Thoughts on AbbVie's Underperformance and High Yield

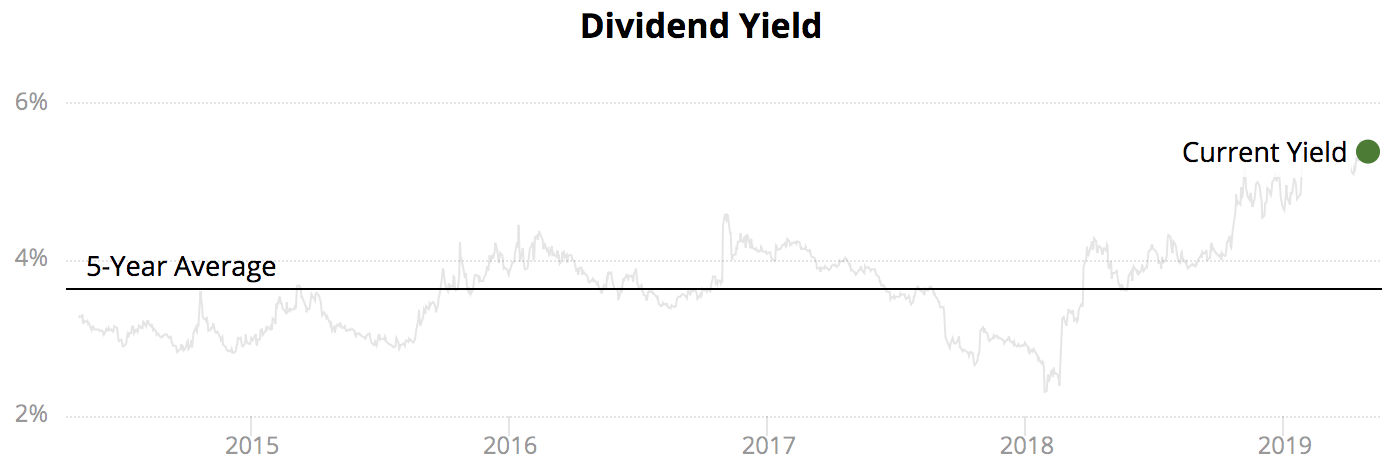

Despite raising its 2019 guidance last week, shares of biotech giant AbbVie (ABBV) remain mired in a bear market and sit almost 40% below their all-time high set back in early 2018. The stock's 5.4% dividend yield is also at an all-time high, causing some investors to worry that AbbVie's dividend might no longer be safe.

Source: Simply Safe Dividends

Let's review AbbVie's latest results to assess whether or not the firm's dividend still looks safe and if the company's seemingly cheap valuation appears justified.

Why The Market Remains Spooked About AbbVie Healthcare stocks, in general, have had a rough few months due to increased regulatory and political concerns that are possibly being heightened by the 2020 campaign season ramping up.

Specifically, presidential hopefuls on the Democratic side are talking about "Medicare for All," a single-payer health system in which every American would get insurance from one government plan.

Meanwhile, political pressure on drug prices continues to mount, creating some uncertainty around the long-term profitability that drugmakers can achieve.

Your guess is as good as mine regarding how these risks will ultimately play out. They are largely outside of AbbVie's control and highlight some of the challenges involved with investing in a complex industry that can be heavily influenced by external forces.

For now, it's just too soon to say what will happen. Maintaining reasonable position sizes, diversifying across various sectors, and sticking with companies that have strong balance sheets and diversified operations seems most prudent.

Looking more closely at AbbVie, the stock's performance in recent months actually hasn't been any worse than most healthcare stocks. However, there are several company-specific reasons why the firm's shares have struggled so much over the past year.

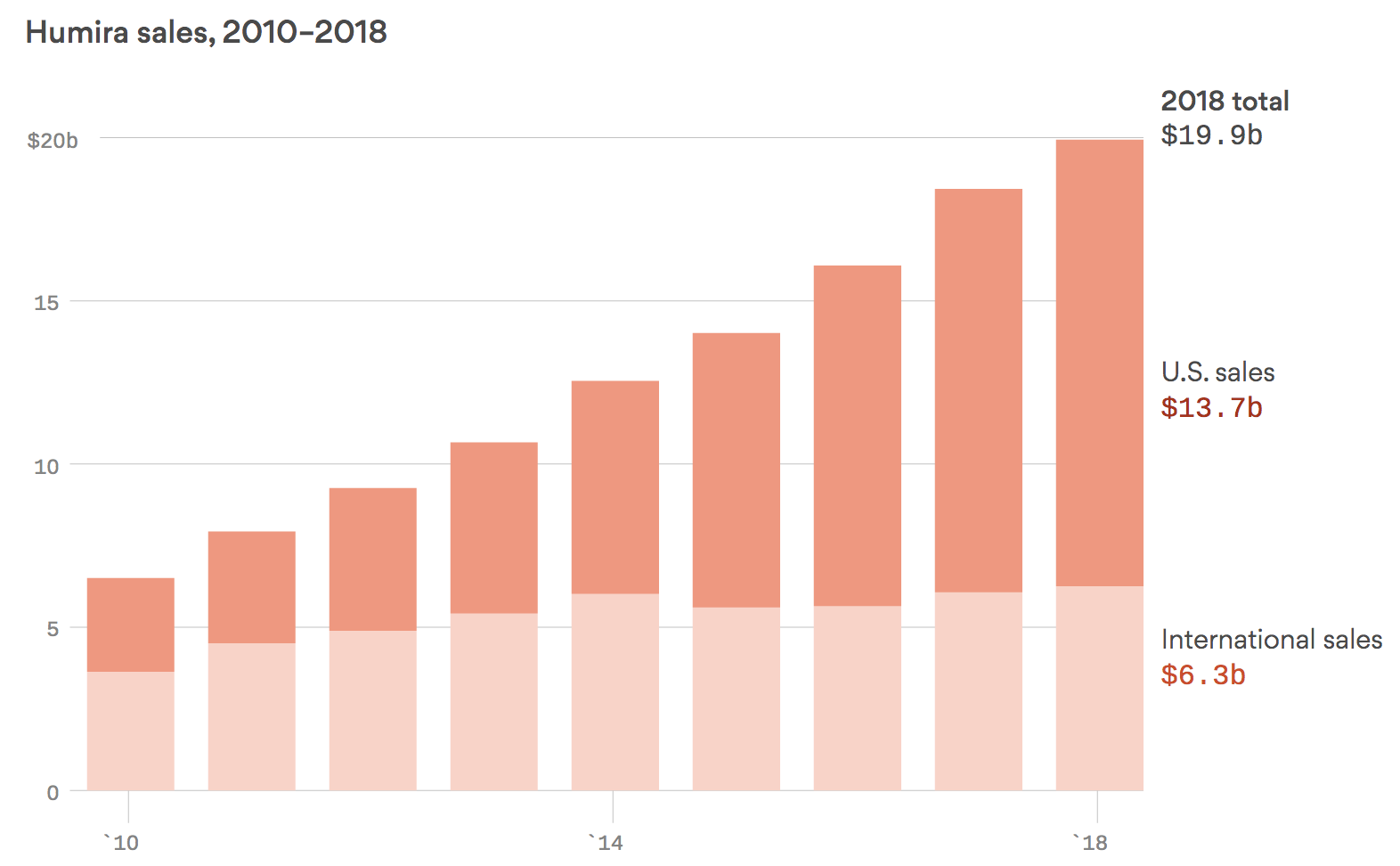

Most importantly, investors remain worried about AbbVie's blockbuster drug Humira, which treats autoimmune diseases such as arthritis and psoriasis. Humira sales rocketed from around $7 billion in 2010 to nearly $20 billion in 2018.

Source: Naema Ahmed / Axios

In the first quarter of 2019 that one drug accounted for 57% of AbbVie's revenue and over 70% of its operating profits. However, global Humira revenue declined 3.8% operationally, marking its first year-over-year fall in at least eight years, according to Bloomberg.

While Humira's success has generated massive profits for AbbVie over the years, in 2018 the drug's patents expired in Europe, and in 2021 it loses patent protection in most major markets outside the U.S. and Europe.

In 2023 Humira loses patent protection in the U.S. and management has said that no less than six biosimilar rival drugs will hit the market that year. Whenever biosimilars (generic versions of biological drugs) arrive drug companies typically see market share and pricing power fall significantly.

For example, AbbVie expects 2019 international Humira revenue to decline 30%, driven by biosimilar competition outside of the U.S. As more patents expire in 2020 and 2021, plus the big patent cliff in the U.S. in 2023, many analysts are projecting double-digit annual Humira declines for the foreseeable future.

Of course, Humira's inevitable decline has been known for a long time. That's the nature of the industry. AbbVie CEO Rick Gonzalez even said on the company's last earnings call that the company has planned for Humira to decline since its 2013 spin-off from Abbott (ABT).

But now that global Humira sales have finally peaked, investors are focused on both the pace of Humira's decline, as well as the pipeline of drugs AbbVie has to offset the growing hole in its business.

Replacing billions of Humira revenue is no small task. Two potential blockbusters make up the core of AbbVie's plans to diversify away from Humira, immunology drugs Skyrizi and Upadacitinib, or Upa.

Both drugs are successor medicines for Humira and were expected to launch in 2019. Those plans remain on track. While Upa is expected to be approved by the FDA in the third quarter, Skyrizi has already been approved by the U.S., Canada, and Japan, with Europe expected to approve soon.

The company expects to achieve $150 million in Skyrizi sales in 2019 (mostly second half of the year). A multi-year ramp is expected to eventually bring sales to $5 billion to $6 billion per year. Upa is also expected to deliver $5 billion to $6 billion in annual peak sales by 2025. For context, AbbVie's 2018 sales were $32.8 billion.

As Bloomberg notes, neither drug is the first of its kind. Instead, "AbbVie is betting that they’ll overcome that by being the best. It wants to reprise the success of third-to-market Humira, which ended up dwarfing the sales of speedier rivals."

However, there are no guarantees for any drug's ultimate long-term performance, regardless of how good its data might look. The marketplace for medicine is extremely competitive, drug pricing pressure is more severe today than it has been in years, and it's possible these new drugs cannibalize some of Humira's existing revenue base, accelerating its decline.

In fact, on the earnings call AbbVie's CEO said he expects that Humira will slow somewhat in the psoriasis category as Skyrizi starts to ramp in a very significant way.

While Skyrizi and Upa are the core of AbbVie's new pipeline, they can't on their own deliver strong growth until they can scale up to significant revenues. In the short term, AbbVie must rely on its portfolio of current drugs which includes a strong oncology (cancer) franchise consisting of Imbruvica and Venclexta.

Strong revenue growth reported by these two drugs, plus 7.1% Humira sales growth in the U.S. (which accounts for just over 72% of all Humira revenue and is technically protected from biosimilar competition through 2022), helped drive solid first-quarter earnings results.

In fact, AbbVie's revenues and adjusted EPS growth both beat expectations, and management raised its guidance for full-year EPS growth from 10% to 11% (high single-digits excluding buybacks). Basically, AbbVie's first-quarter results show that management's growth plans appear to remain on track for now.

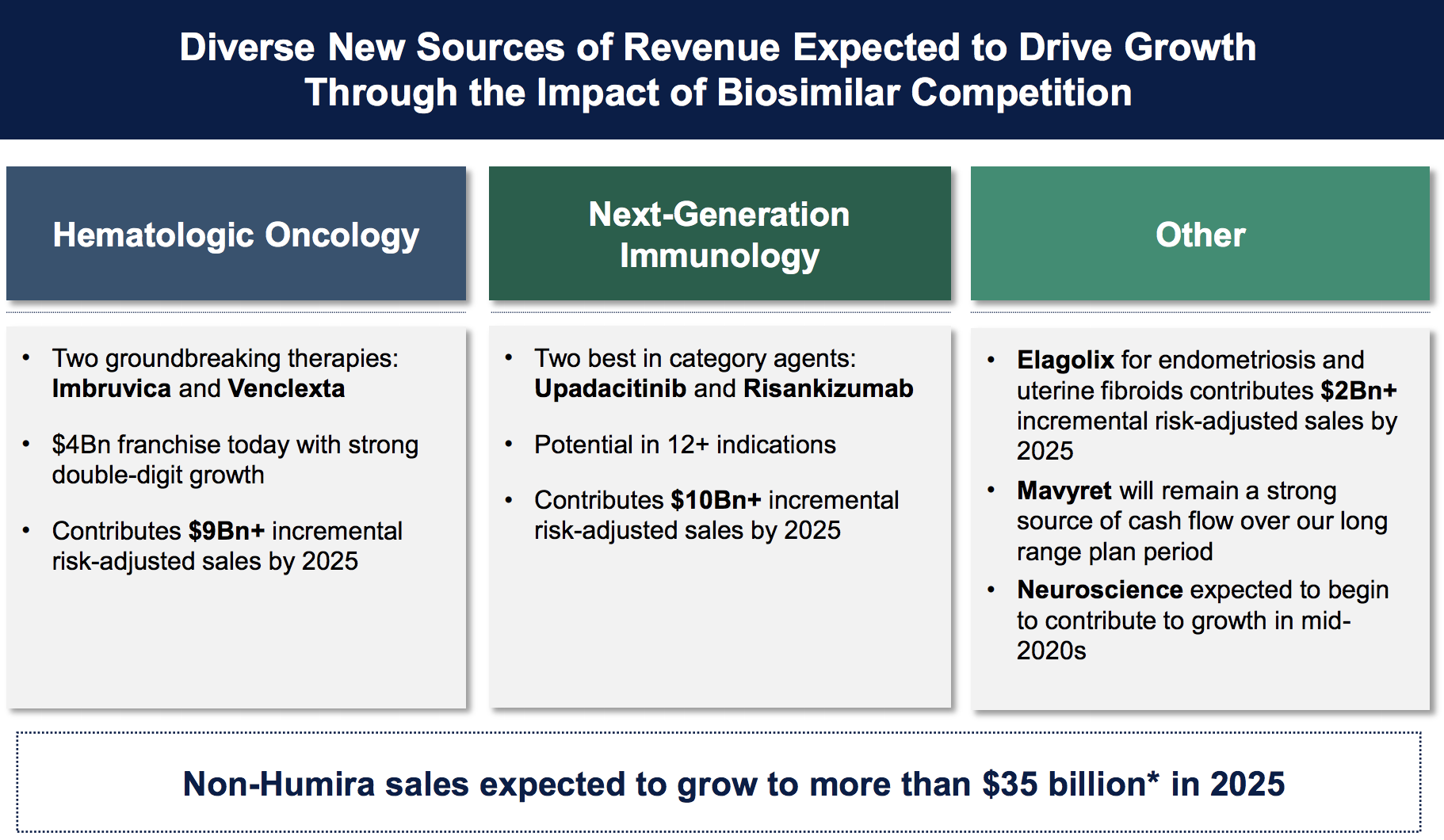

Looking further out and adjusting for the risk of drug trial failures, AbbVie expects that by 2025 non-Humira sales will amount to $35 billion. Management believes Humira will add another $12 billion to the firm's revenue in 2025, resulting in $47 billion in total projected sales and representing about 5% annual revenue growth going forward.

If everything goes according to plan, by 2025 the company expects to have reduced Humira sales concentration to about 25% of total revenue (compared to 95% in 2013).

Source: AbbVie Investor Presentation

In theory, AbbVie's plan sounds great – its drug portfolio becomes diversified, sales and earnings keep growing, and patent expirations for any single medicine become less of a concern. However, the only certainty investors have right now is that Humira's revenue is set to shrink meaningfully over the next five years.

Management actually has to deliver on AbbVie's drug pipeline to offset that growing hole. Unfortunately, there's no easy way for investors to gauge the likelihood of AbbVie hitting on all of its ambitious revenue targets. Only time will tell.

Plenty of investment funds have hired PhDs and med school grads over the years to try and help them pick the next big biotech winners. I've yet to hear or see any examples of sustained success in this area. It's a hard place to invest, which is why I like to instead pick diversified drugmakers who are not overly dependent on any single medicine and maintain strong balance sheets to get them through any tough years.

That's not to say AbbVie won't be successful. The market is just pricing in some skepticism in light of the firm's looming decline in Humira revenue, yet-to-be-delivered growth from its potential blockbusters, and the changing healthcare landscape, which could put additional pressure on Humira and the ultimate financial results of AbbVie's drug pipeline.

For example, what happens if the 2020 election does bring sweeping changes to healthcare, making it harder for branded drugs to fend off biosimilars even with patents, or perhaps capping prices on new medicines? However unlikely, changes like those would materially affect AbbVie's business.

As for AbbVie's dividend, once again nothing has really changed here until we know more in the coming years. Management has a policy of paying out about 50% of expected free cash flow for the next year, and the firm's current payout ratio is right at that target (48% in 2018).

This implies that AbbVie's dividend is likely to grow in line with free cash flow per share, which would grow at a mid-single-digit pace over the next few years if management's guidance proves true.

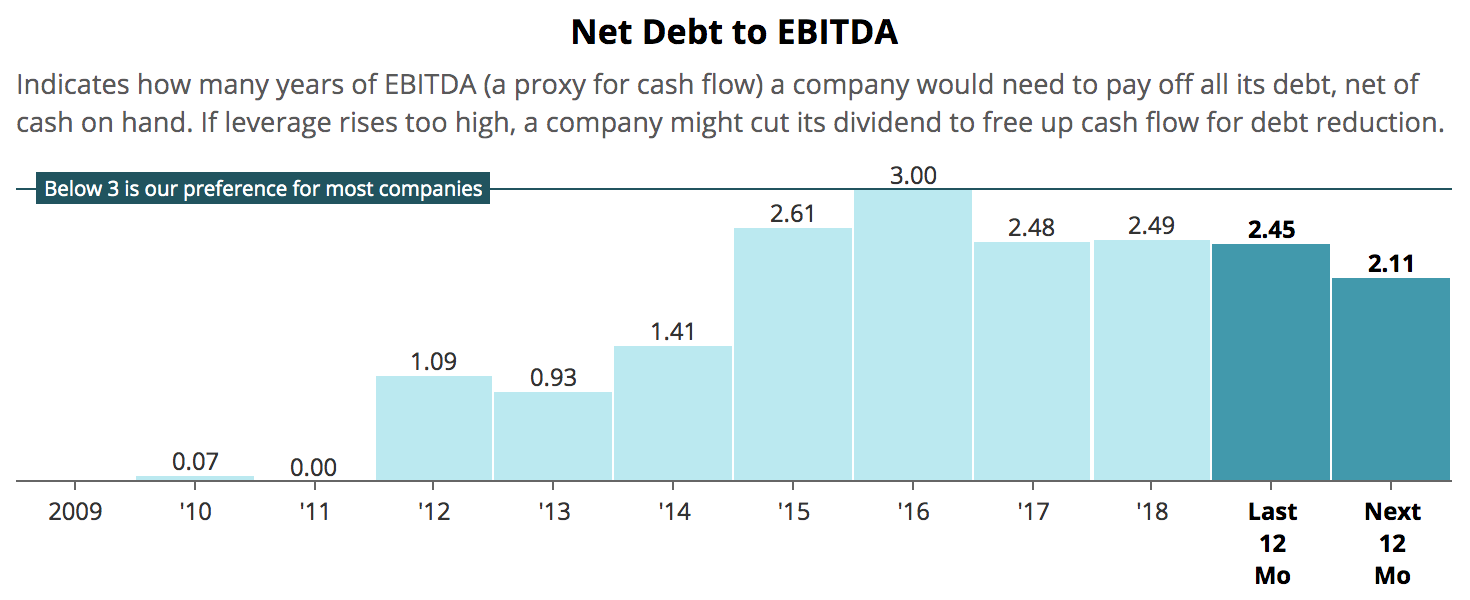

Meanwhile, AbbVie's debt levels look manageable and supportive of its dividend. The firm took on a lot of debt in 2015 and 2016 for two major acquisitions, one of which gave it cancer blockbuster Imbruvica, but has gradually reduced its leverage. As a result, AbbVie maintains an A- credit rating from Standard & Poor's.

Source: Simply Safe Dividends

Management says it doesn't have any near-term plans to acquire other companies since it is focused on bringing its own drug pipeline to the market, but AbbVie is open to making what it calls a "larger bolt-on" transaction valued as much as $30 billion if the right opportunity arose.

We would prefer for the company to maintain a strong balance sheet and stay entirely focused on its own pipeline for now, which seems to be the most likely case. However, if AbbVie jumped at a large deal, its dividend safety profile could be downgraded.

After all, while AbbVie has made some great acquisitions, the firm has also faced its fair share of failures. Most notably was its 2016 acquisition of Stemcentrx for $10 billion. That debt-funded deal increased the company's leverage to one of the highest levels in the industry. Worse, the cancer drug AbbVie bought, Rova-T, suffered major drug trial failures in early 2018 that resulted in its peak annual sales potential falling off a cliff.

As a result, EvaluatePharma cut its net present value of that drug (based on discounted future cash flows) by 98%, from $8.5 billion to less than $200 million, making Rova-T the biggest major drug failure of the past year. AbbVie admitted as much with a $4.6 billion write-down on the Stemcentrx acquisition in late 2018.

For now, AbbVie's short-term outlook appears to remain stable, including guidance calling for double-digit earnings and cash flow per share growth this year. The firm's longer-term outlook remains a bit fuzzier until AbbVie's pipeline delivers on management's expectations, Humira's fade proves manageable, and the healthcare landscape settles into a steadier state.

Concluding Thoughts In many ways, not much has changed with AbbVie's fundamentals over the last year. Management even expects low double-digit EPS growth this year. Instead, the market has become increasingly fearful over regulatory and political risks for the healthcare sector. AbbVie's Humira business, which still accounts for over 70% of the company's operating profits, has also officially begun to decline.

Investors will need to closely monitor the pace of Humira's erosion as competition ramps up in the coming years, as well as any developments with healthcare reform. Politicians on both sides of the aisle desire to make medicine more affordable, which could result in proposals that increase the amount of biosimilar competition Humira faces in the U.S. sooner than expected and reduce the long-term profitability of AbbVie's drug pipeline.

For now, it continues to feel too early to react to these risks until more information is known in the next couple of years. As we noted last year, the pharmaceutical industry is highly complex and prone to large amounts of headline risk. Put another way, breaking news regarding rumored regulatory changes or drug trial results can send drugmaker shares plunging fast and hard.

And thanks to the long and costly drug approval process, it's not always easy to know how quickly a pharmaceutical company's profits will grow in the future, or even if they'll grow at all. AbbVie's major dependence on Humira makes that statement even more true and reduces management's margin for error with bringing new medicines to the market.

Therefore, it's generally best for conservative income investors who are interested in this space to stick to the more diversified blue chips whose businesses are less likely to be disrupted if something goes wrong with any single drug.

Johnson & Johnson (JNJ), Merck (MRK), and Pfizer (PFE) are three examples of pharma companies who have strong balance sheets, balanced drug portfolios, and good potential to deliver safe and growing dividends for the foreseeable future. While they still face the same regulatory risks as AbbVie, they require less monitoring due to the diversified nature of their cash flow streams.

There's nothing necessarily wrong with investing in AbbVie, especially with its shares appearing beat up and its dividend remaining safe as long as management delivers on its long-term diversification plans.

However, investors must be comfortable with the firm's Humira concentration and prepared for heightened volatility as the market continues adjusting its long-term growth expectations for Humira and AbbVie's blossoming drug pipeline. As always, make sure to maintain a well-diversified portfolio and size your positions appropriately to manage risk.