Imperial's Dividend Safety Score Downgraded to Unsafe on Vaping Challenges, Management Change

On September 26, Imperial Brands (IMBBY) lowered its guidance for the year due to challenging conditions in the U.S. vapor market. One week later, Imperial's CEO Alison Cooper stepped down after leading the company since 2010. Ms. Cooper had spearheaded Imperial's push into the vaping category.

As a result of these developments, which seem likely to pressure the firm's deleveraging efforts and need to invest in next-generation products (NGP), we are downgrading Imperial's Dividend Safety Score from Borderline Safe to Unsafe.

An Unsafe score does not mean a dividend cut is imminent. After all, Imperial's payout is still technically covered by the company's cash flow.

However, the company's stretched balance sheet, stalling earnings growth, slowing traction in the vaping market, and upcoming leadership change suggest Imperial may be more likely to alter its capital allocation framework and reduce its dividend in the future, making it a speculative income stock.

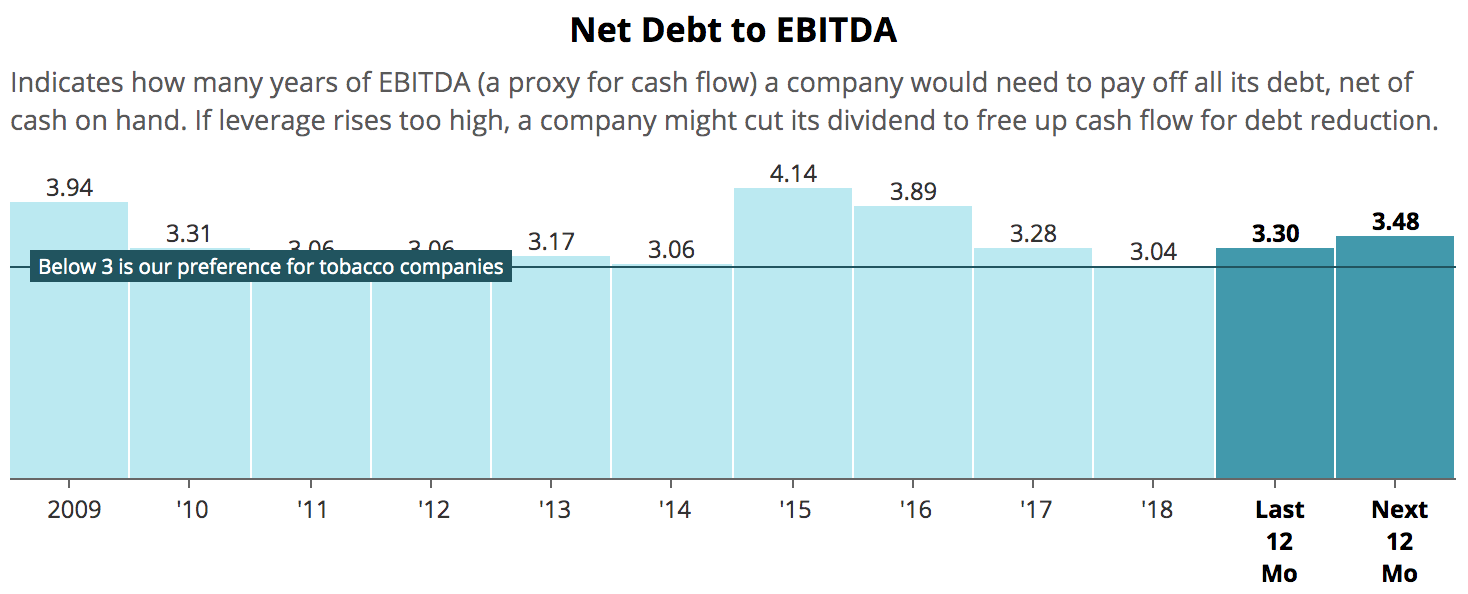

Let's start with the balance sheet. As we discussed in July, when Imperial ended its 10% annual dividend growth target, the company's net debt to EBITDA ratio is a full turn higher than the leverage ratios maintained by Altria and Philip Morris.

With Imperial now calling for EPS to remain flat this year rather than growing by 4% to 8% as previously expected, you can see that Imperial's leverage ratio is actually forecast to tick higher over the next year if nothing else changes.

Source: Simply Safe Dividends

Management desires to maintain an investment grade credit rating and reduce its leverage ratio to a range of 2.0 to 2.5 times. Based on our analysis earlier this summer, we noted that if Imperial Brands fails to grow its EBITDA going forward, it will need to reduce its net debt by $5 billion ,or nearly 30%, to hit the high end of its target leverage range.

Imperial is working to divest several businesses with hopes of raising up to $2.5 billion in proceeds by May 2020. The company has only sold $370 million worth of assets thus far, and with the dynamic state of the global tobacco market, it's hard to say if Imperial will be able to achieve the valuations it hopes for key assets like its premium cigar business.

Even if the divestiture plan is successful, the firm will need to retain enough cash flow to work down its debt load. Fortunately, Standard & Poor's does not view management's guidance reduction as a material threat to Imperial's BBB investment-grade credit rating.

Another growing problem for Imperial's dividend is the company's bet on vaping. In 2014 Imperial bought several U.S. cigarette brands and e-cigarette maker blu for $7.1 billion (for context, Imperial's current market cap is about $21 billion).

Imperial has poured money into developing blu, building consumer awareness, and establishing distribution in many countries worldwide. Management has long believed the world would move rapidly to e-vapor products, with blu positioning itself as a leader.

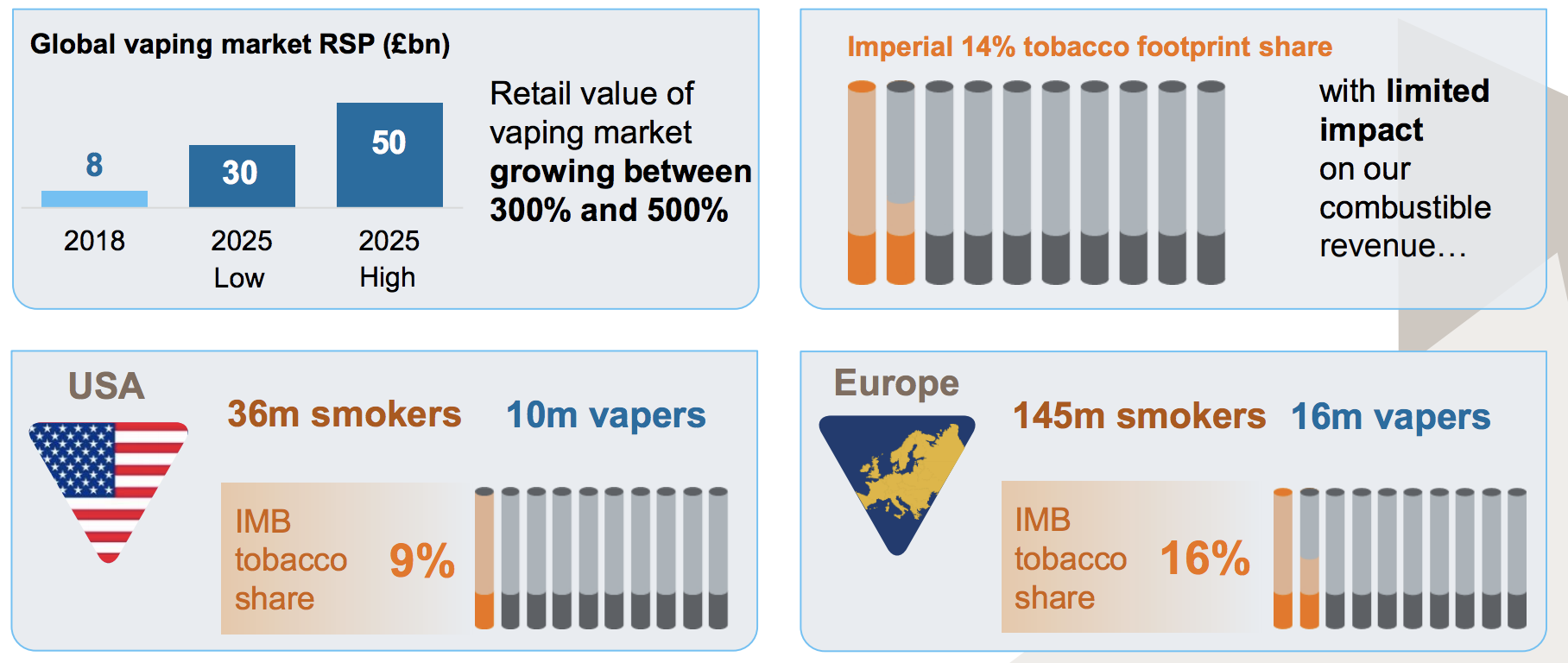

As you can see, earlier this year Imperial presented a forecast for the global vaping market calling for its value to rise from £8 billion in 2018 to as much as £50 billion in 2025.

Source: Imperial Brands

Unfortunately, Imperial's vaping thesis is on thin ice. The firm's NGP sales in the second half of fiscal 2019 are now expected to be at a similar level to the first half. Management also forecasts its NGPs will lose money rather than reach a breakeven exit rate this year.

Regulatory uncertainty in the U.S. has hurt demand for blu despite Imperial's higher investment in branding, driving the firm's guidance reduction, and blu's progress has also slowed in Europe.

Even if the regulatory climate eventually improves, many consumers now believe vaping is more dangerous than tobacco and could be reluctant to ever return to the category.

If the vaping industry fails to take off as Imperial has long expected, or if blu is unable to be as competitive as management hoped, then the company will likely need to step up its investments in NGPs.

This could mean doubling down on e-cigarettes, pouring more money into its heat-not-burn tobacco product, or going a different direction entirely.

Either way, it seems likely that management will eventually need to spend more money to ensure Imperial remains relevant in the long term.

The board's recent decision to part ways with CEO Alison Cooper, who was behind the firm's big push into vaping, also suggests Imperial's long-term NGP strategy could be evolving and will require greater financial flexibility going forward.

Imperial's stretched balance sheet, smaller scale, and less dominant cigarette brands are especially liabilities here. Imperial retains about $1 billion in free cash flow after paying dividends each year and will need to use much of this cash to pay down debt.

With NGPs expected to lose money for longer than management expected, plus a potential change in strategy coming, it could become increasingly difficult for Imperial to return to its target leverage range.

Meanwhile, unlike Altria and Philip Morris who enjoy rights to the world's No. 1 cigarette brand (Marlboro), Imperial doesn't own many cigarette brands that dominate their markets (less than 10% share in the U.S. and 16% share in Europe).

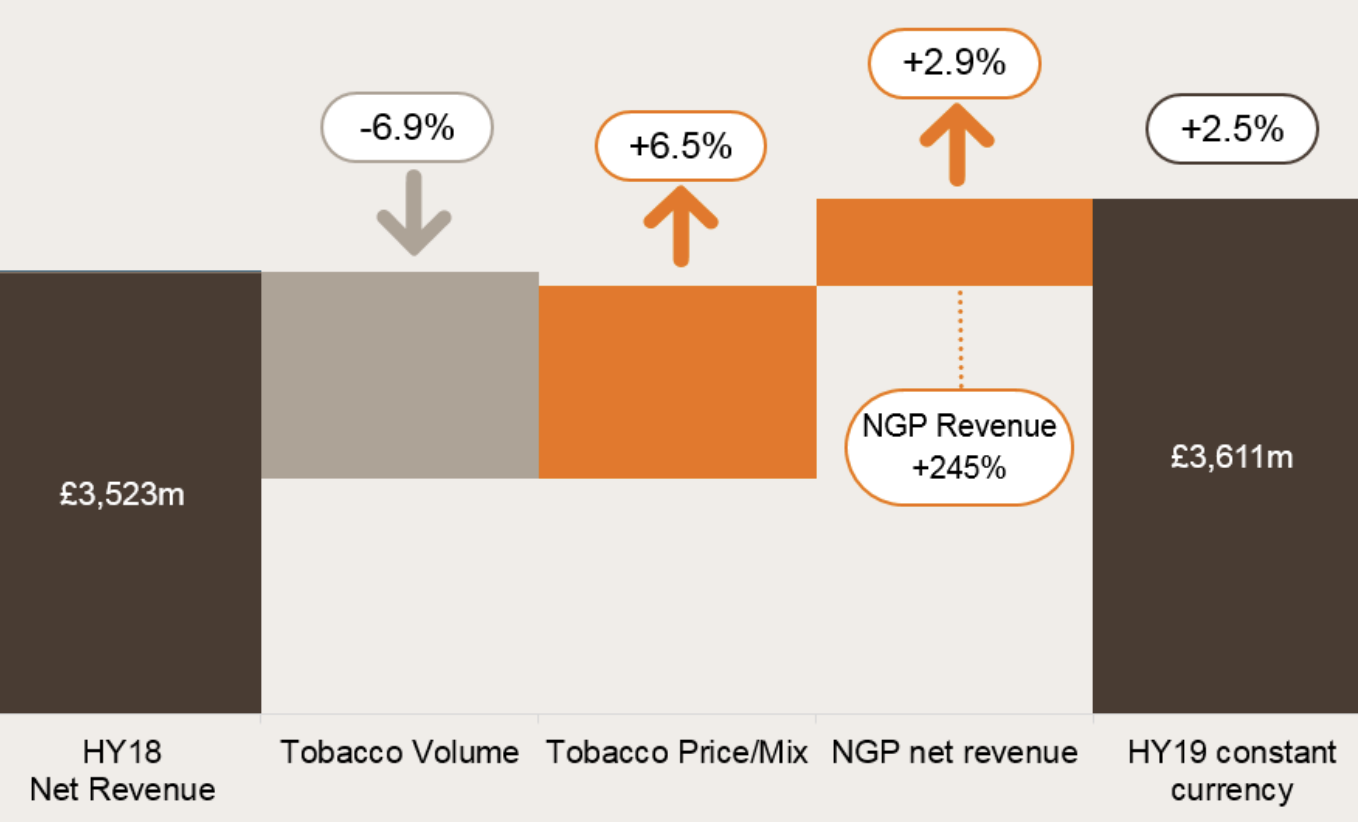

Through the first half of fiscal 2019, Imperial's tobacco price/mix increases did not offset the 6.9% volume decline the company experienced. The firm's top line only grew 2.5% thanks to an increase in NGP revenue, which is now leveling off as the vaping market slows down.

Source: Imperial Brands

While Philip Morris does not have any exposure to the U.S. (the Americas region generates nearly 30% of Imperial's revenue), its portfolio is performing much better. PM's constant current net revenues grew 6.2% in the first half of 2019, with cigarette volumes down just 1.9%.

Imperial's cigarette volumes were impacted by some shipment timing noise, but they still declined 4.9% excluding this item. In other words, Imperial appears to have a weaker portfolio of brands that could be more susceptible to the secular decline in smoking rates, increasing its urgency to adapt.

Overall, the shockwave rippling through the vaping market coupled with Imperial's CEO departure and uncomfortable financial flexibility place the firm's dividend on shakier ground. The stock's double-digit yield may look tempting, but it could go up in smoke if management believes it would be prudent for Imperial to invest more in NGPs and improve its balance sheet in these uncertain times.