much rent Kimco will end up collecting going forward. Businesses previously on the brink of failure may simply throw in the towel instead of seeking relief.

Furthermore, nobody knows yet just how deep and long lasting the impacts of the pandemic will be on retailers, restaurants, and more. Kimco ultimately relies on a thriving retail scene for its own business model to succeed.

Prior to COVID-19, Kimco's payout ratio sat above 95% but was expected to improve in 2020 and 2021 as the REIT's (re)development projects began increasing cash flow.

Now, with a number of tenants unlikely to pay rent for an unknown period of time, Kimco's $470 million dividend will no longer be covered by cash flow in the short term (and potentially much longer).

The REIT's liquidity position is solid, with $800 million of cash on hand and $1.3 billion available under its revolving credit facility, which expires in March 2022.

That's plenty to cover the company's $172 million in debt obligations maturing this year and management's modest plans to acquire $100 million to $200 million of assets, which seem likely to be suspended anyway. (Kimco also planned to divest $200 million to $300 million of assets.)

However, just because Kimco could use its financial flexibility (including a BBB+ credit rating from Standard & Poor's) to pay its dividend doesn't mean that it will.

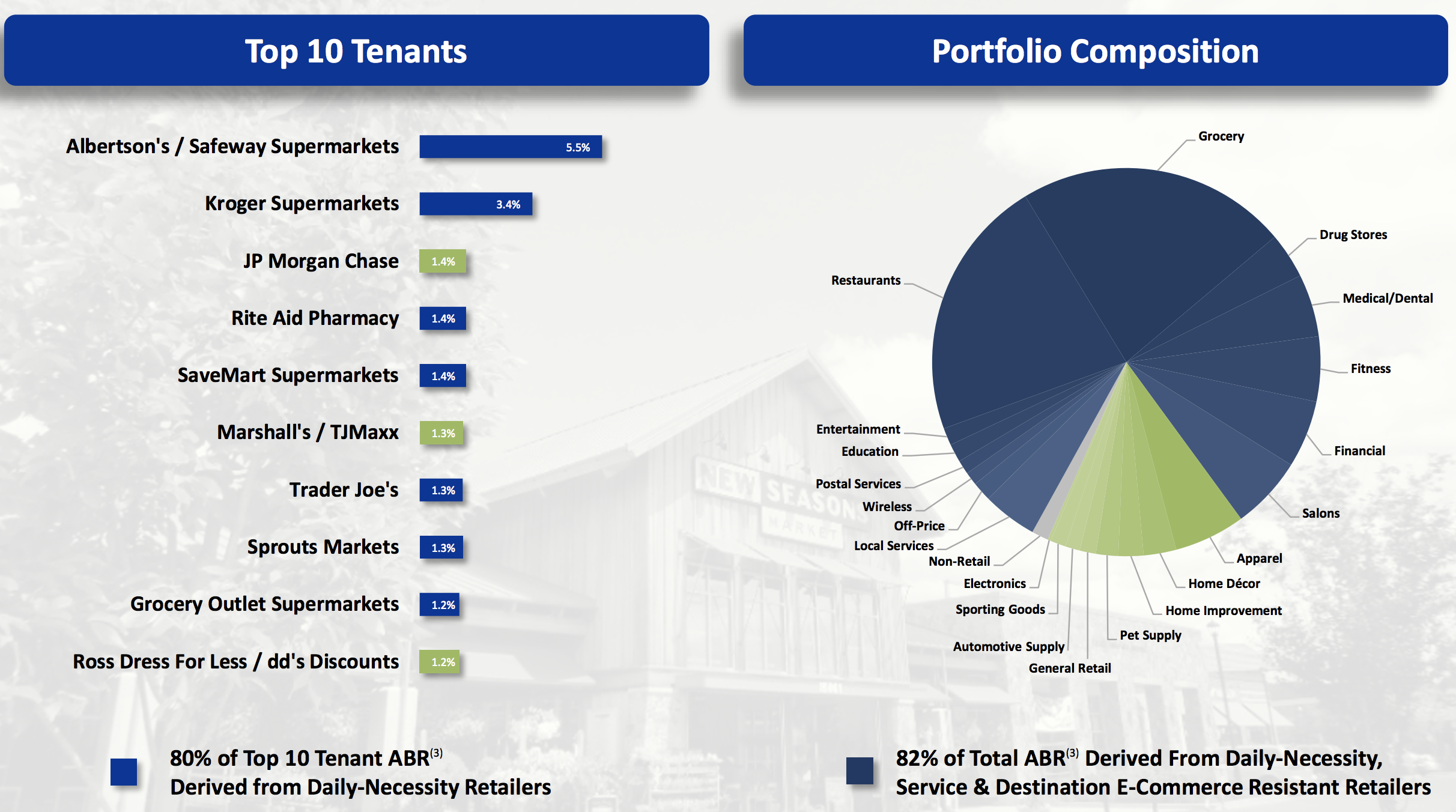

For example, earlier today peer Retail Opportunity Investments (ROIC), which generates 98% of its rent from grocery- or pharmacy-anchored shopping centers, suspended its dividend despite:

Having no material debt maturing for the next four years

Noting that 79% of its tenants are designated "essential businesses"

Maintaining a BBB- investment grade credit rating

Holding over $130 million of cash with another $367 million available under its credit facility (ROIC's dividend costs $100 million)

Collecting 67.5% of April rent

Achieving a 97.7% occupancy rate at the end of March

ROIC is smaller with only 88 shopping centers compared to more than 400 for Kimco, but there are enough similarities between their businesses (see ROIC's customer mix below) to be concerned about Kimco's dividend given the unprecedented challenges facing the industry.

Source: ROIC Investor Presentation

All said, we are downgrading Kimco's Dividend Safety Score from Borderline Safe to Unsafe in recognition of the increased likelihood of a dividend cut.

The REIT's cash flow seems unlikely to cover the dividend for the foreseeable future as many of its tenants remain under stress.

Right-sizing the payout to better reflect this new reality and preserve capital in today's uncertain environment would seem prudent.

A lot of bad news is already reflected in Kimco's stock price, but current shareholders should weigh whether they are comfortable holding a stock that has increasingly questionable dividend prospects and could struggle to return to growth anytime soon.