Energy Transfer's Distribution Looks Supported, But Management's Past Actions Weigh on Investor Sentiment

Energy Transfer LP (ET) units have drifted about 10% lower over the past month, causing some investors to question the safety of ET's 9.7% dividend yield.

Aside from the price of oil slipping lower, which has weighed on the energy sector, the only recent news out on Energy Transfer is its planned $5 billion acquisition of midstream company SemGroup, announced on September 16.

Source: Energy Transfer Investor Presentation

This deal isn't huge compared to Energy Transfer's size (ET's market cap exceeds $30 billion), and it isn't expected to affect the firm's Borderline Safe Dividend Safety Score or credit rating.

"The stable outlook on ET reflects our belief that the combined company's credit measures will be acceptable for the rating, and that the robust distribution coverage ratios of almost 2x will provide the partnership with financial flexibility and funding certainty and help strengthen the balance sheet over time. We expect pro forma consolidated leverage to be about 4.5x in 2019 and about 4.7x in 2020 before improving to the 4.3x-4.5x range in 2021."

But some investors found the timing of Energy Transfer's latest acquisition to be rather curious. Management has prioritized deleveraging and the firm's move to a self-funded business model, which eliminates the need to issue equity to fund ET's growth backlog.

Buying SemGroup in a deal funded with 40% cash (debt) and 60% units (shares) nudges Energy Transfer's leverage higher next year and shows management is still willing to issue equity under the right circumstances. (ET expects the deal to immediately increase the firm's distributable cash flow per share.)

While these gripes might seem like some investors are making a mountain out of a molehill, they reflect past hurts inflicted by this management team.

For example, in the last five years Energy Transfer imposed "stealth distribution cuts" across its affiliated MLPs while simplifying its business model and dealing with several project delays.

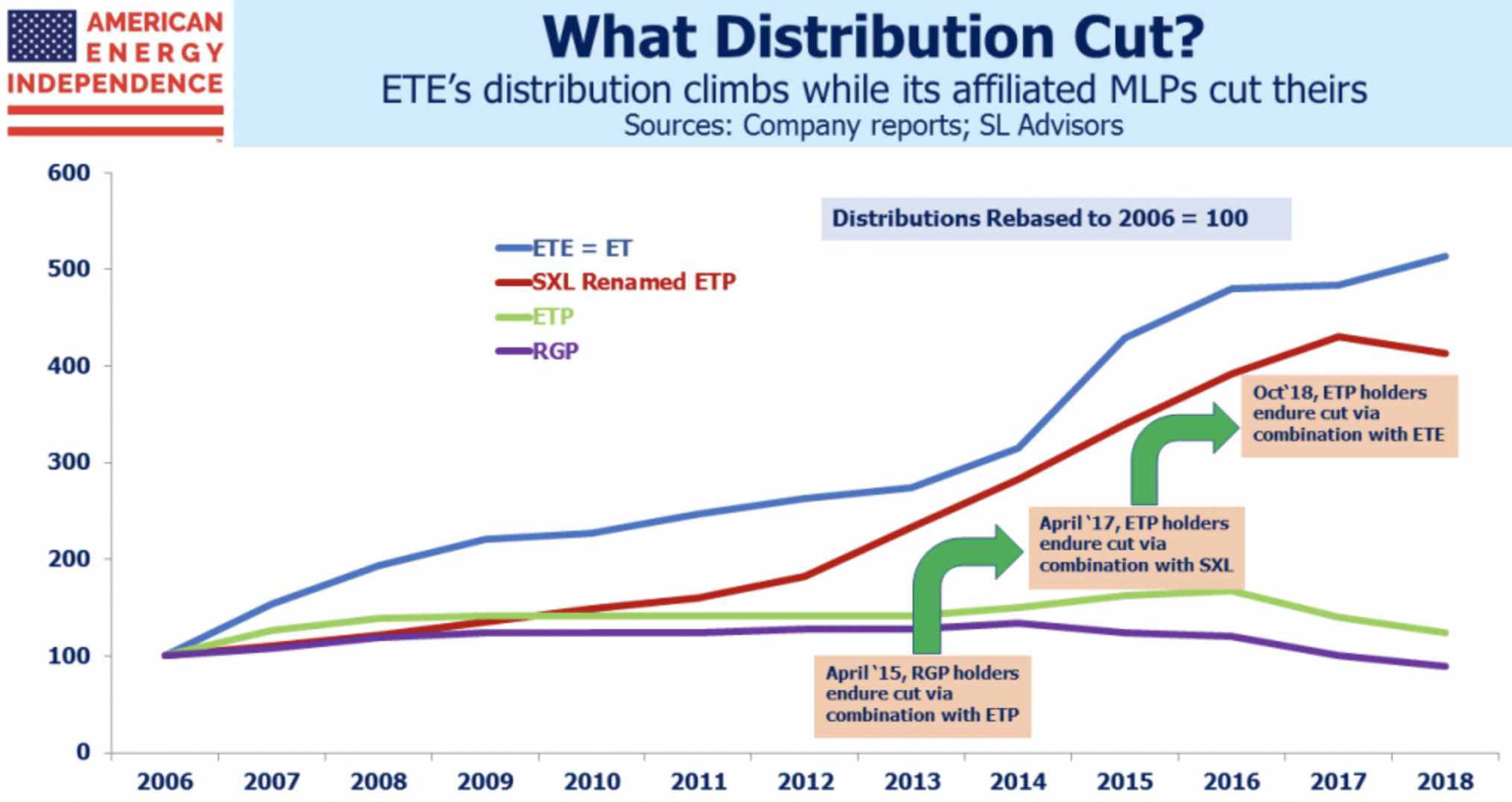

Management, led by Texas billionaire CEO Kelcy Warren, is most aligned with Energy Transfer Equity, which became Energy Transfer in 2018. As you can see, ET is the only partnership which has maintained steady or rising distributions.

Source: SL Advisors

Management's worst self-dealing behaviors were on display following ET's attempted $48 billion buyout of the Williams Companies (WMB) in 2015.

With oil prices falling lower, raising the risk profile of the deal and threatening Energy Transfer's credit rating, the firm's board wanted to retract its previous offer, which management felt was now too high.

After negotiations with the Williams Companies for a lower valuation failed, Energy Transfer decided to issue convertible preferred units to try and kill the deal. These securities were only issued to Warren, certain board members, and others whom Warren picked to be recipients.

As SL Advisors explained, these convertible preferred units diluted the subsequent value of ETE units, effectively lowering the cash-and-units offer the firm had made to the Williams Companies. Meanwhile, Warren and the firm's insiders were protected against any dilution and given preferential treatment to distributions, leaving common unitholders to bear the risk.

After the deal with the Williams Companies was canceled, Energy Transfer still chose to keep management's convertible preferreds outstanding. This sent a clear message to common unitholders that Warren is most interested in looking out for himself and the management team first.

Governance concerns seem like the most reasonable explanation for Energy Transfer's high yield and "cheap" valuation. As the MLP space continues evolving, what's to say another opportunity (a large acquisition, merger, etc.) won't come along where the common unitholders are left with the short end of the stick?

Ironically, Warren would probably be better off financially (he owns about 10% of the firm) if he didn't tarnish Energy Transfer's reputation and thus cause the firm to trade at a discounted valuation multiple.

For example, ET's unit price would need to nearly double to match the price-to-discounted cash flow (P/DCF) multiples enjoyed by investment-grade MLPs such as Enterprise Products Partners L.P. (EPD) and Magellan Midstream Partners, L.P. (MMP).

Despite its lackluster valuation, Energy Transfer's business fundamentals otherwise look healthy and supportive of its distribution.

Last quarter the company's payout ratio was about 50%, management revised adjusted EBITDA guidance higher while lowering full-year capital spending guidance, distributable cash flow grew nearly 25%, and liquidity exceeded $3.5 billion.

Source: Simply Safe Dividends

After paying distributions, Energy Transfer also retained $800 million in excess cash flow. That's $3.2 billion on an annualized basis, providing nearly 70% of the capital the firm needs to execute on its $4.6 billion to $4.8 billion of organic growth projects this year.

In other words, the firm's need for external financing continues to look manageable, and management's claim that no common equity issuances are needed to fund organic growth seems reasonable.

The firm's diversification across nearly all of the major U.S. producing basins, substantial customer base, and dependence on fee-based businesses, which generate over 90% of its cash flow, all lower its fundamental risk profile.

Ultimately, if you're invested in Energy Transfer, then you have to be comfortable with management's potential for self-dealing in the future and believe the stock's higher yield and cheaper multiple are worthy tradeoffs.