Magellan Provides Business Update, Expects to Maintain Distribution

On March 20, we published a note on Magellan Midstream Partners (MMP) and maintained our Safe rating after concluding that the firm appeared "to have the balance sheet, distribution coverage, and commitment to its payout to wait out better times."

Less than a week later on March 26, Magellan said it was indeed maintaining its distribution guidance for the year, which even calls for a 3% increase.

Like most midstream businesses, Magellan is feeling the effects of the coronavirus and the crash in oil prices. Please see our March note for more background on these issues and how they impact the firm.

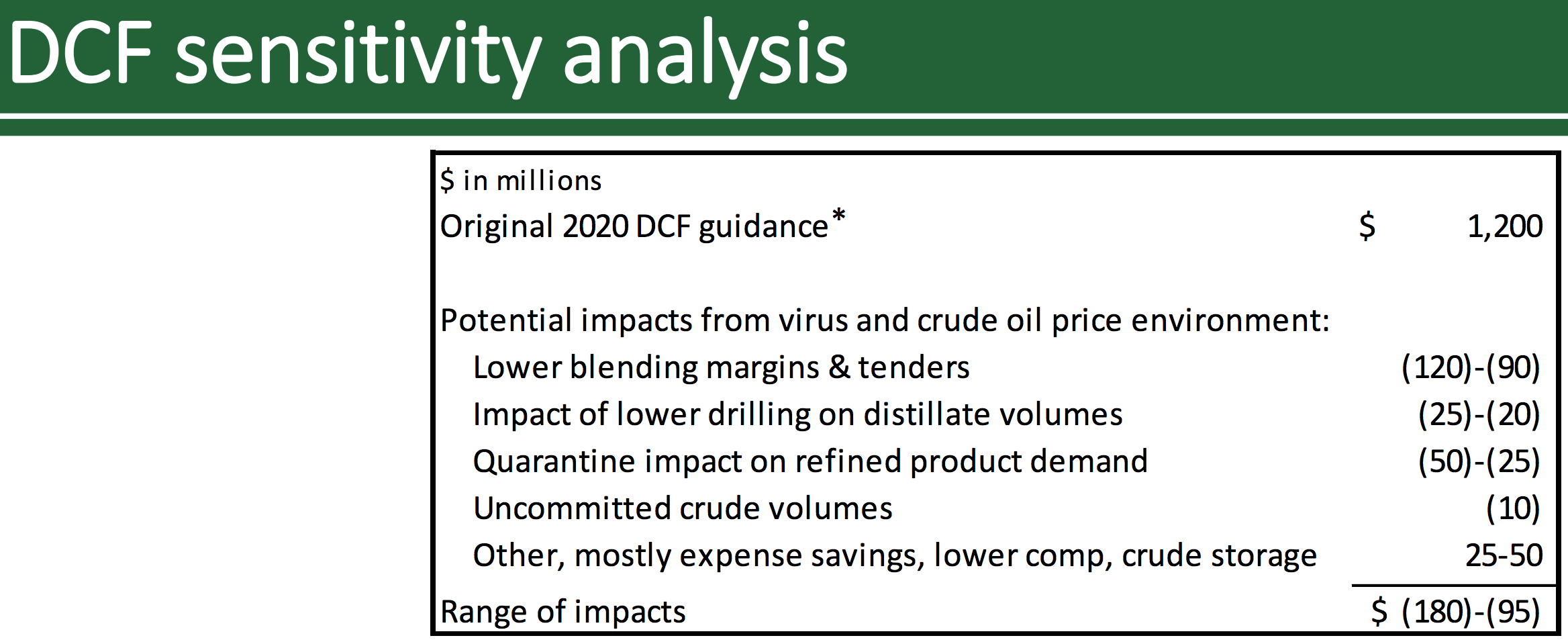

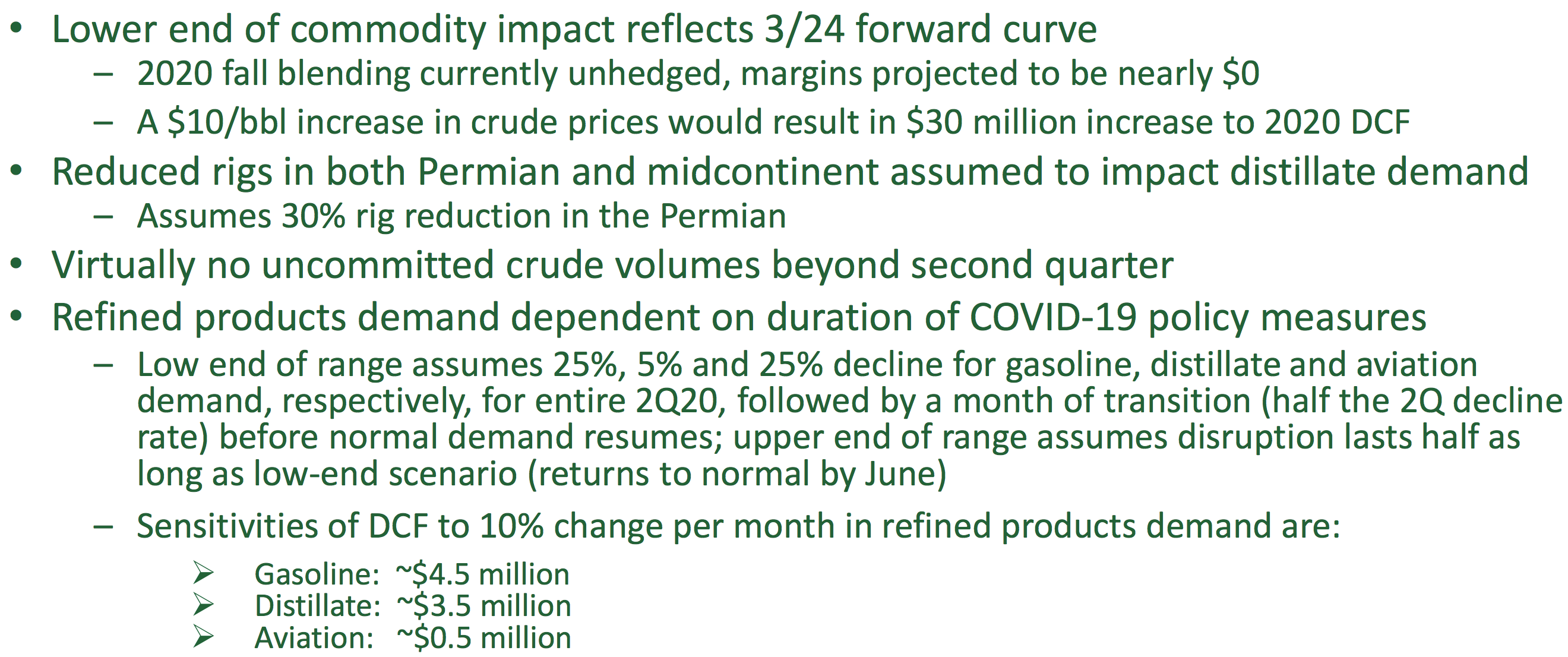

Magellan's business update provided a more detailed look at how its distributable cash flow (DCF) could change based on various assumptions about commodity prices, fuel demand, and drilling activity.

Overall, management believes these factors could reduce DCF this year by 8% to 15% compared to guidance issued by Magellan in January.

Importantly, the low end of Magellan's guidance still reflects a distribution coverage ratio of about 1.1x (down from initial guidance calling for 1.25x).

Source: Magellan Investor Presentation

Here's a look at the assumptions Magellan made in its sensitivity analysis:

Source: Magellan Investor Presentation

The biggest potential hit to DCF comes from the firm's blending business (around 5% of cash flow), which earns a margin based on the price of gasoline versus the price of butane. The plunge in fuel prices has led management to assume that this business makes no margin in 2020.

Even if this commodity price environment persists through 2021, Magellan doesn't view its weak blending business as a threat to its distribution.

The harder factor to forecast is refined products demand, which drives about two-thirds of Magellan's revenue.

Based on conversations with customers and recent demand trends, management expects gasoline demand to fall by 25% in the second quarter of 2020 (through June) before gradually returning to normal demand levels in August.

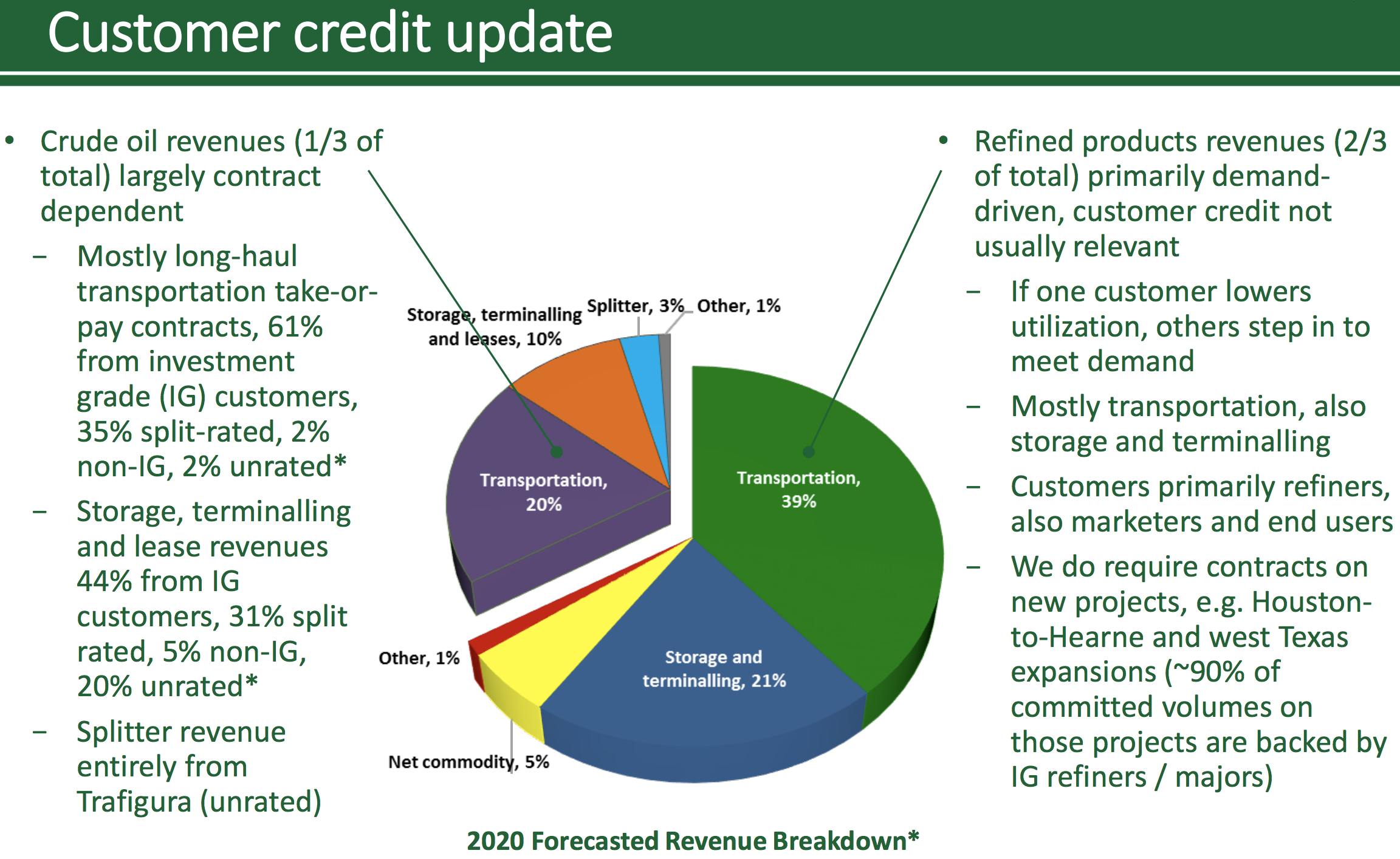

It's also worth noting that Magellan assumes most of its customers will remain healthy and creditworthy.

As we discussed in March, counterparty risk is mostly an issue in the firm's crude oil business (one-third of sales) since the refined products side is driven primarily by demand rather than contracts.

In crude oil, close to 60% of revenue is from investment grade customers, and management said they still expect their customers to be able to pay.

Source: Magellan Investor Presentation

Overall, we think Magellan's assumptions seem reasonable, and the firm's management team is known for taking a conservative stance. Magellan's liquidity and balance sheet provide an extra layer of cushion as well.

Looking at the firm's projected sources and uses of cash in 2020, you can see that Magellan does not need to issue any equity, and its plan requires less than $150 million of incremental debt. Sales proceeds are largely locked in already after Magellan closed its $250 million marine terminals sale on March 20, too.

Source: Magellan Investor Presentation

After completing its $400 million of growth spending this year, no expansion projects are committed in 2021 and beyond, providing even more financial flexibility if needed.

And aside from a $550 million debt maturity in 2021, no long-term debt is due until 2025. The firm also has $1 billion of available borrowing capacity under its credit revolver, which doesn't mature until 2024.

Magellan's dip in cash flow is expected to increase its leverage ratio to between 3.4x and 3.7x, but it remains comfortably below management's long-standing target maximum of 4x. Simply put, the firm's balance sheet and liquidity remain solid and do not threaten the distribution.

Management also said that the relatively poor performance of MLPs in recent weeks has not influenced the firm's internal discussions about potentially converting to a corporation.

We would be surprised if management took any actions that would trigger a taxable event for unitholders or pressure the payout. Enterprise Products Partners (EPD) is mulling over the same issue, which we discussed here.

Overall, Magellan's update provides income investors with some relief for now. Unless lockdowns and travel restrictions persist well beyond April, or many oil customers unexpectedly default on their contracts, Magellan's distribution appears secure. We will continue monitoring the situation.