In June 2015 our Long-term Dividend Growth portfolio initiated a position in MSC Industrial (MSM) at a price of $69.81 per share. MSM shares closed at $69.55 today, virtually unchanged from the date of our purchase and matching the price they traded at eight years ago in July 2011.

MSC Industrial hasn't lost us money, but the company's performance has been a major disappointment given the broader market's strong rally. Not even news of a 19% dividend increase today could help the stock overcome another weak earnings report, which pushed shares lower by about 4%.

Let's revisit why I initially bought shares of the stock, review the company's recent operating results, and gauge whether or not MSC Industrial remains a quality dividend growth stock that's worth holding for the long term.

Company-specific and Macro Headwinds Persist

MSC Industrial is one of the largest North American distributors of metalworking and maintenance, repair, and operations (MRO) products. The company has been in business for more than 75 years and offers over 1.7 million products, as well as inventory management and other services.

MSC serves individual machine shops, Fortune 100 companies, and manufacturers of all sizes. About 70% of its revenue comes from the manufacturing sector. The firm's products include cutting tools, measuring instruments, fasteners, janitorial supplies, power tools, electrical components, and other supplies.

Source: MSC Industrial Investor Presentation

MSC initially appealed to me because it was a simple business that sold timeless products and appeared to have a long runway for profitable growth.

Practically every industrial business has an ongoing need for the supplies MSC distributes. Working with multiple suppliers, tracking inventory, placing accurate orders, making costly one-off purchases, and storing products are all pain points MSC helps alleviate. Many of the firm's customers lack the resources to manage and monitor their MRO inventories effectively.

By touting these savings it can achieve for customers while focusing on higher-margin, lower-volume products, MSC could reduce its dependence on winning market share by simply offering lower prices than its rivals.

Source: MSC Industrial Investor Presentation

As one of the larger distributors in the market, MSC also possessed several benefits that seemed likely to provide the company with opportunities to achieve profitable long-term growth.

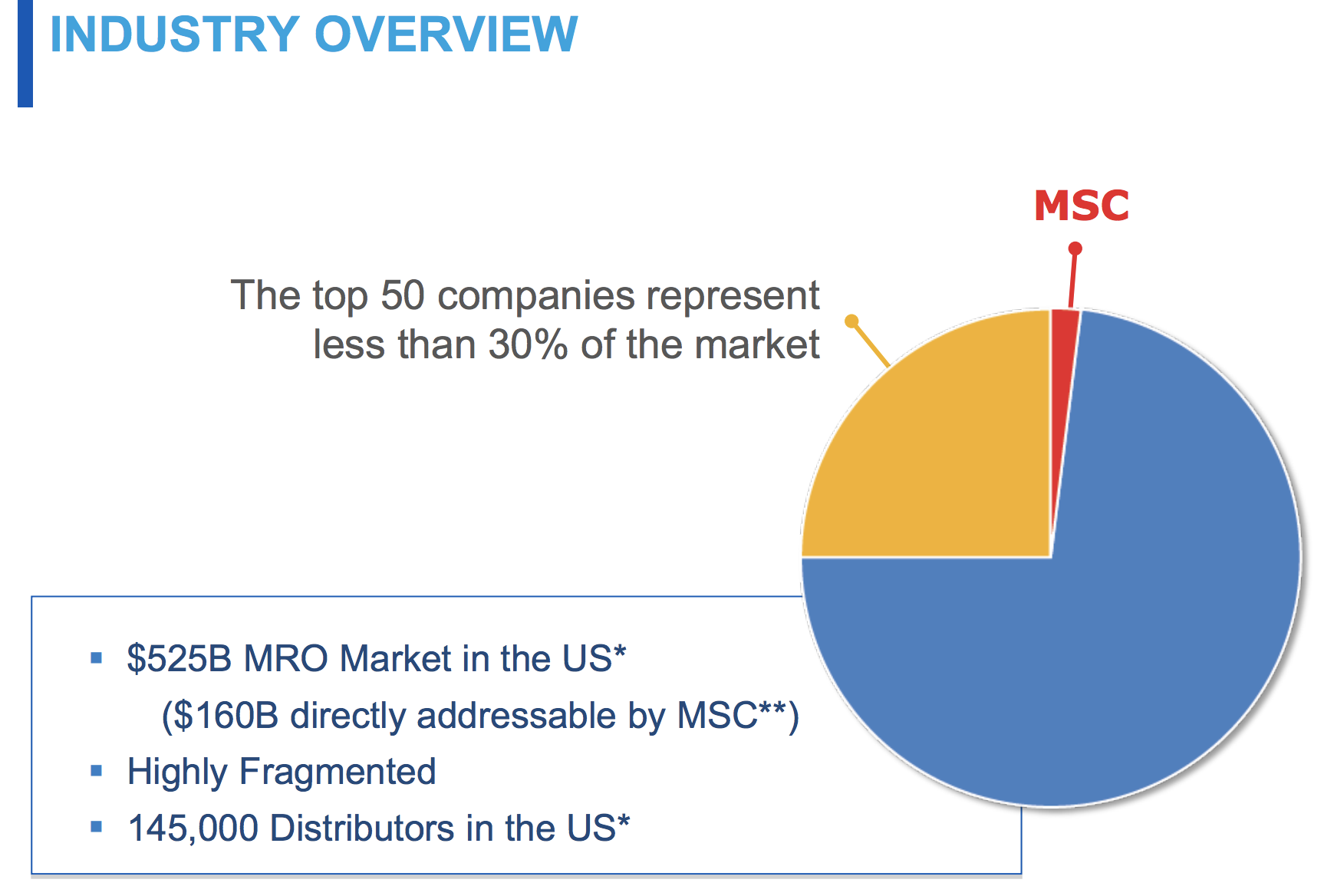

The U.S. MRO market exceeds $500 billion in size, according to a 2017 presentation by the company. However, the top 50 firms represent less than 30% of the market, and MSC is just a small slice of the pie.

Source: MSC Investor Presentation

MSC has stated that 70% of the market consists of local and regional distributors, which have much smaller scale than the company. In many cases they cannot match MSC's breadth of inventory, speedy fulfillment of orders (same-day and next-day delivery), competitive cost structure, or convenient online ordering (customers place more than 60% of their orders digitally through MSC's technology platforms).

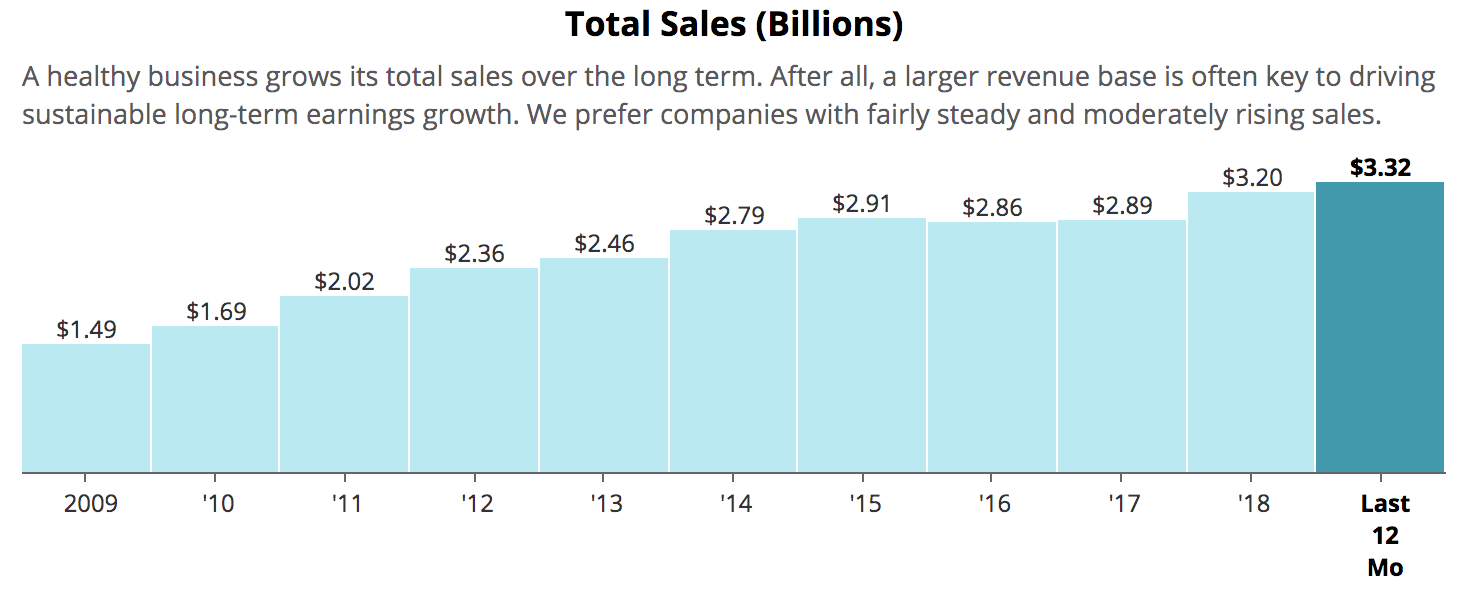

With the right execution, MSC seemed poised to take an increasing share of the market as smaller players were forced to consolidate. To an extent, that has happened. MSC's sales are up from $2 billion in 2011 to approximately $3.3 billion today, driven in part by acquisitive growth.

Source: Simply Safe Dividends

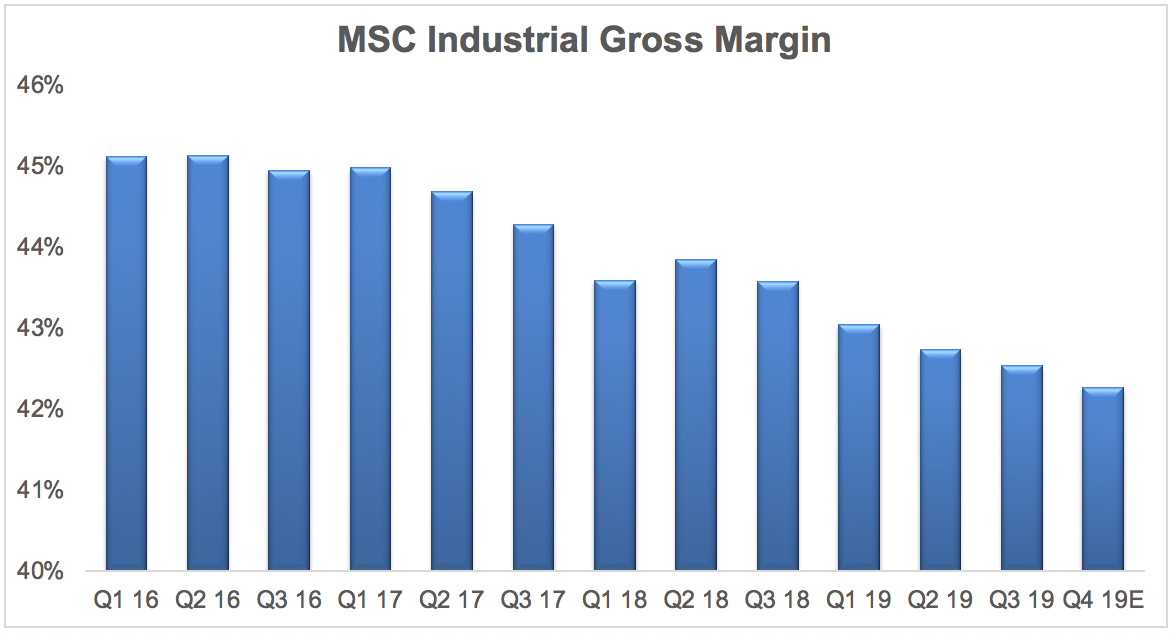

Unfortunately, during that period the company's operating margin has also declined from 17% to 14%, and MSC's continuous slide in gross margin raises some concerns about its management quality and long-term outlook for growth. If the business just isn't as good as I thought it was several years ago, I'm content moving on to greener pastures.

Source: MSC Industrial, Simply Safe Dividends

MCS's falling gross margin indicates that the gap between its selling prices and the cost of its products has narrowed. In other words, in recent years the firm's growing scale and expanding supplier base has not helped its profitability.

There could be many reasons for this. Perhaps the acquisitions the company has made are not providing as much value as expected. Maybe price transparency or competition is increasing as more orders move online. Or perhaps it's just the result of an unfortunate set of macro factors that will eventually reverse.

According to management, the latest margin disappointment was actually driven in part by the company's success in winning new accounts, which have not converted into revenue as quickly as expected. If the market believed this optimistic excuse, MSC's stock price would probably not be sitting at its 52-week low.

The bigger issue management discussed was a slowdown in demand, coupled with tariffs on the goods it buys from China. MSC sources about 10% of its products from China. Current tariffs are raising the cost of about half of those purchases, and the remainder will be hit as tariffs on lists 3 and 4 go into effect.

With the tariff rate on many of these goods rising from 10% to 25% earlier this summer, MSC expects the cost of its Chinese imports to rise significantly over the next year. If MSC is unable to be excluded from these tariffs or pass on some of the increase to its customers, its gross margin will likely remain under mild pressure for the foreseeable future.

Meanwhile, many of the manufacturers and metalworkers MSC works with are supposedly slowing their buying activity as they navigate through some of the uncertainties caused by the U.S.-China trade war.

Competitive intensity across the distribution landscape is especially high when demand conditions soften. Local and regional distributors will often use price as a lever to retain accounts when things get tight, and this seems to be affecting MSC's competitiveness as well.

I don't mind owning a company that's temporarily beaten down for reasons outside of its control. However, the last couple of years have raised some questions about MSC's overall business quality and management's ability to execute.

Speaking of leadership, it's worth noting that MSC's founding family controls the majority of the voting power, giving them full power over how the company is run. The son of MSC's founder, Sid Jacobson, is the Chairman of the board, and Sid Jacobson's grandson Erik Gershwind took over as CEO in 2013.

That's not to say Mr. Gershwind is unqualified. After all, he's been with the company since 1996 and graduated near the top of his class at both the University of Pennsylvania and Harvard Law School.

However, nepotism still bothers me, and MSC's unexpected decision today to boost its dividend by 19% feels like a desperate move to try and appease shareholders. Management also said they planned to raise their hurdle rate for acquisitions as they focus more on addressing internal performance issues:

"In response to near-term trends, we have implemented a three-part action plan to 1) improve field sales execution and accelerate new account implementation; 2) increase profitability of our supplier programs; and 3) drive increased expense control and productivity." – CEO Erik Gershwind

If nothing else, MSC's ongoing string of disappointing results suggest this business may not be as strong as I initially believed back in 2015. The company is struggling to push through price increases, its acquisitions have not delivered clear value, and the shift in capital allocation priorities to return more cash to shareholders rather than invest for growth suggests its best days could be behind it.

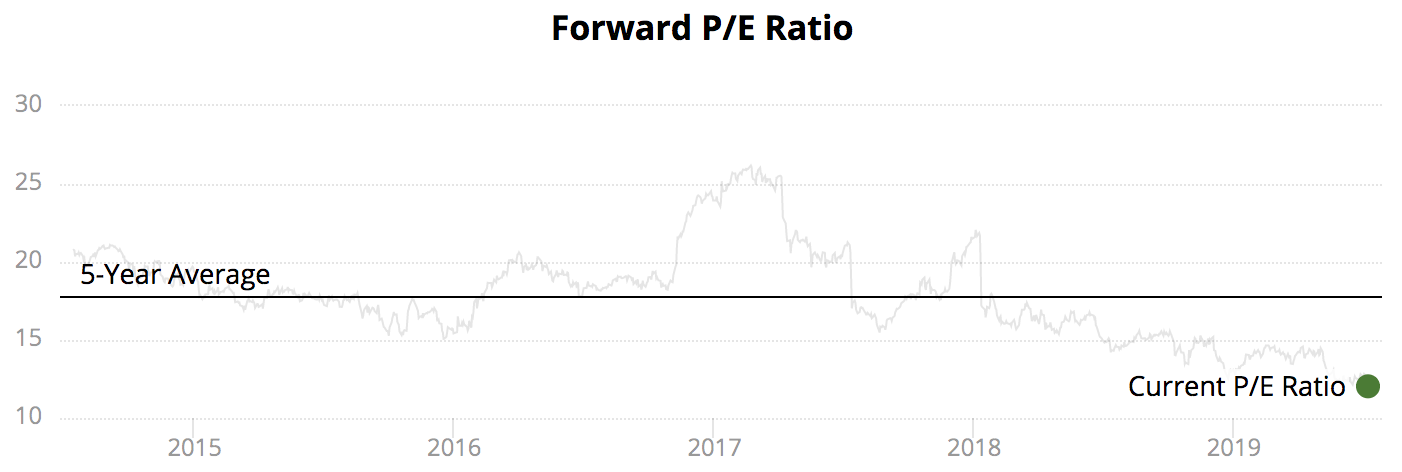

With that said, expectations do look low. Shares of MSC now sport a safe 4% forward dividend yield and a forward P/E ratio of just 12.0, well below their five-year average of 17.8. The company's repeated earnings misses, coupled with tariff-related challenges, have lost it credibility with investors. It will likely take time and better internal execution to start regaining trust.

Source: Simply Safe Dividends

I plan to take a wait-and-see approach with MSC over the next few quarters and would be open to upgrading into a higher quality company if MSC's valuation strengthens. I believe a number of macro headwinds have legitimately made the operating environment harder for the firm in the short term, but I also prefer owning companies that have more within their control and clearer long-term growth prospects.

The good news for income investors is that MSC's dividend continues to look safe. The firm's forward payout ratio will sit a little below 60% after today's raise, and MSC should continue generating solid free cash flow while maintaining a healthy balance sheet. However, given the payout ratio, which is on the high side for an industrial firm, it's hard to imagine future dividend increases exceeding a low- to mid-single digit pace until profitability improves.