Pfizer's Mylan Deal Keeps Income Investors Whole But Will Likely Affect The Firm's Current Dividend

Pfizer (PFE) has taken steps in recent years to focus its business on higher-margin, faster-growing prescription drugs. For example, in 2013 the company spun off its animal health business, late last year Pfizer reached a deal with GlaxoSmithKline (GSK) to combine their consumer health businesses, and in June 2019 the firm agreed to buy cancer treatment firm Array BioPharma for $10.6 billion.

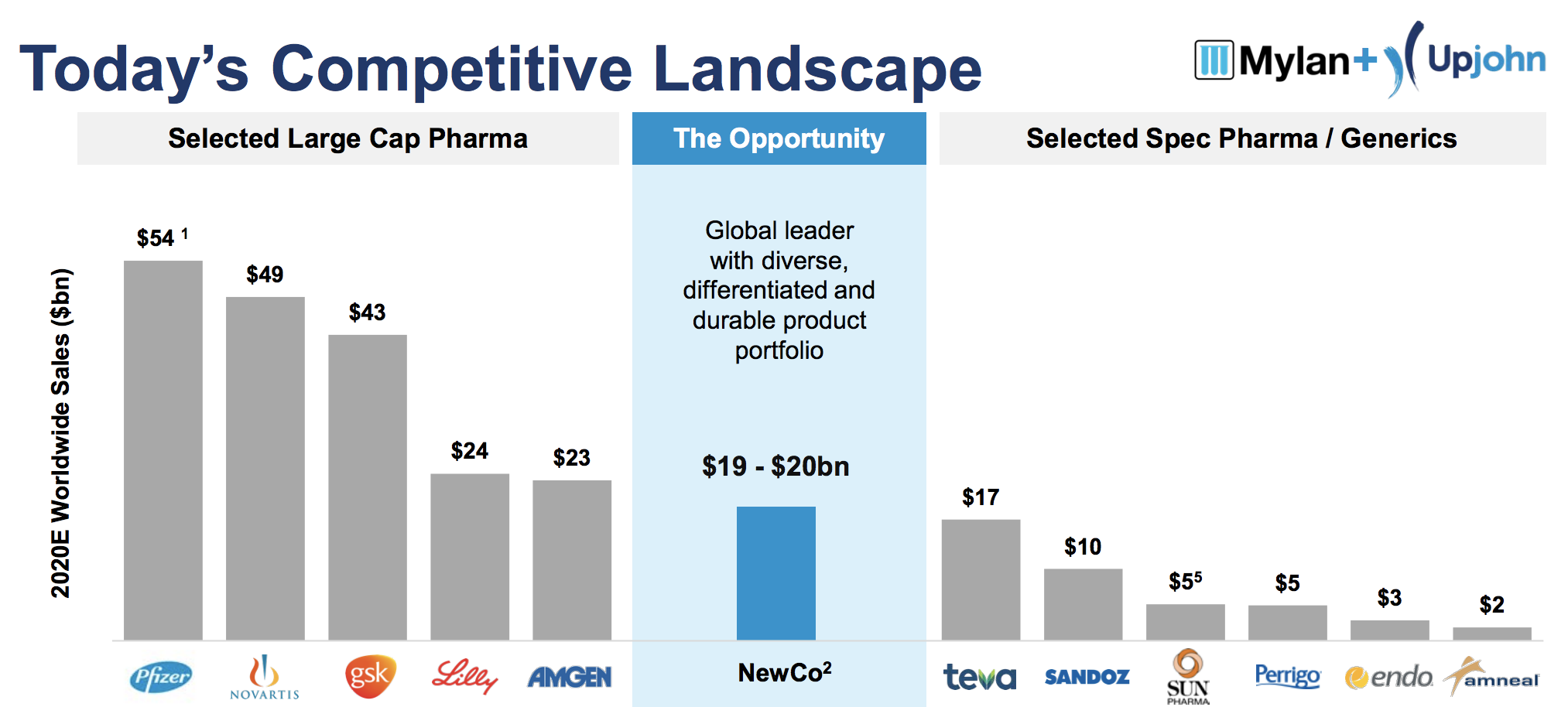

Pfizer's evolution took its biggest step forward this past weekend when management announced plans to combine its off-patent established medicines with generic drugmaker Mylan (MYL), creating a new global pharmaceutical company with nearly $20 billion in revenue. This deal has important implications for dividend investors.

Source: Pfizer Investor Presentation

Pfizer's established drugs business, which management calls Upjohn, was expected to account for about 18% of the company's EBITDA in the year ahead. Therefore, once the transaction closes in mid-2020, subject to approval by Mylan shareholders, Pfizer's cash flow will fall significantly. We estimate the firm's payout ratio will rise to between 65% and 80%.

While Pfizer's $8 billion annual dividend commitment would still be covered by the $10 billion or so of free cash flow the firm will likely generate, management probably desires to retain more cash flow to invest in drug development and acquisitions.

After all, Pfizer has taken these separation actions to improve its standalone growth profile. By spotlighting its faster-growing drugs that enjoy patent protection, management hopes Pfizer will achieve a higher valuation. Companies focused more on growth typically do not maintain a high payout ratio.

Additionally, the biopharma business is a riskier industry given the substantial costs and high failure rates associated with developing breakthrough medicines. Once new drugs eventually lose patent protection, cash flow can decline quickly, too. As a result, acquisitions happen frequently in this space to help replenish drug pipelines, and it's important for companies to maintain financial flexibility.

These reasons further support Pfizer's likely need to lower its payout ratio once its off-patent established medicines business is separated next year. Management has not specified how Pfizer's $1.44 per share dividend will be adjusted.

However, the company stated that the combined dividend to Pfizer shareholders is expected to equal Pfizer's dividend immediately prior to closing:

"Pfizer also expects that following the closing of the transaction the combined dividend dollar amount received by Pfizer shareholders in the event the equity distribution is structured as a spinoff, based upon the combination of continued Pfizer ownership and an expected 0.12 shares of the new company granted for each Pfizer share, will equate to Pfizer’s dividend amount in effect immediately prior to closing."

In other words, Pfizer's current dividend will probably be reduced (we'd guess by 10% to 20%), but the new company formed with Mylan will pay a dividend that makes income investors whole.

Pfizer investors are expected to receive 0.12 shares of the new company for each Pfizer share they hold, assuming the deal is structured as a spinoff. The new company, which does not yet have a name, expects at least 25% of its free cash flow to be paid as a dividend.

Should conservative income investors continue holding Pfizer? What about the new company being formed with Mylan?

I've held shares of Pfizer in our Conservative Retirees portfolio since April 2017, and I plan to stay the course for now. When I bought Pfizer, I actually liked its mature consumer health and established medicines business. They provided steady cash flow, helped diversify the company's drug portfolio, and took some pressure off of its biopharma division, which can be volatile.

Going forward, Pfizer will still generate a boatload of cash, but you can see management is really pushing the company's improved revenue growth profile:

Source: Pfizer Investor Presentation

Wanting to achieve faster top-line growth is not necessarily a bad thing. It's just not the reason why I bought shares of Pfizer in the first place. A generous dividend and moderate growth are quite alright with me. As a conservative investor, I also prefer to own healthcare companies whose fates are not tied to the success of a small handful of drugs.

Pfizer's business will become more concentrated following the separation, but it doesn't look uncomfortably risky to me. Based on the firm's second-quarter results, and assuming only the biopharma business stays with Pfizer, its four largest drugs would account for 13.1%, 12.3%, 11.3%, and 6.4% of total revenue.

Pfizer will have about $40 billion in annual sales, along with a drug development pipeline that includes 15 potential blockbusters (at least $1 billion revenue potential) that could be approved for sale by regulators by 2022.

Management believes this will help the company drive growth through the mid-2020s:

"Following the close of the proposed transaction, I expect Pfizer will be positioned to deliver revenue and Adjusted diluted EPS growth through the mid-2020s that is among the industry leaders while continuing to allocate significant capital directly to shareholders, primarily through dividends." – CEO Dr. Albert Bourla

Pfizer also issued $12 billion of debt that the new company will carry, but Pfizer retained the cash. This move strengthens Pfizer's balance sheet and positions it to opportunistically acquire other medicines.

Overall, Pfizer seems likely to remain a solid dividend holding following the separation of its Upjohn business. Unless its drug portfolio becomes increasingly concentrated or a much better income opportunity arises elsewhere in the market, I expect to continue holding my shares.

I'm less certain about the new Upjohn-Mylan business that will be formed. Both companies face growth challenges. Upjohn's operational revenue fell 7% last quarter as Pfizer's older drugs continue facing competitive pressures. This business consists of past blockbusters such as Lipitor, Viagra, and Lyrica.

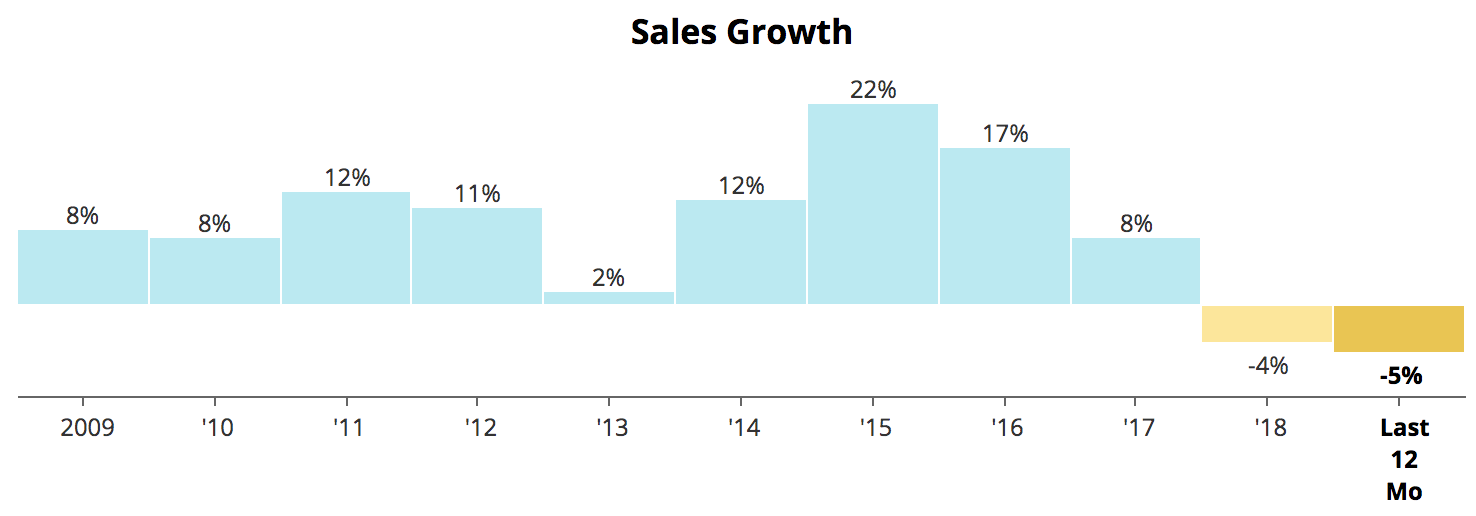

Mylan, maker of the EpiPen, has a portfolio covering many geographies and therapeutic areas, such as central nervous system and anesthesia, infectious disease, and cardiovascular. However, its revenue has also been falling at a mid-single digit pace thanks to generic drug price declines, stiff competition, and manufacturing challenges.

Mylan Sales Growth – Source: Simply Safe Dividends

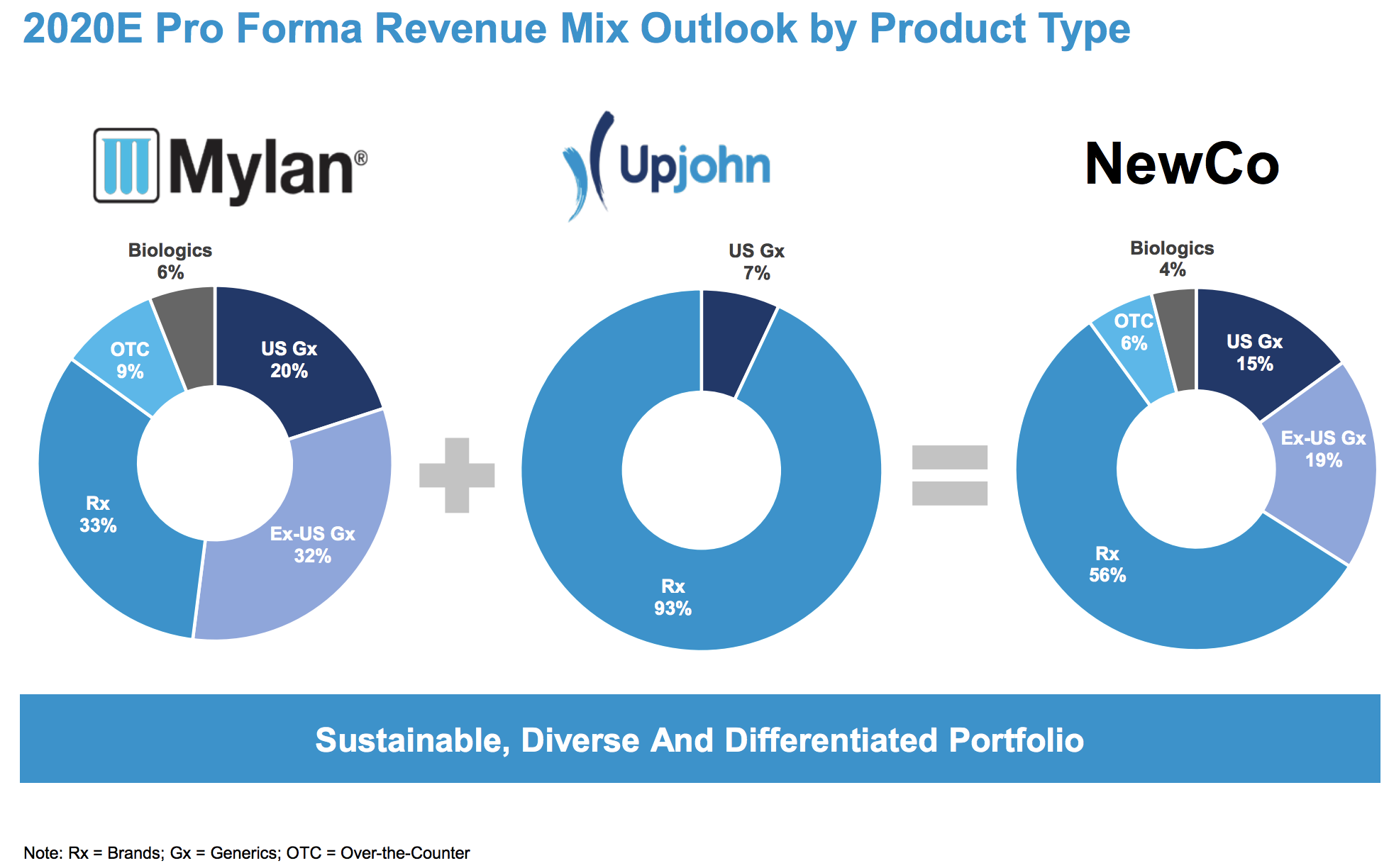

Management hopes that teaming up will improve the combined company's growth potential and profitability in the long term. Pricing pressure is expected to temper short-term growth, but the firm targets $3 billion in new revenue from products expected to launch by 2023, with a focus on complex generics (Gx), biosimilars, and global key brands (Rx). For context, the new company will have close to $20 billion in revenue next year.

Management sees opportunity to bring some of Mylan's products to Upjohn's growth markets, too. Approximately 30% of the new company's revenue is derived in Asia Pacific, with another 15% from emerging markets.

Source: Pfizer Investor Presentation

However, it's hard to envision this business ever achieving more than a low-single digit pace of revenue growth (at best). The good news is Pfizer embarked on this deal after generic drug price headwinds began rippling through the sector (Mylan's stock is down more than 70% since mid-2015), helping keep expectations low and perhaps reducing valuation risk.

While revenue growth may never amount to much, thanks to greater scale management believes the new company can achieve cost synergies of at least $1 billion annually (nearly 5% of sales) by 2023. If successful, this should help the business remain a cash cow, even if the pricing environment remains tough.

The Upjohn-Mylan company needs to continue generating solid cash flow due to its balance sheet, which will hold roughly $24.5 billion in debt when the deal closes. Although management expects the firm to have an investment grade credit rating, the new company's gross leverage ratio will sit at an elevated level between 3.1 and 3.3.

Management seeks to reduce the firm's gross leverage ratio to no higher than 2.5 by the end of 2021. This objective seems achievable since the business is expected to generate around $3 billion of free cash flow after paying dividends each year.

Ultimately, the new Upjohn-Mylan company doesn't look like much to get excited about. The firm consists of two mature businesses that each face their own growth headwinds and risks, and the balance sheet does not provide much flexibility in the short term if the ice cube melts much faster than expected (though that seems unlikely).

On the bright side, Pfizer struck a deal with Mylan at an interesting time when the generic drugmaker's valuation was in the dumps. The new company should generate decent cash flow and benefit from greater scale. It's also focused wisely on returning capital to shareholders. However, a 25% payout ratio suggests its dividend yield might not be high enough to appeal to income investors given its weaker growth profile.

Given my plans to continue holding Pfizer, plus the transaction's mid-2020 close date (assuming Mylan shareholders approve it), there's nothing to do for now. I'll continue digesting more information on this new business before making a call on whether to hold the shares I receive in the future or upgrade into a dividend stock that might be better aligned with my objectives. It's not an urgent decision.

Regardless, if income is your objective, be aware that Pfizer's dividend will probably be adjusted somewhat lower next year, but dividends paid by the new Upjohn-Mylan company are expected to make up the difference. For this reason, Pfizer's Safe Dividend Safety Score remains unchanged. If anything changes materially with this transaction, we will provide another update.