Lowe's Long-term Outlook Appears Intact Despite Recent Weakness

Shares of Lowe's (LOW) have slumped more than 15% since the home improvement retailer released earnings on May 22, including the stock's worst-ever single-day loss of 12%.

The market is notorious for overreacting to short-term results, even for quality dividend kings such as Lowe's. However, the world of retail is also evolving as e-commerce and trade wars could force a record number of store closings this year.

Whenever one of my holdings experiences an unusually large decline, I like to investigate the situation to try and assess if I might be missing anything. Let's take a look at why the market was so disappointed with Lowe's and why the firm's long-term outlook appears to remain intact.

For context, recall that Home Depot (HD) has posted better results than Lowe's for several years. As a result, last year the retailer decided to shake up its management team with hopes of delivering stronger performance, naming former Home Depot executive Marvin Ellison as its new CEO in May 2018.

Besides hiring Ellison, Lowe's revamped management team includes three new board members, a new CFO from CVS, a new supply chain head who previously worked at Walmart, a new head of merchandising, a new head of stores with experience at Home Depot, and almost complete turnover of its merchandising executives.

On the bright side, these changes helped Lowe's record 3.5% same-store sales growth last quarter, outpacing Home Depot's 2.5% growth for the first time since 2016, according to The Wall Street Journal.

However, Lowe's also encountered several challenges that led management to cut fiscal 2019 guidance. While the firm's 3% same-store sales growth target was maintained, its full-year adjusted EPS guidance was reduced by about 8% at the midpoint, and its operating margin expansion target was reduced.

The revised guidance was mainly due to severe margin compression which, according to CEO Marvin Ellison, was the result of several factors:

"The unanticipated impact of the convergence of cost pressure, significant transition in our merchandising organization, and ineffective legacy pricing tools and processes led to gross margin contraction in the quarter which impacted earnings...We are still in the early stages of our transformation."

Some of these issues were outside of management's control, such as trade tariffs pressuring Lowe's costs. However, investors likely believed the company's turnaround plan was further along than it was.

Given the relatively early stage of Lowe's turnaround plan, I'm not very alarmed by one disappointing quarter. Few success stories are linear in nature, and 90 days of results is not much time to measure anything, especially in the volatile retail world.

The main issue to watch going forward is Lowe's ability to restore its margins, either through increasing its prices on inelastic products or taking costs out in different areas of its business.

As The Wall Street Journal noted, "Lowe's merchants agreed to price increases from some vendors last year without finding ways to make up for those cost increases elsewhere in the business."

With more spending shifting to online channels, which tend to be more transparent and easier to price-shop, Lowe's will need to show that this recent drop in profitability is truly just a short-term operational blip rather than a bigger issue.

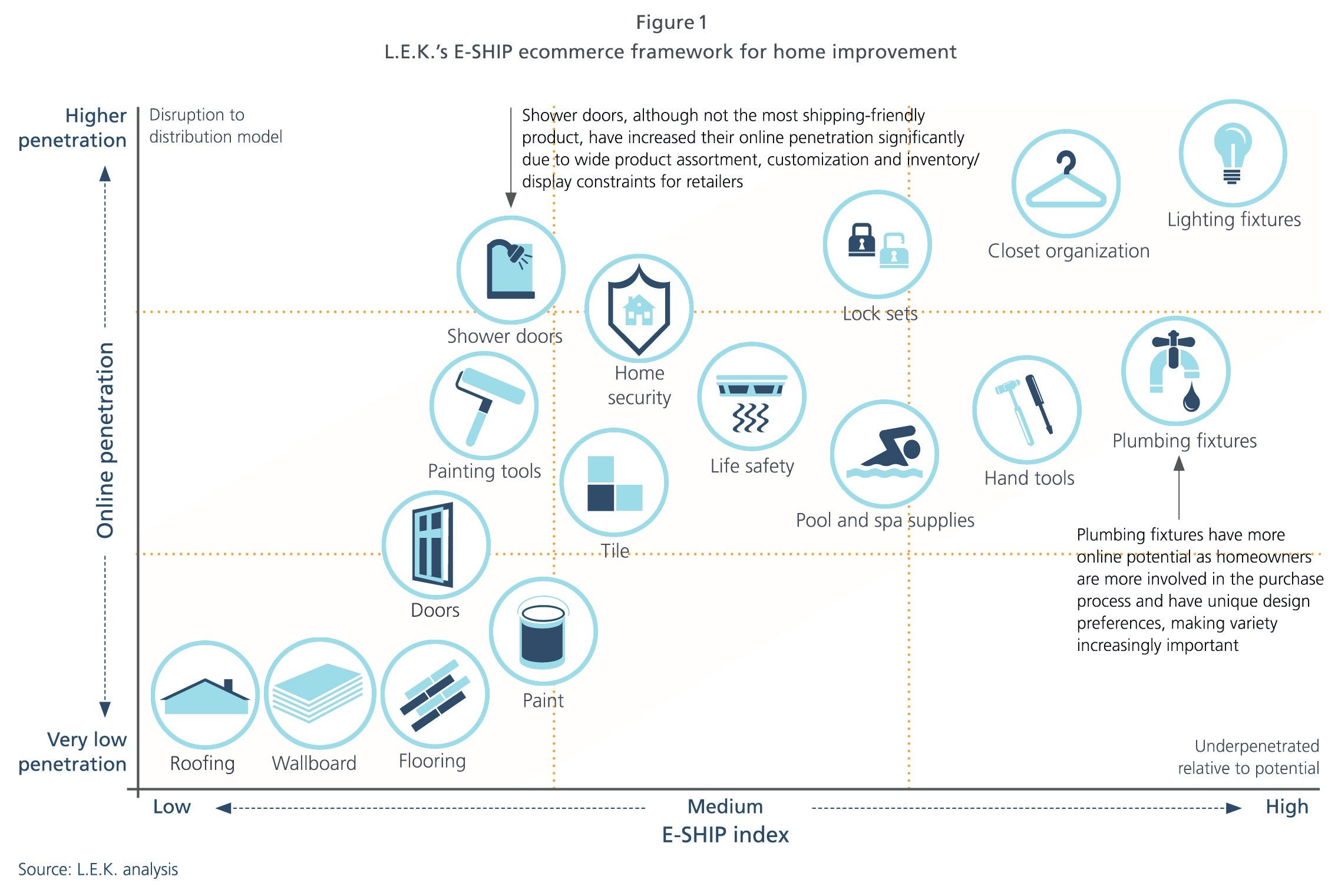

After all, parts of the home improvement market are changing. L.E.K. Consulting estimates that Amazon's home improvement business was possibly larger than Menards in 2018, for example. They also highlighted how some home improvement product categories are more vulnerable to online shopping than others.

Source: L.E.K. Consulting

For now, Lowe's deserves the benefit of the doubt. The company is investing significantly in its own omni-channel initiatives, which are expected to account for close to half of Lowe's capital expenditures going forward, and its digital sales continue growing at a double-digit pace.

Many of the long-term pricing, cost-cutting, merchandising, and efficiency programs management wants to put in place will take time to implement and deliver results, especially given the sweeping leadership changes Lowe's made.

In fact, some of the firm's new executives have been at Lowe's for just six months, and transitioning work across a supply chain that spans over 1,700 stores and generates more than $70 billion in annual revenue is no small task.

Describing the transition from legacy merchants to new merchants, Lowe's CEO said there "was much more disruption" than the firm anticipated. The company's new merchants "did not have a clear line of sight to the cost increases that were accepted by prior merchants," so they could not "quickly analyze and offset these cost increases with appropriate pricing action."

Such a sweeping overhaul of the company's logistics and omni-channel operations is going to be a lumpy process, not one that flows seamlessly and smoothly at all times.

However, as CEO Ellison said on the earnings call, they have taken "more aggressive steps to make sure we analyze, review, and do systematic reviews of every single thing we can imagine so as not to have another unexpected event like we experienced" in the first quarter.

Looking further out, Lowe's turnaround is expected to take five years and include every part of its business. In effect, Lowe's is waging a multi-front war on inefficiency as it takes on the largest corporate shake-up in the company's history.

Investments exceeding $1 billion will be targeted at revamping the efficiency of Lowe's supply chain and improving its omni-channel operations. Increasing the time associates spend with customers and growing sales from contractors, who are more loyal and make bigger purchases, are key focus areas as well.

Source: Lowe's Investor Presentation

Management believes that its efforts will result in significantly improved sales per square foot (up from $335 in 2018 to $370 in the long term) and much higher operating margins (up from 9.3% in 2018 to 12% in the long term).

Should Lowe's succeed in these efforts while maintaining its pace of share repurchases, then the company has potential to continue driving double-digit average annual EPS and dividend growth like it has done for many years.

Overall, Lowe's recent slump looks more like noise than news for long-term investors, though it could take several additional quarters for the company's new executives to get the business firing on more cylinders. Some patience could be required in the meantime, especially if economic growth slows (home improvement retailers are not among the best recession proof dividend stocks).

However, Lowe's ultimately seems likely to grow its earning power over time as it wrings out various inefficiencies and continues adapting its business model to meet the rise of online shopping. The company appears to remain a solid choice for long-term dividend growth investors, and its current valuation looks reasonable.