Ventas Falls on Weak Senior Housing Outlook but the Dividend Continues to Look Safe

Shares of Ventas (VTR) tumbled nearly 10% on Friday in an uncharacteristic move for this healthcare REIT known for its stability.

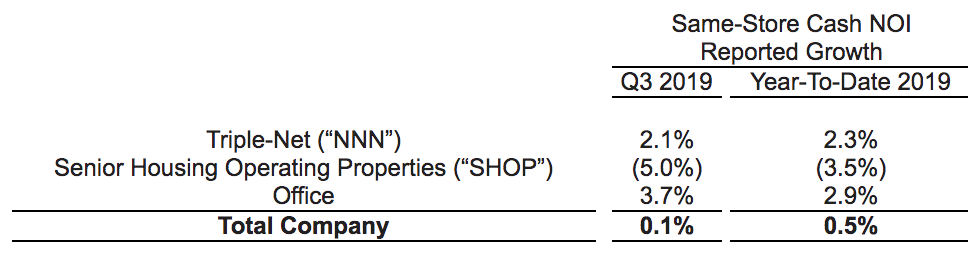

Ventas' third-quarter earnings report was the driver. Management cited "unprecedented" weakness in the senior housing market, which drives just over half of the firm's net operating income (NOI).

The firm's senior housing operating properties (SHOP), where Ventas partners up to run its own properties rather than lease them out as a landlord, generated 33% of the firm's NOI in 2019. SHOP's same-store NOI fell 5% last quarter.

Source: Ventas Earnings Release

The midpoint of Ventas' 2019 funds from operations (FFO) per share guidance was mostly maintained, but management said it no longer expects FFO to grow in 2020 due to prolonged softness in senior housing. Analysts had expected growth.

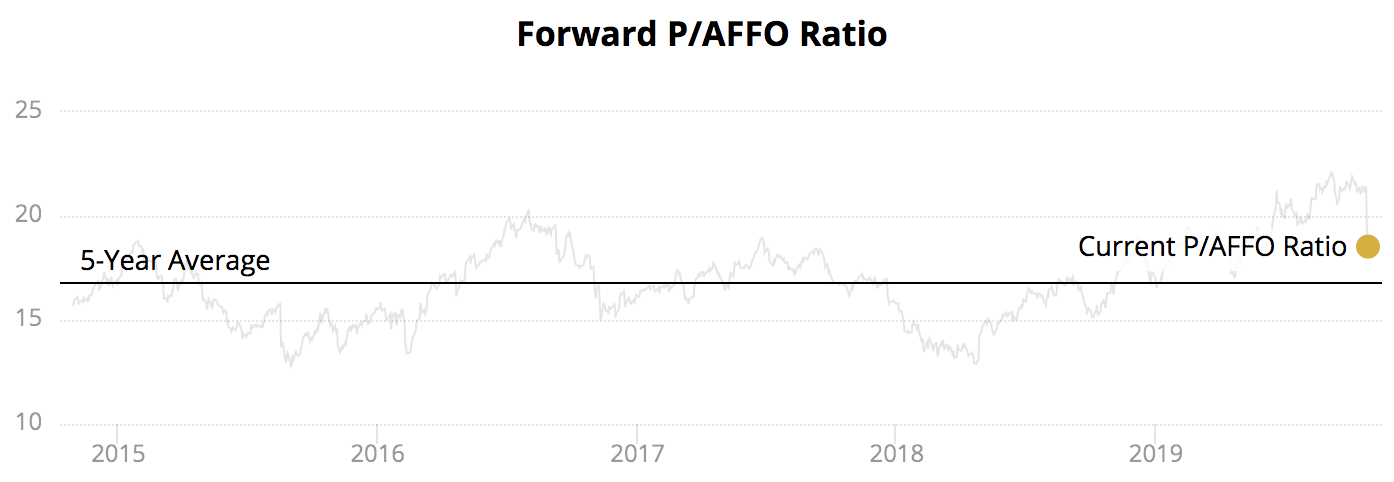

Combined with the elevated valuation multiple shares of Ventas had going into the quarter, it's not surprising to see the stock respond so negatively to this news. The bar was high. Many investors believed the senior housing market had bottomed earlier this year, but now Ventas faces more uncertainty over its return to growth.

Source: Simply Safe Dividends

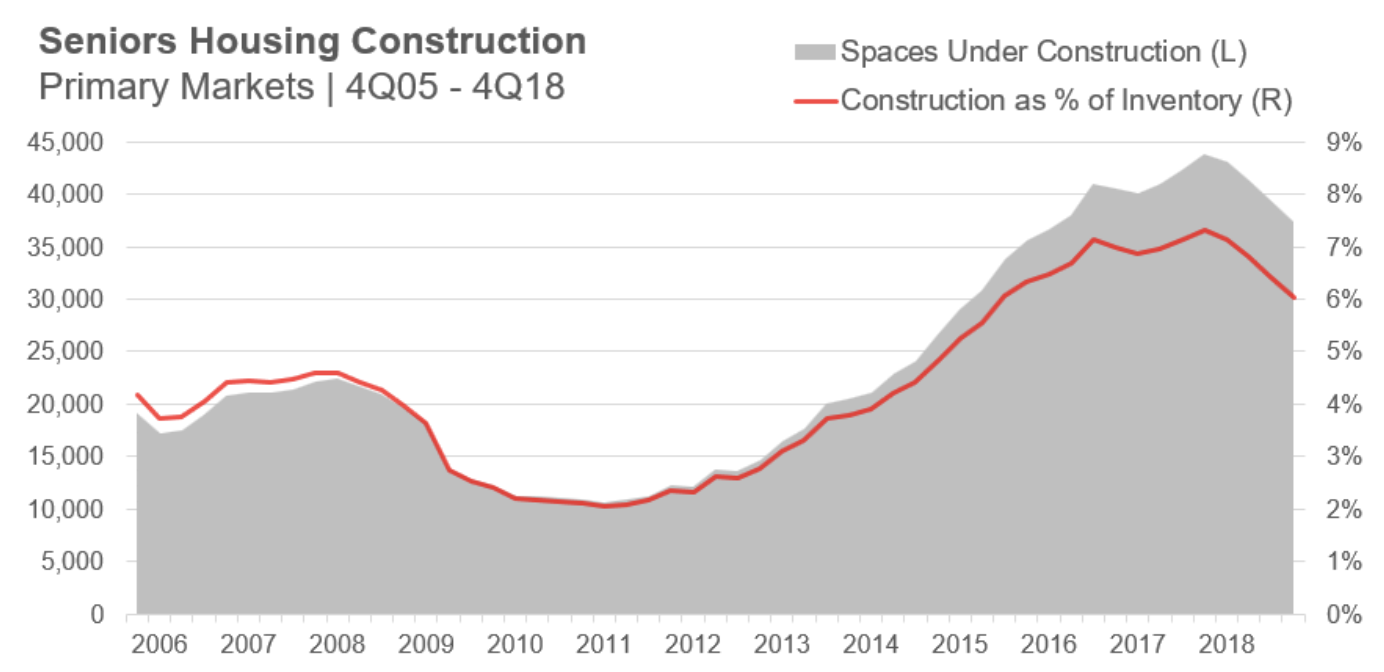

In recent years, capital flooded into the senior housing market as investors anticipated a boom in demand thanks to America's aging population. As you can see, the number of senior housing spaces under construction doubled over the last decade and only began falling in 2018.

Source: National Investment Center for Seniors Housing & Care

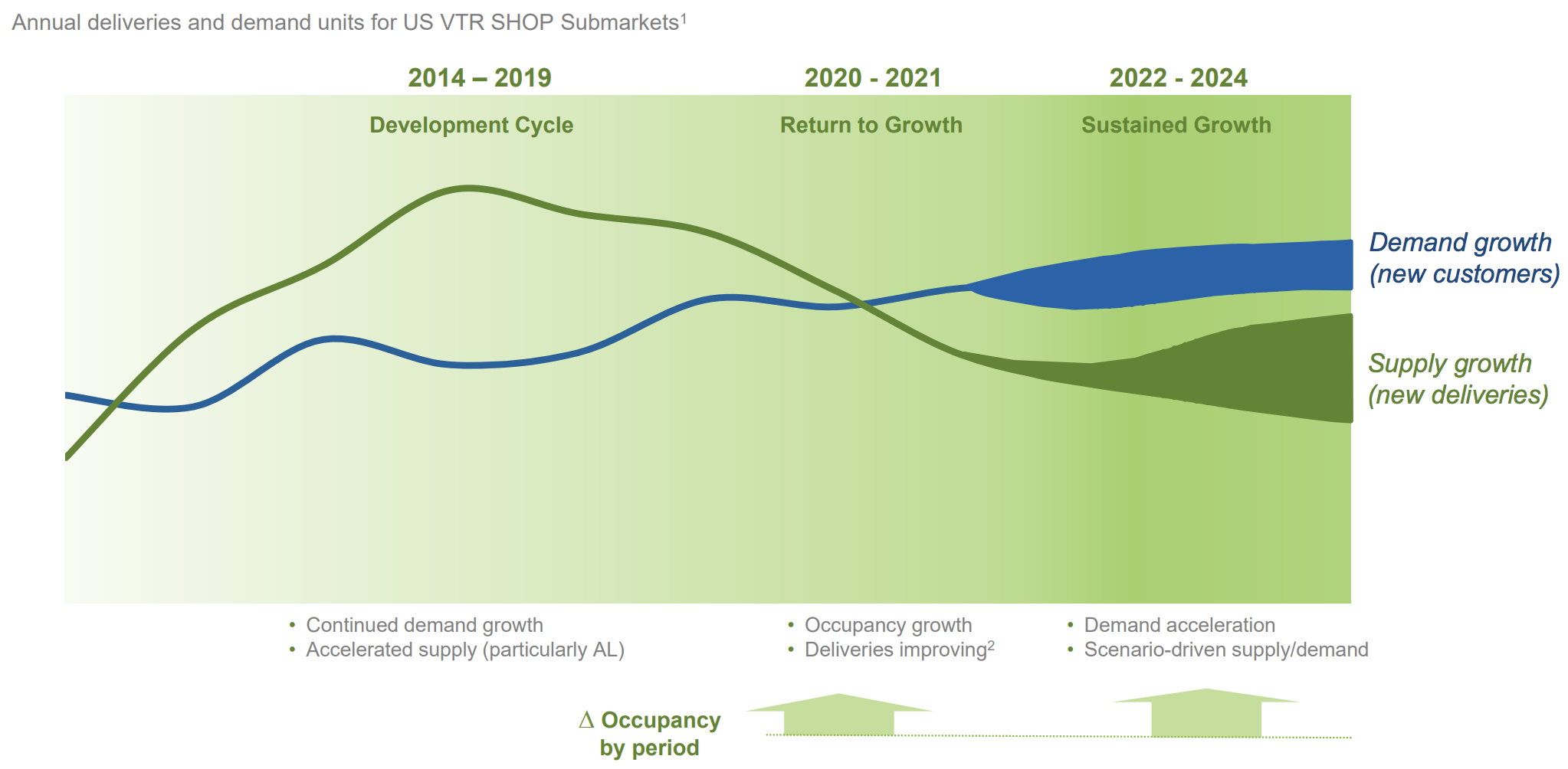

It takes time for these properties to reach completion, come online, and add new residents. Management was hopeful that the industry would return to growth next year as new construction starts moderated and demand continued growing, but that forecast no longer appears likely.

Source: Ventas Investor Presentation

Instead, the cumulative effect of new senior housing openings is weighing on occupancy levels and resulting in unexpected pricing pressures. Ventas said it plans to get more aggressive with its own pricing to help maintain its occupancy levels. The REIT will also consider pruning parts of its portfolio.

Management's inability to get in front of this challenge or better communicate more reasonable growth expectations is disappointing. Ventas also refused to offer more guidance on 2020 until January, further frustrating investors.

Fortunately, Ventas' disappointing outlook in SHOP seems likely to fade in the years ahead. Sure, industry fundamentals could remain weaker for longer, but the population will continue aging and new construction activity is slowing. It's mostly a matter of when more people will decide to move into senior housing.

Matthew Huber, senior vice president at People's United Bank Healthcare Financial Services, detailed four reasons to be cautious about senior housing construction in late 2018.

The first point he raised was that today's oldest baby boomers are still years away from the age that most folks have historically considered moving into senior housing. Baby boomers are also in better health than past generations, perhaps pushing their move-in dates even further out:

"Much of today’s construction seemingly is justified by the aging baby boomers. There’s no question this 76 million strong generation will put plenty of demand on the senior care market … eventually. But even the very oldest boomers are 72 years old (the youngest are turning 54 this year); that’s 10 years younger than the average person in the previous generation, the Silent Generation, opted to move into senior housing."

Despite some of his reasons for caution, Mr. Huber said he did not believe senior housing was in a bubble, and Ventas called out record demand for senior housing last quarter. Ventas' healthcare portfolio is also diversified to provide some protection in case the senior housing market continues struggling to stabilize.

In fact, U.S. SHOP only accounts for about 25% of the firm's NOI, and the other areas of its business (research, life sciences, medical office, triple-net senior housing, Canadian SHOP) continue enjoying low-single digit NOI growth.

Even its portfolio of triple-net senior housing properties (about 25% of NOI) continues generating growth since most of Ventas' tenants remain in solid enough financial health to honor their rent commitments despite industry headwinds.

Therefore, based on what we know today, the latest step down in senior housing fundamentals seems unlikely to affect the safety of Ventas' dividend.

It would probably take much greater industry pressure, along with rent defaults in Ventas' triple-net senior housing portfolio (no tenant accounts for more than 9% of firm-wide NOI), to eventually put the dividend at risk.

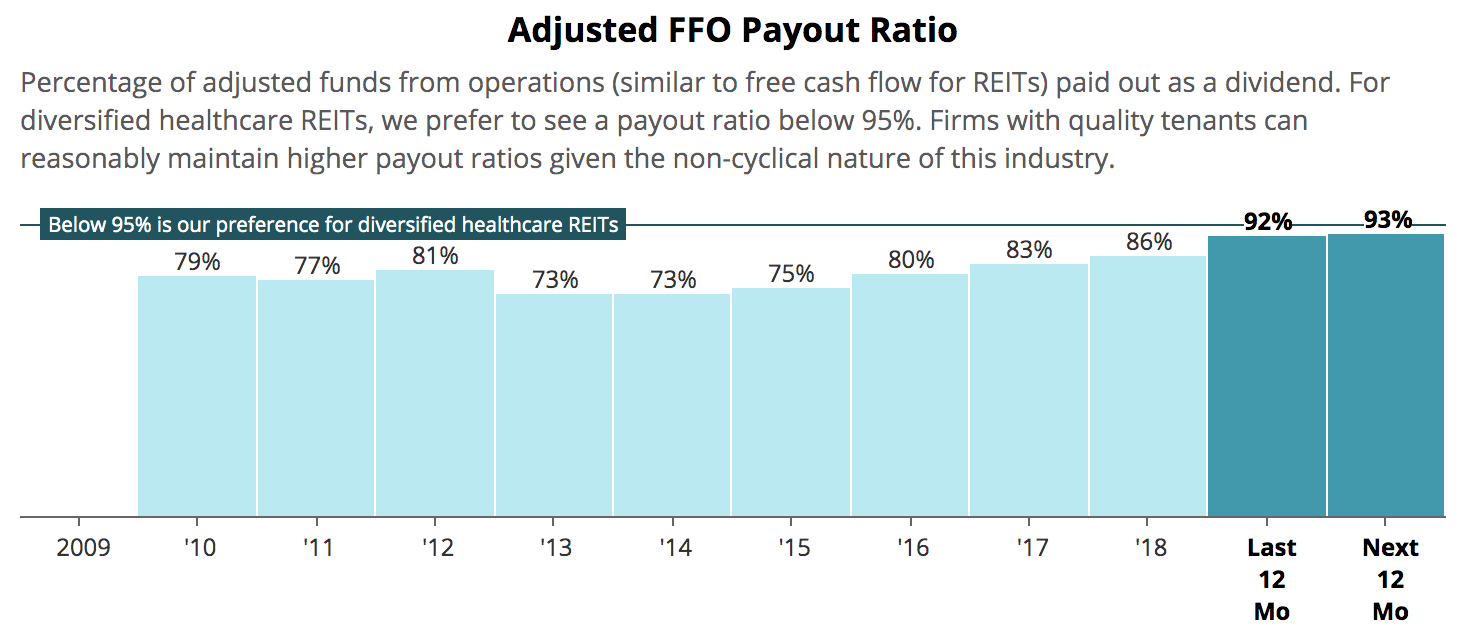

Despite the weakened outlook for 2020, the firm's payout ratio should remain at a reasonable level for most diversified healthcare REITs. Ventas executed a number of divestitures in recent years which pushed up its payout ratio but also improved the safety and quality of its cash flow, making its rising payout less of a concern.

Source: Simply Safe Dividends

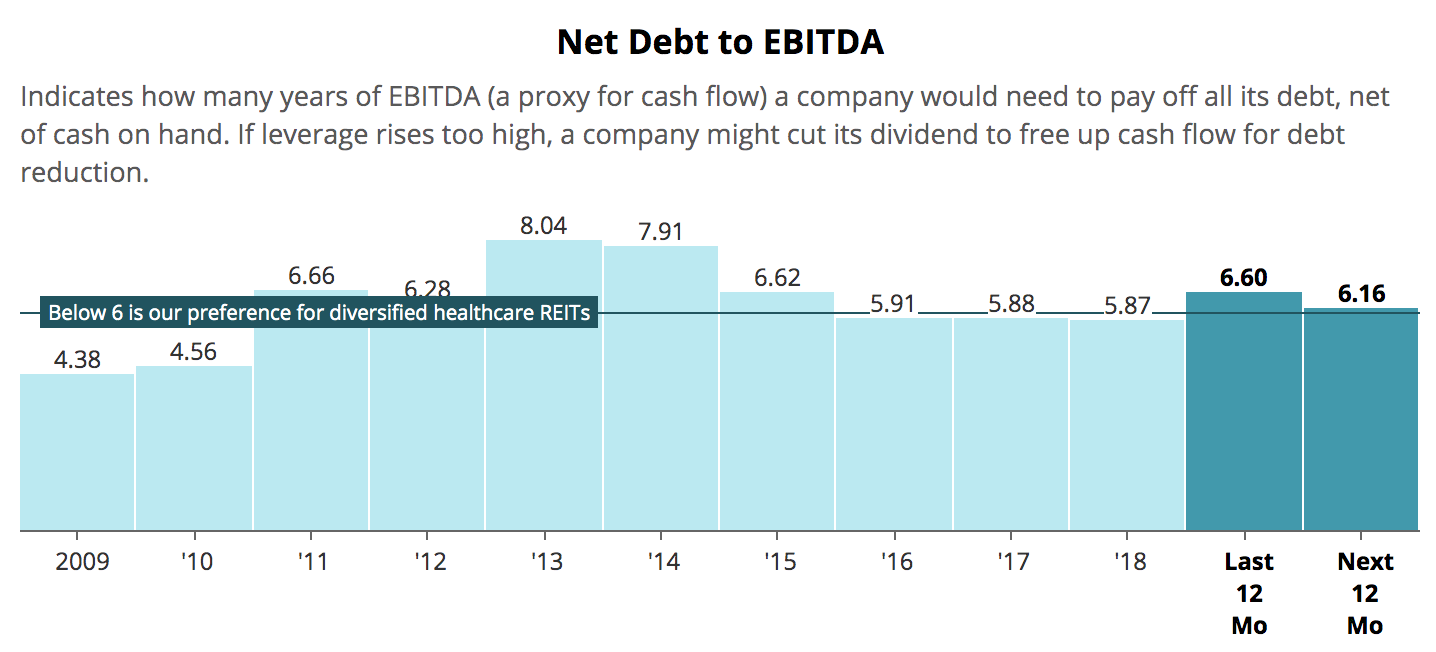

Ventas also maintains a leverage ratio in line with its historical levels, earning the REIT a solid BBB+ investment-grade credit rating from Standard & Poor's. This provides flexibility for Ventas to continue making selective acquisitions without jeopardizing its balance sheet or ability to pay its dividend.

However, investors shouldn't expect much, if any, dividend growth from Ventas until the business returns to positive NOI growth.

Source: Simply Safe Dividends

Overall, I'd bet that the long-term fundamentals of U.S. senior housing remain intact, but I couldn't begin to guess when the industry's current imbalance will correct itself.

The industry's low barriers to entry make life difficult for most operators, and visibility is clearly limited. Ventas doesn't have much of an edge outside of its historically conservative and disciplined management team, as well as its access to affordable capital.

With that said, Ventas appears to continue maintaining the financial strength and portfolio diversification necessary to weather most storms without threatening the safety of its dividend.

The stock's valuation also looks a little more reasonable following the selloff, but future performance will depend on management's ability to get Ventas growing again. If I owned shares of the REIT, I would stay patient and continue holding.