MPLX Faces Uncertainty From Low Gas Prices But Retains Borderline Safe Rating

MPLX LP's (MPLX) unit price has slumped 30% over the past year, including a 15% decline in recent weeks. With a dividend yield approaching 10%, the stock has some income investors wondering whether or not the firm's payout is safe.

Let's take a closer look at MPLX's business and the factors that have weighed on its stock.

Source: Simply Safe Dividends

MPLX LP (MPLX) was formed in 2012 by Marathon Petroleum (MPC), the largest crude oil refiner in America, and owns midstream energy infrastructure and logistics assets. MPLX helps Marathon Petroleum and other energy companies transport and store oil and refined products and gather, process, and transport natural gas and natural gas liquids.

Source: MPLX Investor Presentation

MPLX's initial purpose was to be used by Marathon as a financing vehicle (MPC owns over 60% of MPLX's units). Marathon would drop down completed midstream assets to MPLX, which would issue equity and debt to fund these purchases. MPLX's high payout made the stock attractive to income investors, keeping its cost of capital reasonably low, and Marathon used proceeds from the dropdowns to fund growth projects and repurchase its stock.

MPLX's model has evolved since its formation. The MLP no longer depends on Marathon to primarily fuel its growth via dropdowns but is instead pursuing many of its own projects. In 2015 MPLX acquired MarkWest Energy Partners LP, a processor and transporter of natural gas, for $15.6 billion, creating the fourth-largest MLP by market value.

At the time, MPLX's business consisted of oil and refined product pipelines running across the Midwest and Gulf Coast regions. These assets are highly integrated with Marathon's refining operations. As Reuters noted, MarkWest added "natural gas processing facilities to MPLX's crude-heavy portfolio."

Then, in November 2017, Marathon agreed to drop down midstream assets worth $8.1 billion to MPLX. Following the completion of the dropdowns in early 2018, Marathon's incentive distribution rights, or IDRs, were eliminated. IDRs send up to 50% of incremental cash flow to the general partner and greatly increase an MLP's cost of capital.

Marathon's general partner interest in MPLX was also converted into a non-economic interest. These actions reduced MPLX's cost of capital, simplified its organizational structure, and better positioned the business to be able to self-fund its growth going forward.

Furthering these efforts, in May 2019 MPLX announced plans to acquire Marathon's other midstream MLP, Andeavor Logistics LP (ANDX), in a $14 billion deal. Andeavor Logistics' business model is similar to MPLX's in that its midstream logistics assets are also utilized by Marathon's refining operations.

However, Andeavor has more of a presence across the western and mid-continent regions of the U.S. The firm also has a substantial oil gathering business in the fast-growing Permian basin, where MPLX is mostly focused on natural gas gathering and processing.

MPLX closed its acquisition of Andeavor on July 30, 2019, so we don't yet have official financials of the combined company. However, this deal significantly increased MPLX's scale and diversification.

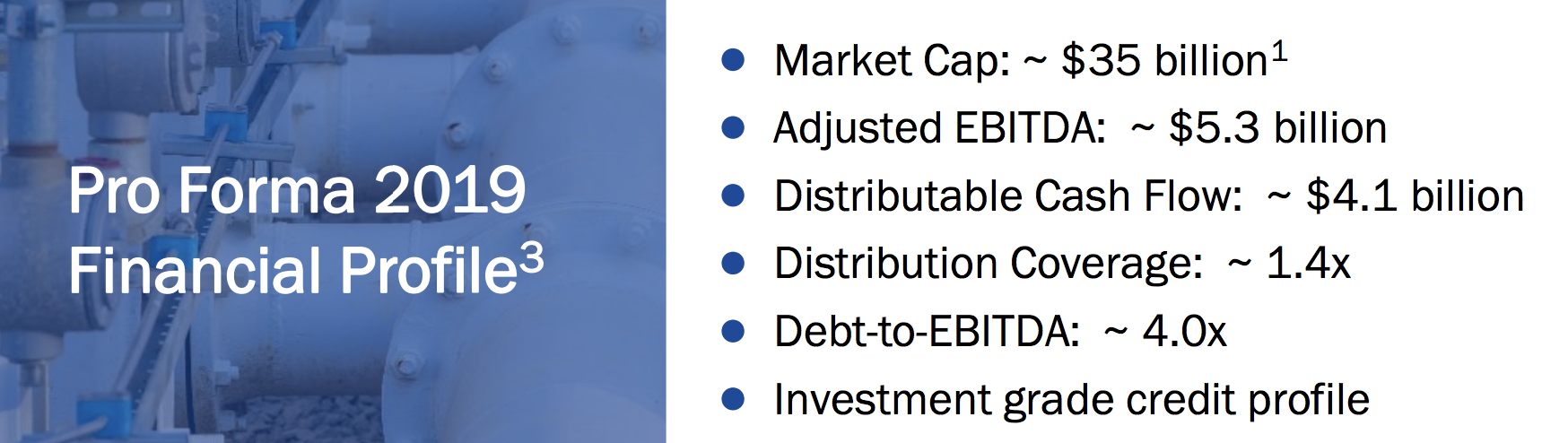

Given that backdrop, why has MPLX's stock been so weak? The good news is that the firm's pro forma financial profile, which incorporates Andeavor Logistics, looks solid for now. The combined company expects to maintain a healthy distribution coverage ratio of 1.4 and an investment grade credit profile.

Source: MPLX Investor Presentation

Like most midstream MLPs, MPLX also touts the long-term, fee-based agreements with minimum volume commitments it has with its customers. In fact, Moody's notes that over 80% of the combined company's revenues are fee-based, highly contracted and with significant throughput attributable to" Marathon.

As stated in MPLX's annual report, this business model is meant to provide the firm with "a stable and predictable revenue stream and source of cash flows."

However, a contract doesn't provide stable cash flow if customers can't honor the terms. With the prices of oil and natural gas slumping, investors are growing concerned about the health of some of MPLX's customers, which could cause the MLP's financial profile to weaken.

The main sore spot is MPLX's Gathering and Processing business, which generates approximately 40% of the firm's EBITDA. This segment consists primarily of several natural gas gathering and processing systems in the Northeast.

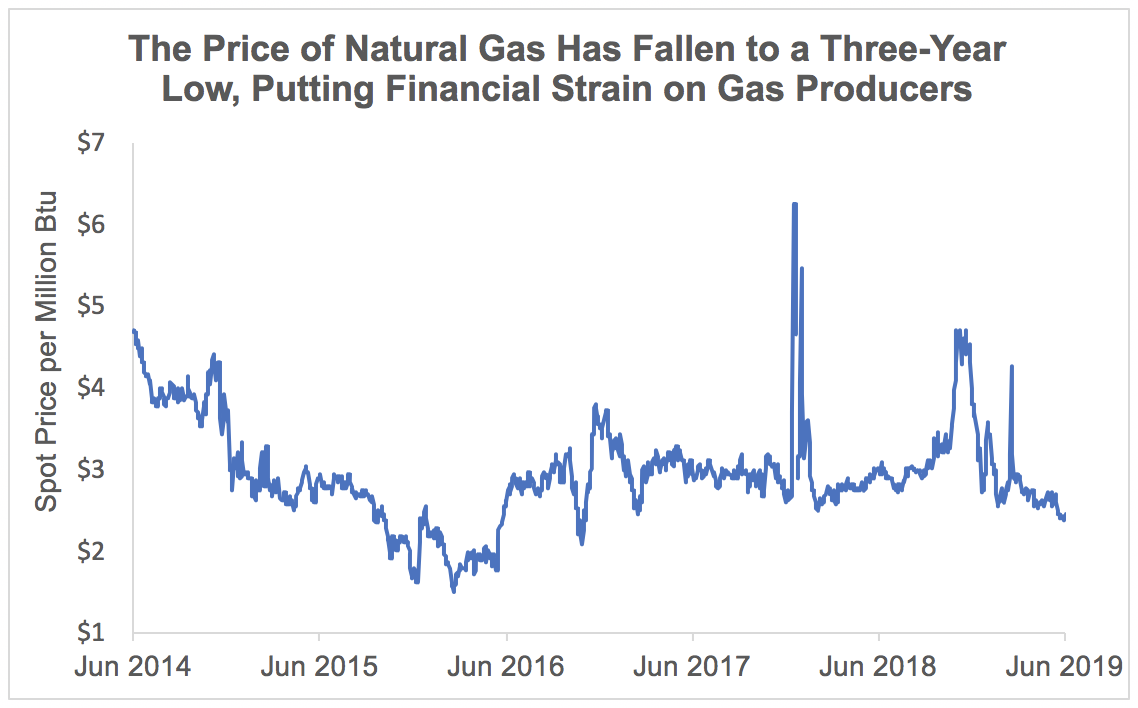

Unfortunately, the price of natural gas has fallen more than 20% over the last year to reach its lowest level since the summer of 2016. Mild summer temperatures, which reduce demand for gas used to power air conditioners, have contributed to the weakness. Meanwhile, U.S. gas production continues to rise, hitting a recordearlier this year.

Source: U.S. Energy Information Administration, Simply Safe Dividends

Gas producers, MPLX's main customers in its Gathering and Processing division, are hurting. Several major customers MPLX discloses are Antero Resources (AR), EQT (EQT), and Range Resources (RRC).

Each company's stock price has lost between 55% and 80% over the past year, and generating free cash flow has proven to be difficult. For example, Antero Resources previously indicated it could achieve free cash flow neutrality at $50 per barrel oil and $2.85 gas, but gas prices sit near $2.20 today.

Antero Resources – Source: Simply Safe Dividends

MPLX's annual report notes that "decreases in energy prices can decrease drilling activity, production rates and investments by third parties in the development of new oil and natural gas reserves."

MPLX's Gathering and Processing business depends on production from oil and natural gas reserves and wells owned by its producer customers. Production at a well naturally declines over time, so to maintain or grow throughput levels and the utilization rate of its facilities, MPLX must continually obtain new oil and gas supplies, which "depend in part on the level of successful drilling activity near our facilities," per MPLX.

Low energy prices are causing producers to reduce their drilling activity, clouding their future production growth profiles. When Antero Resources announcedsecond-quarter earnings results on July 31, the firm noted that its "drilling and completion capital spend" fell to its lowest quarterly level since Antero's IPO in 2013.

MPLX's gathering and processing contracts do contain some volume protection, but they are far from being fully covered. In the critical Marcellus region, only 67% of MPLX's 2018 capacity contained minimum volume commitments, and less than 30% of its capacity in other regions contained such provisions.

Source: MPLX 10-K

It's difficult to say whether or not weak gas prices will materially affect the amount of volume moving through MPLX's network, or the ability of gas producers to honor the terms of their contracts. Short-term energy prices are notoriously volatile, and we don't have great visibility into many of MPLX's customers.

However, the crux of MPLX's investment thesis is that strong production growth will support rising demand for its infrastructure assets. Persistently weak energy prices could pressure otherwise optimistic production growth forecasts.

Source: MPLX Investor Presentation

Part of MPLX's business is also directly tied to prices of natural gas liquids (NGL). Management estimates that every $0.05 change in weighted average NGL prices would result in a $23 million annual impact to EBITDA. MPLX had planned for an average price of $0.76 per gallon this year, but the price recently has been closer to $0.40, suggesting a 3% hit to the company's overall EBITDA.

In addition to uncertainty surrounding commodity prices and future production growth rates, management's communication hasn't helped investor confidence either.

MPLX declined to offer EBITDA guidance for 2020, citing dynamic producer plans and the firm's intention to reduce its own capital spending while also evaluating potential divestitures. Here are the priorities management listed on MPLX's latest earnings call:

"First, we expect to streamline our capital expenditures focusing on the most attractive returns. Second, we are working with [Marathon] on a portfolio optimization initiative, which could include potential asset divestitures. Third, we plan to use the proceeds from any divestitures for general purposes such as investments and high return projects, as well as debt reduction."

What does it all mean for the firm's distribution safety? For now, MPLX retains its low Borderline Safe Dividend Safety Score.

After combining with Andeavor Logistics, we estimate MPLX's distribution will consume $2.8 billion annually. Management expects the company to generate $4.1 billion in distributable cash flow, resulting in retained cash flow of about $1.3 billion per year.

Retained cash flow can be used to invest in growth projects, pay down debt, repurchase shares, or make acquisitions. In recent years, some MLPs ran into trouble because they retained too little cash flow to support their growth, making them overly dependent on issuing equity and debt to fund their businesses. Once their unit prices tanked during the 2014-16 oil crash, they had to choose between maintaining their distributions or cutting back on growth spending.

Fortunately, MPLX's elimination of its IDRs and efforts to better focus its growth spending suggest it won't run into this issue. Prior to combining with Andeavor, MPLX's annual growth capex was around $2 billion, and Andeavor's target was $600 million. Management plans to "streamline and optimize" this spending, suggesting it will come in much less than $2.6 billion.

For the $1 billion or so of growth capex not covered by MPLX's retained cash flow, the firm plans to issue debt to fill the gap. With a reasonable leverage ratio near 4.0, an investment grade credit rating, and over $2.5 billion of liquidity available through its credit facilities, MPLX appears well positioned to execute this strategy. Importantly, MPLX does not need to issue equity to fund its growth backlog, so its low unit price isn't a direct threat to its business model or distribution.

With that said, MPLX's distributable cash flow could change depending on the potential divestitures the company pursues, as well as any financial fallout with gas producers or integration challenges with Andeavor Logistics. It's too soon to say what will happen, but the firm's current distribution coverage at least leaves some margin for error. Until more clarity is provided, MPLX's Borderline SafeDividend Safety Score is expected to remain unchanged.

Overall, there are a number of moving parts to MPLX's story. On the bright side, the MLP has become even larger and more diversified following its acquisition of Andeavor Logistics. MLPX also maintains a reasonable amount of leverage, has a decent distribution coverage ratio, and employs a self-funded business model.

However, investors remain concerned about the difficult environment gas producers face, which could threaten some of MPLX's contracts and cash flow. Other gas-focused MLPs such as Antero Midstream (AM) remain weak on similar fears. Since MPLX's gas gathering and processing business was largely the result of its MarkWest acquisition in 2015, investors have probably lost some faith in management's capital allocation skill, too.

Management's lack of details regarding its plans for Andeavor Logistics, capital spending priorities, and potential divestitures hasn't helped that perception. While most stocks with yields near 10% have weaker fundamentals than MLPX, the firm may not be out of the woods until gas producers find themselves on more stable ground, demonstrating they can and will continue honoring their contracts and growing their production.