High dividend stocks appeal to many investors in retirement because they provide substantial passive income. And unlike the fixed interest paid from bonds, dividends can grow each year to help combat inflation.

But not all of the highest dividend stocks are safe. From aggressive payout ratios to risky debt loads and businesses in secular decline, stocks with high dividends require extra research to avoid investing in yield traps.

We reviewed the universe of high dividend stocks to identify companies capable of paying safe dividends. These businesses maintain prudent dividend policies, strong balance sheets, and operations that generate predictable cash flow.

The top 25 high dividend stocks analyzed below possess these traits and have:

An average dividend yield above 4%, with some as high as 10%

The high-yield dividend stocks below are ordered by how many consecutive years they have maintained or increased their dividends, starting with the shortest streaks.

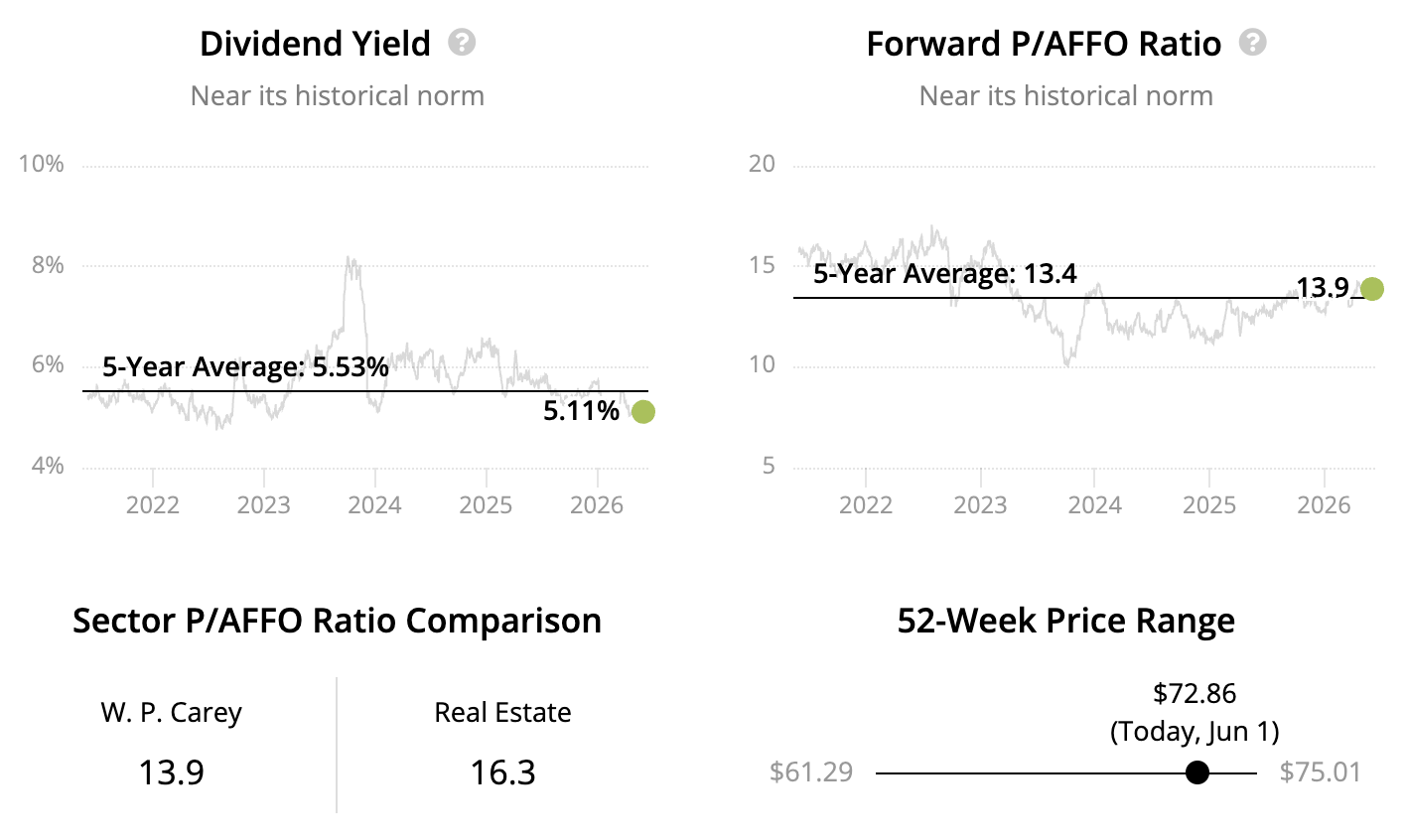

High Dividend Stock #25: W.P. Carey

Sector: Real Estate – Diversified REITs Dividend Yield: 5.1% Dividend Safety Score: Safe Uninterrupted Dividend Streak: 2 years

Named after its founder and formed in 1973, W.P. Carey (WPC) owns over 1,300 single-tenant properties primarily spanning industrial (~35% of rent), warehouse (~30%), retail (~20%), and self-storage (<10%) markets.

Source: W.P. Carey

The REIT's diverse portfolio is leased to more than 300 tenants operating in over 20 industries across the U.S. and Europe. No tenant exceeds 4% of rent, and W.P. Carey is not overly dependent on any single market.

W.P. Carey's risk profile is strengthened by the firm's focus on buildings that serve critical functions for tenants. Examples include key distribution facilities, profitable manufacturing plants, and top-performing retail stores.

These operationally essential properties are also occupied mostly by larger companies, such as ExtraSpace Storage and Apotex (Canada's largest generic drug manufacturer), which are better equipped to weather economic downturns.

Coupled with an average lease duration of over 10 years, W.P. Carey has historically maintained strong occupancy rates of nearly 100% and collected nearly all of its rent through the 2020 pandemic.

Further backed by a BBB+ credit rating and healthy payout ratio targeted around 70%, W.P. Carey is an appealing high-yield dividend stock well-positioned to support a stable dividend.

Source: Simply Safe Dividends

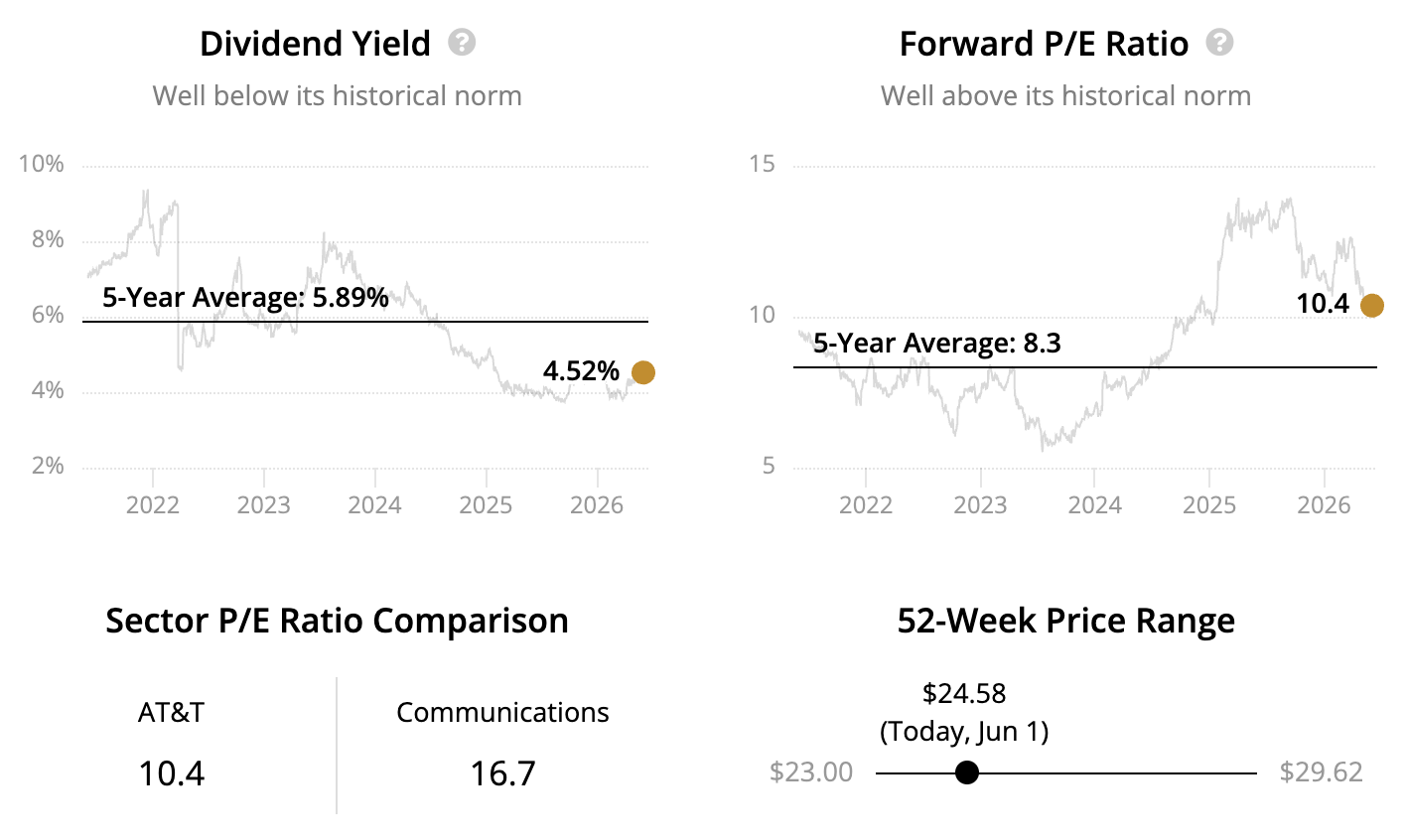

High Dividend Stock #24: AT&T

Sector: Communications – Wireless and Internet Services

Dividend Yield: 4.5% Dividend Safety Score: Safe

Uninterrupted Dividend Streak: 3 years

AT&T (T) has frustrated investors for years. From overpaying for acquisitions to overextending the company's balance sheet and cutting the dividend in 2021, management has found no shortage of ways to destroy shareholder value.

But the future looks brighter. After shedding DirecTV and its media business, wireless and internet services now drive the bulk of AT&T's profits.

Source: AT&T

These businesses enjoy high barriers to entry due to their capital intensity, and they generate predictable cash flow over an economic cycle thanks to the essential needs they serve.

With increased focus from management on the core business, AT&T has the potential to deliver more reliable growth in wireless services and broadband revenue while also improving margins.

Coupled with a healthier payout ratio near 50% and consistent free cash flow generation to strengthen its BBB rated balance sheet, AT&T's high dividend looks better supported.

As the company continues returning to its communication roots and no longer focuses on empire-building, contrarian investors interested in high yielding dividend stocks may consider giving AT&T another look.

Source: Simply Safe Dividends

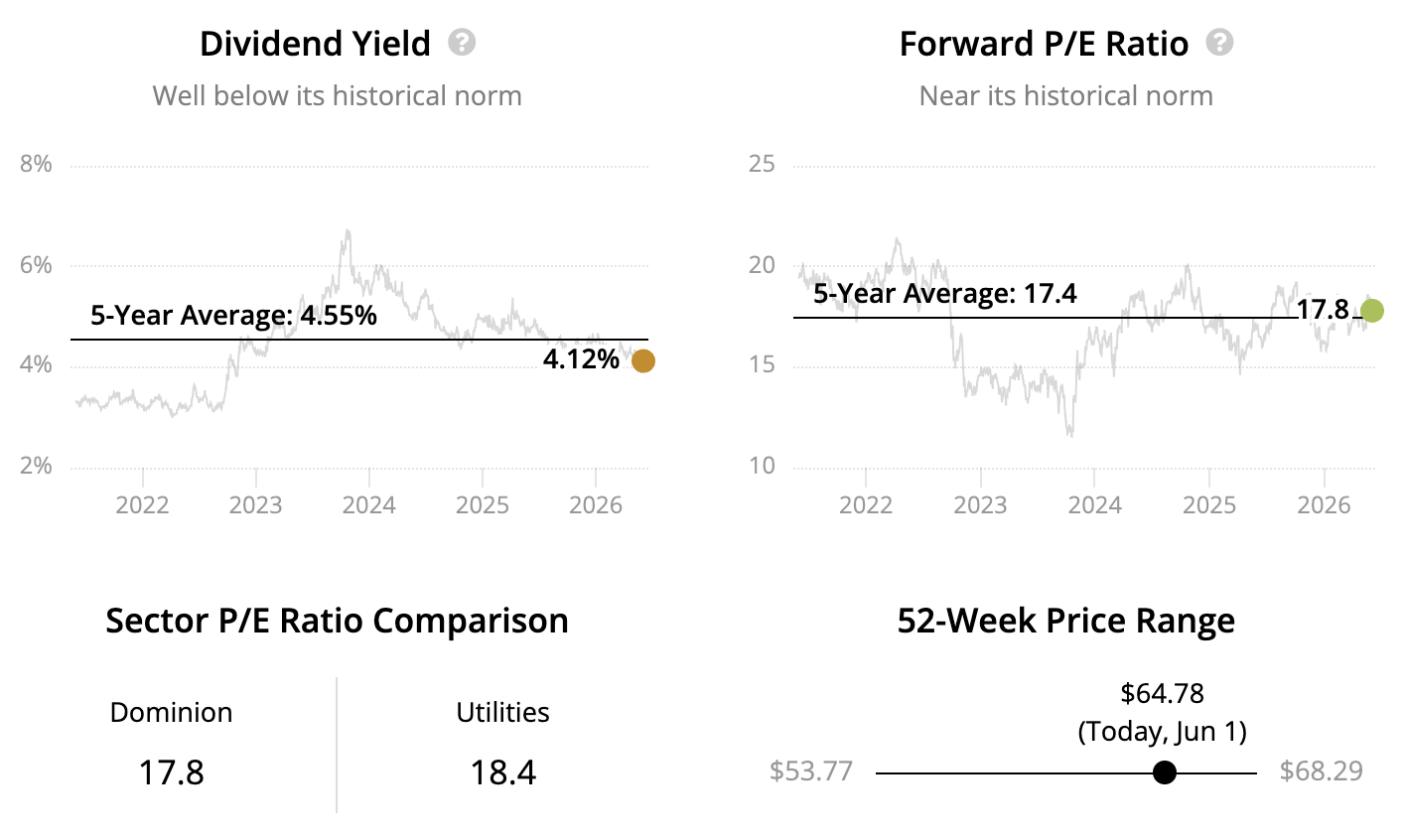

High Dividend Stock #23: Dominion Energy

Sector: Utilities – Electric Utilities Dividend Yield: 4.1% Dividend Safety Score: Safe Uninterrupted Dividend Streak: 5 years

Dominion Energy (D) and its predecessors have delivered diversified forms of energy since 1898. However, in 2024, the company simplified into a pure-play electric utility primarily serving Virginia and the Carolinas.

Source: Dominion Energy

Dominion Energy has been out of favor with investors in recent years, more so than other utility operators stung by higher interest rates and a preference for growth stocks, as the company embarked on a lengthy strategic review of the business following a surprise dividend cut in 2020.

However, with the review concluded and resulting in the divestiture of its natural gas businesses (the proceeds of which will be used to reduce debt), Dominion will move forward with a more predictable income stream as a pure-play electric utility.

Despite the improved income stability achieved through divesting its natural gas assets, the firm's payout ratio will be stretched. Even so, management intends to keep the dividend intact – but the payout will be frozen for up to five years until dividend coverage improves.

That said, now could be an interesting time to lock in a solid dividend yield for patient investors who will be rewarded once the dividend starts growing again at what could be one of the faster rates in the sector.

Dominion's footprint in Virginia (~70% of earnings) looks particularly interesting. The state's cheap land, low-cost energy, proximity to East Coast cities, and low natural disaster risk have made it the largest data center market in the world.

Data centers require tons of electricity to power servers and cooling systems. Artificial intelligence, cloud computing, and the continued adoption of digital technologies could cause long-term power demand to come in stronger than that market expects, giving Dominion a long runway to invest in needed infrastructure.

Coupled with a BBB+ credit rating, high mix of regulated earnings, and an industry-leading yield, Dominion could be attractive to defensive income investors willing to forgo a few years of dividend growth.

Note that NextEra Energy (NEE) is in the process of acquiring Dominion.

Source: Simply Safe Dividends

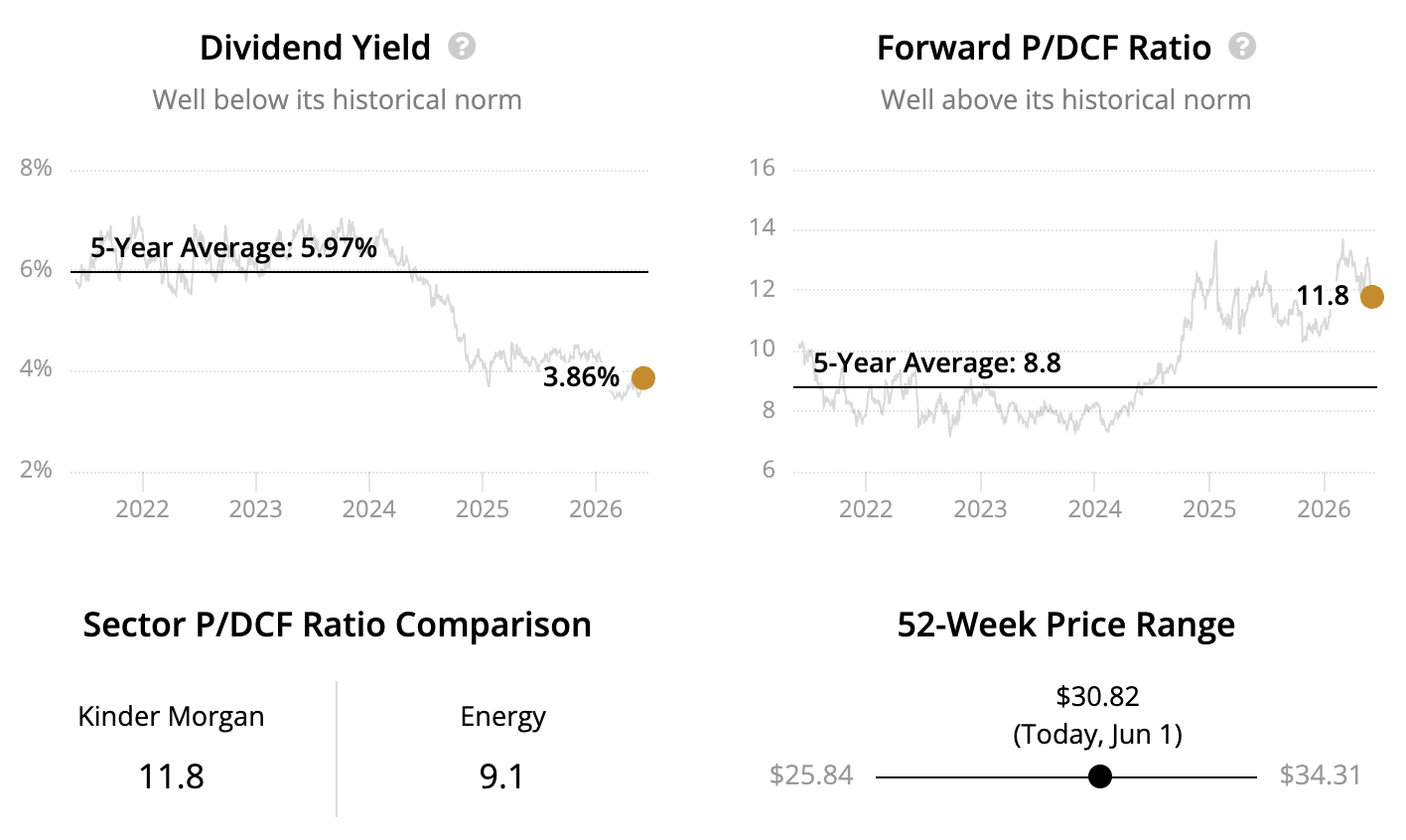

High Dividend Stock #22: Kinder Morgan

Sector: Energy – Oil and Gas Storage and Transportation

Dividend Yield: 3.8% Dividend Safety Score: Safe

Uninterrupted Dividend Streak: 10 years

Kinder Morgan (KMI) has grown since its formation in 1997 to become of the largest midstream infrastructure companies in North America. The firm makes most of its money from natural gas pipelines, with remainder balanced between refined products and oil pipelines, storage, and sales of carbon dioxide used in oil production.

Kinder Morgan's pipelines, storage facilities, and terminals are integrated into almost all parts of the U.S. energy industry, including every major gas and oil shale formation and export markets along the Gulf Coast.

Source: Kinder Morgan

Despite generating stable cash flow from its essential infrastructure assets, Kinder Morgan burned high-yield investors in 2015 by slashing its dividend by 75%. (The firm had a Very UnsafeDividend Safety Score™ prior to its cut announcement.)

The payout reduction was caused by the company's high leverage and dependence on issuing equity to fund large expansion projects.

Management prioritized growth spending and preserving Kinder Morgan's investment-grade credit rating over the dividend when oil prices crashed in 2015 and caused investors to sour on the midstream industry, cutting off access to equity financing.

Kinder Morgan has since de-risked its business profile by implementing a self-funding business model (no need to issue equity), scaling down its growth ambitions, reducing its debt, and improving its credit rating by two notches to BBB+.

Coupled with a conservative payout ratio near 50% and a durable cash flow stream backed primarily by long-term contracts and fee-based, take-or-pay contracts, Kinder Morgan should be one of the more reliable stocks with high dividends going forward.

Source: Simply Safe Dividends

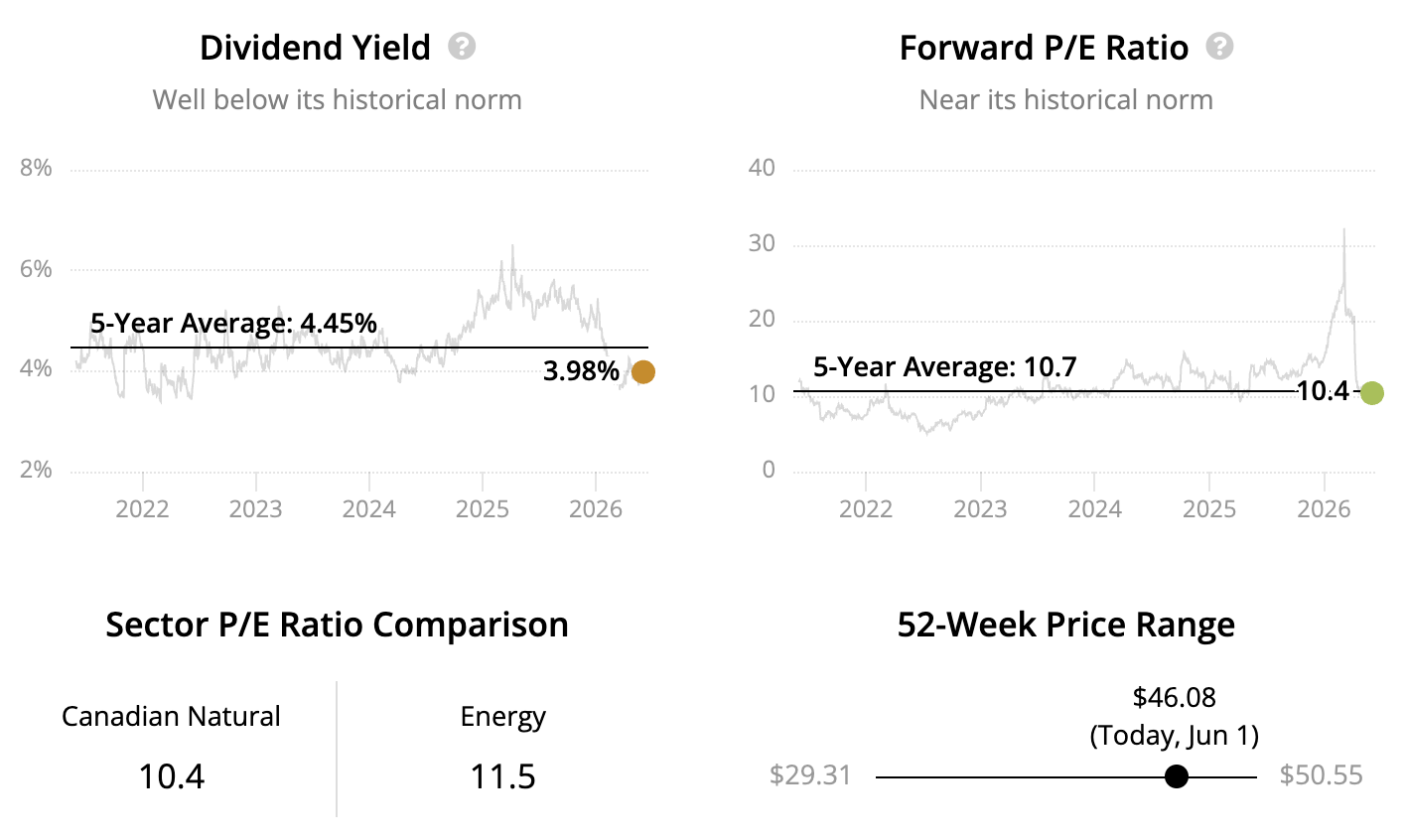

High Dividend Stock #21: Canadian Natural Resources

Sector: Energy – Oil and Gas Exploration and Production

Dividend Yield: 4.0% Dividend Safety Score: Safe

Uninterrupted Dividend Streak: 25 years

Formed in 1973, Canadian Natural Resources (CNQ) is Canada's biggest oil producer. The firm generates most of its profits from upstream activities with a balanced production mix across heavy, light, and synthetic oil and natural gas.

Around 60% of the company's production comes from long-life, low-decline resources with an emphasis on oil sands. Oil sand is a heavy mixture of bitumen, sand, fine clays, and water. Since it doesn't flow like conventional crude oil, it must be mined or heated underground before processing, making it one of the world's highest carbon-emitting oil grades.

Source: Canadian Natural Resources

Big foreign oil producers have been exiting Canada's oil sands as a result, giving Canadian Natural opportunities to acquire more production at attractive prices and gain synergies across the rest of its operations. Most recently, Canadian Natural in October 2024 agreed to buy Chevron's Canada oil sand and shale assets for $6.5 billion, which will lift its output by about 9%.

While oil sands have high fixed costs, their reserves have a very long life and a minimal cost to sustain production. Canadian Natural's existing resource base is expected to support several decades of production at current rates, and the company can cover its dividend and maintenance capital expenditures at an oil price near $40 per barrel.

These qualities, plus a disciplined used of debt that supports a BBB- credit rating, have helped the firm raise its dividend for 24 consecutive years. The best time to buy Canadian Natural is during a period of plunging oil prices, but shares look reasonably valued for income investors who believe in the staying power of fossil fuels.

Source: Simply Safe Dividends

Note that as a Canadian company, dividends paid by Canadian Natural to U.S. investors are subject to a 15% withholding tax. Investors can avoid this tax by holding Canadian Natural in retirement accounts. Otherwise, with some additional paperwork, investors can generally claim a tax credit with the IRS to offset the withholding tax.

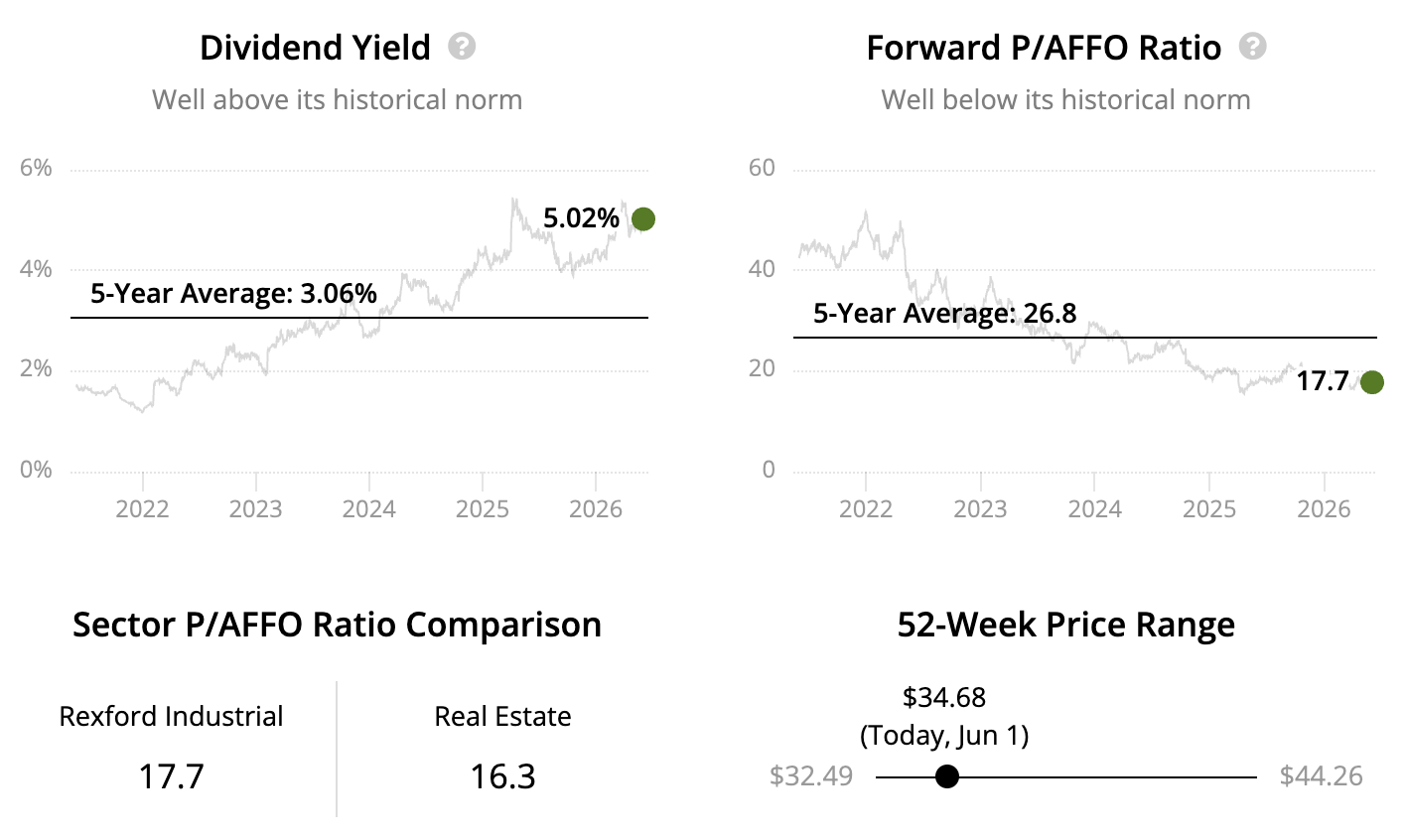

High Dividend Stock #20: Rexford Industrial

Sector: Real Estate – Industrial REITs

Dividend Yield: 5.0% Dividend Safety Score: Very Safe

Uninterrupted Dividend Streak: 11 years

Rexford Industrial (REXR) owns and manages industrial properties like warehouses and distribution centers across Southern California, one of America's most land-constrained and supply-limited markets.

Source: Rexford Industrial

The region's dense population and proximity to shipping ports make it a crucial hub for logistics, while the scarcity of developable land creates significant barriers to entry for new competitors. This dynamic has enabled the REIT to maintain high occupancy rates of over 95% and a stable cash flow stream.

Rexford's unique position near Southern California's shipping ports, which play a critical role in the American economy, provides some protection against recessionary headwinds. Industrial real estate demand in the area remains solid, driven by e-commerce and the ongoing need for logistics hubs close to major urban centers.

Rexford's well-located properties, combined with limited new supply, should provide continued pricing power, allowing it to grow rents even in slower economic environments.

The company's low leverage (BBB+ credit rating from S&P), healthy payout ratio around 85%, and long-term lease structures add further stability to the business.

Source: Simply Safe Dividends

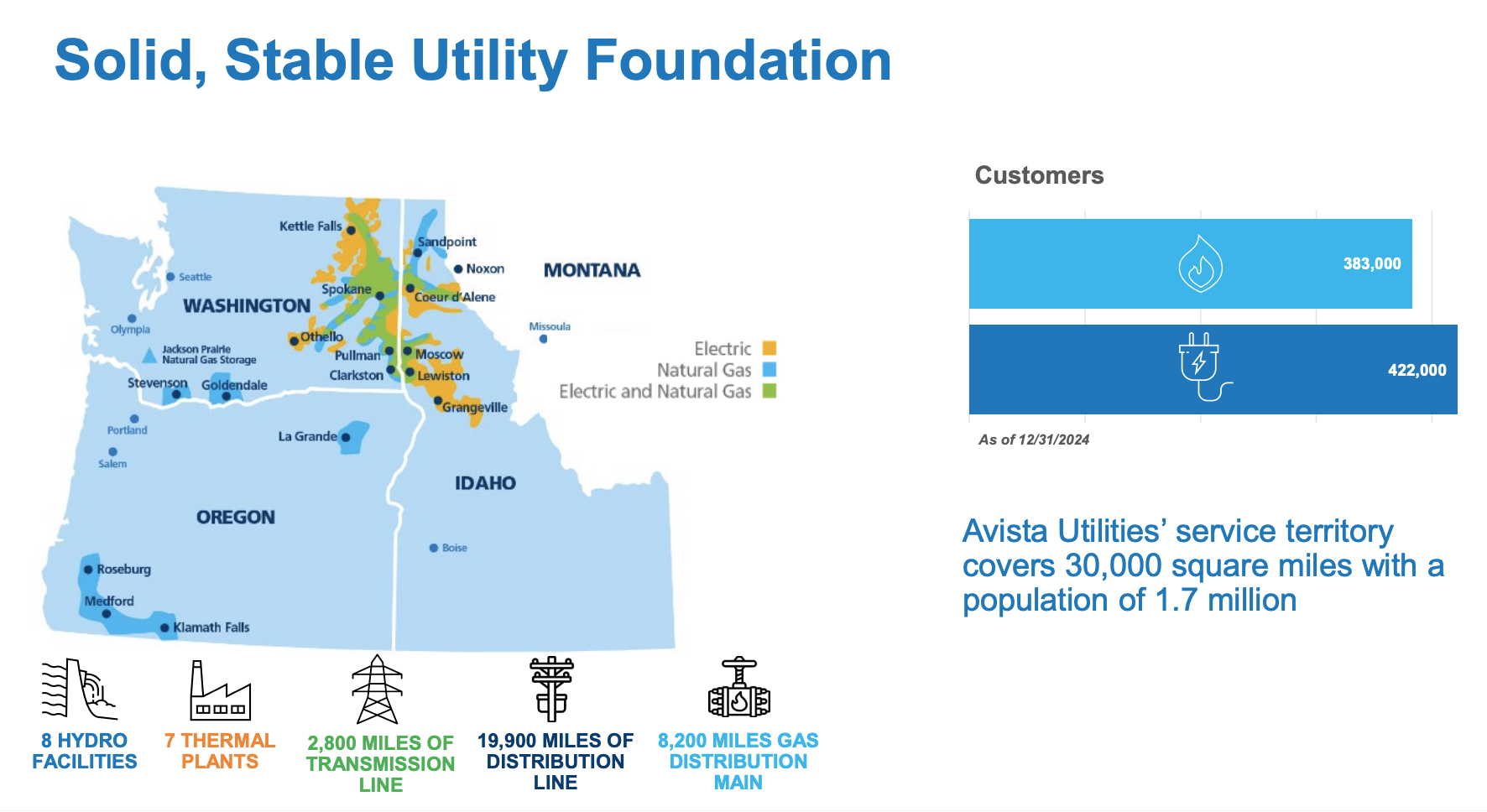

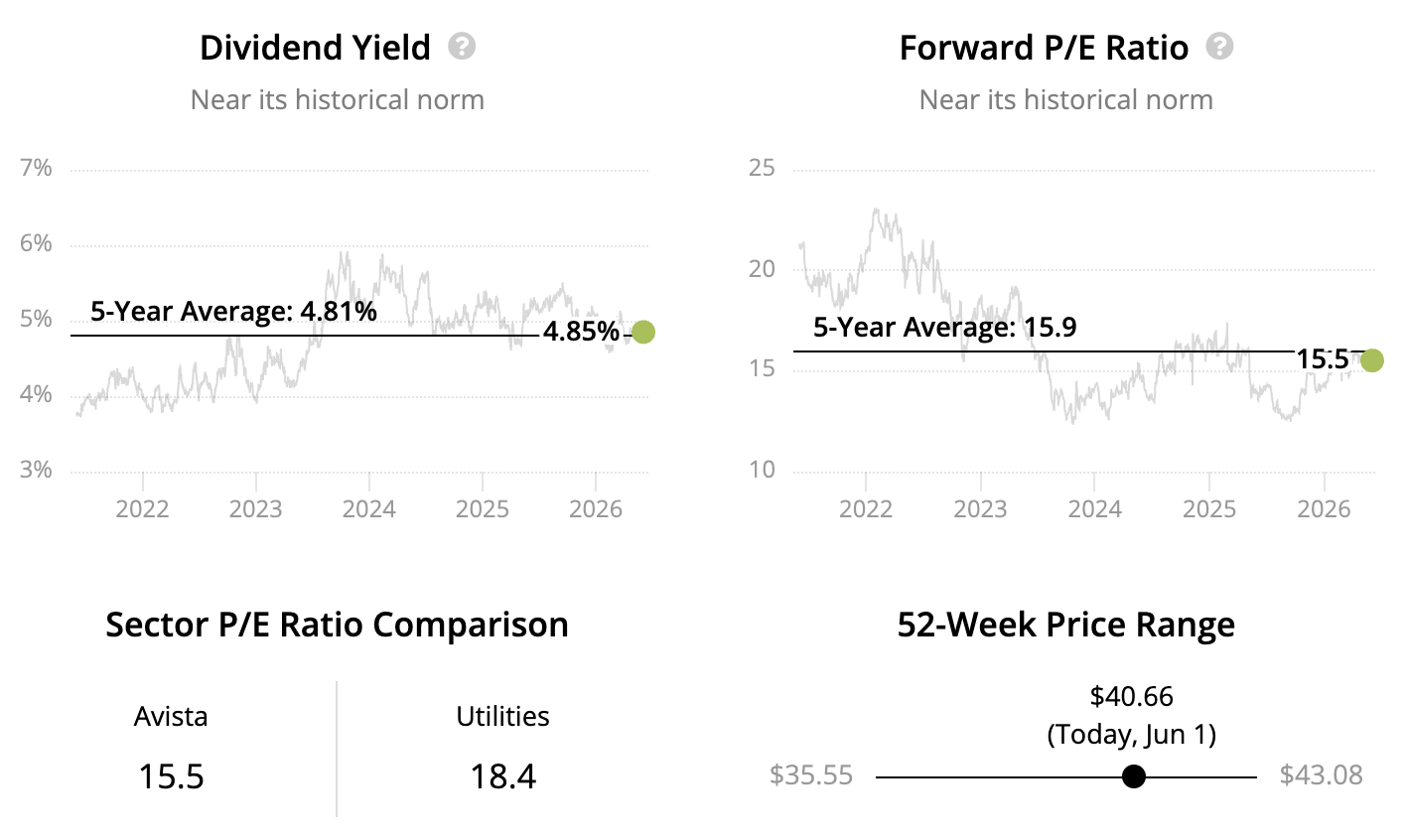

Founded in 1889, Avista (AVA) initially focused on harnessing hydroelectric power from the Spokane River. Today, the company is an electric and gas utility serving customers in eastern Washington and north Idaho.

Source: Avista

Washington and Idaho may not boast rapid population growth or booming industries like AI-driven data centers, but Avista's service areas have proven to be steady profit generators.

As a pure-play regulated utility, Avista's predictable earnings have supported safe dividend payments every year since at least 1950. The only exception was in 1998, when a new CEO cut the payout to fund an aggressive growth plan that ultimately failed.

Today, the company is in a much stronger position. Avista remains committed to its low-risk, regulated utilities, carries a BBB credit rating, and is steadily working to lower its payout ratio to management's 65% to 75% target range. This should support mid-single-digit annual dividend growth within a few years.

Despite these strengths, Avista trades at a discount to the broader utilities sector. This likely reflects its smaller size, slower growth rate, and investor concerns over wildfire risk, although these concerns may be overstated.

Avista has implemented emergency power shut-offs, upgraded field equipment, and benefits from regulatory cost recovery. The most expensive fire it has faced cost $21 million and was fully covered by insurance. Compared to California utilities, Avista's climate risk is relatively modest.

Source: Simply Safe Dividends

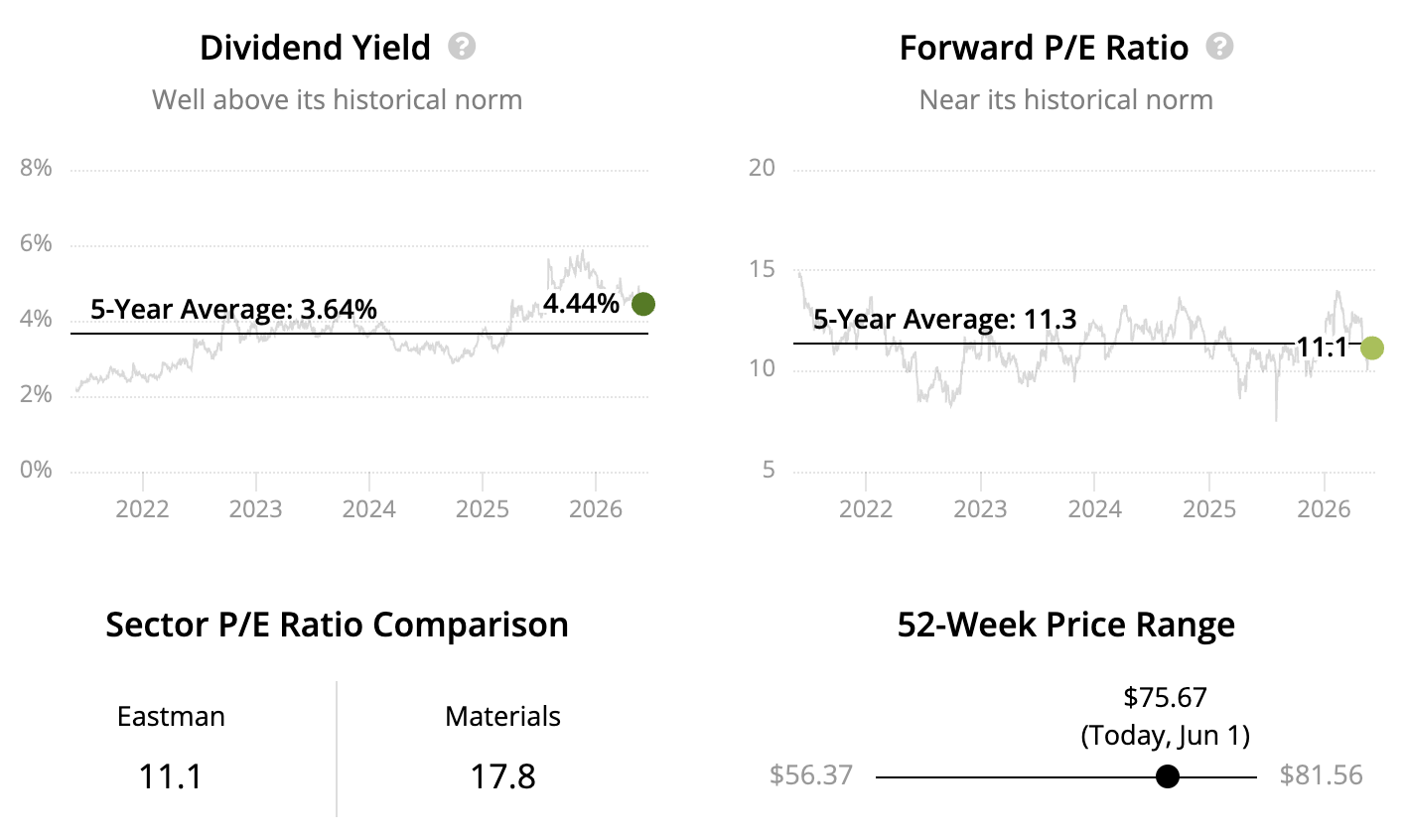

High Dividend Stock #18: Eastman Chemical

Sector: Materials – Commodity Chemicals

Dividend Yield: 4.4% Dividend Safety Score: Safe

Uninterrupted Dividend Streak: 31 years

With roots tracing back to 1920, Eastman Chemical (EMN) supplies materials used in everything from car windshields and medical devices to food packaging and durable consumer goods.

Eastman generates about two‑thirds of its revenue from specialty plastics and additives that improve product performance and command higher, more stable margins than basic commodity chemicals. These offerings serve long‑term trends in lightweight autos, durable packaging, and electronics, giving Eastman pricing power and customer stickiness.

Source: Eastman Chemical

Over half of Eastman's revenue comes from additives and specialty plastics tied to everyday items, including food packaging and personal care goods like shampoo bottles. This stable demand helps Eastman's cash flow hold up in downturns.

Coupled with cost‑plus contracts that pass raw‑material swings to customers, a highly integrated low‑cost manufacturing network, a BBB‑rated balance sheet, and a payout ratio near 40%, Eastman has solid flexibility to protect its dividend in all manner of economic environments.

Investors comfortable with the chemical industry's cyclicality may find Eastman to be one of the more interesting income plays in the space.

Source: Simply Safe Dividends

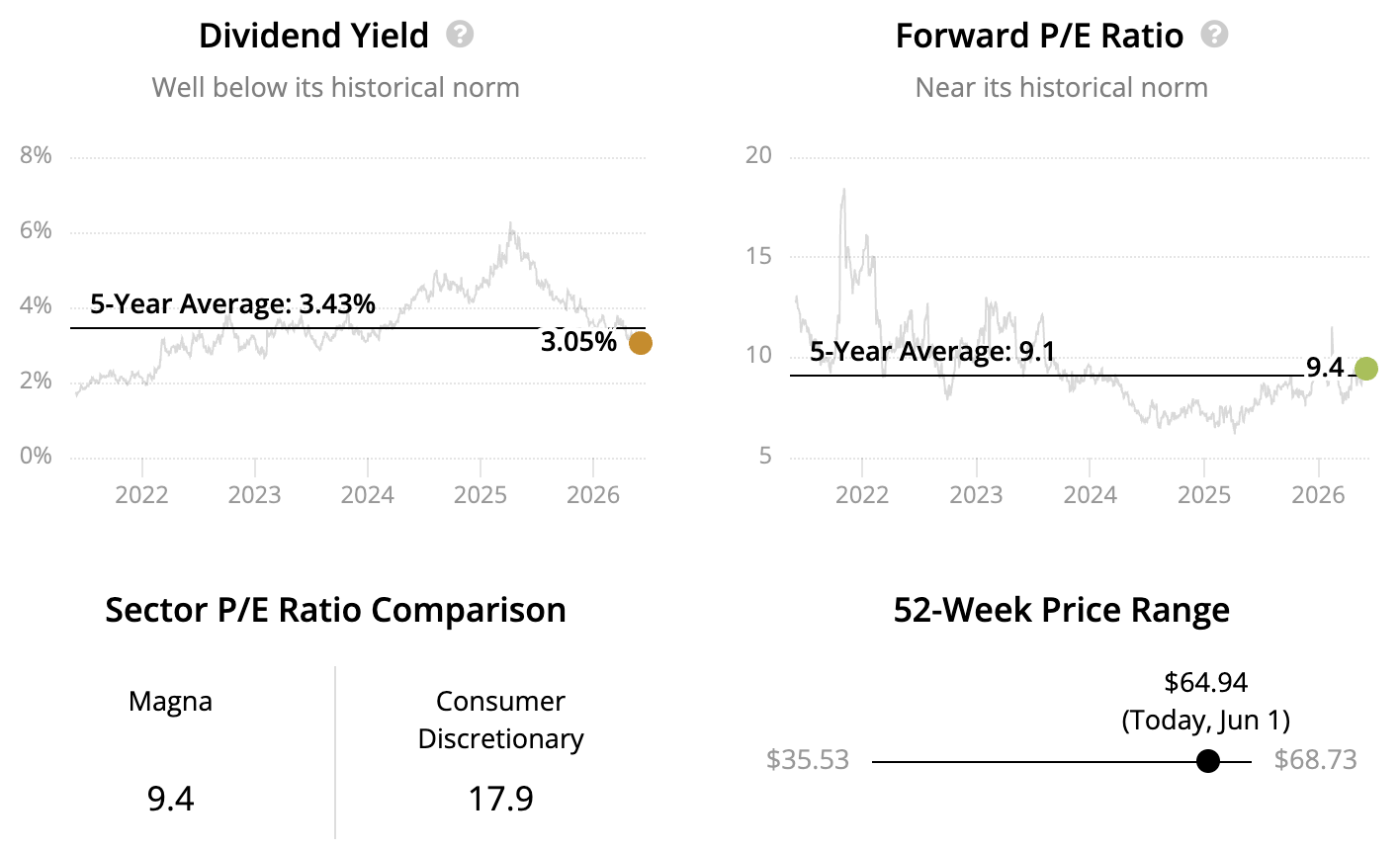

High Dividend Stock #17: Magna

Sector: Consumer Discretionary – Automotive Parts and Equipment

Dividend Yield: 3.1% Dividend Safety Score: Safe

Uninterrupted Dividend Streak: 15 years

Magna (MGA) is the world's third-largest auto parts supplier. This tough industry is characterized by thin margins and cyclical demand trends tied to vehicle production volumes and is suitable only for long-term investors.

Source: Magna

Magna's shares slumped under pressure from inflation and higher interest rates, which dampened demand for new vehicles. A slowdown in electric vehicle (EV) adoption has also reduced the near-term returns Magna can earn on its investments in developing new EV components, such as powertrain electrification and advanced driver-assistance systems. Increased competition from Chinese suppliers has also weighed on performance.

Despite these real challenges, Magna stands out in the group because of its conservative management. The company prioritizes maintaining an A- credit rating, does not overly depend on any single vehicle manufacturer (General Motors is the largest customer at 15% of sales), and has a well-diversified product portfolio that is mostly agnostic to engine types (seats, mirrors, and body structures are used in both electric vehicles and cars with internal combustible engines).

Industry conditions could worsen, especially if the economy tips into recession. But taking a three- to five-year view, we'd bet that Magna's profitability will strengthen and EV adoption will increase.

Magna cut and then suspended its payout during the 2008 financial crisis, but we think it would take a similarly severe downturn to jeopardize Magna's dividend today. Hopefully, that's an unlikely scenario since most of its auto customers are on much stronger financial ground today.

Investors who are comfortable with the firm's cyclical performance and want exposure to the auto industry may find Magna an interesting option without betting on a specific car brand or having to worry about a company's ability to survive a downturn. Just keep in mind that the industry's tough times can always get worse before they get better.

Source: Simply Safe Dividends

Note that as a Canadian company, dividends paid by Enbridge to U.S. investors are subject to a 15% withholding tax. Investors can avoid this tax by holding Enbridge in retirement accounts. Otherwise, with some additional paperwork, investors can generally claim a tax credit with the IRS to offset the withholding tax.

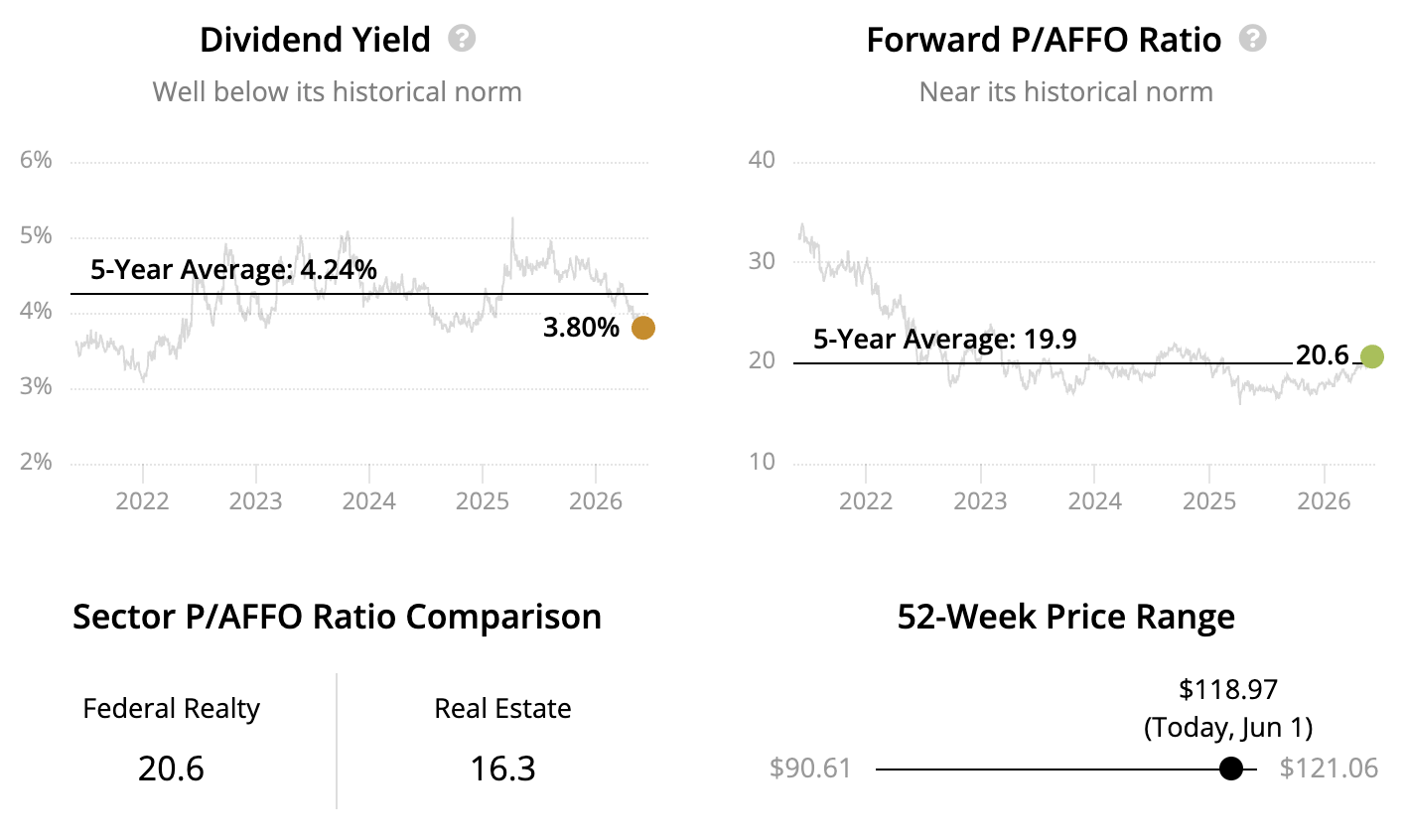

High Dividend Stock #16: Federal Realty

Sector: Real Estate – Retail REITs Dividend Yield: 3.8% Dividend Safety Score: Safe Uninterrupted Dividend Streak: 63 years

Federal Realty (FRT) owns more than 100 open‑air shopping centers and mixed‑use campuses clustered in affluent, land‑constrained coastal markets such as Silicon Valley, Washington DC, Boston, and New York.

Three out of every four properties include a high‑performing grocer, and roughly one‑quarter of rent comes from on‑site apartments and offices. These complementary uses keep foot traffic steady for the REIT's 3,000‑plus retail tenants, which range from restaurants and gyms to pharmacies and home‑goods stores.

Source: Federal Realty

No single tenant contributes more than 3% of revenue, and no metro area tops one‑third, giving FRT a well‑diversified cash flow stream.

Most leases run on a triple‑net basis, pushing taxes, insurance, and maintenance costs to tenants and leaving Federal Realty with high‑margin, predictable rent.

By steadily adding apartments, hotels, and offices to select centers, management further boosts property values and makes the surrounding retail space more attractive, supporting above‑average rent growth that has historically outpaced peers.

Prudent capital allocation is another hallmark. A BBB+ credit rating, reasonable payout ratio near 80%, and a disciplined development pipeline provide flexibility to weather economic slowdowns.

Those strengths underpin a dividend that has grown every year since 1967— the longest streak among REITs—and should keep FRT a reliable high dividend stock for investors comfortable with brick‑and‑mortar retail's slow evolution in the e‑commerce age.

Source: Simply Safe Dividends

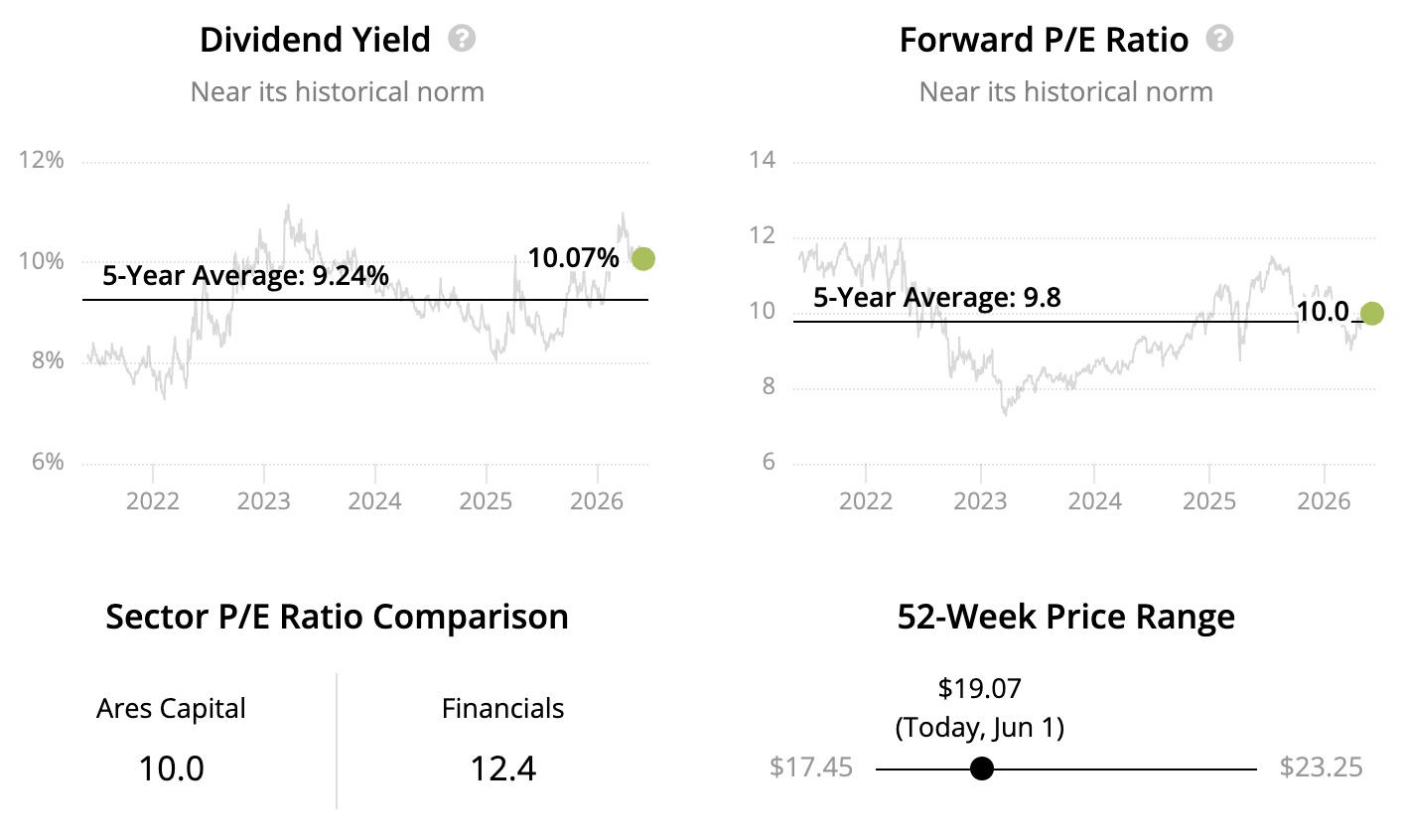

High Dividend Stock #15: Ares Capital

Sector: Financials – Business Development Companies

Ares Capital (ARCC) formed in 2004 when alternative investment manager Ares created the firm to engage in corporate lending activities. Today, Ares Capital is the largest business development company (BDC) in America.

Source: Ares Capital

As a BDC, Ares Capital provides high-yield loans to relatively small, highly levered companies that can't access traditional financing from banks.

This is a risky, cyclical industry. But Ares Capital represents one of the best high dividend stocks in the space thanks in part to its size.

As the biggest BDC, Ares Capital's vast capital base enables the company to serve businesses of all sizes and provide financing over a firm's entire life cycle, creating longer-term relationships.

Ares Capital's large size also makes it easier to maintain a well-diversified portfolio. The BDC's investments span more than 400 companies, none greater than 3% of the portfolio. This reduces the firm's dependence on any single investment.

Management targets less cyclical businesses as well, focusing on service-oriented companies that generate steady cash flow, such as software and health care.

The portfolio's risk is further reduced by Ares Capital's focus on first-lien secured loans, which account for around half of the BDC's investments and get paid first when a borrower defaults. This reduces the chance of major loan losses during downturns.

Ares Capital also uses less leverage than is allowed by regulators, earning the firm a BBB credit rating.

These qualities have helped Ares Capital pay steady dividends since its founding in 2004, with the only blemish being a 17% dividend cut in 2009 when management opted to strengthen the balance sheet in the face of uncertain credit market conditions.

Ares Capital is bigger today with access to a wider variety of capital sources, providing more support for the dividend in future downturns. For investors seeking the highest paying dividend stocks, Ares Capital is a well-run BDC to consider, though it is not immune from the industry's cyclicality.

Source: Simply Safe Dividends

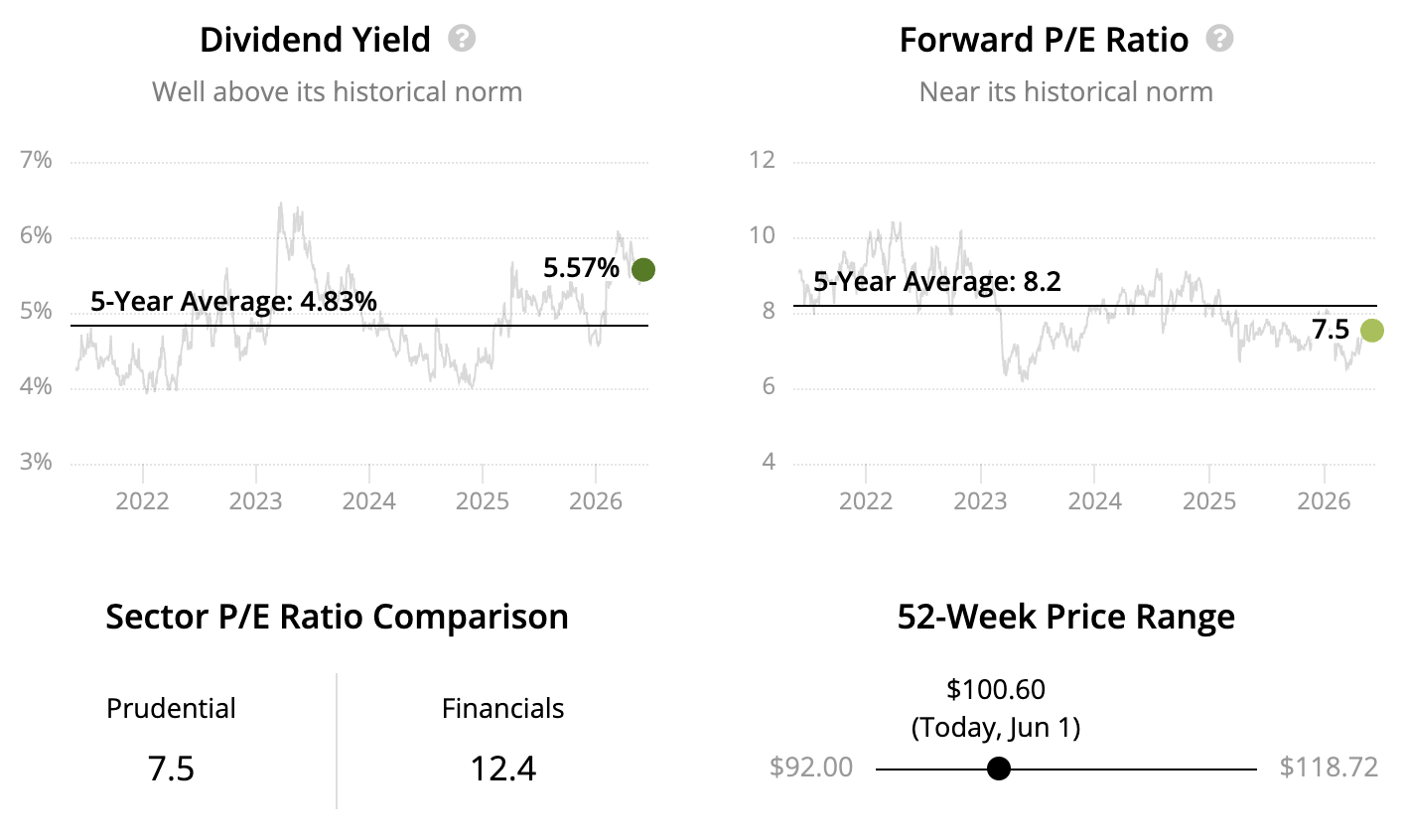

High Dividend Stock #14: Prudential

Sector: Financials – Life and Health Insurance Dividend Yield: 5.6% Dividend Safety Score: Safe Uninterrupted Dividend Streak: 16 years

Prudential Financial (PRU) was founded in 1875 amid the Panic of 1873, which devastated the railroad industry and led to widespread bank failures and the collapse of many life insurers. Founder John F. Dryden aimed to serve the working class, a market largely ignored at the time, by offering affordable burial insurance.

Source: Prudential

Since its inception, Prudential has evolved into a major life insurer in the U.S. and Japan, also offering annuities, mutual funds, and investment management. The company's conservative business approach has enabled it to maintain a strong balance sheet and exceed regulatory capital requirements, helping it navigate financial crises and maintain its industry leadership.

Prudential's business is naturally sensitive to capital market fluctuations. Life insurers and annuity providers must make assumptions about future market returns and interest rates, with adverse deviations potentially forcing them into riskier investments or increased leverage. During the 2007-09 financial crisis, Prudential cut its dividend to preserve its investment-grade credit rating due to losses in mortgage-backed securities.

Recently, Prudential has worked to decrease its market sensitivity by modifying annuity products and focusing on simpler life insurance policies. This strategy aims to stabilize earnings and sustain its history of uninterrupted dividends. The firm is also expanding its less rate-sensitive investment management business and growing its presence in high-growth markets in Asia and Latin America.

Prudential's robust financial foundation and strategic adjustments position it well to continue as an industry leader, adapting effectively to industry cycles and expanding its global footprint.

Source: Simply Safe Dividends

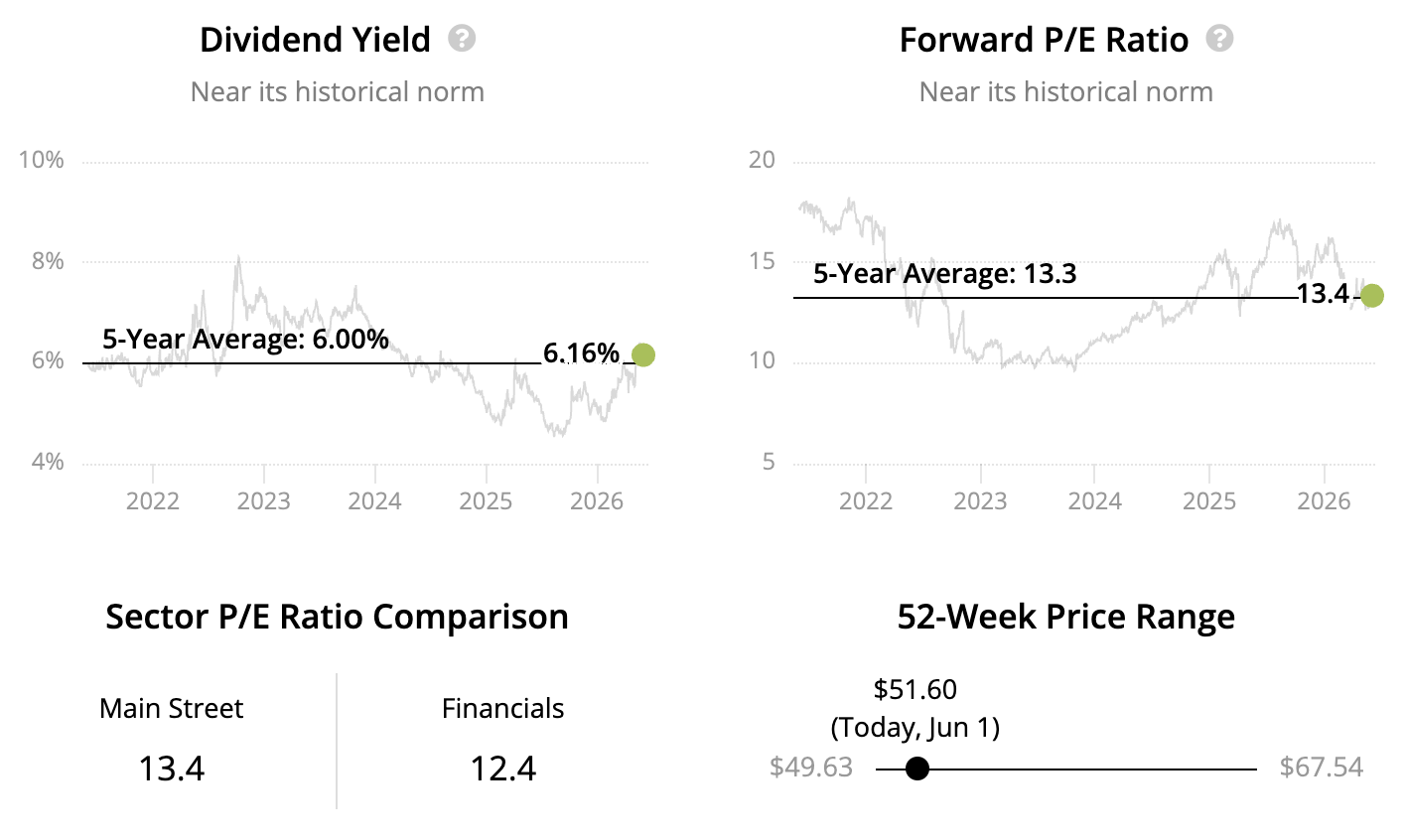

High Dividend Stock #13: Main Street Capital

Sector: Financials – Business Development Companies Dividend Yield: 6.2% Dividend Safety Score: Safe Uninterrupted Dividend Streak: 18 years

Main Street Capital (MAIN), founded in Texas in 1997, is one of the oldest and largest business development companies (BDCs) in the industry. The stock is also the only monthly dividend payer on our list.

As a BDC, Main Street provides debt and equity capital to relatively small, highly leveraged companies that can't tap traditional financing from banks.

This is a cyclical business since loan defaults spike during economic downturns. Paired with the high leverage and aggressive payout ratios maintained by most BDCs, few firms have shown an ability to defend their dividends when the tide goes out.

Main Street is an exception. The firm has never reduced its regular dividend since making its first payout in 2007, a stretch that includes two recessions.

To keep its high dividend safe, Main Street maintains a well-diversified loan portfolio with around 150 companies represented.

No investment tops 5% of the portfolio's income, and industry exposures are kept beneath 10% of the portfolio's value. This provides protection from distress at any single company or sector.

Source: Main Street

Main Street focuses on first-lien secured loans as well. This debt is paid back first in the even of a default, reducing the potential for major loan losses during recessions.

Management also runs the business with much less debt than regulators allow, helping the firm earn a BBB- credit rating.

That said, investors considering Main Street for its high dividend need a strong stomach for volatility given the risks associated with its investments in subprime debt securities. But Main Street is arguably the most conservative high dividend stock in the industry.

Source: Simply Safe Dividends

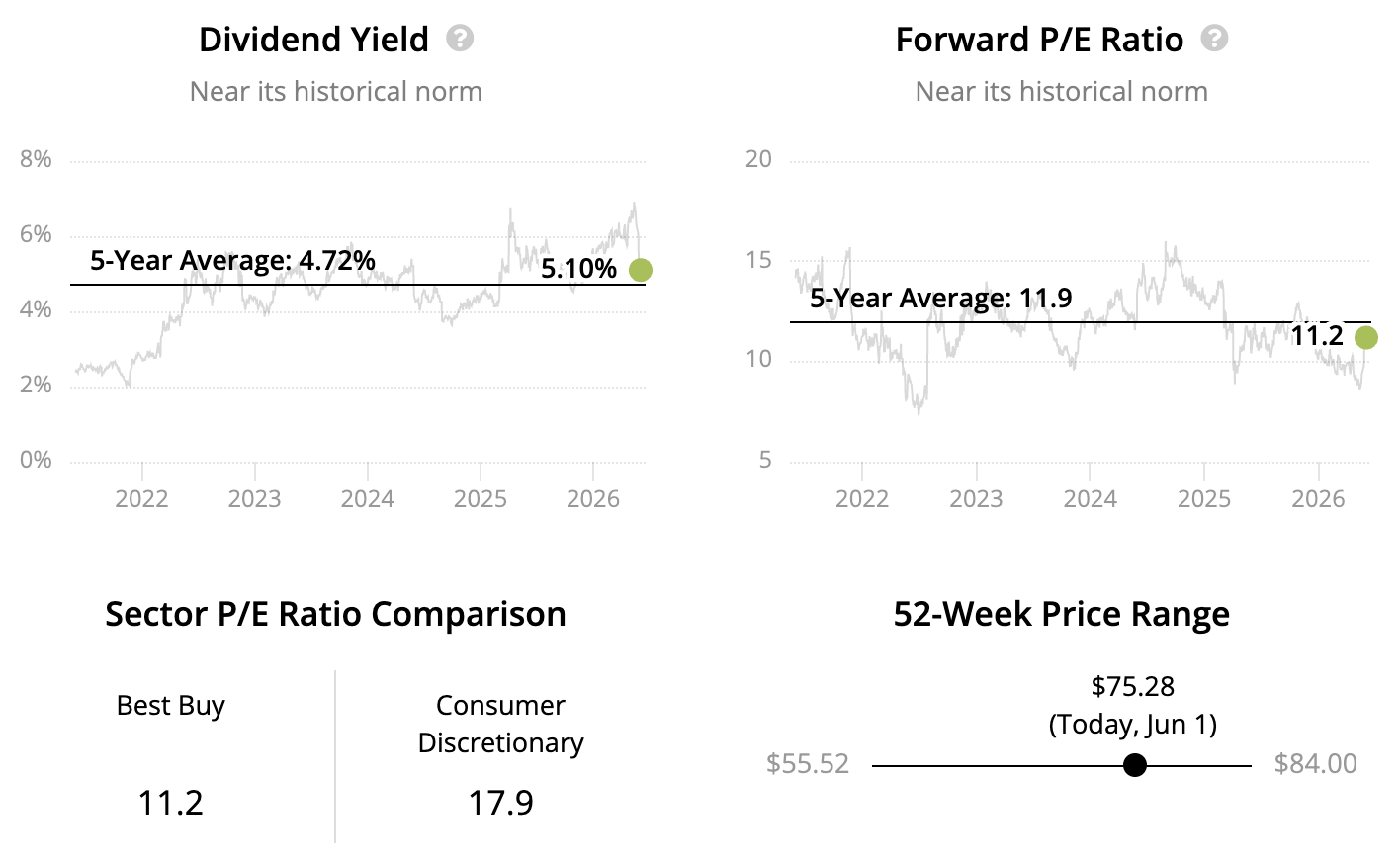

High Dividend Stock #12 Best Buy

Sector: Consumer Discretionary – Computer and Electronics Retail

Founded in 1966 as a small electronics shop focused on stereos, Best Buy (BBY) now has more than 900 stores selling computers, mobile phones, digital cameras, home theater systems, appliances, and more.

Source: Best Buy

Best Buy enjoys a leadership position as America's last remaining national brick-and-mortar electronics retailer. Although the convenience and price competitiveness of online shopping have put many retailers out of business, many customers still prefer an in-store experience.

Knowledgeable employees can help shoppers make better-informed buying decisions, especially for pricey, experiential purchases like home theater systems. And for some consumers, there's added comfort in buying electronics from a trusted source with tech-support options.

Additionally, Best Buy's price match guarantee, online presence (e-commerce now accounts for 30% of U.S. sales), and fast shipping options (over 70% of Americans live within 10 miles of a Best Buy store) have narrowed its online peers' competitive advantages.

Along with the firm's BBB+ credit rating and solid free cash flow generation with few new big-box stores being opened, Best Buy should remain a reliable stock paying high dividends.

Source: Simply Safe Dividends

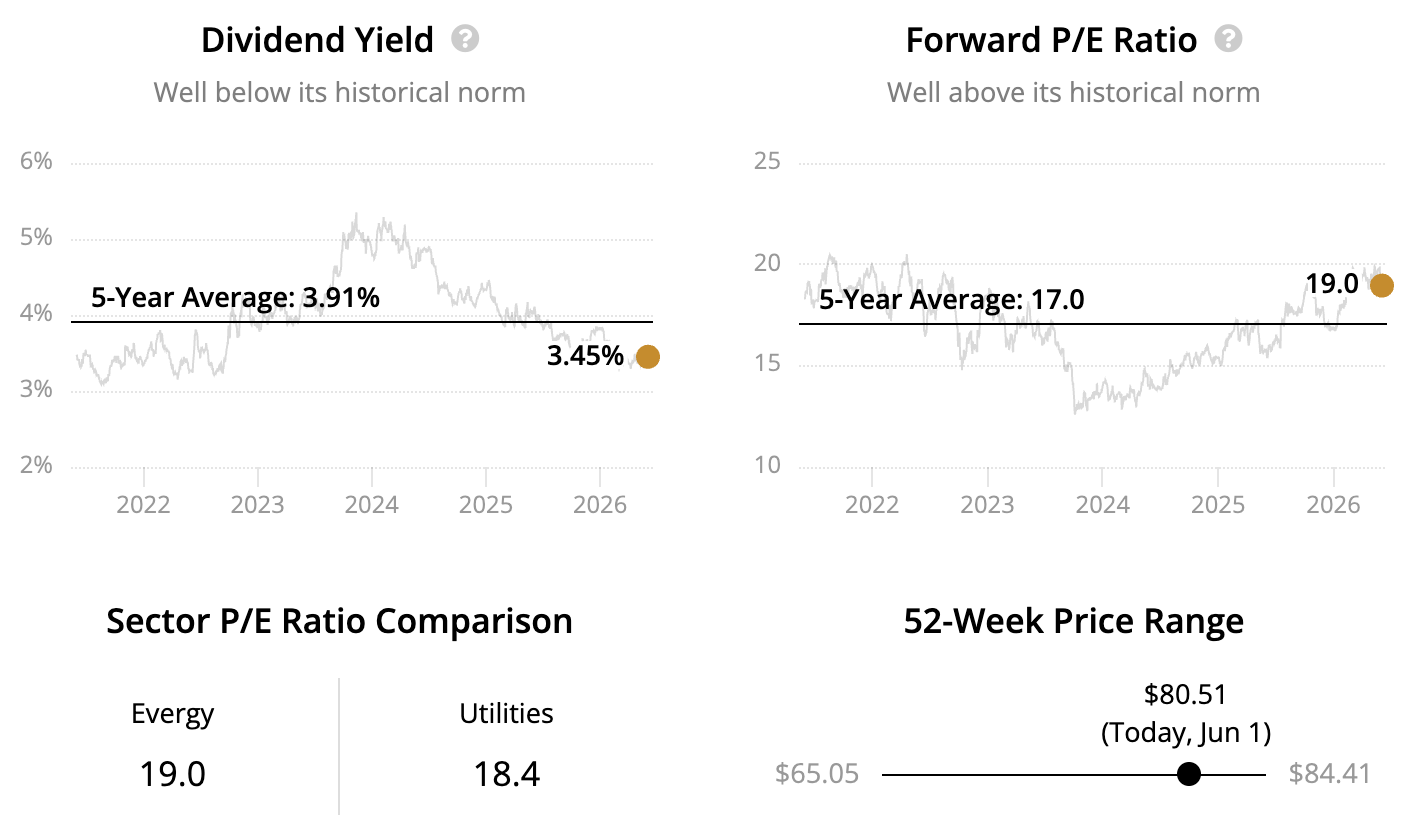

High Dividend Stock #11: Evergy

Sector: Utilities – Electric Utilities

Dividend Yield: 3.5% Dividend Safety Score: Very Safe

Uninterrupted Dividend Streak: 22 years

Evergy (EVRG) is a regulated utility serving Kansas and Missouri, formed in 2018 through the merger of Westar Energy and Kansas City Power and Light. With over a century of service, the company generates stable, predictable earnings primarily from regulated operations.

Source: Evergy

While recent regulatory oversight has been less constructive, leading to a reduction in Evergy’s long-term earnings growth target to 4% to 6%, we view this as a short-term hurdle. The Kansas City area’s economic growth, driven by developments like Google’s data center and Panasonic’s electric vehicle battery plant, continues to drive above-average electricity demand.

Meeting this growth, along with Evergy's clean energy initiatives, will require substantial investment. Over time, regulatory dynamics are expected to normalize to support this critical infrastructure development.

Meanwhile, Evergy’s BBB+ credit rating and mid-single-digit annual growth outlook provide a solid foundation for long-term investors seeking stability and income.

Source: Simply Safe Dividends

High Dividend Stock #10: Enterprise Products Partners

Sector: Energy – Oil and Gas Storage and Transportation

Dividend Yield: 5.9% Dividend Safety Score: Safe

Uninterrupted Dividend Streak: 26 years

Enterprise Products Partners (EPD) began in 1968 as a wholesale marketer of natural gas liquids and has expanded over the decades to become one of the largest master limited partnerships (MLPs) in America.

Energy producers depend on the partnership's network of pipelines, processing plants, storage facilities, and terminals to get raw fossil fuels from their wellheads to end consumers in a ready-to-use state.

Source: Enterprise Product Partners

With hard-to-replicate assets connected to nearly every major U.S. shale basin, Enterprise enables many energy producers to enter a single relationship to move their products to downstream buyers.

These essential services, backed by long-term, fixed-fee contracts with minimum volume guarantees, have insulated Enterprise's cash flow from volatile oil and gas prices over the years.

Coupled with a A- credit rating, self-funded business model, and diversified base of customers working with a variety of commodities, Enterprise has paid higher distributions every year since going public in 1998.

As long as fossil fuels remain an important component of the world's energy mix, Enterprise's high yield should continue to be a good bet for investors who are comfortable with investing in MLPs and receiving the K-1 forms they send at tax time.

Source: Simply Safe Dividends

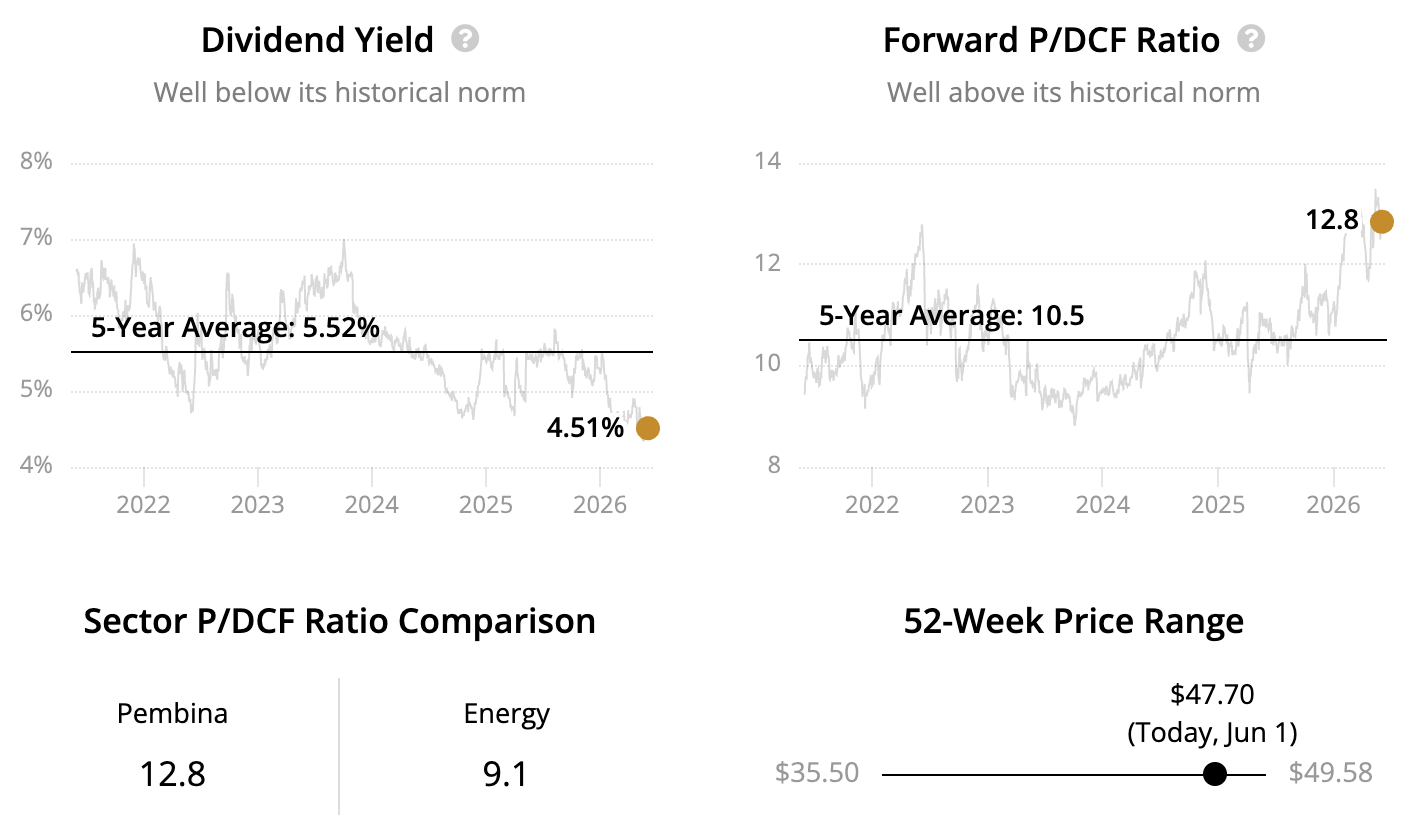

High Dividend Stock #9: Pembina Pipeline

Sector: Energy – Oil and Gas Storage and Transportation

Dividend Yield: 4.5% Dividend Safety Score: Safe

Uninterrupted Dividend Streak: 29 years

Founded in Alberta's Pembina oilfield in 1954, Pembina Pipeline (PBA) provides midstream services throughout western Canada. The company's infrastructure consists primarily of oil and gas pipelines, storage facilities, and processing plants.

Source: Pembina Pipeline

Pembina's network of assets acts as a one-stop shop for energy producers to help move their oil, gas, and natural gas liquids from Canada to the highest value markets worldwide.

This essential business generates stable revenue from fee-based activities backed by long-term contracts with minimum volume protections, insulating cash flow from volatile energy prices.

Management runs the company conservatively as well, with Pembina earning a BBB credit rating and maintaining a self-funded business model that requires no equity issuances to fund growth.

In addition to its well-supported payout, Pembina appeals to income investors thanks to the firm's unblemished track record of no dividend cuts since going public in 1997.

Source: Simply Safe Dividends

Note that as a Canadian company, dividends paid by Enbridge to U.S. investors are subject to a 15% withholding tax. Investors can avoid this tax by holding Enbridge in retirement accounts. Otherwise, with some additional paperwork, investors can generally claim a tax credit with the IRS to offset the withholding tax.

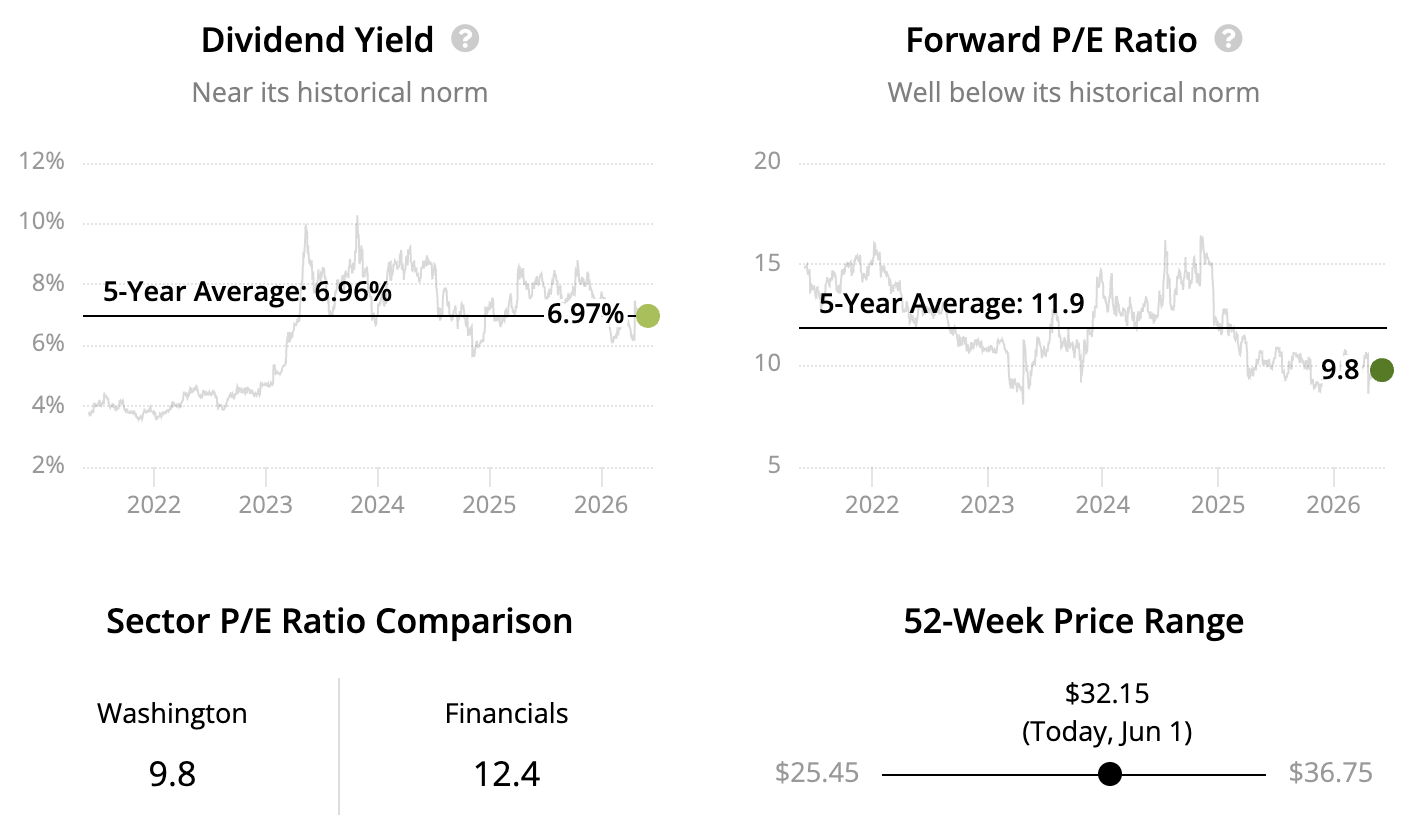

Washington Trust (WASH), a Rhode Island-based community bank founded in 1800, saw its share price drop nearly 50% over the past three years — driven by falling profitability, balance sheet missteps, and shaken investor confidence.

These challenges, while real, aren't necessarily permanent. The small-cap bank has a strong long-term record, including resilient credit performance, over 30 years of uninterrupted dividends, and past outperformance of the financials sector.

Source: Washington Trust Presentation

The Fed's rapid rate hikes in 2022-23 pressured Washington Trust’s net interest margin, as it was stuck with low-yielding assets while funding costs surged.

Earnings fell sharply, and the payout ratio jumped to 95% in 2024. To reverse course, the bank sold low-return assets at a loss, reinvested in higher-yielding securities, cut back on expensive funding, and raised equity to cover a $70 million loss — moves that diluted shareholders and dented credibility.

Still, these actions expanded the bank's margin and brought capital levels near 20-year highs, providing a solid buffer against future credit losses.

The payout ratio is expected to improve to about 65% in 2026, too. Further Fed rate cuts would aid dividend sustainability, pushing coverage closer to the historical norm of 50%.

With a dividend yield north of 6% that has some support behind it, a conservative lending approach, and steady fee revenue from wealth management operations, Washington Trust offers potential for income-focused investors who can stomach short-term volatility and believe in a longer-term margin recovery.

Source: Simply Safe Dividends

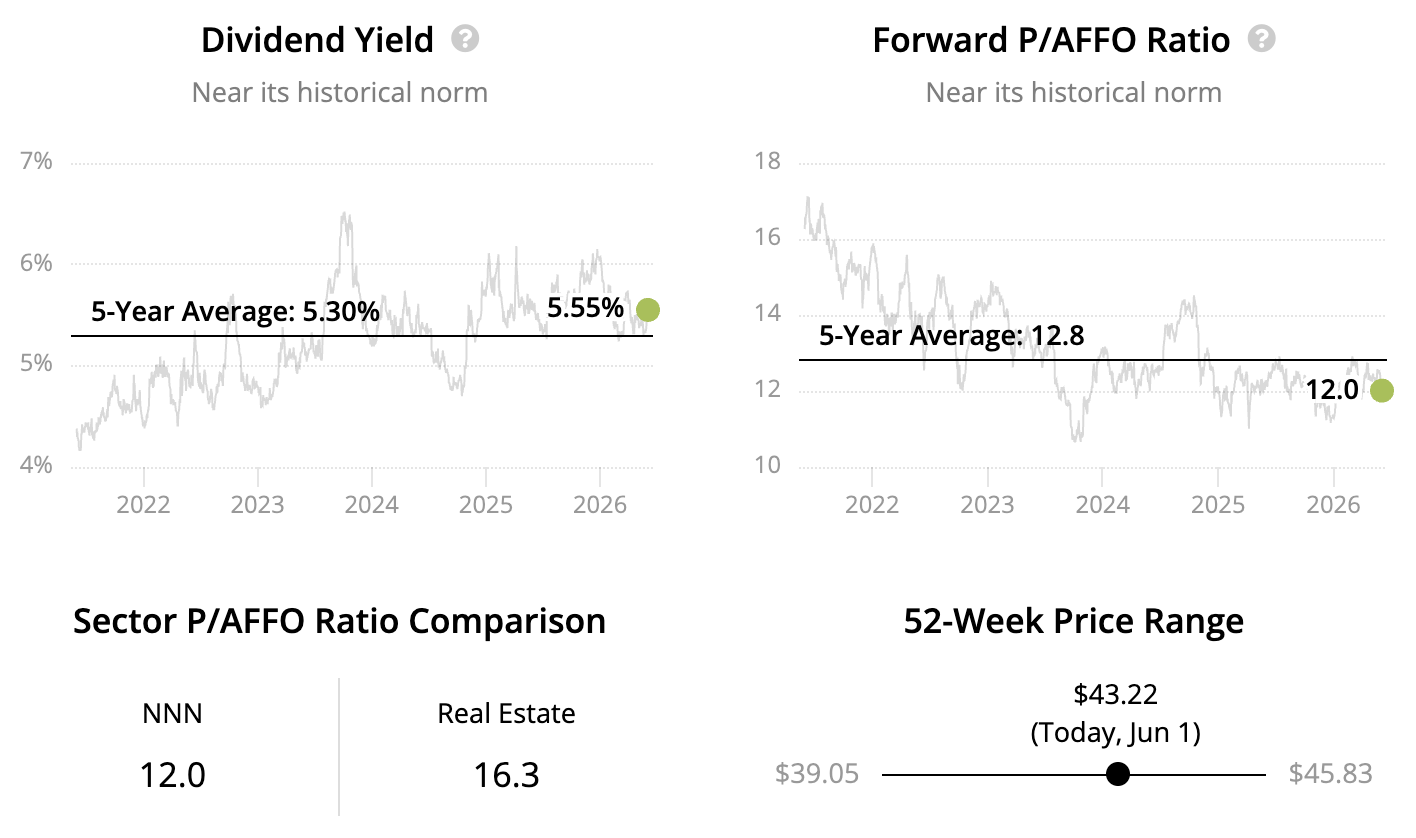

High Dividend Stock #7: NNN

Sector: Real Estate – Retail REITs

Dividend Yield: 5.6% Dividend Safety Score: Safe

Uninterrupted Dividend Streak: 37 years

NNN REIT (NNN), formerly known as National Retail, began in 1984 when restaurant chain Golden Corral formed a REIT to acquire its properties and lease them back. Today, NNN owns over 3,000 single-tenant, freestanding properties across America, leased to more than 350 tenants in over 30 industries.

Source: NNN

The retail REIT has delivered predictable results for decades, thanks in part to its triple-net leases that require tenants to pay for insurance, maintenance, utilities, and property taxes. NNN thus serves purely as a landlord, collecting a recurring stream of high-margin rent.

The REIT's cash flow stream is further protected by a well-diversified portfolio. No industry exceeds 20% of rent, no tenant tops 5% of rent, and the portfolio is spread across the U.S. with no major geographic concentration.

Management has also prioritized avoiding retail categories that are most susceptible to the threat posed by e-commerce, such as departments and malls.

Experiential or service businesses such as convenience stores, automotive service, restaurants, gyms, and entertainment centers are the REIT's largest exposures and drive around 60% of rent.

These traits have helped NNN maintain high occupancy rates and stable cash flow over time, enabling shareholders to enjoy higher dividends each year since 1990.

With a diversified property portfolio, BBB+ credit rating, and conservative payout ratio policy, the company's high dividend seems likely to remain safe and growing for years to come.

Source: Simply Safe Dividends

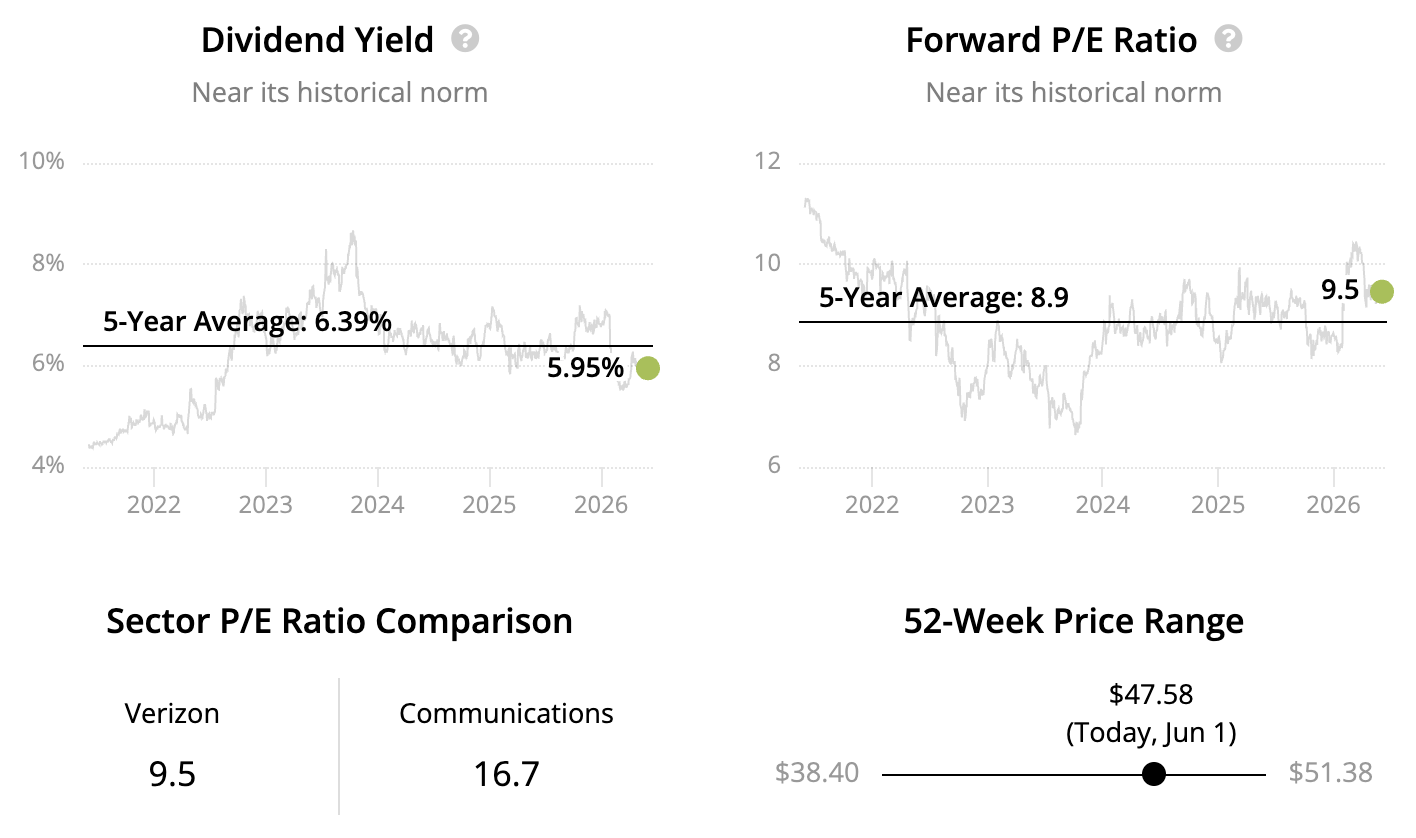

High Dividend Stock #6: Verizon

Sector: Communications – Wireless and Internet Services

Verizon (VZ) formed in 2000 when Bell Atlantic and GTE merged, creating America's largest wireless company. Wireless services continue to generate nearly all of Verizon's profits today.

Source: Verizon

This capital-intensive business has high barriers to entry. Verizon, AT&T, and T-Mobile dominate the industry with massive subscriber bases, which provide the cash flow necessary to maintain their nationwide networks.

Verizon historically maintained superior network reliability, speed, and performance, allowing the telecom giant to charge premium rates and enjoy lower churn.

But there is now far more network coverage parity between the major telecoms. Coupled with a saturated smartphone market and more aggressive promotions from AT&T and T-Mobile, this has made for a challenging competitive environment.

Verizon's high yield reflects the company's more muted subscriber growth in the recent years. The firm has also had to invest heavily in next-generation network technologies such as 5G, resulting in higher debt and uncertain returns as growth opportunities such as 5G home internet and higher plan rates remain fuzzy.

That said, Verizon and its predecessors have paid uninterrupted dividends since 1984, a streak that seems likely to continue.

The BBB+ rated company maintains a healthy payout ratio under 60% and will retain more free cash flow in the years ahead as 5G network spending peaked in 2022.

This will enable deleveraging and support Verizon's high dividend for investors who believe in the firm's recession-resistant services and staying power.

Source: Simply Safe Dividends

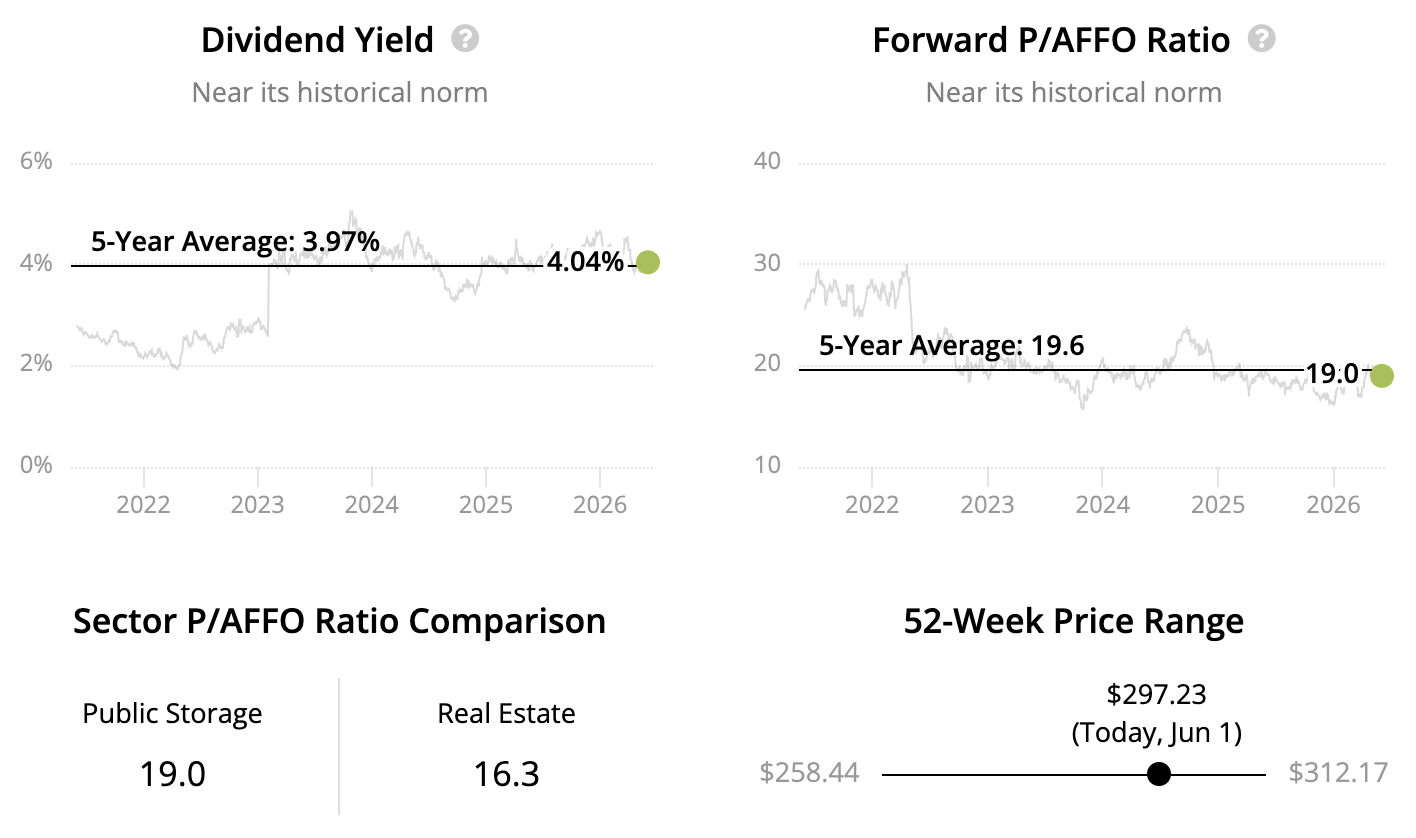

High Dividend Stock #5: Public Storage

Sector: Real Estate – Self-Storage REITs

Dividend Yield: 4.0% Dividend Safety Score: Very Safe Uninterrupted Dividend Streak: 45 years

Public Storage (PSA) is the largest self-storage operator in the U.S. with over 3,000 locations concentrated in major metro areas. This recession-resistant business generates steady cash flow because people need storage during all of life's transitions, and once they've moved in, few are eager to relocate just to save a few dollars. These qualities have helped Public Storage pay uninterrupted dividends for more than 40 years.

From 2020 to 2023, low interest rates and surging demand led to a wave of new self-storage construction, mostly by smaller developers chasing short-term profits. While Public Storage's urban footprint is better protected by strict zoning and high land costs, the industry still saw oversupply in suburban areas, which weighed on pricing and occupancy.

That headwind has caused shares to stagnate and trade below their long-term average cash flow multiple. But new construction is now falling sharply as higher interest rates and tougher economics push marginal players out of the market. As the cycle resets, Public Storage's scale, efficiency, and prime locations should stand out.

Importantly, the company is also well positioned for whatever happens next in the housing market. If the housing shortage persists, people will continue to need storage as they live in smaller or temporary spaces. If housing activity rebounds, more moving will create short term demand. Either way, storage demand should stay resilient.

With an A rated balance sheet and a long runway to keep consolidating a fragmented industry, Public Storage remains one of the most durable income compounders in real estate.

Source: Simply Safe Dividends

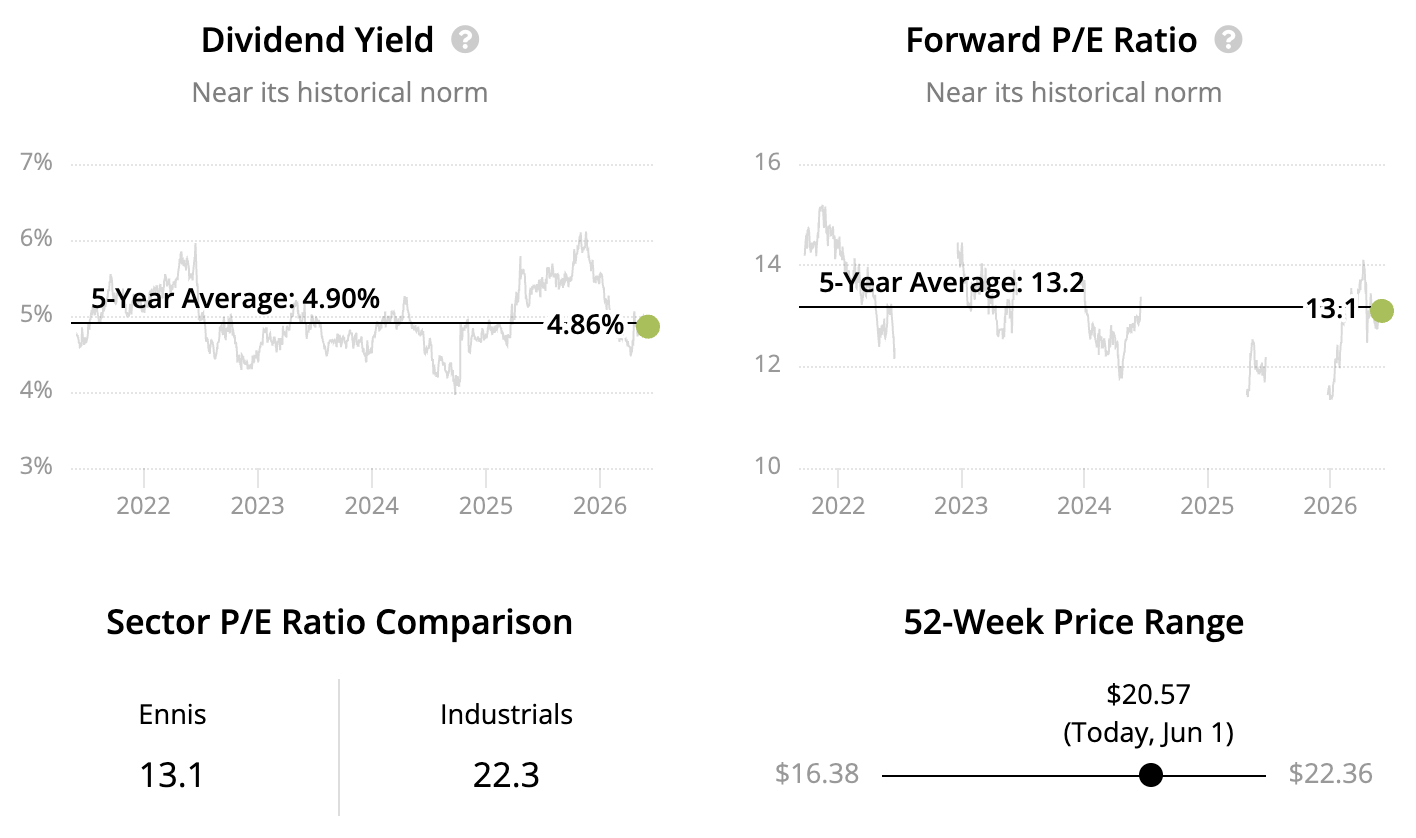

Founded in 1909 as a single print shop in Texas, Ennis (EBF) is the largest provider of business forms, labels, tags, envelopes, and presentation folders to independent distributors in the U.S.

Source: Ennis

Many print-based products have been in decline for decades as cost-effective electronic distribution of documents and other customer communications have driven an increasingly paperless business environment.

Ennis has navigated these challenges in part by acquiring smaller rivals to ensure it maintains the widest variety of products and capabilities in the industry.

The company has also carved out a niche in products that are tailor-made to a customer's specifications for size, color, number of parts, and quantities. These custom and semi-custom products account for over 90% of the business.

With leading scale and geographic reach, and as the industry's only major wholesale left, Ennis enjoys sticky relationships with customers such as print distributors, commercial printers, direct mail companies, and ad agencies.

While the broader industry may continue to gradually contract, Ennis sees growth opportunities as major direct manufacturers abandon older product lines as they redefine their business models.

The company's largest distributors have also had more success capturing business from Fortune 500 companies, who previously were only willing to buy from direct manufacturers such as Staples before the pandemic disrupted supply chains.

With consistent free cash flow generation and a debt-free balance sheet, Ennis remains well positioned to continue consolidating the industry with acquisitions to offset industry revenue declines, too.

Ennis may not have an attractive growth profile, but the firm has paid reliable dividends every year since 1973. The high-yielding stock may appeal to income investors who are comfortable owning a relatively small company that has historically delivered safe payouts with little excitement.

Source: Simply Safe Dividends

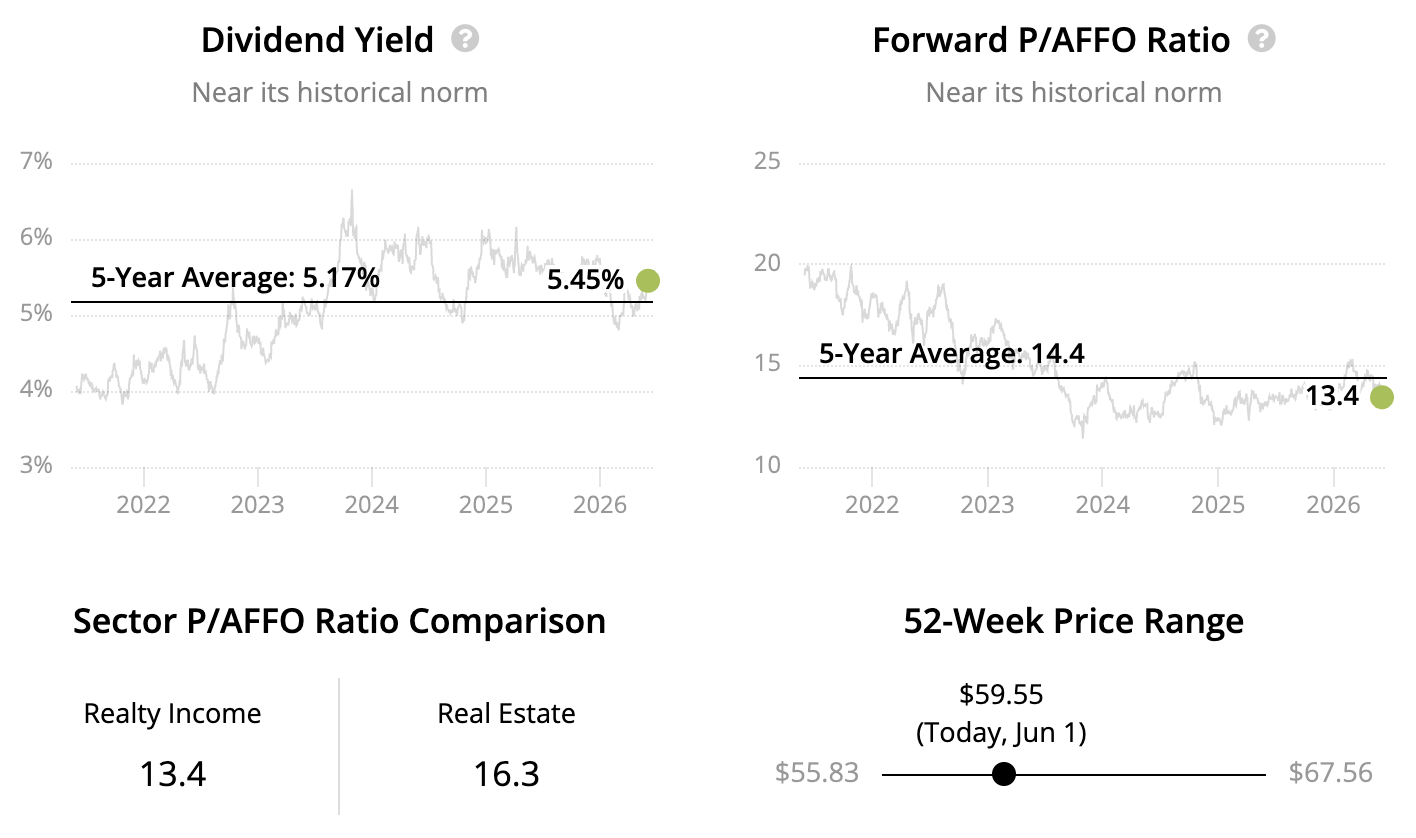

High Dividend Stock #3: Realty Income

Sector: Real Estate – Retail REITs Dividend Yield: 5.5% Dividend Safety Score: Safe Uninterrupted Dividend Streak: 56 years

Realty Income (O) got its start in 1969 with a single investment in a Taco Bell and has paid uninterrupted dividends since its founding.

Today, the REIT owns thousands of retail properties across the U.S. that are leased to hundreds of tenants operating in dozens of industries.

Realty Income generates predictable cash flow thanks to the structure of its leases, which span long durations and shift property operating expenses (maintenance, utilities, taxes, etc) to tenants.

Coupled with a focus on quality locations, a key success factor in retail, Realty Income's occupancy rate has never fallen below 96%, even during the financial crisis and pandemic.

The A- rated company's results are further insulated by its diversified lineup of tenants. No single tenant exceeds 5% of rent, and no industry tops 15% of rent. Realty Income focuses on more durable tenants that have a service, non-discretionary, or low price point element to their business as well.

Source: Realty Income

While Realty Income's growth will never be fast, the highly fragmented single-tenant retail property market provides a long runway for expansion opportunities. This should keep the REIT's monthly dividend safety and growing.

Source: Simply Safe Dividends

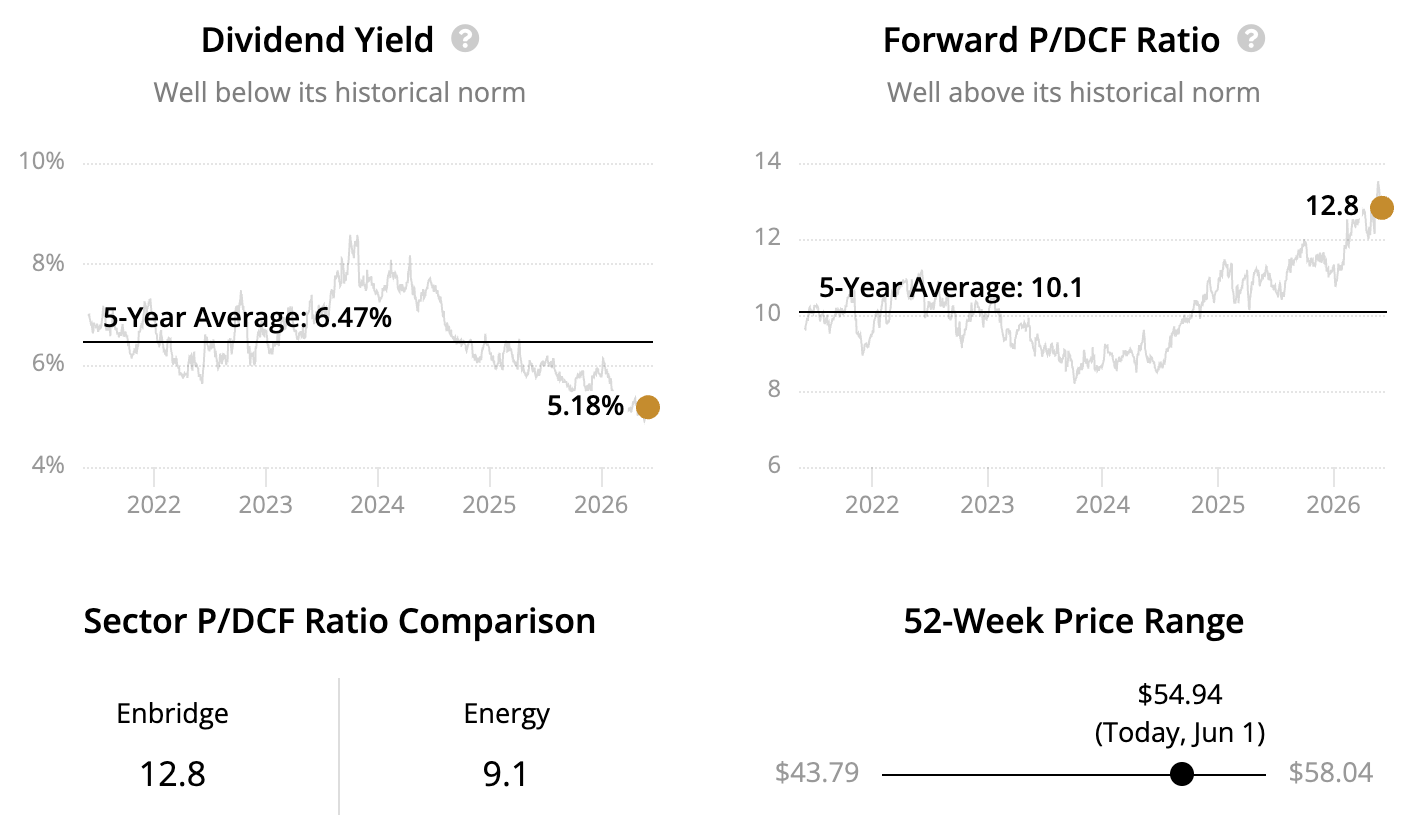

High Dividend Stock #2: Enbridge

Sector: Energy – Oil and Gas Storage and Transportation

Established in 1949, Enbridge (ENB) is the largest midstream company in North America with a network of pipelines, terminals, storage facilities, and processing plants connecting the continent's most vital energy-producing regions.

Source: Enbridge

The economy could not function without Enbridge's energy infrastructure. For example, the firm moves around 30% of the crude oil produced in North America and transports almost 20% of the natural gas consumed in the U.S.

In addition to the essential nature of its services, Enbridge generates nearly all of its revenue from long-term contracts with fixed fee provisions and often minimum volume commitments, resulting in minimal direct exposure to commodity prices.

Furthermore, the firm has expanded its regulated income portfolio to provide even more reliable earnings, accounting for around 20% of profits.

This annuity-like business model results in a steady cash flow stream that has helped Enbridge pay stable or higher dividends every year since 1953.

The company's impressive dividend track record also reflects management's conservative approach to running the business. Enbridge maintains a BBB+ credit rating, has a self-funded business model which requires no equity issuances to fund growth, and does not depend on any single supply basin.

As one of the best-run midstream companies, Enbridge may appeal to high-yield investors who believe in the staying power of fossil fuels and the infrastructure necessary to help move them from energy producers to downstream consumers.

Source: Simply Safe Dividends

Note that as a Canadian company, dividends paid by Enbridge to U.S. investors are subject to a 15% withholding tax. Investors can avoid this tax by holding Enbridge in retirement accounts. Otherwise, with some additional paperwork, investors can generally claim a tax credit with the IRS to offset the withholding tax.

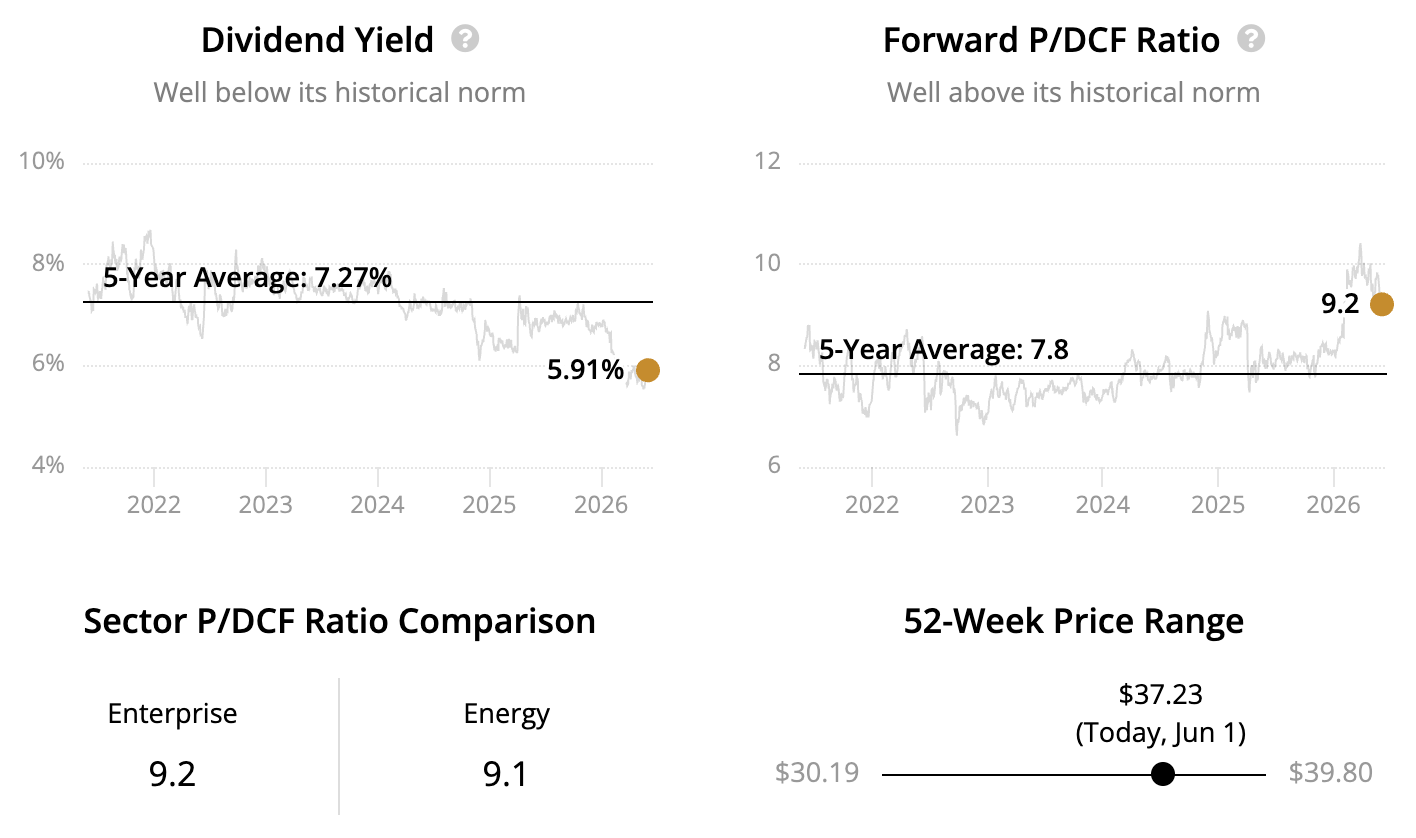

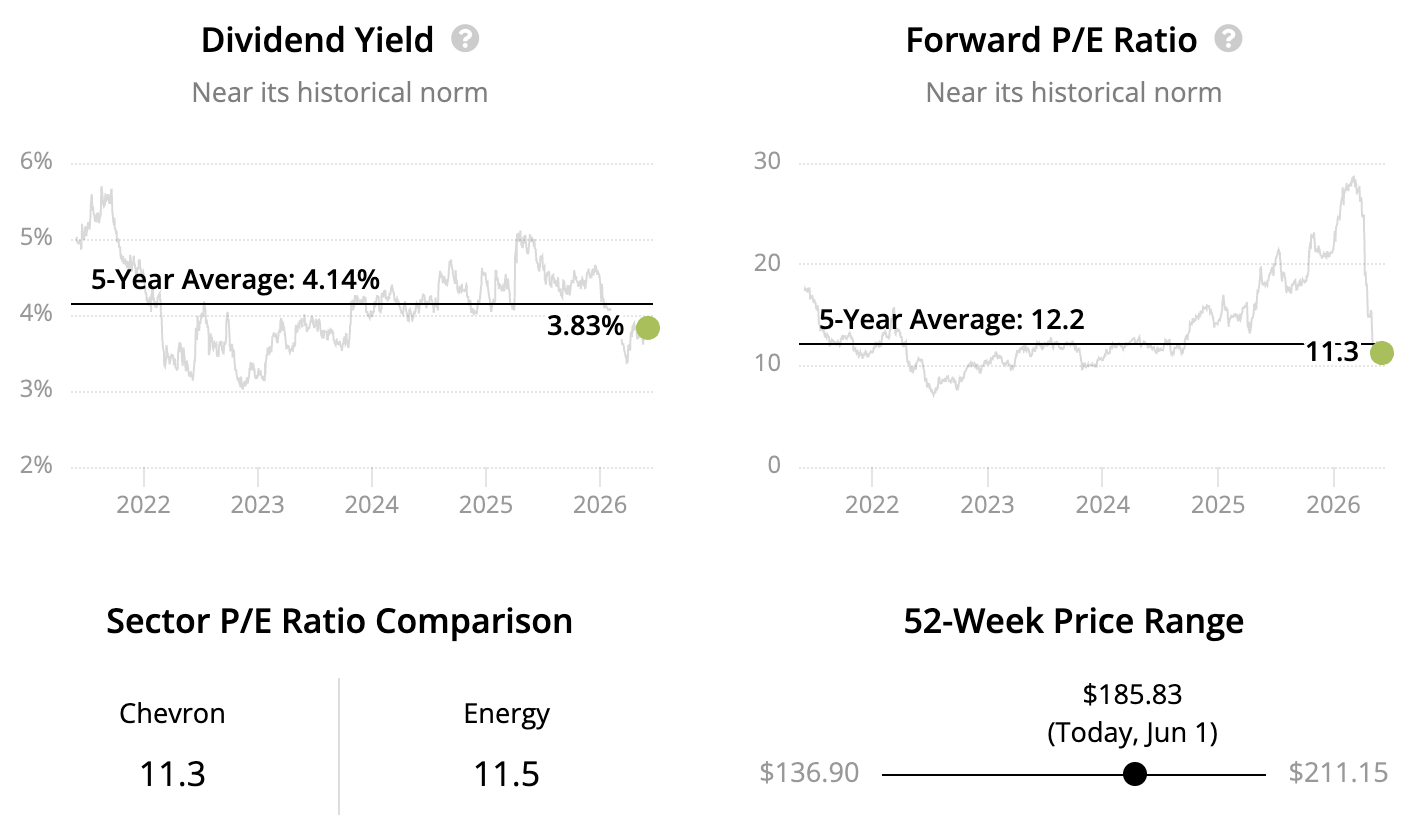

High Dividend Stock #1: Chevron

Sector: Energy – Integrated Oil and Gas Dividend Yield: 3.8% Dividend Safety Score: Very Safe Uninterrupted Dividend Streak: 114 years

Chevron (CVX) traces its roots to an 1879 oil strike near Los Angeles that produced just twenty five barrels a day. Fast‑forward to 2024, and the company pumps more than 1.5 million oil‑equivalent barrels daily from fields spread across six continents.

Upstream production remains its biggest earnings engine, but Chevron also runs refineries, chemical plants, and a large fuel retail network. This vertical integration steadies cash flow because low oil prices that hurt drilling margins typically improve downstream profits.

Scale and diversification give Chevron staying power. The portfolio ranges from West Texas shale wells with fast paybacks to decades‑long liquefied natural gas projects in Australia. Heavy oil, deepwater, pipelines, and petrochemicals add further balance, reducing reliance on any single region or commodity.

Source: Chevron

Management has a proven playbook of buying assets during industry slumps while keeping project spending in check. Capital outlays today run at roughly half the level seen a decade ago, holding the company’s break‑even oil price, or the level required to cover the dividend and essential capital spending, near $50 a barrel.

Financial strength is another edge. Chevron carries an AA credit rating and modest leverage, giving it room to fund dividends and opportunistic deals through commodity cycles. The firm and its predecessors have paid uninterrupted dividends since 1912 and raised the payout for over 35 straight years, a rarity in such a volatile business.

Investors who can tolerate the volatility of energy markets and want blue‑chip exposure to the sector may find Chevron's high dividend, conservative balance sheet, and diversified asset base a compelling combination.

Source: Simply Safe Dividends

Closing Thoughts on High Dividend Stocks

The highest-paying dividend stocks appeal to investors seeking current income, but many sky-high yields end up being too good to be true.

Maintaining a well-diversified portfolio and focusing on high-quality companies with strong financial health can help avoid the potential pitfalls of this strategy.

By the way, many of the investors interested in high dividend stocks are retirees looking to generate dependable income from dividend stocks.

If that sounds like you, you might enjoy trying our online product, which lets you track your portfolio's income, dividend safety, and more.

You can learn more about our suite of portfolio tools and research for dividend investors by clicking here. Thanks for reading!

.png)