PetMed Express (PETS) reported disappointing earnings on May 6, causing the firm's Dividend Safety Score to fall from our lowest "Borderline Safe" rating into the "Unsafe" bucket.

A low score does not necessarily mean a dividend cut is imminent. However, these companies have higher risk of reducing their payouts in the future and often depend on favorable business, financial, and economic conditions to maintain their dividends.

Let's review the unfavorable change in PetMed's long-term outlook.

PetMed's Dividend Safety Founded in 1996, PetMed claims to be the largest pet pharmacy in America. The firm delivers prescription and generic pet medications for dogs and cats straight to consumers' homes. Approximately 85% of its sales are generated through its website, with the remainder via phone orders and direct mail.

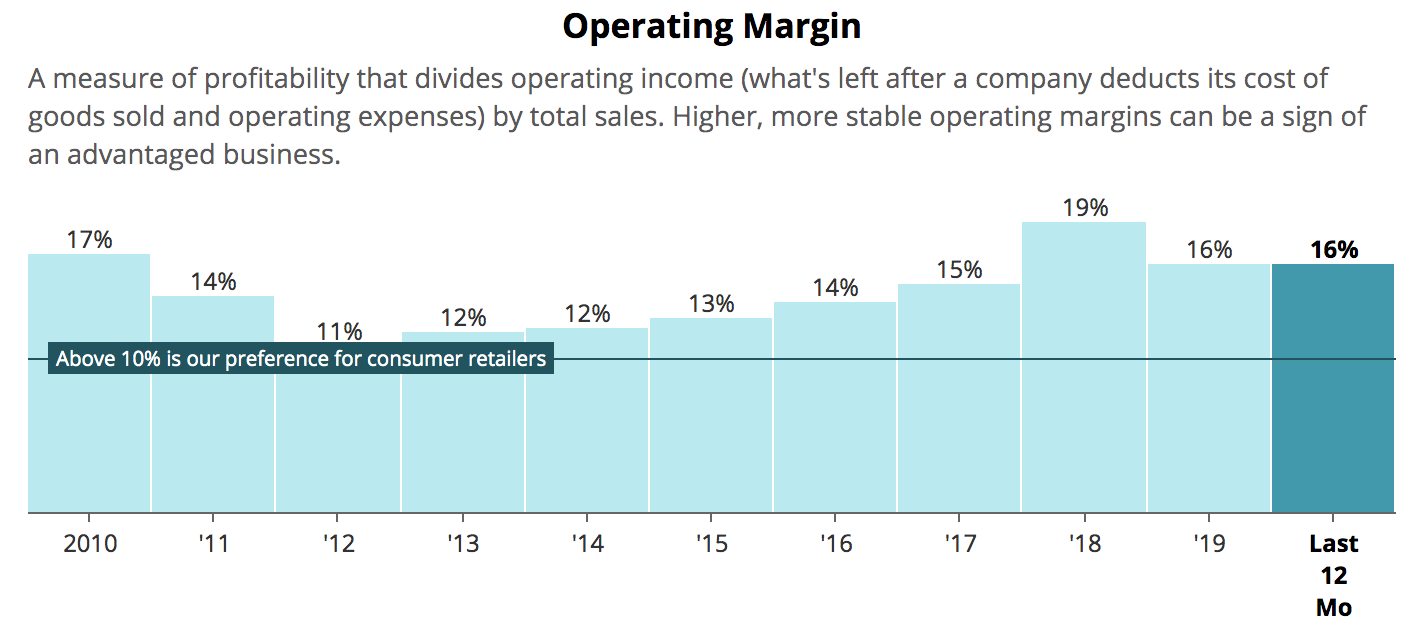

Unlike many e-commerce operators, PetMed runs its business for a profit rather than pursuing growth at any cost. As you can see, for years the firm generated a double-digit operating margin.

Source: Simply Safe Dividends

Unfortunately, more growth-hungry competitors are emerging, and they aren't so concerned about generating profits today. Instead, they want to take as much of the market as possible, spending large sums to acquire and retain customers.

Most notably, in May 2017 PetSmart acquired online pet retailer Chewy.com for $3 billion. At the time, Chewy.com dominated the pet food market but has since rapidly expanded its business.

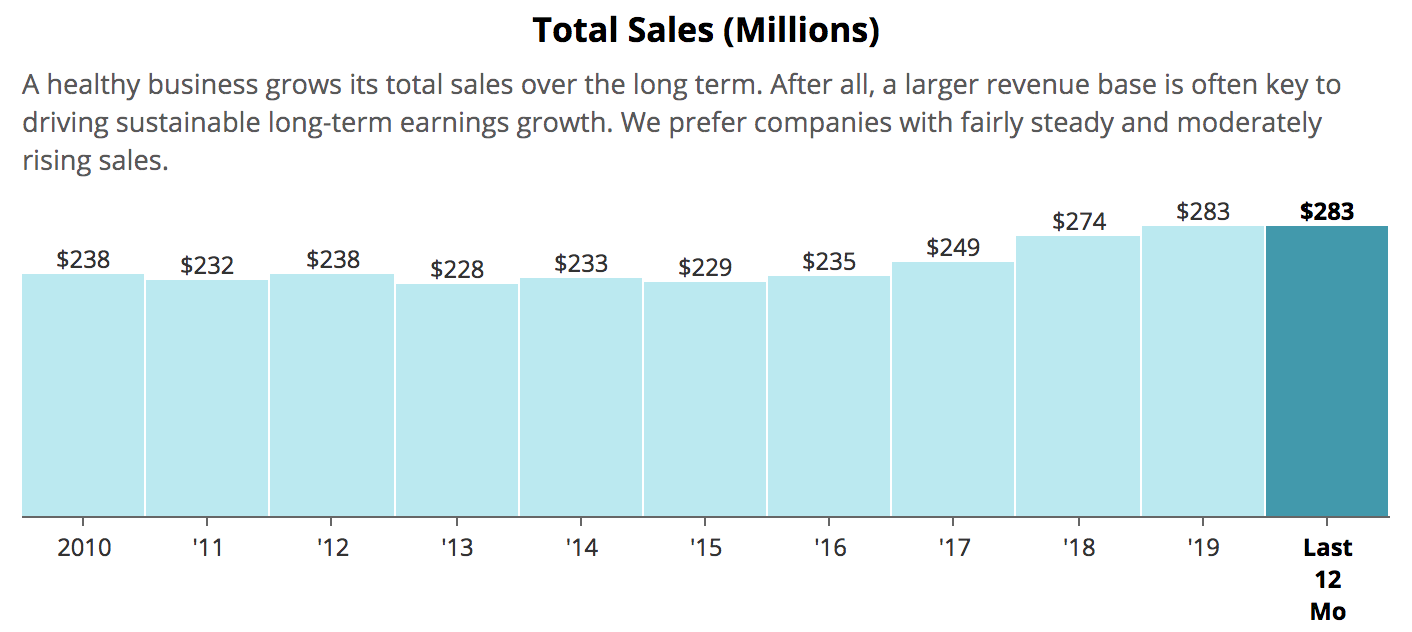

In fact, the firm's revenue increased from nearly $900 million in 2016 to $2.1 billion in 2017 and $3.5 billion in 2018. For comparison, PetMed's annual revenue totals about $280 million and hasn't increased much over the past decade.

Source: Simply Safe Dividends

Unfortunately, Chewy.com decided to launch its own online pet pharmacy in July 2018, encroaching on PetMed's turf.

With the backing of hundreds of millions of dollars of private equity and venture capital financing, Chewy.com ran its business focused on growth rather than profitability; despite delivering over $3 billion in 2018 revenue, Chewy.com lost $268 million.

Simply put, PetMed's margin has become Chewy.com's opportunity. Companies with strong brands can fight off competition, but it's appearing more likely that PetMed has no enduring moat in this space.

The firm's retail customers want products that solve the issues ailing their pets, and they want them to be affordable and convenient. PetMed is just an intermediary, and customer loyalty appears low.

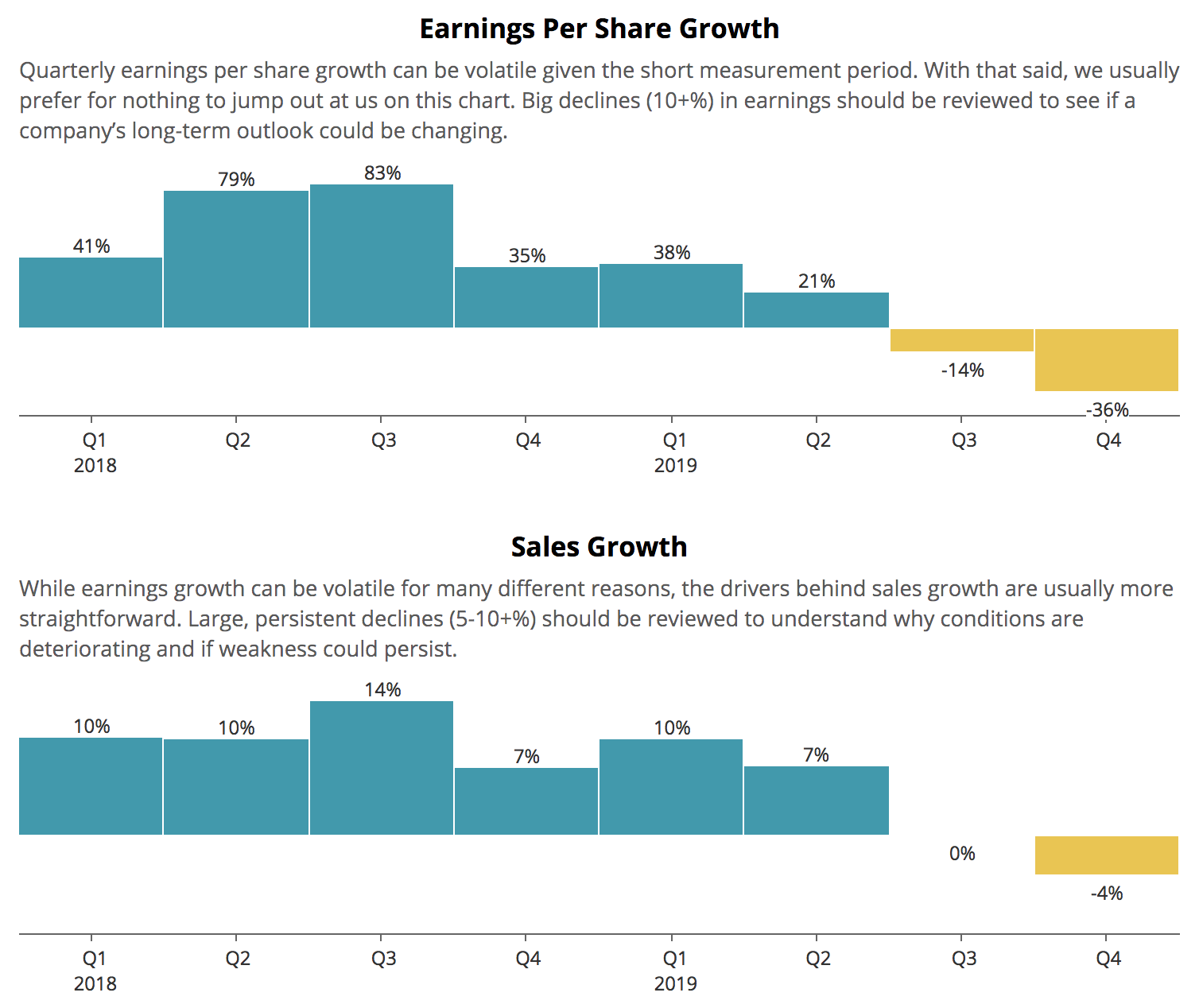

Increased competition from Chewy.com and other online rivals caused PetMed's sales to decline 4% last quarter, and its earnings plunged 36%.

Source: Simply Safe Dividends

Management cited a 15% decrease in new order sales (due to lower prices) and feels a greater urgency to ramp up advertising spending in an effort to hold market share.

In fact, PetMed said its advertising cost of acquiring a customer last quarter (defined as total advertising expenses divided by total new customers acquired) jumped to $65 compared to $38 for the same quarter as the prior year.

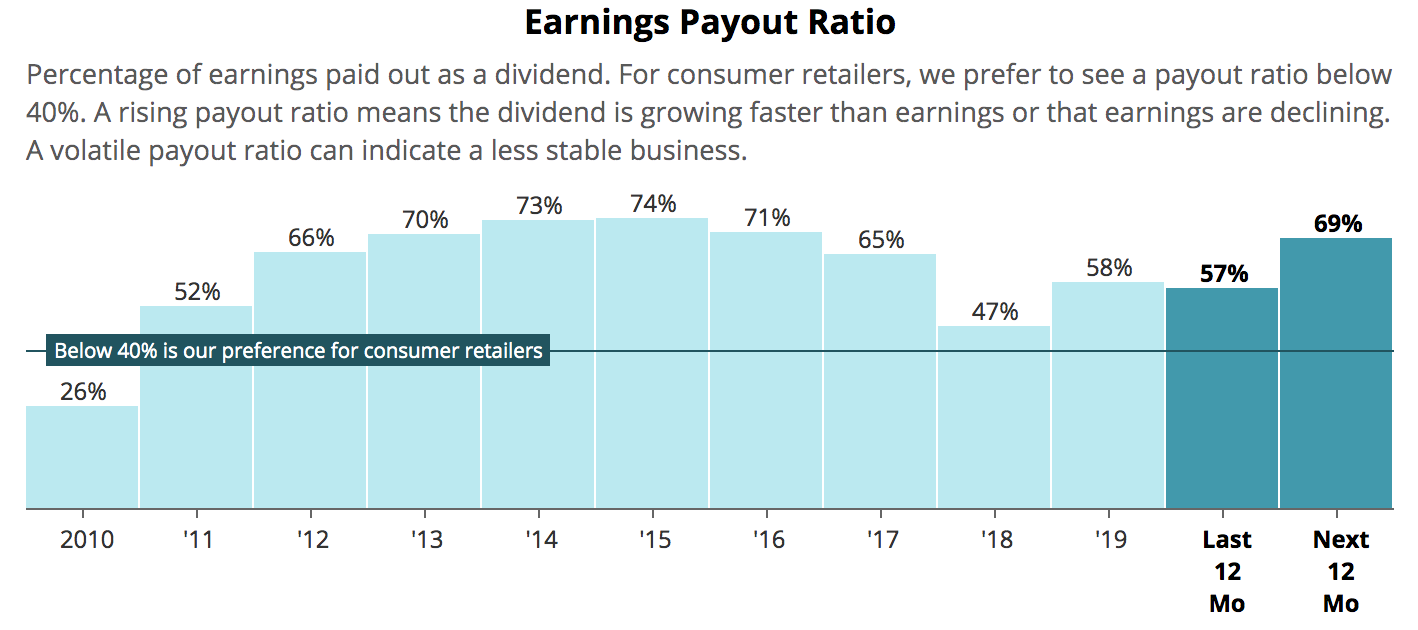

Thanks to higher spending and falling sales, the firm's gross margin fell from 37% to 32%, and profits are expected to remain under pressure. As a result, PetMed's payout ratio is expected to increase to nearly 70% over the next year.

Source: Simply Safe Dividends

PetMed's payout ratio has been even higher in the past, topping out near 75% in 2015, but the competitive landscape appears to be much more intense today. It's hard to imagine the company's profitability improving anytime soon. PetMed's CEO Menderes Akdag even made the following remark on the firm's earnings call:

"We anticipate continuing pressure on gross margins, and it's going to depend on the competitiveness of the markets. We'll see where it ends up."

The news got worse yesterday when Walmart announced that it, too, would launch its own online pet pharmacy, WalmartPetRX.com. In its press release, the company stated (emphasis added):

Millennial dog owners, for example, spend up to $1,285 a year on their furry friends, with the majority of spend going towards vet care and vaccinations, food and supplies. We’re about to bring that cost down.

With massive scale, free two-day shipping on orders over $35, and the fact that 90% of Americans live within 10 miles of a Walmart store, Walmart's entry into the market isn't good for the industry's competitive landscape.

Walmart plans to offer "low cost pet prescriptions" for dogs, cats, horses, and livestock from more than 300 brands. The company listed conditions like flea and tick, heartworm, and others that are PetMed's main focus. Walmart will also expand its number of in-store veterinary clinics, with ambitions to reach 100 locations within 12 months.

Simply put, PetMed's historical advantages in terms of convenience, price, and speed of delivery seem likely to continue being eroded by larger, more well-capitalized rivals such as Chewy.com, Walmart, Amazon, and others.

Given the company's relatively small size, management could eventually decide to reduce PetMed's dividend to redirect more capital towards growth initiatives.

The firm's dividend consumes about $22 million annually, a meaningful sum. For perspective, that's the same amount of money PetMed spent on advertising last year, which accounted for roughly 8% of its revenue.

With analysts estimating that PetMed's earnings will decline 15% next year as management ramps up advertising spending to protect market share, the dividend will consume about 70% of the firm's profits. That's up from 55% prior to this week's earnings report.

In other words, the company's margin of safety is shrinking. With PetMed's rivals willing to forgo profits, how high of a profit margin can the company realistically continue to maintain if this environment persists? Should PetMed's operating margin get cut in half to 8%, its dividend would no longer be covered by earnings.

Fortunately, PetMed still has an excellent balance sheet which buys it more time to try and stabilize its business. The company holds about $100 million in cash and has no debt.

From a purely financial perspective, for now PetMed can continue paying its dividend without worrying about stepping up its advertising spending and lowering its prices to be competitive, within reason.

However, as a relatively small business that has paid dividends for less than a decade, management may decide to adjust the firm's capital allocation priorities as it adapts the company to an increasingly competitive online retail world. Differentiating itself from Chewy.com, Walmart, and others won't come cheap, and reducing the dividend would free up a meaningful amount of capital.

For these reasons, plus the conservative, long-term view our scoring system takes, PetMed's dividend profile looks riskier compared to other companies. A dividend cut doesn't seem imminent given the firm's solid balance sheet and sub-100% payout ratio, but pressure is quickly mounting on the company to adapt.

Even if the dividend remains safe, it's hard to find a compelling reason why PetMed can be a larger and more profitable business over the next decade. There doesn't seem to be much of a moat in the online pet pharmacy market. Conservative income investors may prefer to look elsewhere.