UnitedHealth's Sell-Off Highlights Fears About Healthcare Reform

On April 16, United Healthcare (UNH) reported earnings that spooked some investors as its share priced plunged as much as 7% at one point. That decline added to several months of weakness that resulted in the company's stock price falling more than 20% from its all-time high.

Let's take a look at why the market is fearful of UnitedHealth and many other parts of the healthcare sector right now and review the company's long-term dividend safety and growth prospects.

Why the Market is Bearish on UnitedHealth

UnitedHealth's weakness doesn't appear to be based on its current fundamentals like revenue, earnings, or cash flow growth.

In fact, the company's first-quarter 2019 results delivered healthy revenue and earnings growth that also beat expectations:

Revenue grew 9.3%

Operating income increased 19%

Adjusted EPS rose 23%

2019 EPS growth guidance revised slightly higher to about 14%

UnitedHealth's stock was actually up in early trading but crashed during the company's conference call following CEO David Wichmann's comments regarding Medicare for All (single-payer healthcare):

"The wholesale disruption of American health care being discussed in some of these proposals would surely jeopardize the relationship people have with their doctors, destabilize the nation's health system, and limit the ability of clinicians to practice medicine at their best. And the inherent cost burden would surely have a severe impact on the economy and jobs, all without fundamentally increasing access to care."

Investors appear to have fixated on the "wholesale disruption" part of what appears to be a standard political statement criticizing single-payer healthcare, which has long been the worst-case scenario for the health insurance industry.

If the U.S. ever adopted some form of single-payer healthcare, then the private health insurance industry could effectively be wiped out in America, or at least limited to non-covered expenses such as premium services.

After Mr. Wichmann made his comments on the call, all health insurers' stock prices proceeded to decline sharply, as did many healthcare stocks such as pharmaceuticals.

Another potential risk that Wall Street is likely focused on is the proposed changes that the U.S. Department of Health and Human Services, or HHS, outlined in January 2019.

Specifically, the HHS proposed a new rule banning backdoor drug rebatesbetween drug companies and pharmacy benefit managers (PBMs), Part D plans, and Medicaid managed care organizations.

UnitedHealth's OptumRx is the third largest PBM in the country, and the HHS's consideration would effectively remove the safe harbor clauses that protect it from accepting discounted drug prices from the pharmaceutical industry.

The way the current system operates is that PBMs negotiate for better drug prices on behalf of insurance companies. In recent years these discounts have sometimes been as high as 51% of a drug's list price, in exchange for PBMs giving drug makers preferential treatment in their formulary. This helps drug giants gain market share and slows the rate of drug sales declines once patents expire and generic/biosimilar competition hits the market.

Some of those savings have been kept by both PBMs and insurance companies, creating heavy political criticism that the current rebate system creates an incentive for drug makers to inflate their list prices significantly. Out-of-pocket patient expenses (co-pays) are generally based on list prices.

According to the HHS, between 2011 and 2015 Medicare Part D reimbursement for branded drugs rose 77% while consumer out of pocket expenses increased byalmost 100%. In other words, the current rebate system is at least partially responsible for the fast rise in healthcare costs that the government and consumers have experienced for decades.

The HHS's proposal to eliminate these protections and force PBMs to use a flat rate fee system (which eliminates the incentive for high drug list prices) could potentially harm some insurers and PBMs. Wall Street appears to be concerned that UnitedHealth might be one of them, which is likely why the stock price has been so weak.

Political and regulatory risks are always something investors need to consider with any healthcare company. Let's review what these developments could mean for UnitedHealth's dividend safety and long-term outlook.

UnitedHealth's Dividend Safety Profile

The stock's sharp 10% decline after the CEO's comment regarding Medicare for All appears to be an overreaction. Mr. Wichmann doesn't appear to think that the risk of single-payer healthcare passing is very high, and his political comments are what one would expect to hear from any critic of Medicare for All.

Given that the government eventually covering all Americans under Medicare could negatively impact UnitedHealth's core business model, it's not surprising that he's against it and considers it a bad idea for the healthcare sector as a whole.

While single-payer healthcare is always a risk to consider, it's also been something that politicians have talked about for decades. Medicare for All appears to have little chance of becoming reality since it would likely require four things:

Democrats would need to regain control of all three branches of government

The Senate's Filibuster rule would need to be eliminated

The Senate would need to pass it with a majority vote (not guaranteed since this policy is highly controversial and Democratic senators from conservative states could vote against it)

The 5/4 conservative-leaning Supreme Court would have to uphold the law because it's likely to be challenged as unconstitutional

Basically, single-payer healthcare, while indeed threatening "wholesale disruption" to all healthcare company business models, is one of those low probability, worst-case scenarios that shouldn't necessarily keep someone from owning a quality company they otherwise like.

The market is constantly weighing the probabilities of good and bad long-term outcomes for every business, baking all of those considerations into the current valuation.

Any company's path can unexpectedly deviate from the base case that's priced in by the market, which is why it's important for investors to diversify their portfolios across numerous sectors and businesses.

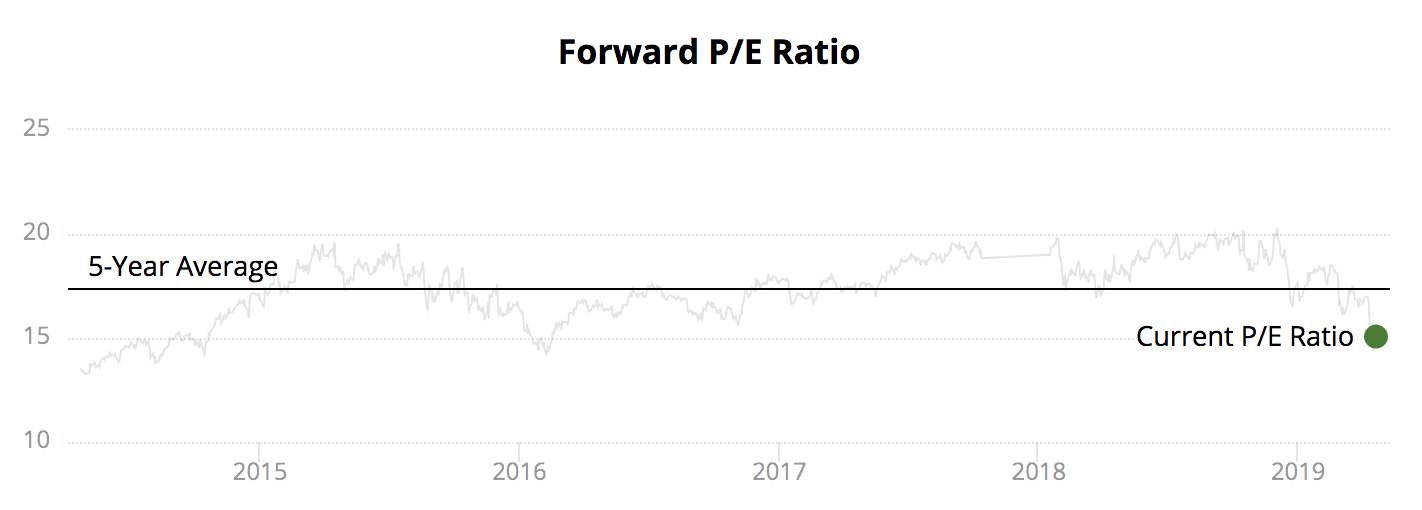

Throughout most of 2018 UnitedHealth's stock traded at a forward P/E ratio near 20, well above its long-term average, as investors rewarded the stock with a premium multiple for its impressive growth profile.

Sentiment quickly reversed this year as investors became anxious over the healthcare regulatory environment, causing UnitedHealth's forward P/E ratio to fall to about 15 (a discount to the broader market).

Source: Simply Safe Dividends

Of course, the market can be prone to overreactions. For example, biotech stocks lost around 50% between late 2015 and early 2016 following Hilary Clinton's promise to reduce drug prices if she was elected, according to The Wall Street Journal. However, those stocks ultimately bounced back.

For now, despite the market's swing, it feels too soon to worry about single-payer healthcare becoming a reality and damaging UnitedHealth's long-term outlook. Rightly or wrongly, investors have just nudged up the low probability of such an event occurring.

What about the risks of the HHS's proposed PBM rebate changes? While the chances of that occurring are higher (though still not certain to actually become law), UnitedHealth does not appear to be in much danger. That's because, as Jason Prince, the CEO of UnitedHealth's OptumRx PBM, told analysts at the last conference call:

"Overall, rebates only exist on 7% of prescriptions. 90% of what we manage is generic with no rebates, 10% is brand, and subset to that is rebatable drug. When you look at in the Medicare market today none of that value we’ve managed from a discount rebate is held by us, it's 100% is passed on to our clients. And fully disclosed with CMS the 100% is passed on the Medicaid market, within our total client base. 98% of our discounts are passed on to our clients...the plan for rebates does not impact our bottom-line or our economics."

Essentially, UnitedHealth has planned for the eventual end of rebates for many years now, and was proactively offering rebates to customers at the point of sale. Today just 2% of UnitedHealth's PBM drug rebates are boosting its bottom line, an insignificant amount.

Simply put, management appears to be running the business conservatively and doing a nice job trying to stay ahead of changes in healthcare.

Regardless, investors considering the stock should understand that headline risks will probably remain high as the 2020 election season heats up. This might cause UnitedHealth's stock to remain weak or potentially even fall lower.

However, as the largest and most vertically integrated health insurer in the country, UnitedHealth is arguably the best-positioned company in its industry to adapt to almost any challenge regulators put in front of it.

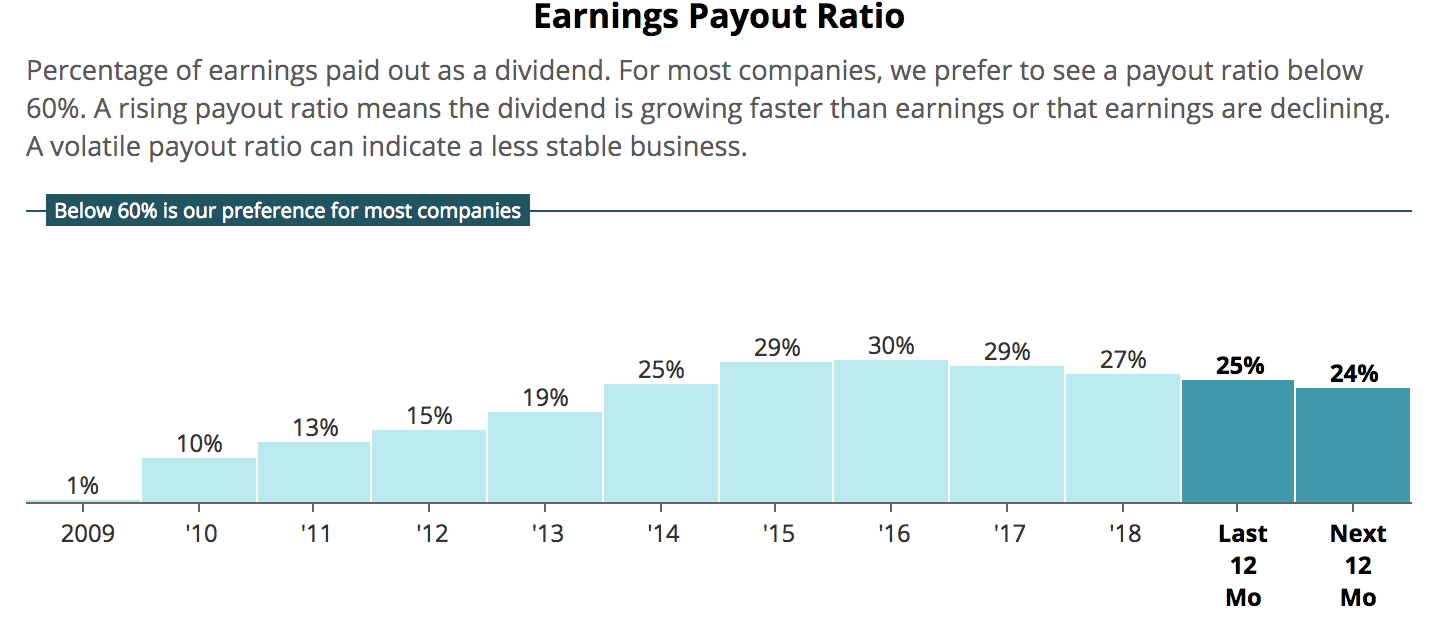

The insurer's financial profile remains excellent as well, resulting in a very safe dividend profile based on the information we know today. Despite raising its dividend by over 20% annually in recent years, UnitedHealth's payout ratio remains below 30%. That level provides a comfortable margin of safety in the event of an unfavorable development with its PBM business or insurance operations.

Source: Simply Safe Dividends

With a recession-resistant business model and cash flow coming from not only insuring about 75 million people (and providing healthcare to 93 million via OptumHealth) but also being one of the largest ambulatory care and data analytics providers, UnitedHealth's dividend looks safe and able to continue growing at double-digit rates for at least the next few years.

Management's guidance calls for 14% EPS growth in 2019, and analysts expect a similar pace of growth will continue over the next five years, according to data from FactSet. UnitedHealth has raised its dividend every year since it began paying one in 2010 and will likely hike its payout once more with its next announcement.

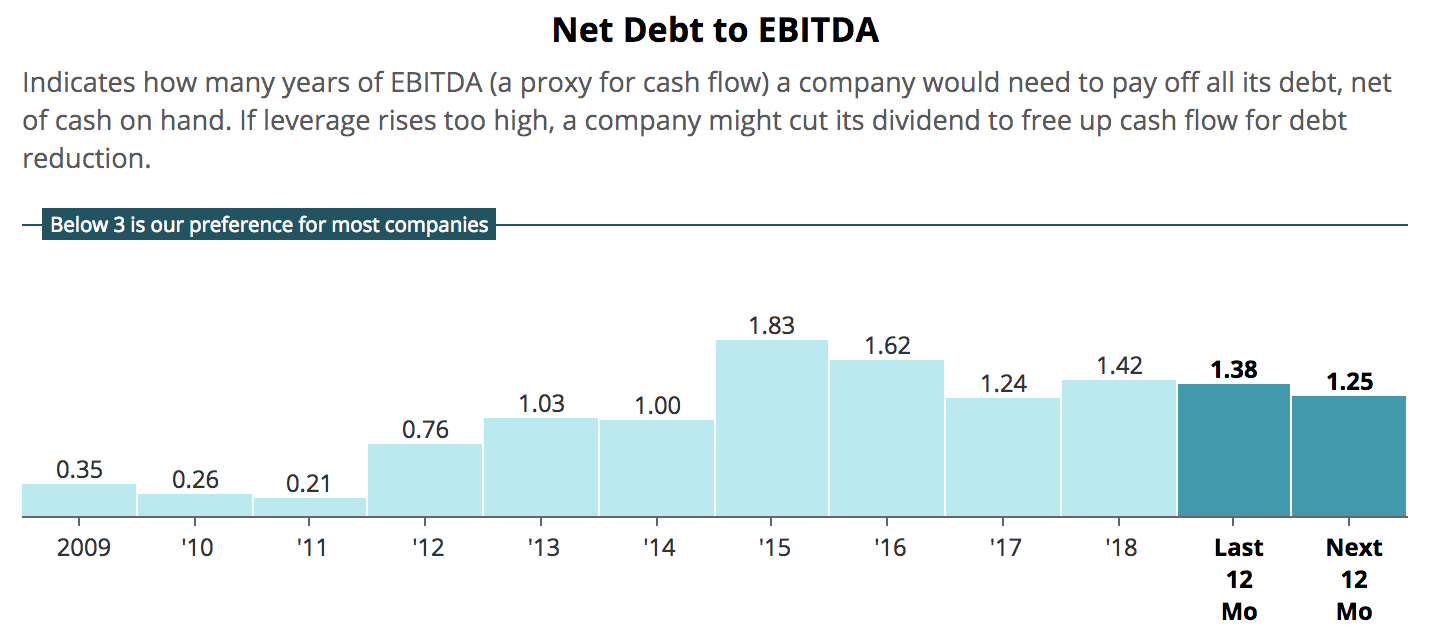

The insurer's healthy dividend profile is supported by the firm's balance sheet, too. As you can see, UnitedHealth manages its business with low leverage, and its debt has even declined over time following some major acquisitions it made in the PBM space in 2015. Standard & Poor's also gives the firm a strong A+ credit rating.

Source: Simply Safe Dividends

Overall, UnitedHealth's strong balance sheet, low payout ratio, and recession-resistant cash flow support the company's dividend profile and provide management with good financial flexibility to adapt the business as the healthcare sector continues evolving.

A worst-case, single-payer healthcare scenario would still change the game for UnitedHealth and virtually all other businesses in the sector. However, the risk of large-scale government intervention, which is at least several years away, still seems unlikely to materialize.

Concluding Thoughts

UnitedHealth's recent drop appears not to be a function of anything wrong with the company's short-term fundamentals, but rather due to the market's overall bearish sentiment on all things healthcare.

UnitedHealth CEO David Wichmann's political statement denouncing Medicare for All as a bad plan for America and for healthcare stoked fears about the sector's future as the regulatory climate evolves. But for now, the likelihood of single-payer healthcare actually passing and disrupting UnitedHealth's business model appears low (due to partisan gridlock).

However, the risk of rebate changes at the federal level is higher. Fortunately, UnitedHealth appears to have insulated itself here as well, with 98% of all rebates already being passed onto customers.

The stock may continue to experience sharp volatility for the next year or two, due to the 2020 election season creating a lot of political headline risk. But overall, based on what we know today, UnitedHealth's fundamentals and solid dividend profile appear to remain intact.

Investors just need to remain mindful of the healthcare sector's complexities and practice good risk management, which means owning a well-diversified portfolio in case the worst-case scenario does happen to play out.