Altria's Potential Merger With Philip Morris International Seems Favorable in the Long Term

In 2008, Altria (MO) spun off Philip Morris International (PM) with hopes of unlocking value from its faster-growing international business, which was underappreciated by investors who worried about the decline in U.S. cigarette consumption and the threat from tobacco litigation.

Now, more than a decade later, both companies announced on August 27 that they are exploring a possible reunion (see Altria's press release here and PM's statement here).

Very few details are available about the proposed combination, and both companies have said there can be no assurance that any deal will result from these discussions. After all, any transaction would be subject to the approval of the two companies’ shareholders, and the market didn't like the news.

Shares of Altria initially rallied nearly 10%, but they are now about 7% below where they traded before the announcement was made. Philip Morris shares have also lost roughly 7%.

Why the pessimism? In Altria's case, I believe investors are concerned that an "all-stock, merger of equals" could represent a takeunder of the company, leaving value on the table.

The companies have not said anything about the terms of the potential merger they are discussing, but a "merger of equals" seems to imply that Philip Morris, which is the larger of the two firms, is unlikely to pay a premium for Altria.

Altria's stock has performed worse than PM's over the past year and sports a forward P/E ratio of just 10.1, less than half the multiple it traded at as recently as late 2017 and well below Philip Morris International's 13.5 ratio.

An increasingly murky outlook for combustible cigarettes in the U.S., where Altria does all of its business, has driven the firm's weak valuation.

Compared to most other countries, cigarette volume declines have accelerated in America, and regulators have significantly increased their scrutiny of next-generation products such as e-cigarettes.

This uncertainty has weighed on shares of Altria, so combining companies now without any premium would lock in Altria's weak valuation. (Someone briefed on the deals terms told The Financial Times that Philip Morris would own between 57% and 59% of the combined company).

Besides concerns about Altria's valuation and the general lack of details about the transaction being discussed, investors might also read into this news as a negative datapoint for U.S. cigarette consumption trends.

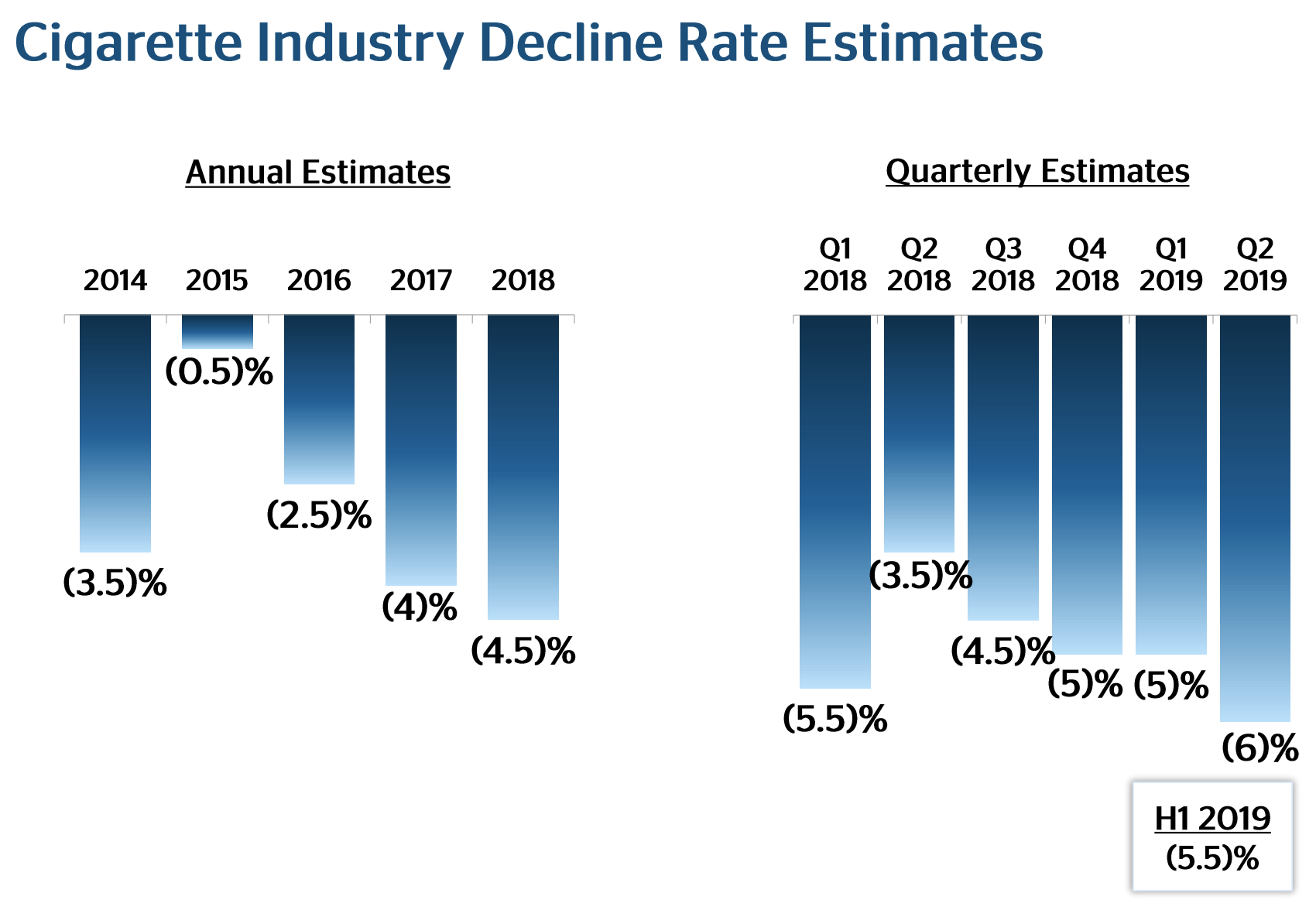

When Altria spun of Philip Morris International in 2008, U.S. cigarette consumption was declining at a 3% to 4% annual rate, according to The Wall Street Journal.

That manageable pace of decline largely continued through 2016 but has since accelerated due to the continued aging of older smokers, growth in alternative products such as e-cigarettes, and many states raising the legal age to purchase tobacco products to 21.

As a result, in July 2019, Altria expanded its estimated range for annual average U.S. cigarette industry volume declines through 2023 to 4% to 6% from a range of 4% to 5%.

Source: Altria Earnings Presentation

If Altria was optimistic these trends were not accelerating further and felt great about its business positioning, management probably wouldn't be keen to ink a deal with Philip Morris International, at least nowhere near the company's current valuation.

With that said, it's hard to make a judgement on the valuation until terms are disclosed. However, fundamentally, there are several reasons why Altria shareholders should like the idea of a merger from a long-term perspective.

First, combining with Philip Morris International immediately diversifies the company's products, regulatory risk profile, and geographic reach.

Altria generated $19.7 billion in revenue over the past year compared to Philip Morris International's $29.5 billion. Thanks to years of investments focused on technology that can help create a "smoke-free" world, reduced-risk products accounted for nearly 20% of PM's net revenue last quarter.

Altria was largely caught off guard by the rise of vaping and other nicotine products with perceived lower risk. As a result, in late 2018 the firm invested $14.6 billion for minority stakes in privately held vaping giant Juul Labs and cannabis company Cronos (CRON).

Combining with Philip Morris International gives Altria a much larger mix of reduced-risk products, better positioning the firm for the future. Philip Morris International also substantially increases Altria's distribution of alternative products thanks to its presence in more than 180 countries.

For example, management is working to expand Juul's vaping products internationally, so Philip Morris International's established network overseas could help the company scale its e-cigarette portfolio faster.

The countries Philip Morris International operates in also appear to be more resistant to cigarette volume declines. Through the first half of 2019, Altria estimates U.S. cigarette shipments fell 5.5%, while Philip Morris International's cigarette volume slipped just 1.5% during the same period.

Standard & Poor's believes that developing markets are seeing steadier volumes because "smoke-free alternatives are generally more expensive and less available than cigarettes." The populations in these countries are usually younger and faster-growing compared to America's, too.

Increased product and geographic diversification also improves Altria's regulatory risk profile, which has deteriorated significantly in recent years. If these two giants combined, the U.S. would represent close to 40% of combined revenue, compared to 100% for Altria today (excluding its stake in ABInBev).

Finally, merging with Philip Morris increases the company's scale. Tobacco is far from a capital-intensive industry, reducing the magnitude of potential cost synergies, but developing and distributing next-generation products is very costly.

The combined business would likely be better positioned to produce and scale reduced-risk offerings covering the full spectrum of vaping and heated tobacco products.

Costs could also be taken out of the business by eliminating duplicative corporate overhead costs, ensuring the dividend remains covered without compromising on making necessary "smoke-free" investments for the future.

From a financial perspective, it's too soon to make many claims since we don't know what the combined firm's capital structure will look like or the financial policies management will implement.

However, given each company's dedication to its dividend, plus Altria's 50th consecutive annual dividend increase announced just last week, I would expect income investors in both firms to be kept whole in any transaction.

I'd also be surprised if the combined entity did not maintain an investment grade credit rating, and the transaction seems likely to be structured as a tax-free combination if it reaches the finish line.

Overall, no change is expected in Altria or Philip Morris International's SafeDividend Safety Scores based on what we know today.

Altria investors are right to have some concerns about the firm's valuation if a "merger of equals" commences, but a combination also provides long-term diversification benefits, especially given the risk created by the dynamic U.S. regulatory and consumer environment.

As more information is released about what a transaction might look like, we will keep everyone updated. For now, we plan to continue holding the shares of Altria and Philip Morris International we own in our Top 20 Dividend Stocks and Conservative Retirees portfolios.