Converting to a Corporation Would Unlikely Affect Enterprise Products' Distribution Safety

The 2014-16 oil crash, regulatory changes, and U.S. tax reform combined to upend the midstream MLP industry in recent years. As a result of these challenges, numerous MLPs have executed substantial corporate restructuring activities, with some converting from partnerships to corporations.

Enterprise Products Partners LP (EPD) has long defended its structure as a partnership. After all, unlike many other MLPs, the firm has never had trouble accessing affordable capital and runs its business conservatively.

However, management's tune appears to be changing. On December 11, Bloomberg reported that Enterprise's CFO Randy Folwer said at a conference that "there may be an element of inevitability" regarding an eventual corporate conversion as "K-1 island is becoming very exotic."

In other words, as more pipelines ditch the MLP model, Enterprise feels it may be forced to abandon it as well, lest it be one of the few remaining firms with a business structure that's not fully rewarded by investors.

After all, most ETFs can't own MLPs, and the S&P 500 specifically excludes them. In theory, a conversion could increase investor interest (including on the retail side with simpler tax forms) and lead to higher valuations.

Over the last year C-Corp pipelines have outperformed midstream MLPs such as Enterprise and Energy Transfer (ET), perhaps increasing the appeal of converting.

Besides relative valuation, Enterprise is also considering cash income taxes it would need to pay as a corporation (MLPs don't pay corporate taxes, passing that obligation on to their unitholders) as well as the relative depth of equity and debt capital it could have access to.

For now, a potential conversion to a corporation is likely a year or two away, assuming such an event takes place. Enterprise realizes this is a long-term decision and is hesitant to rush into anything given the financial flexibility the business enjoys today.

One of the key drivers is the 21% corporate tax rate, which in 2017 was reduced from 35% as part of tax reform. With another election around the corner, Enterprise would like to make sure the rate is here to stay for the foreseeable future, making the firm unlikely to take any action before then.

If Enterprise does elect to become a corporation, perhaps in late 2020, the process could take two to three months for the firm to complete the transition and gain approval from its unitholders, according to Enterprise's CFO.

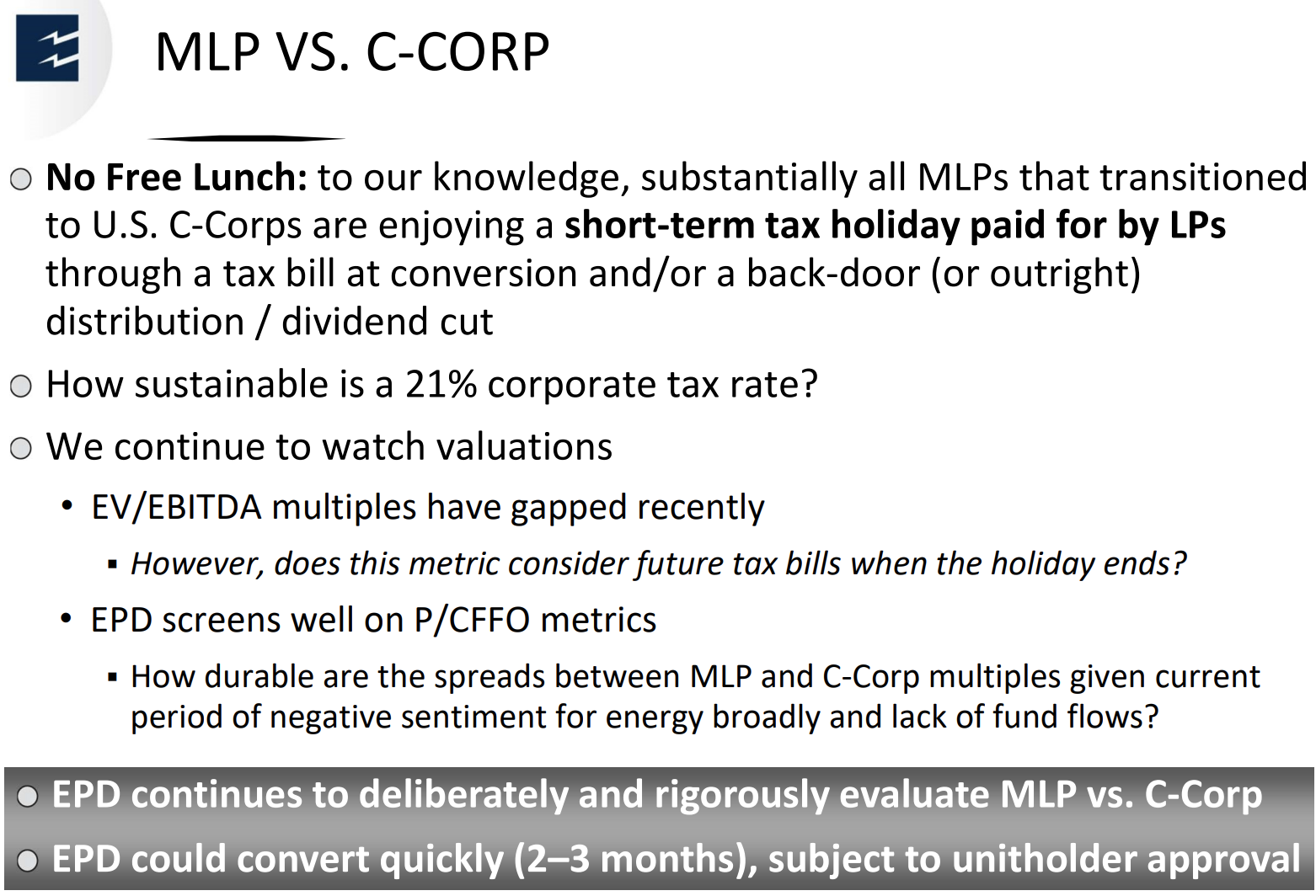

Source: Enterprise Investor Presentation

Would Enterprise's distribution remain safe if it converts to a corporation?

Almost certainly. Unlike many other MLPs involved in conversions, Enterprise has already addressed potentially costly issues such as eliminating incentive distribution rights (completed in 2011) and moving to a more conservative self-funding model for the equity portion of growth projects (reached in 2018).

The main incremental cost is income taxes, which MLPs passed through to their unitholders but corporations must pay. Fortunately, thanks in part to tax reform enacting more generous bonus depreciation rules for capital spending, in October 2018 Enterprise surmised that "you can keep your income taxes negligible for quite a while just depending on what your growth rate is."

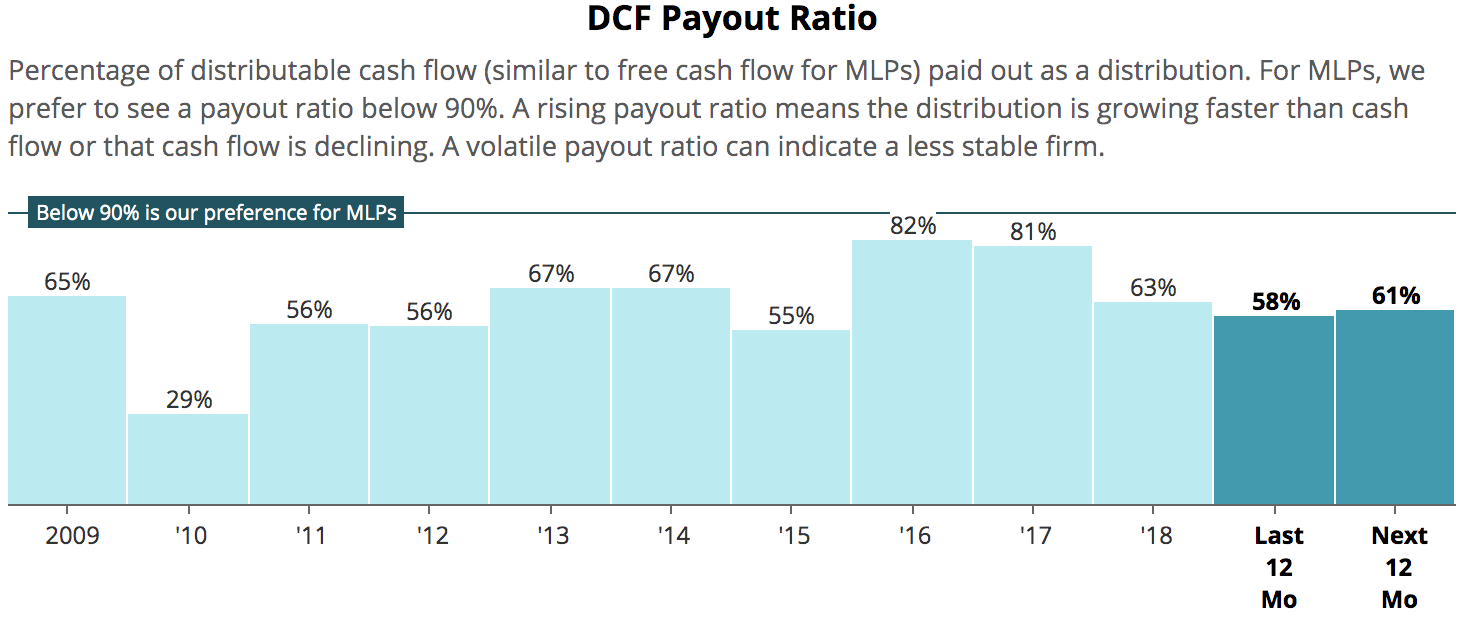

In other words, cash income taxes seem unlikely to be a material outlay for at least several years if Enterprise converted. Even if taxes aren't deferred as much as expected, Enterprise's excellent distribution coverage appears to provide room to both pay taxes and maintain the current payout with hurting the business.

Source: Simply Safe Dividends

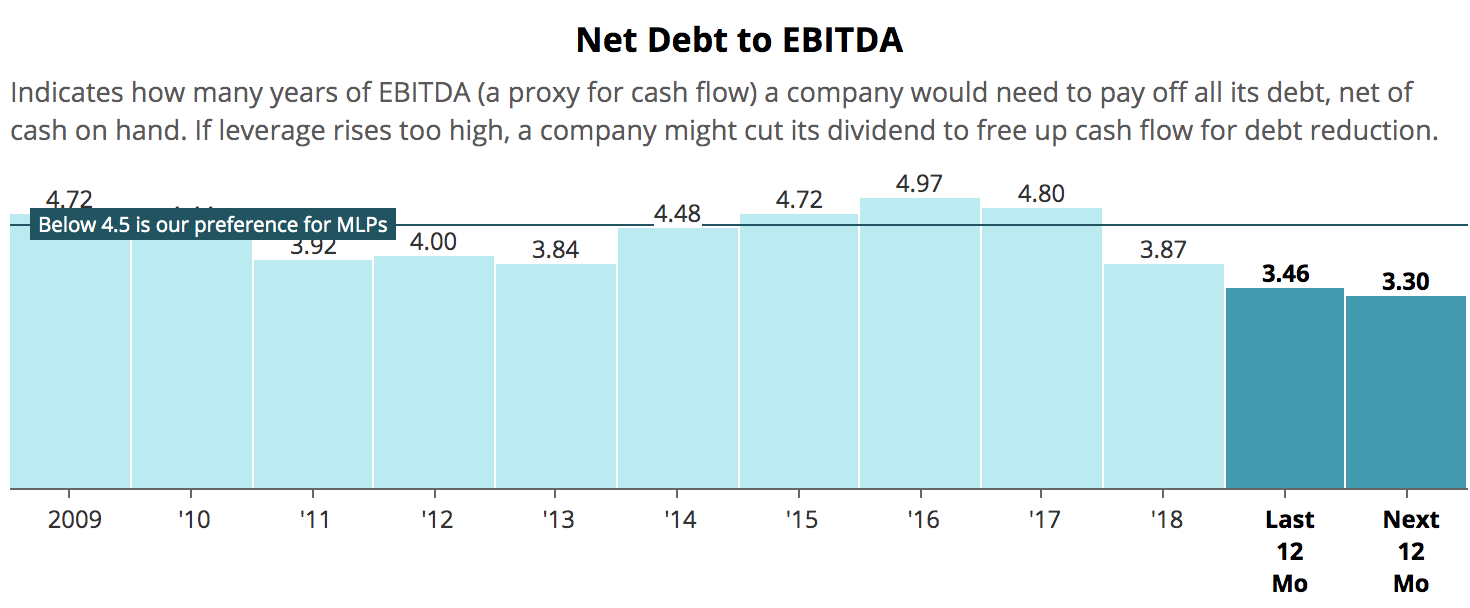

Enterprise will likely desire to continue self-funding its business. If corporate income taxes did materially reduce the amount of internally generated cash flow the business had available after paying dividends, then Enterprise could presumably lean more on debt capital until its cash flow grew higher.

As you can see, Enterprise's leverage ratio is in great shape, providing the business with flexibility to continue investing in its future while continuing to reward investors with higher payouts, as it has done for more than two decades.

Source: Simply Safe Dividends

Importantly, current unitholders are also unlikely to be stuck with a tax bill if Enterprise becomes a corporation.

When a pass-through entity converts to a C-Corp (rather than being bought out by a C-Corp), negative capital accounts are the main issue that can trigger a potential gain for unitholders upon conversion. You can check your K-1 to see the last balance of your capital account, and it's very unlikely to be negative.

In 2017, Enterprise said it reviewed the 2015 K-1s it issued, and less than 250,000 of its 2.1 billion units outstanding (at the time) had a negative capital account associated with them. The cumulative negative capital account balance was also less than $1 million.

Enterprise has also said it did not foresee doing any type of tax basis step-up which would create a tax liability for its limited partners.

As a C-Corp, Enterprise's shareholders would receive Form 1099-DIVs, eliminating Schedule K-1s and simplifying tax reporting. Depending on the company's income, which is often depressed by the high depreciation charges incurred by capital-intensive midstream businesses, a material amount of each payout could be classified as a non-taxable return of capital.

For example, pipeline corporation ONEOK (OKE) has classified 80-90% of its dividends as a return of capital in recent years, and Kinder Morgan (KMI) issued the same classification to about 70% of its total payout in 2018.

A return of capital reduces the adjusted cost basis of your stock and is not taxable, deferring the tax liability into the future, usually until you sell your shares. If your basis reaches zero, future returns of capital are taxable as a capital gain.

Overall, Enterprise's potentially increased interest in becoming a corporation seems like good news. In the event of a conversion, the firm's distribution is very likely to remain safe, and the vast majority of unitholders are unlikely to be stuck with a tax bill based on management's expressed intentions.

Most importantly, Enterprise is under no pressure to convert its business structure. The firm remains in excellent financial health and continues enjoying flexibility to execute on its growth opportunities as an MLP.

Becoming a corporation would simply be an opportunistic move done because management believes it would unlock more long-term value for unitholders.