Sysco Pivots to Serve Retail Grocers, Maintains Dividend For Now

The novel coronavirus outbreak has triggered temporary store closures and social distancing restrictions designed to slow the virus' spread.

The end result has been unprecedented disruption for most of Sysco's food distribution customers, including restaurants (62% of sales), hotels (9%), and schools and governments (9%).

Based on the analysis shared below, we are downgrading Sysco's Dividend Safety Score to Borderline Safe and plan to sell the shares of Sysco that we hold in our Conservative Retirees portfolio on Monday, March 23.

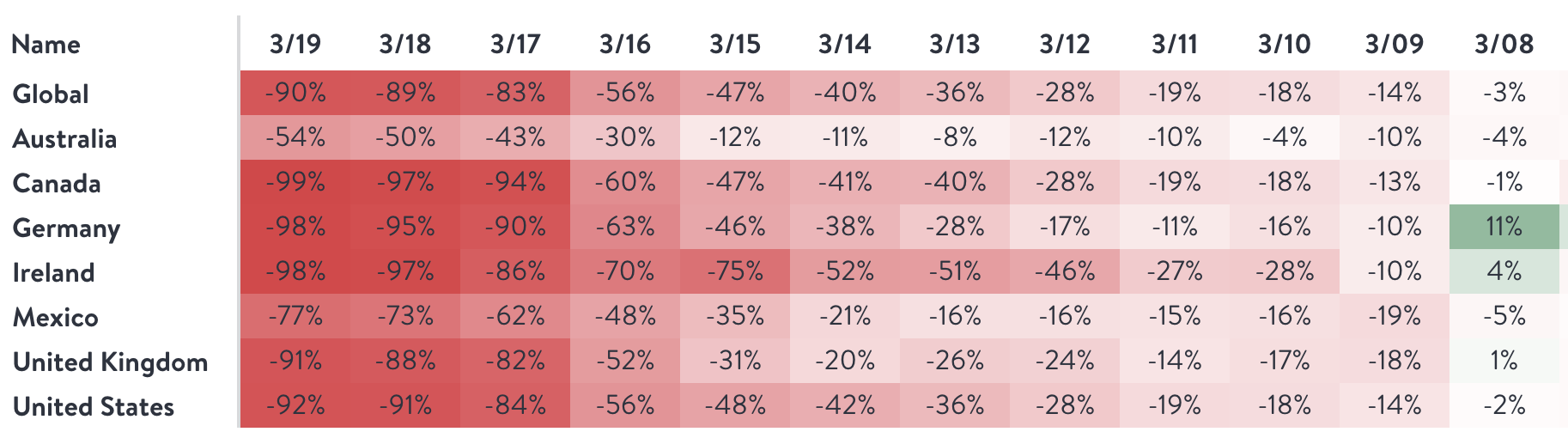

To show how rapidly the operating environment has changed, OpenTable, a widely-used online reservation platform, reported a 92% year-over-year drop in restaurant bookings in the U.S. for Thursday, March 19. As you can see, the trend has significantly accelerated over the last 10 days.

Source: OpenTable

The uncertainty ahead for Sysco's core restaurant customers is staggering:

Will restaurants be closed nationwide, or just in some states and cities?

How long will any closures last? A few weeks? Months?

What will demand for carryout look like, especially for restaurants where to-go is not the norm?

What assistance will governments provide restaurants?

Once restaurants are reopened, will traffic return to normal? Or will people be timid to dine at restaurants due to lingering concerns of infection?

Hotels face many of the same issues. Simply put, there are a lot more questions than answers, as there's no precedent to what's currently taking place in the industry. Moreover, the situation is changing by the day.

In response to this uncertainty, Sysco's stock price plunged nearly 60% between March 10 and March 18.

S&P then downgraded Sysco's credit rating from BBB+ to BBB- (one notch above junk) with expectations that the firm's adjusted EBITDA could decline "by well over 50% over the next few quarters depending on the severity of the sales drop."

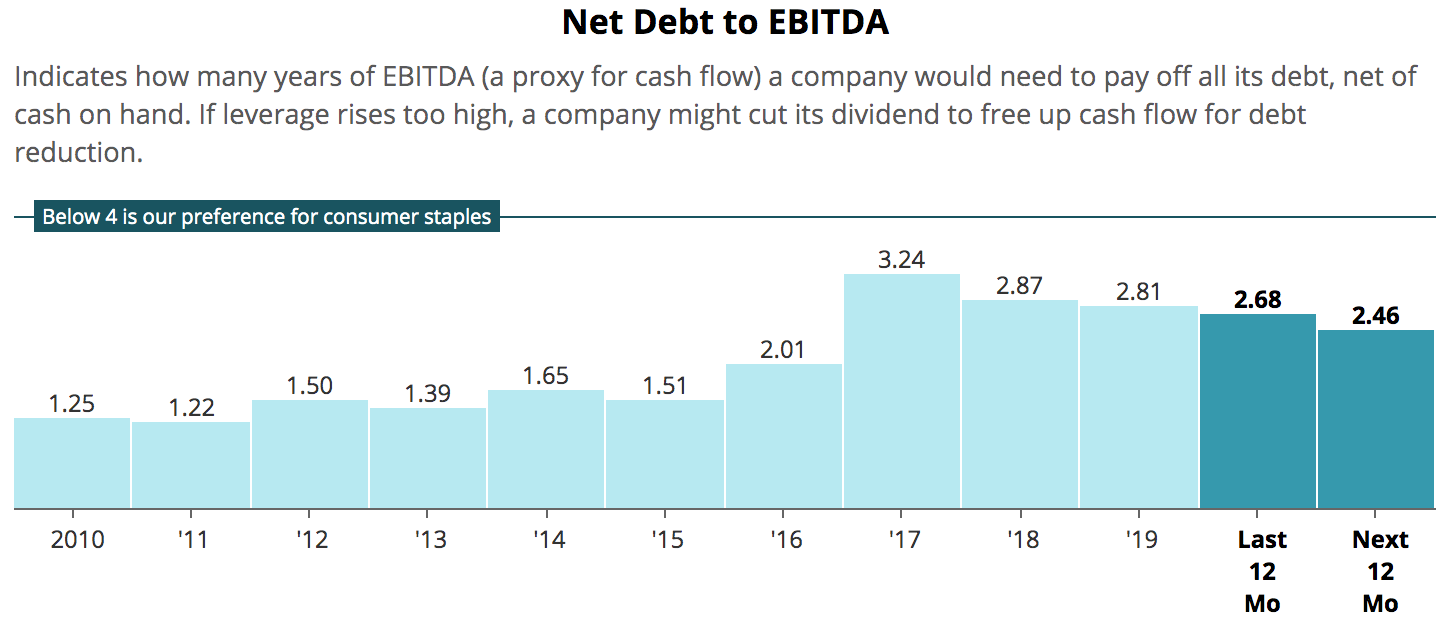

As this plays out, S&P believes Sysco's net debt to EBITDA leverage ratio could spike well above 5x over the next year or so, putting the company's balance sheet into uncharted territory.

Source: Simply Safe Dividends

To avoid losing its investment-grade credit rating, S&P says Sysco needs to demonstrate that it can sustain a leverage ratio near 4x.

Over the last three years, Sysco's annual operating cash flow has averaged $2.3 billion, and its capital expenditures have hovered just under $700 million, resulting in average annual free cash flow of about $1.6 billion.

Cutting Sysco's operating cash flow in half for a year while holding capex steady would reduce free cash flow to around $400 million to $500 million, falling short of the firm's $900 million dividend.

To improve cash flow generation without touching the dividend, management could make extreme cuts to capex or free up working capital by collecting on Sysco's $4.1 billion of receivables from customers (at least from those who can still pay) while buying less inventory.

However, until demand rebounds and provides enough free cash flow for dividends and debt reduction, there's not much the company can do to improve its balance sheet while maintaining its payout.

No one knows how long the virus outbreak will last, but Sysco provided a better-than-feared update this morning. The company said it is managing its costs, capital spending, and working capital to maintain a positive free cash flow position.

Sysco is also pursuing new sources of revenue by leveraging its supply chain and distribution network to serve the retail grocery sector.

Management expects this net new business to help off-set some of the declines in the food-away-from-home segment while providing long-term growth opportunities once the crisis subsides.

“As the largest foodservice distribution company in the industry, we play a significant role in supporting the food supply chain. Due to the significant impact on the food-away-from-home business, we are pivoting our business to better support the surge in demand that is being experienced in the retail grocery store setting. We are establishing new customer relationships with retail grocers to provide them with logistics services and much needed product." – CEO Kevin Hourican

This bold plan actually seems practical. Just yesterday the Wall Street Journal was out with an article about America's struggle to move enough food to meet unprecedented demand from grocery stores. But food supply isn't the issue:

"You wouldn’t know it from the bare grocery store shelves across the country, but America has plenty of food. The challenge is getting it from the farm to your table."

It's hard to say how quickly Sysco can ramp up these efforts and how big this business can become in the short term to offset some of the demand decline at restaurants, hotels, and other shuttered institutions. Anything helps in this environment, but Sysco has a big hole to fill.

Most importantly, management reassured investors that the company believes it has "meaningful financial flexibility" to navigate this environment, including $2 billion of cash on hand (following a recent $1.5 billion draw on its revolver) and no debt maturities for the next six months.

Additionally, the company said it is working with its banking partners to explore opportunities to raise more funds and further strengthen its liquidity.

Suppose Sysco stayed free cash flow neutral during the outbreak, and the outbreak depressed demand for six months. In that scenario the company would burn through around $450 million to maintain two quarters' worth of its dividend, which it has increased steadily for more than 50 consecutive years.

Assuming demand returned to normalized levels by that point, we estimate that Sysco could pay down the incremental debt taken on to cover the dividend in less than eight months. (Sysco was previously on pace to generate around $700 million of annual free cash flow after paying dividends.)

Credit rating agencies may not like it, but that seems to be management's agenda for now. The company is essentially betting that most of its customers will return to business as usual before the end of the year which, combined with some self-help initiatives (cost cuts, grocery retail expansion, etc.), will help Sysco begin reducing its leverage.

Given this sudden, delicate, and fluid situation, which we think will force certain customers out of business and disrupt demand for potentially longer than management expects, we are downgrading Sysco's Dividend Safety Score to Borderline Safe.

Despite the importance of preserving cash in an environment as uncertain as this one, a dividend cut does not seem imminent. If demand recovers within a couple of months and Sysco is generating the cash flow necessary to restore its balance sheet, then the company's Dividend Safety Score could be upgraded.

However, if the operating environment for Sysco's customers does not show material signs of improvement or takes another step back, then the company's score could be downgraded. There's a wide range of uncertainty.

We plan to sell the shares of Sysco we hold in our Conservative Retirees portfolio on Monday, March 23. With many high-yielding stocks selling off, we believe we will have opportunity to own a different stock that generates similar income but has a safer customer base in this extreme environment.

While unlikely, we will send out an email if we make a purchase before our next newsletter publishes on Friday, April 3.