Franklin Retains "Very Safe" Dividend Safety Score Following Plans to Acquire Legg Mason

On Tuesday, Franklin Resources (BEN) announced plans to acquire rival asset manager Legg Mason (LM) for $4.5 billion. Franklin's assets under management will rise from about $700 billion to $1.5 trillion once the deal closes by the third quarter of 2020, underscoring the significance of this transaction.

Fortunately, Franklin's payout ratio, balance sheet, and cash flow generation will remain strong. As a result, we expect Franklin to maintain its Very Safe Dividend Safety Score.

We estimate the combined company will generate about $1.5 billion of free cash flow while paying out around $500 million of dividends annually. This would put Franklin's payout ratio somewhere between 30% and 40%, a very reasonable level that also remains in line with the firm's results in recent years.

Source: Simply Safe Dividends

Franklin will continue to maintain a strong balance sheet as well. Prior to buying Legg Mason, Franklin held more cash than debt and enjoyed an A+ credit rating from Standard & Poor's.

The firm's credit rating was reaffirmed following this news, and although we estimate Franklin will swing to a modest net debt position of about $1 billion (excluding investments the firm has made in its own funds), its financial profile remains solid.

More specifically, the combined company's net debt to EBITDA leverage ratio should sit at a very conservative level below 1x (below 1.5x is our preference for asset managers), and Franklin will likely generate around $1 billion of free cash flow after paying dividends each year, providing ongoing financial flexibility.

Management remains very supportive of the dividend as well. Here's what Franklin CFO Matt Nicholls said on the merger call:

"Our combined cash flow generation and earnings power, together with our strong balance sheet, will support our dividend and provide plenty of capacity to continue growing [it], as we have done annually since 1981."

From a strategic perspective, Franklin and Legg Mason believe they will be stronger together as active asset managers continue facing fee pressure and client redemptions due to the growing popularity of passive funds.

By combining with Legg Mason, Franklin creates a more balanced and diversified business with a greater focus on fixed income and alternatives, areas that have thus far been less susceptible to passive investing compared to stock funds.

This combination also reduces Franklin's dependence on the long-term success of any single investment strategy and helps ensure the firm always has something to sell, regardless of how the market is behaving in any given period.

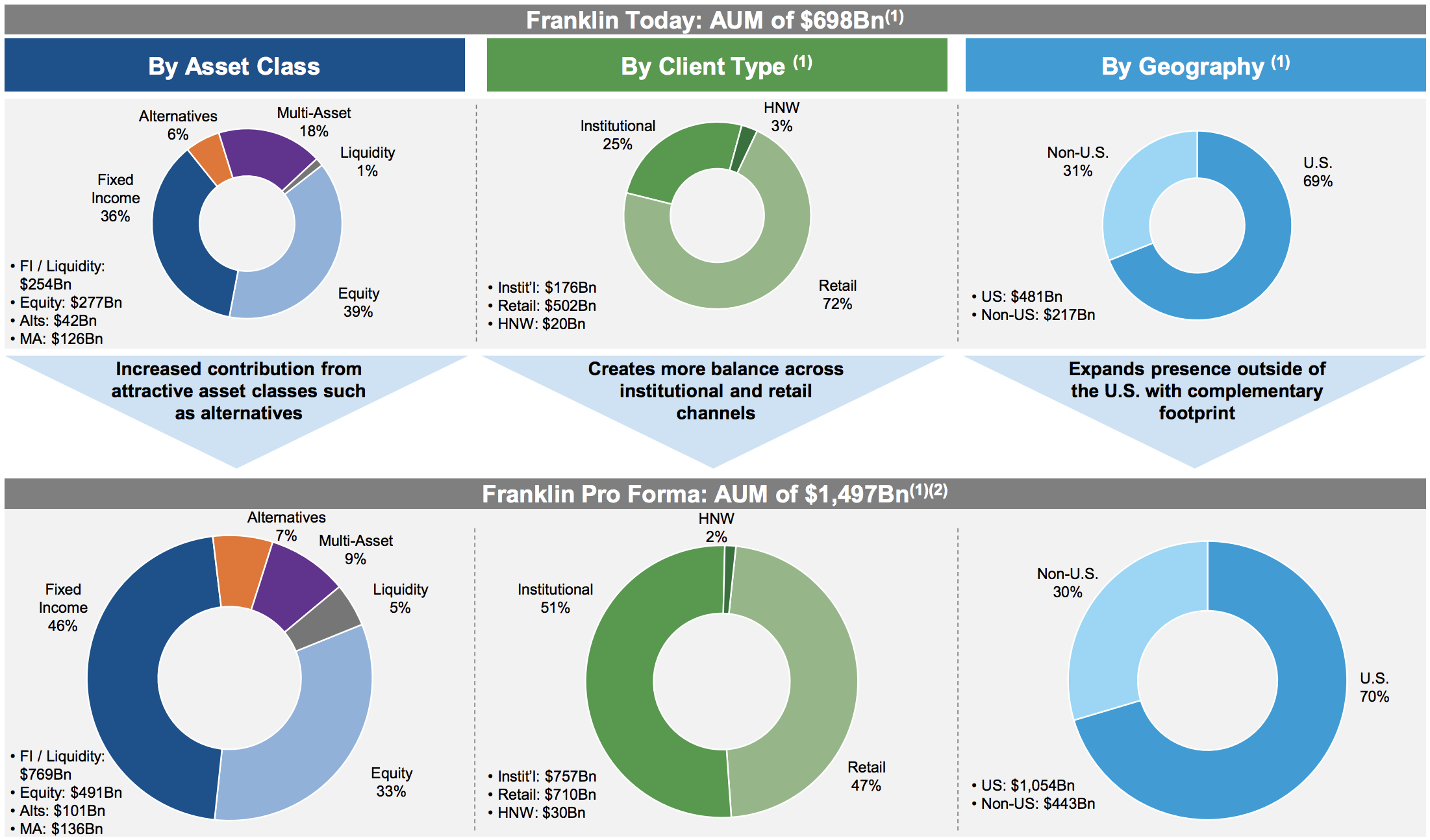

The firm's client base and distribution channels will also become more diversified, with institutional clients, which tend to be stickier clients compared to retail investors, growing from 25% of assets under management to 51%. Franklin's overseas assets will more than double, too.

Source: Franklin Merger Presentation

Management hopes the two firms can leverage their complementary products and distribution channels to drive a return to organic growth. However, both firms, especially Franklin, have experienced net client outflows in recent years.

Despite the market's strong appreciation, Franklin's assets under management have fallen from a peak of $898 billion in 2014 to $698 billion today, representing a 22% slump. Only 25% and 20% of Franklin's equity and fixed income assets, respectively, have outperformed their benchmarks over the past five years.

Legg Mason has fared better, with 83% of strategy assets under management beating their benchmarks over the same period. Adding these products to Franklin's distribution channels has potential to help stabilize the combined company's asset base.

Overall, the combined company has potential to benefit from its greater financial resources, fund diversification, global infrastructure, and complementary distribution channels.

However, industry headwinds seem unlikely to abate, and a deal of this magnitude carries execution risk. Clients get nervous when the funds they are invested in experience a change of control. If key personnel leave or the investment strategy seems to be drifting, they are more likely to pull their money.

Franklin has experience making large deals, including its $912 million acquisition of Templeton in 1992. Management also believes the affiliate structure of Legg Mason, in which its investment companies operate largely independently from the parent company, will minimize client breakage and cultural clashes.

Franklin doesn't plan to meddle with those operations. Instead, management will focus on integrating the parent companies to save costs while also increasing distribution opportunities.

Barring a material change in the combined company's fund performance, net asset ouflows, or integration execution, Franklin seems likely to maintain its Very Safe Dividend Safety Score while delivering low- to mid-single-digit dividend growth for the foreseeable future.

However, as we discussed in our December 2019 note, Franklin's path to profitable long-term growth faces some challenges. Combining with Legg Mason provides benefits, but it won't stop the headwinds facing active asset managers.