V.F. Corp's New Dividend, Plus Kontoor, Makes Income Investors Whole For Now

Earlier this week V.F. Corp (VFC) declared a quarterly dividend of $0.43 per share. The company's prior quarterly dividend rate was $0.51 per share, resulting in some headlines claiming that this dividend aristocrat had cut its payout.

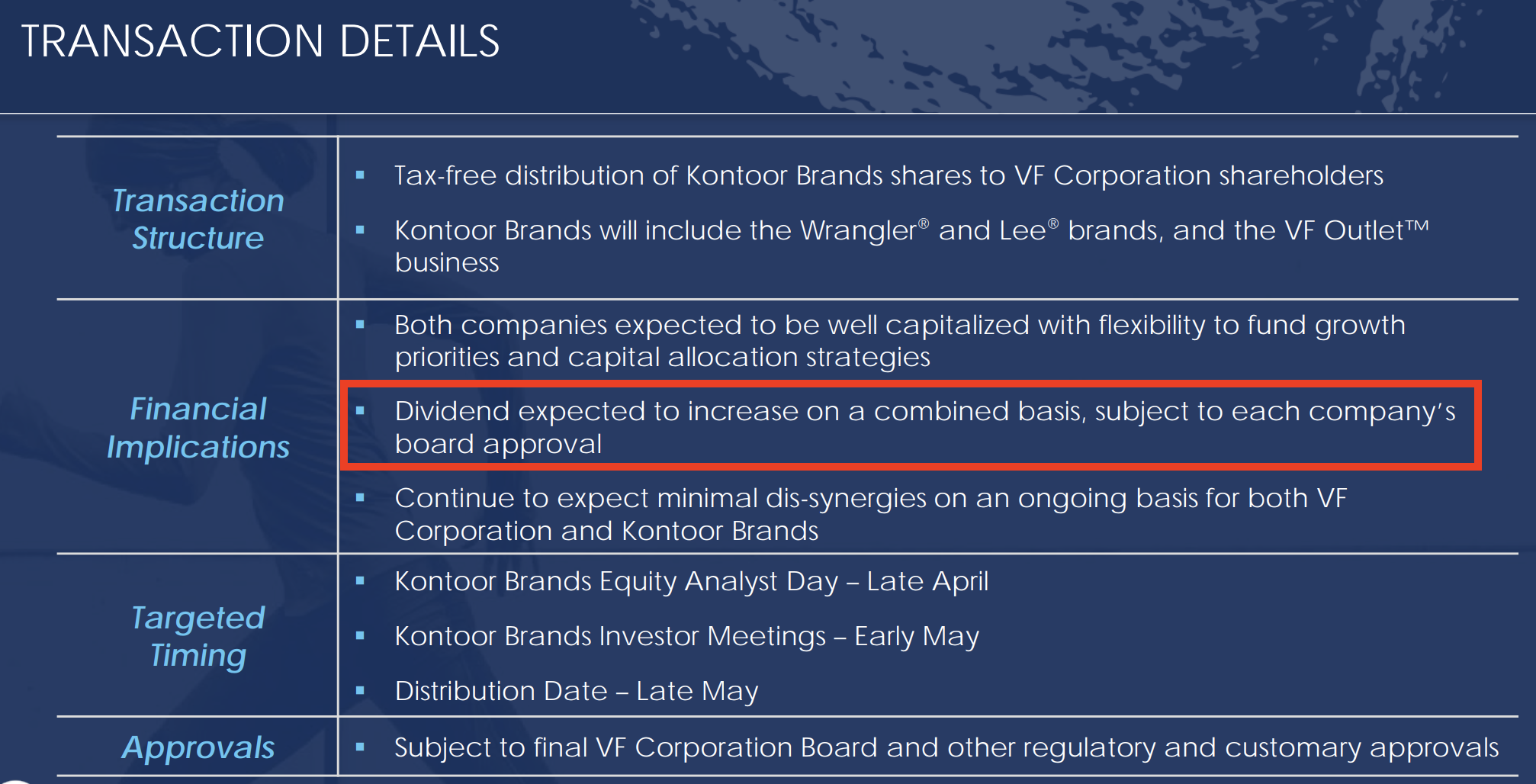

While V.F. Corp's new dividend rate is technically lower, investors didn't actually receive a payout cut. In May, V.F. Corp spun off its jeans business into an independent, publicly traded company called Kontoor Brands (KTB). VFC investors received shares in Kontoor, which also pays a dividend.

As management had previously communicated when the separation was first announced, the combined dividends from V.F. Corp and Kontoor equal the dividend V.F. Corp paid prior to the spinoff.

Source: V.F. Corp Investor Presentation

Here's what management said on the company's second-quarter earnings call this week (emphasis added):

"Consistent with our prior communication and disclosure, VFs dividend adjustment represents the recalibration of our dividend following the spinoff of Kontoor brands.

And as Kontoor announced yesterday, they intend to pay an initial quarterly dividend of $0.56 per share. When considering the Kontoor and dividend combined with our dividend of $0.43 per share, shareholders who hold both companies will receive a total distribution that is equal to the dividend they had with VF prior to the spinoff.

The dividend remains a key component of our long term TSR algorithm and we intend to grow our dividend consistent with earnings as we move forward." – CFO Scott Roe

The jeans business accounted for 18% of V.F. Corp's revenue and 14% of its segment profit last fiscal year. Spinning off this business into a new company reduced V.F. Corp's cash flow, which is why management lowered the firm's dividend by about 15% to keep the firm's payout ratio steady.

Again, shareholders need to remember that they received one share of stock in dividend-paying Kontoor Brands for every seven shares of V.F. Corp they held, so their total distributions remain equal to the dividends they were receiving from V.F. Corp before it shed its jeans business.

V.F. Corp chose to separate off its jeans business because it was pulling down the company's overall growth rate. The jeans division, which consists of the Wrangler, Lee, and Rock & Republic brands, experienced moderate revenue and profit declines in each of the past three fiscal years. Many consumers are ditching their denim for greater comfort, with the "athleisure" category growing rapidly.

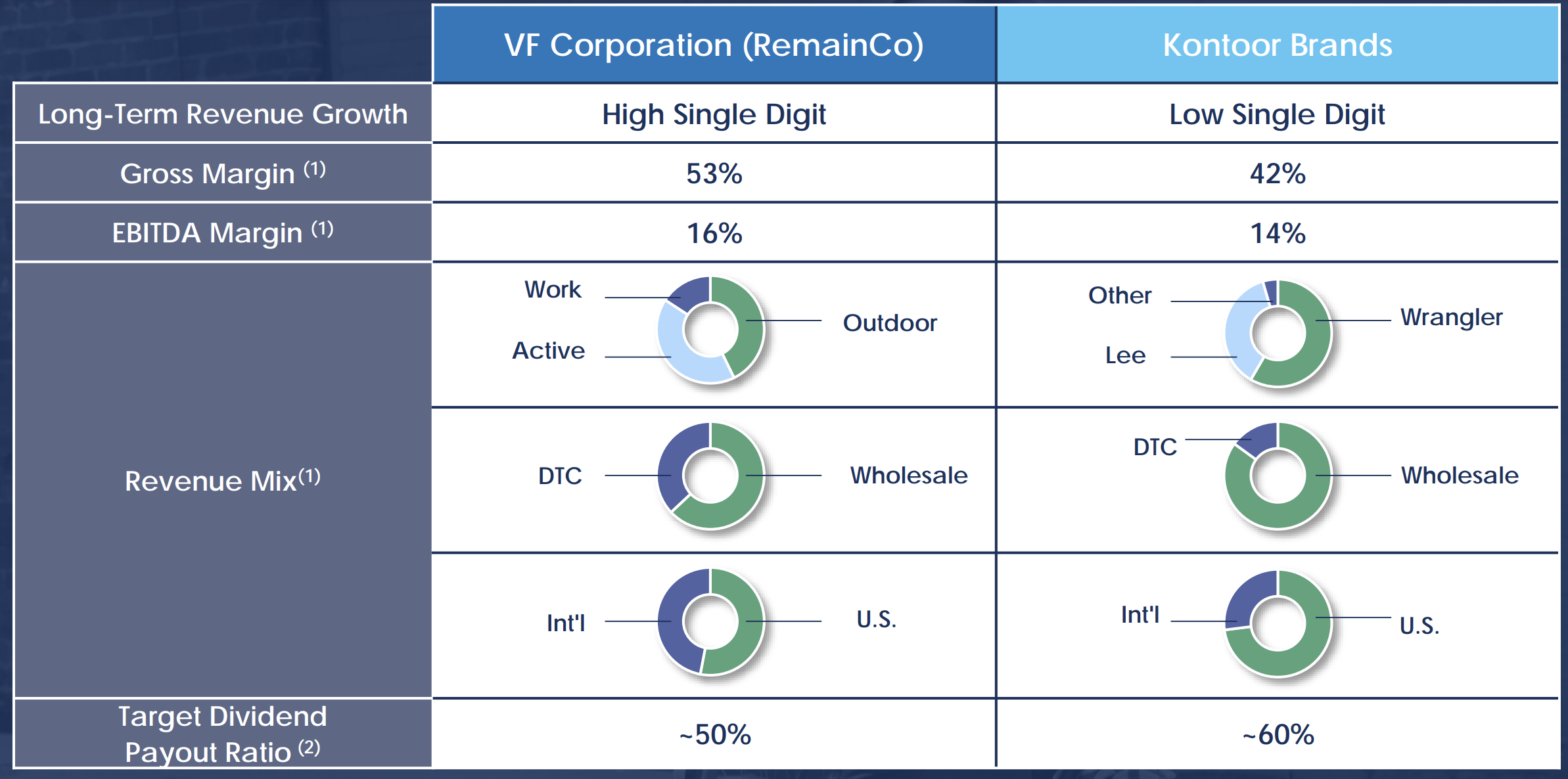

The remaining V.F. Corp is centered around four outdoor and activity-based lifestyle and workwear brands – Vans, The North Face, Timberland, and Dickies. Management expects these assets to generate high-single digit revenue growth going forward, while Kontoor Brands hopes to achieve low-single digit growth.

Source: V.F. Corp Investor Presentation

Essentially, V.F. Corp has become an even more attractive company with higher margins and a faster growth profile. Its dividend growth is expected to track earnings growth going forward, suggesting the firm has around 10% annual payout growth potential.

However, V.F. Corp's business has also become more concentrated in its remaining brands and product categories. But this looks to be a worthwhile tradeoff based on today's consumer preferences. Of course fashion styles change over time, but V.F. Corp has a 100-plus-year history of making timely acquisitions and divestitures that create long-term value.

The appeal of Kontoor Brands is less certain. Management has emphasized the firm's "strong dividend policy" and "compelling, durable, and consistent cash flow." However, there's a reason why V.F. Corp chose to separate this business – it's not as attractive as its other assets, and future growth is uncertain.

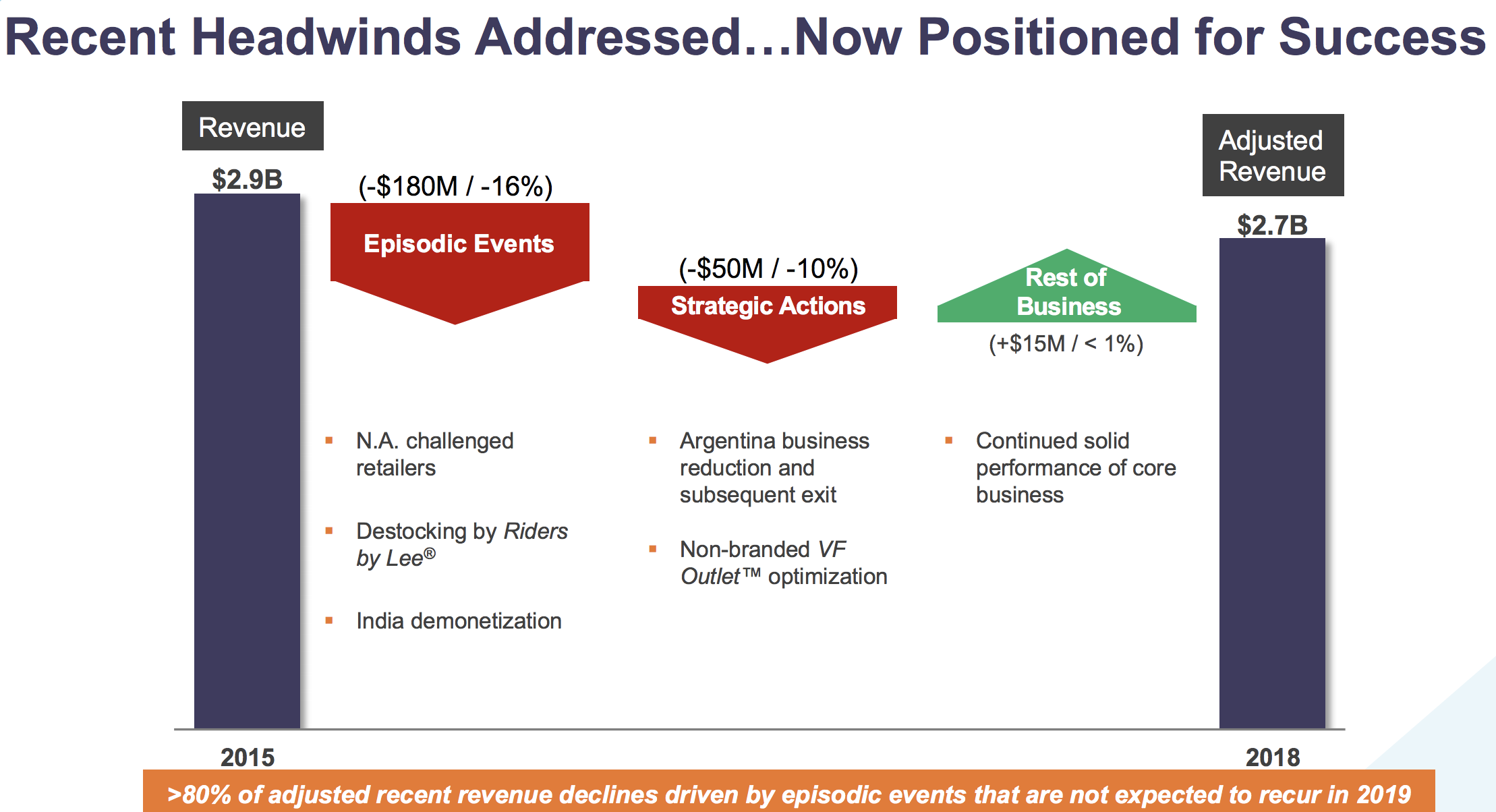

Kontoor argues that a combination of non-recurring factors are responsible for its lackluster performance in recent years, and better times are ahead. Management cited "challenged retailers" in North America, for example, and believes episodic events explain over 80% of the adjusted revenue decline Kontoor has experienced since 2015.

Source: Kontoor Brands Investor Presentation

Kontoor's finger-pointing feels like a bit of a stretch given the fast pace of change in retail. It seems more likely to me that jeans are just not as appealing for as many people as the athleisure trend accelerates, so growth will probably remain difficult going forward.

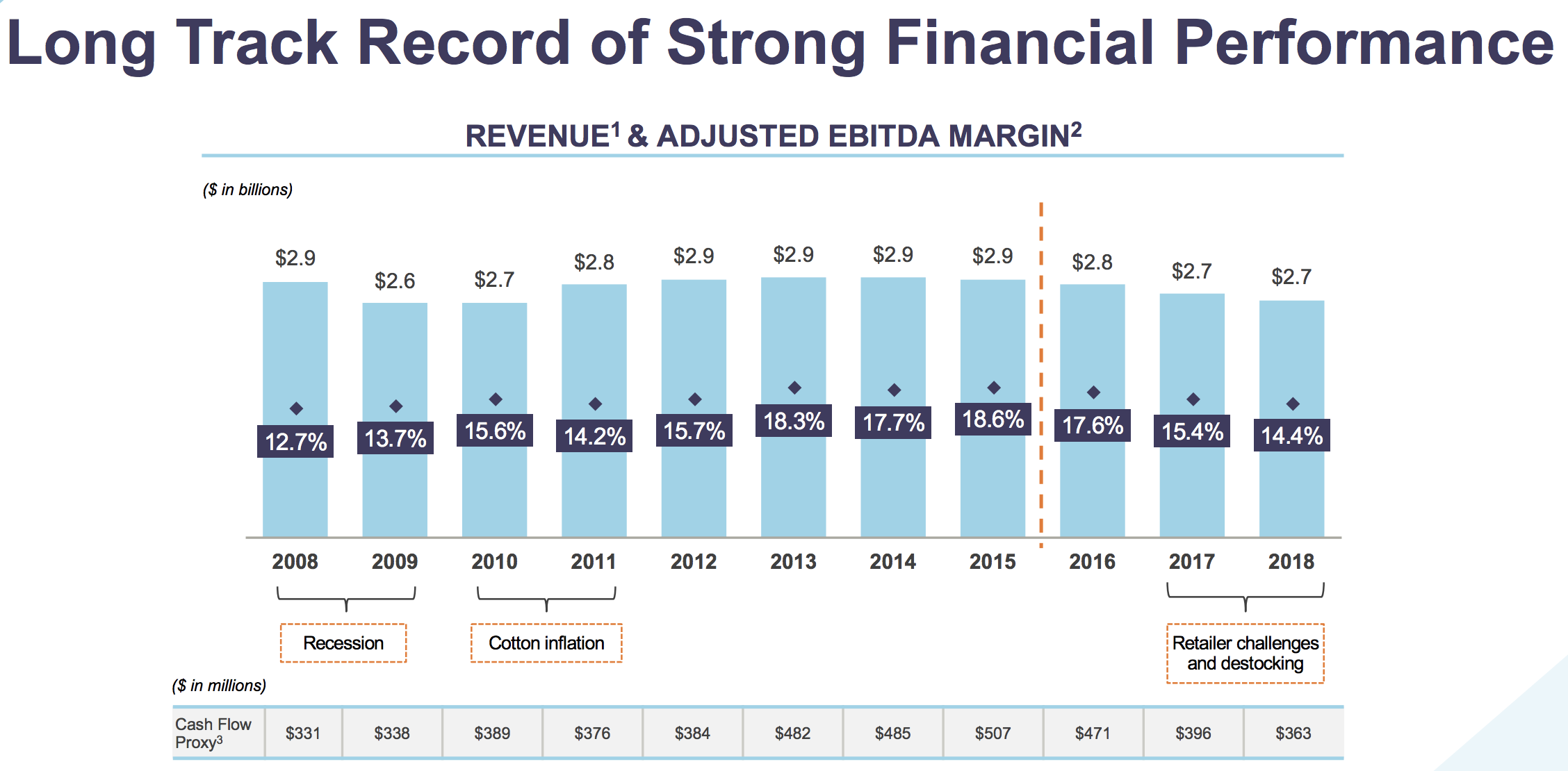

Despite Kontoor's sluggish growth and challenges, the business has at least generated reliable cash flow between $300 million and $500 million each year for more than a decade. With more focus dedicated to the business, management can hopefully pull some levers to get the margin a little higher, too.

Source: Kontoor Brands Investor Presentation

Kontoor's dividend will consume around $130 million annually, according to our estimates. Based on management's cash flow and capital expenditure guidance, the business could throw off between $250 million and $300 million in free cash flow, comfortably covering the payout.

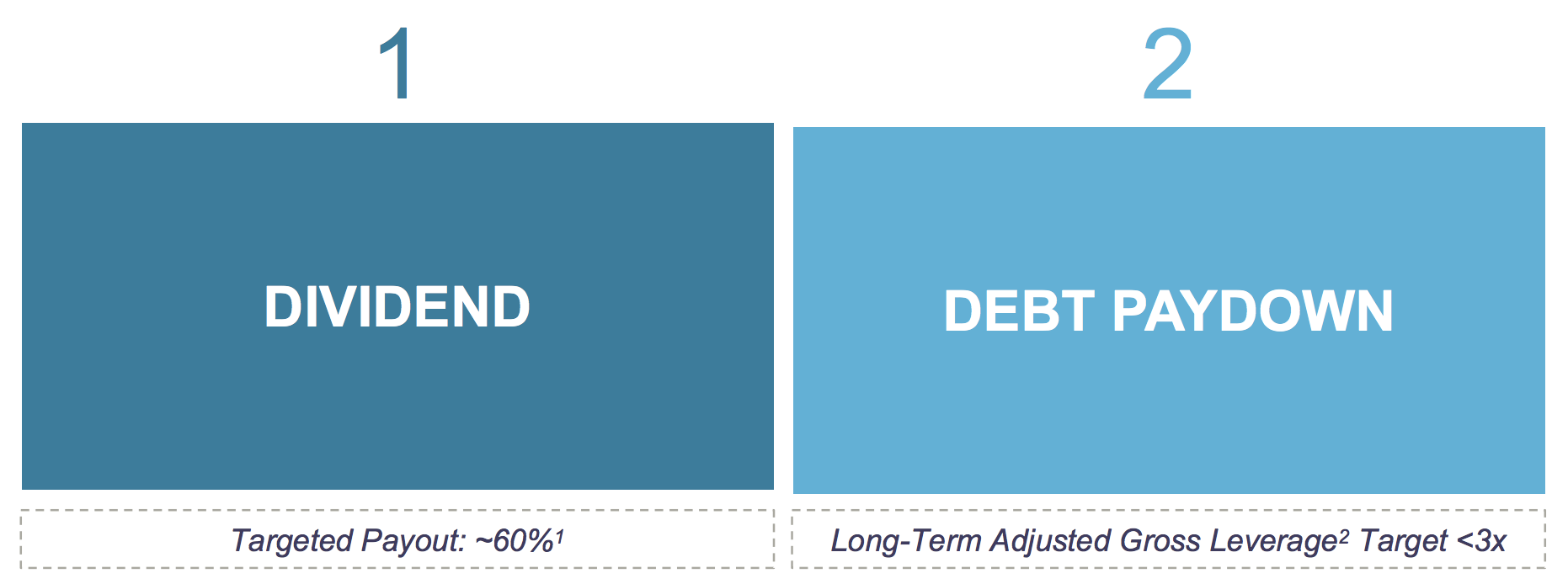

However, it's critical that Kontoor's payout ratio does not exceed management's 60% target level given the firm's leverage. Kontoor has a junk credit rating (BB-) from Standard & Poor's and carries a little over $1 billion in long-term debt, resulting in an initial adjusted net leverage ratio of 2.5x.

That's not an alarmingly high level for most businesses, but Kontoor has yet to prove it can generate profitable growth. The company is also concentrated in just one product category (jeans) and has some sensitivity to consumer spending.

For these reasons, management would like to maintain a healthy level of financial flexibility as they work on improving the business. As you can see, debt paydown is one of Kontoor's top capital allocation priorities.

Source: Kontoor Investor Presentation

Overall, while it's still early days, Kontoor doesn't look like a great stock for conservative income investors. The high yield is attractive, but it also reflects the company's growth challenges, operational risk as a standalone business, and somewhat elevated payout ratio and leverage profile.

My personal preference is to avoid most companies involved in apparel and consumer retail since fashion trends can change quickly. Kontoor's dependence on a single category, one that does not appear aligned with the latest consumer trends, further increases its risk profile.

Although Kontoor's dividend is likely to remain stable for now thanks to its decent cash flow and desire to attract an investor base, risk averse income investors may want to begin looking for replacement ideas.