Dividend investors exploring how to invest in REITs may wonder how higher interest rates can impact this sector, and for good reason.

Over the past decade, interest rates fell to historically low levels. This has created a challenging environment for income investors who previously enjoyed healthy, low-risk returns from money market funds, CDs, and Treasury bonds.

In fact, since the darkest days of the financial crisis, many yield-starved investors have been forced to search elsewhere for their income needs, driving up demand for bond alternatives such as REITs.

However, with interest rates now on the rise, many dividend investors are concerned about whether or not REITs are still a good sector to own.

Let’s take a look at the long-term history of how REITs respond to varying interest rate environments to see which ones, if any, are most likely to continue doing well in the coming years.

More importantly, find out what REIT investors need to know to better manage the risk in their portfolios as interest rates potentially rise.

Are Higher Interest Rates Bad for REITs?

The chart below plots the 10-year Treasury yield going back to 1962. As you can see, interest rates have never been this low for this long, making many of the academic studies about rising rates potentially less relevant.

Source: Federal Reserve Bank of St. Louis

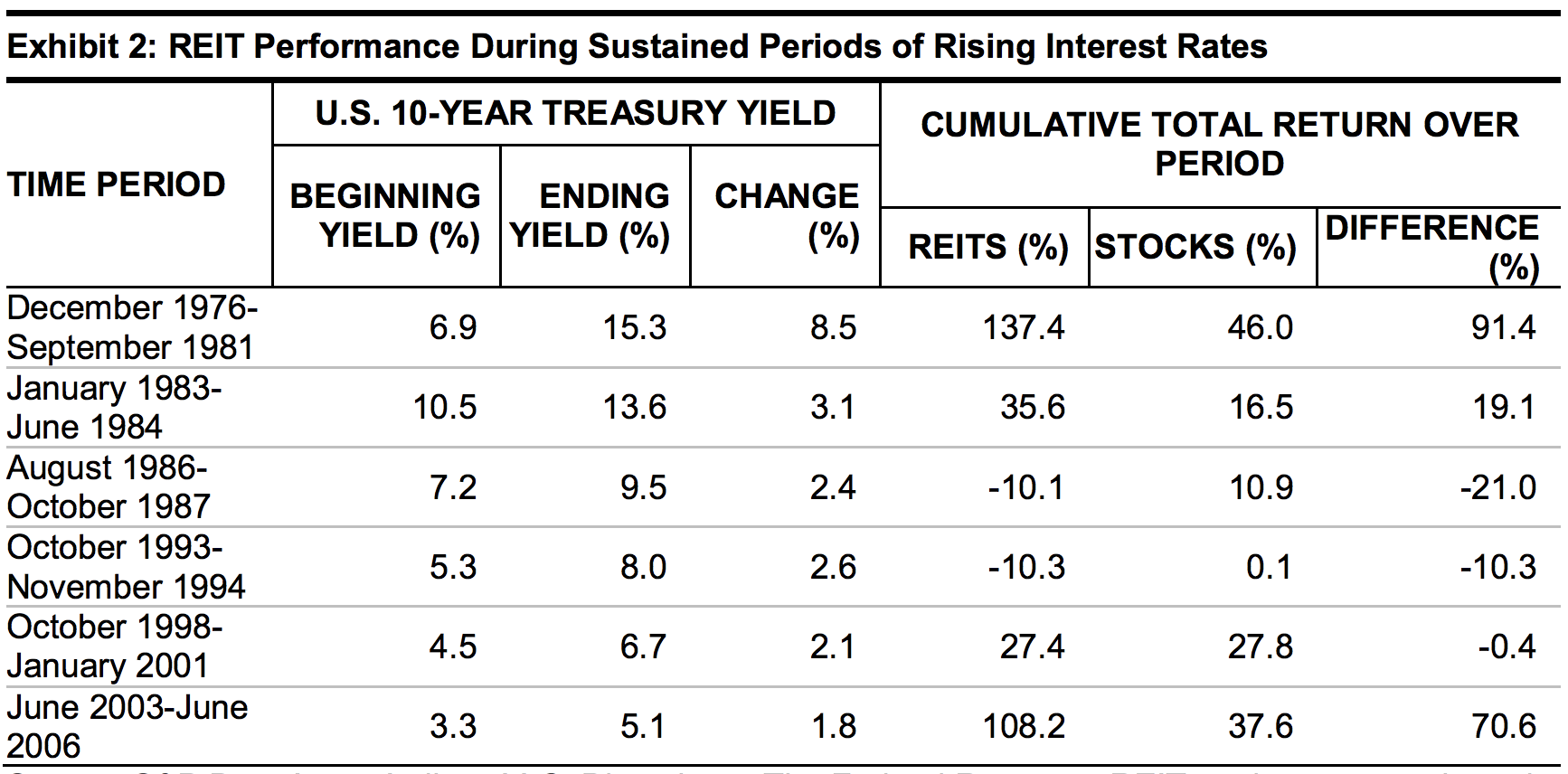

With that said, Standard & Poor's reviewed six periods since the early 1970s during which the 10-year Treasury yield increased substantially. REITs recorded a positive total return in four of those periods and actually beat the market during half of them.

So from a historical perspective, it is clear that generalizations made about interest rates and REIT performance might be unfair. Rates matter, but predicting the direction of yields and REIT performance is anyone's guess.

Source: S&P Dow Jones Indices LLC, Bloomberg, The Federal Reserve

There are two reasons why interest rates matter to REITs, and both have to do with the underlying business model of this high-yield industry.

REITs exist so that the companies that own the properties can avoid paying corporate taxes as long as they distribute 90% of taxable income as unqualified dividends.

This means that REITs aren’t able to retain much of their earnings or adjusted funds from operations (AFFO – similar to free cash flow for a REIT).

Thus, in order to grow, REITs need to raise external debt and equity capital from investors. As a result, higher interest rates increase a REIT’s cost of debt and make it incrementally harder to achieve profitable growth.

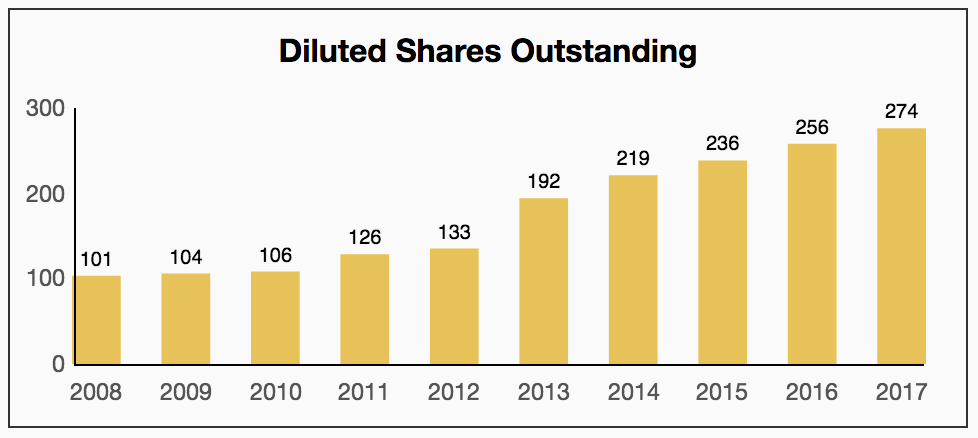

That’s especially true because REITs frequently use secondary offerings (i.e. they sell new shares) to raise growth capital.

Realty Income (O) has nearly tripled its share count since 2008, for example:

Source: Simply Safe Dividends

Management has to make sure that any new properties it buys are still accretive to investors, meaning that the additional AFFO growth is enough to offset the dilution it took by issuing new shares to fund the property acquisitions.

In other words, AFFO per share needs to continue growing in order for the dividends to grow in a sustainable and secure manner.

However, when interest rates rise, bonds, including risk-free Treasury bonds, decline in value, causing their yield to rise.

REITs compete for new capital with bonds, as well as savings accounts, money market funds, and CDs.

Some investors who own REITs today might be inclined to sell their shares if rates rise because they can now achieve similar but less risky yields elsewhere.

To put it another way, because REITs are often seen as bond alternatives, higher interest rates could mean decreased demand for REIT shares, causing a REIT’s yield to rise.

While that’s great for dividend investors looking for new places to put money to work, it can also be a problem for the REIT’s long-term growth prospects.

That’s because the higher a REIT’s valuation (i.e. share price), the less new shares it takes to raise growth capital.

In other words, the less dilution to existing investors is needed in order to continue growing a REIT’s AFFO, and thus its dividend.

Think of it this way. Suppose a REIT currently yields 5%, and management is able to buy new properties at a capitalization rate (annual net income / purchase price) of 7%.

Even if the REIT has to raise 100% of the capital to buy a property by selling new shares, then AFFO per share will still increase, and so will the dividend.

And if the REIT buys the property with a 50/50 mix of equity and debt (with an interest rate of 4%), then the amount that AFFO per share increases is even more due to less dilution and an even lower weighted average cost of capital, or WACC.

However, if interest rates increased to 6% and a REIT’s shares fell enough to raise its dividend yield to 8%, then suddenly the ability to buy that property with 100% equity capital disappears.

The 8% yield a REIT would have to pay on its newly issued shares is more than the 7% capitalization rate it earns on its property, destroying shareholder value.

In other words, the REIT’s cost of capital has risen high enough to not make the deal accretive.

REITs essentially have an optimal growth sweet spot, in terms of their yield. If shares are too expensive, then the yield is too low for investors to earn the income they need.

But if shares are too cheap for too long (due to higher interest rates, for example), then the REIT gets cut off from growth capital and can’t expand its property portfolio and dividend.

So with the Federal Reserve predicting that interest rates will rise by a meaningful amount over the next few years, are REITs a bad investment idea?

Not necessarily. What it does mean, however, is that you need to stay diversified and be highly selective with which REITs you add to your portfolio.

The Best REITs Can Still Grow Despite Higher Interest Rates

It’s important to note that REIT share prices aren’t just affected by interest rates but can and do trade on other factors, including a REIT’s fundamentals, long-term growth prospects, and dividend growth history.

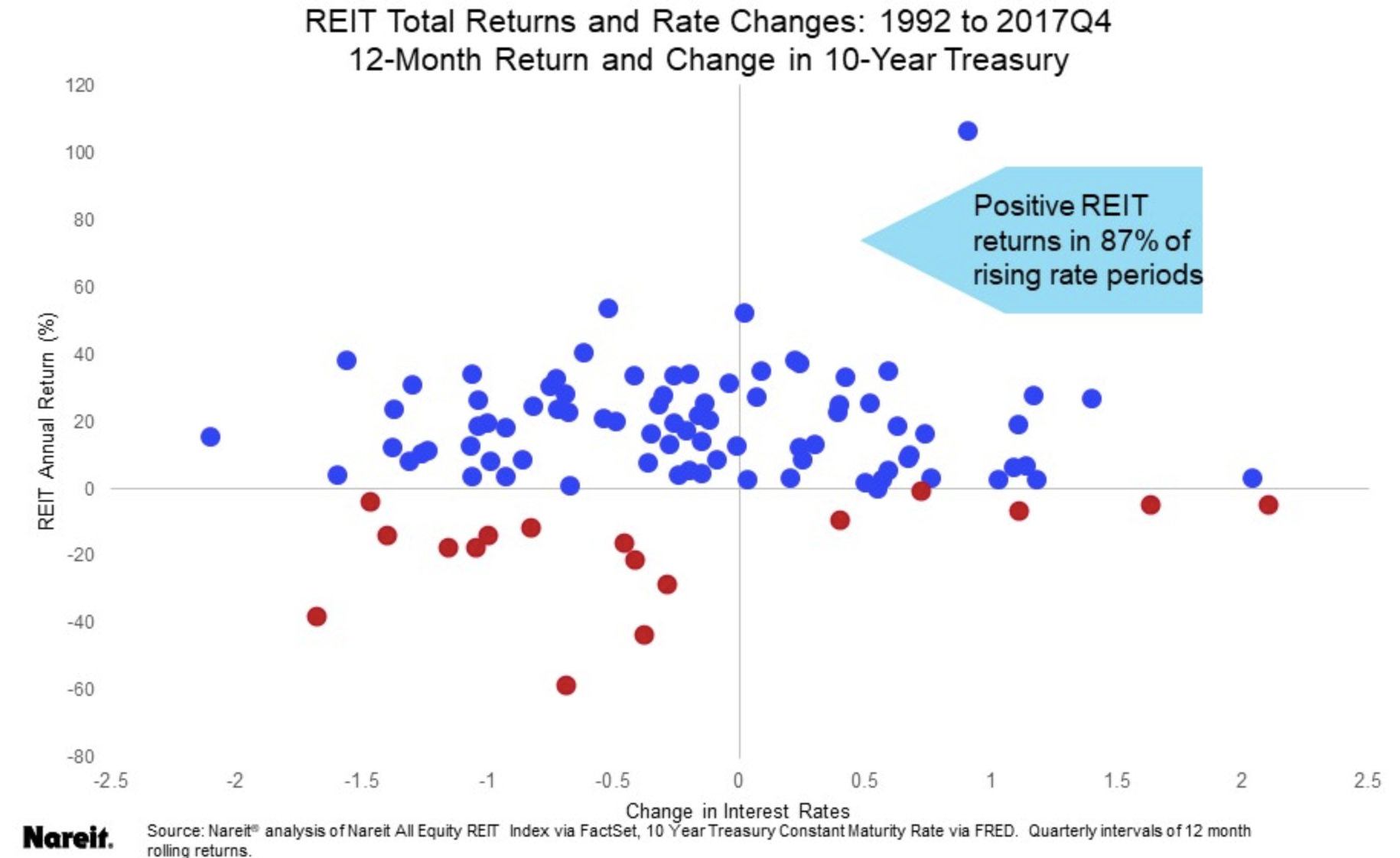

The chart below, courtesy of REIT.com, plots the 12-month return of REITson the y-axis, and the change in the 10-year Treasury yield on the x-axis from 1992 through 2017. The blue dots represent periods when REITs earned a positive total return during each of those periods. The red dots signal that REITs lost money.

While an investment in REITs made money in 87% of rising rate periods observed, it is clear that REITs have been positively and negatively correlated with interest rates during different periods of time, indicating that there are other factors influencing their returns. Like all other stocks, shares will periodically trade at large premiums and discounts to a REIT’s intrinsic or fair value.

A quality management team will take advantage of these periods of overvaluation to raise more equity capital when the cost of equity is low (high share price), and then raise cheap debt capital when shares are undervalued (low share price).

This kind of smart capital management is why blue-chip REITs, such as Realty Income, have a history of consistent growth throughout all kinds of interest rate and economic environments.

In fact, during the last period of rising interest rates, Realty Income was able to grow its cash flow per share between 4.9% and 9.4% each year.

Source: Realty Income Investor Presentation

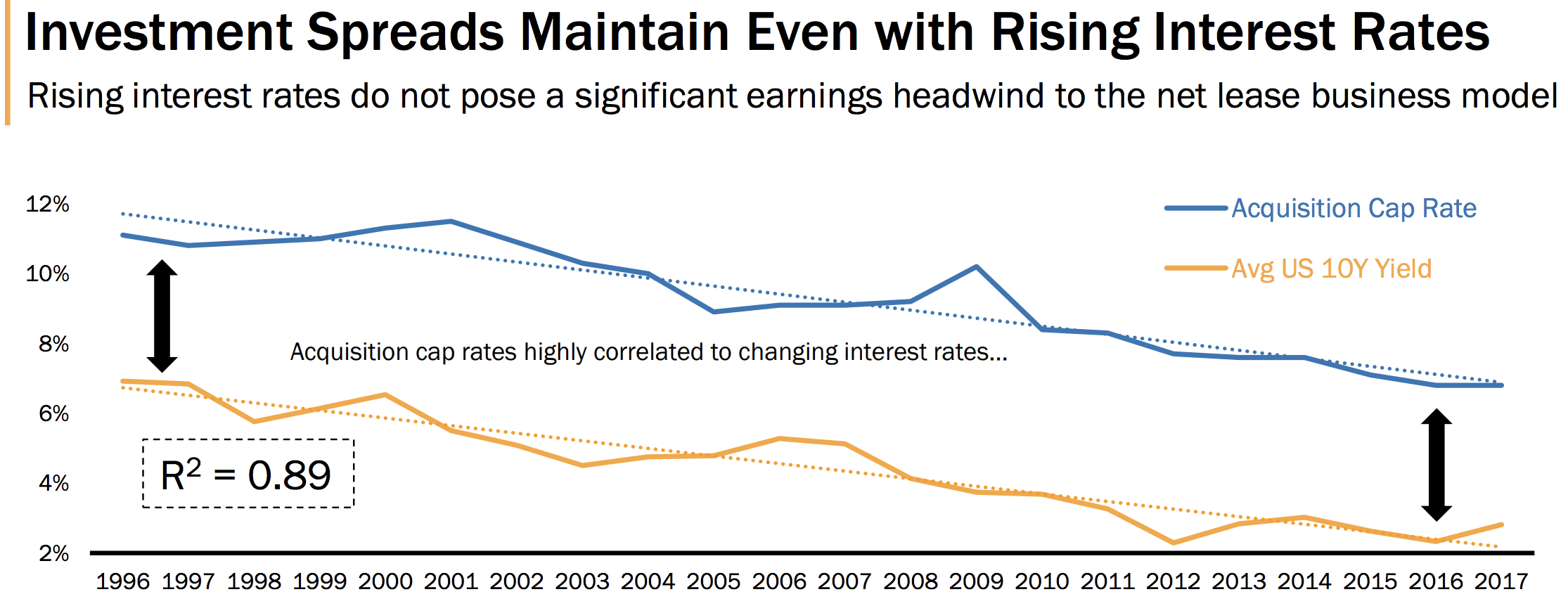

While higher interest rates make it harder to grow profitably (due to higher costs of capital), higher rates also tend to depress real estate prices. Therefore, a quality management team can acquire new properties for lower prices and thus higher cap rates.

Realty Income's historical results provide a nice example. The company's cap rates have had a strong correlation with interest rates, but the spread between the two has remained fairly constant, providing a steady level of profitability.

Source: Realty Income Investor Presentation

It's also worth mentioning that most management teams are not asleep at the wheel. They see all of the bearish headlines and forecasts surrounding higher interest rates, and they are doing the best they can to position their companies for success.

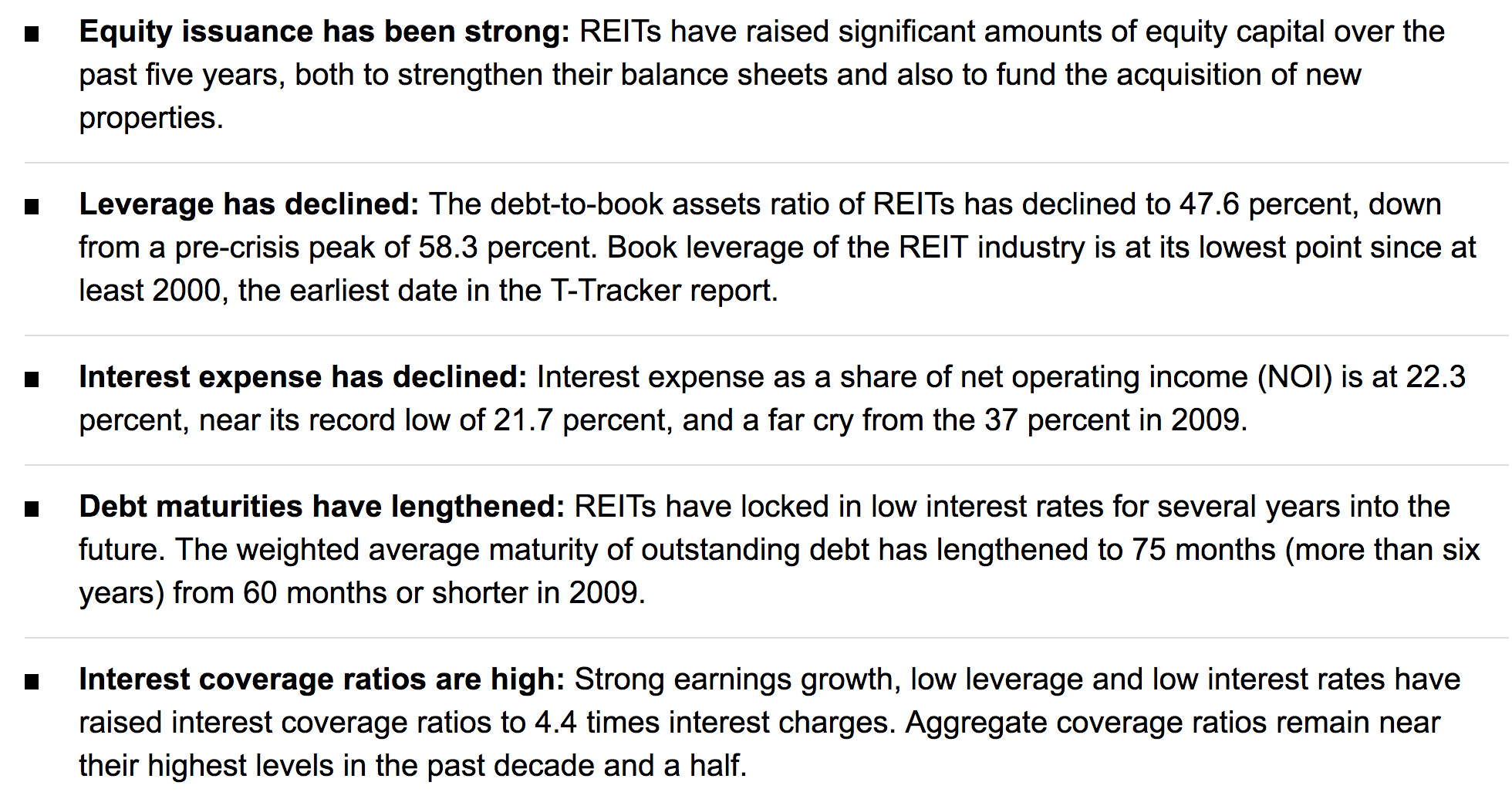

For example, at the end of 2017 REIT leverage and interest coverage metrics across the board are much stronger than they were since before the financial crisis.

Source: REIT.com

Not All REITs Are Equally Rate Sensitive

Of course, just because higher interest rates won’t stop the best REITs from delivering sustainable and consistent dividend growth doesn’t mean that all REITs are equally sensitive to interest rates.

The U.S. News & World Report cited Robert R. Johnson, a member at the Fed Policy Investment Research Group in Virginia, who made several observations about REITs. During rising interest rate environments from 1972 to 2013, Johnson found that equity REITs returned 9.8% annually, but mortgage REITs lose 4.1% per year.

Mortgage REITs, which invest in residential or commercial mortgage securities instead of physical, rent accruing properties, are extremely rate sensitive and thus far riskier than most equity REITs (those that own rental properties).

This is because the share price of mortgage REITs generally trades as a multiple of its net asset value (i.e. book value per share).

Since the value of a mortgage bond trades inversely to interest rates (higher rates cause mortgage bond values to decline), higher rates will mean that the NAV of a mortgage REIT will decline and often take the share price with it.

Of course, as with most things in finance, mortgage REIT investing isn’t as simple as saying, “Don’t own mortgage REITs if rates are rising.”

After all, mortgage REITs make their money by borrowing at short-term (i.e. low) rates and then investing in longer-term (i.e. higher-yielding) investments.

If short-term rates rise slowly over time but longer-term rates rise quicker (i.e. the yield curve steepens), then a mortgage REIT’s profitability will actually grow, cash flows will strengthen, and the dividend becomes more secure.

This will attract more investor capital, meaning a rising share price, which will further allow management to keep raising cheap enough equity capital to keep growing.

The best kinds of mortgage REITs to own in a rising rate environment are those that will actually benefit from rising rates.

Mortgage REITs that borrow at fixed rates but lend at mostly floating interest rates include commercial mortgage REITs such as Starwood Property Trust (STWD), Ladder Capital (LADR), Jernigan Capital (JCAP), and Ares Commercial Real Estate Corporation (ACRE).

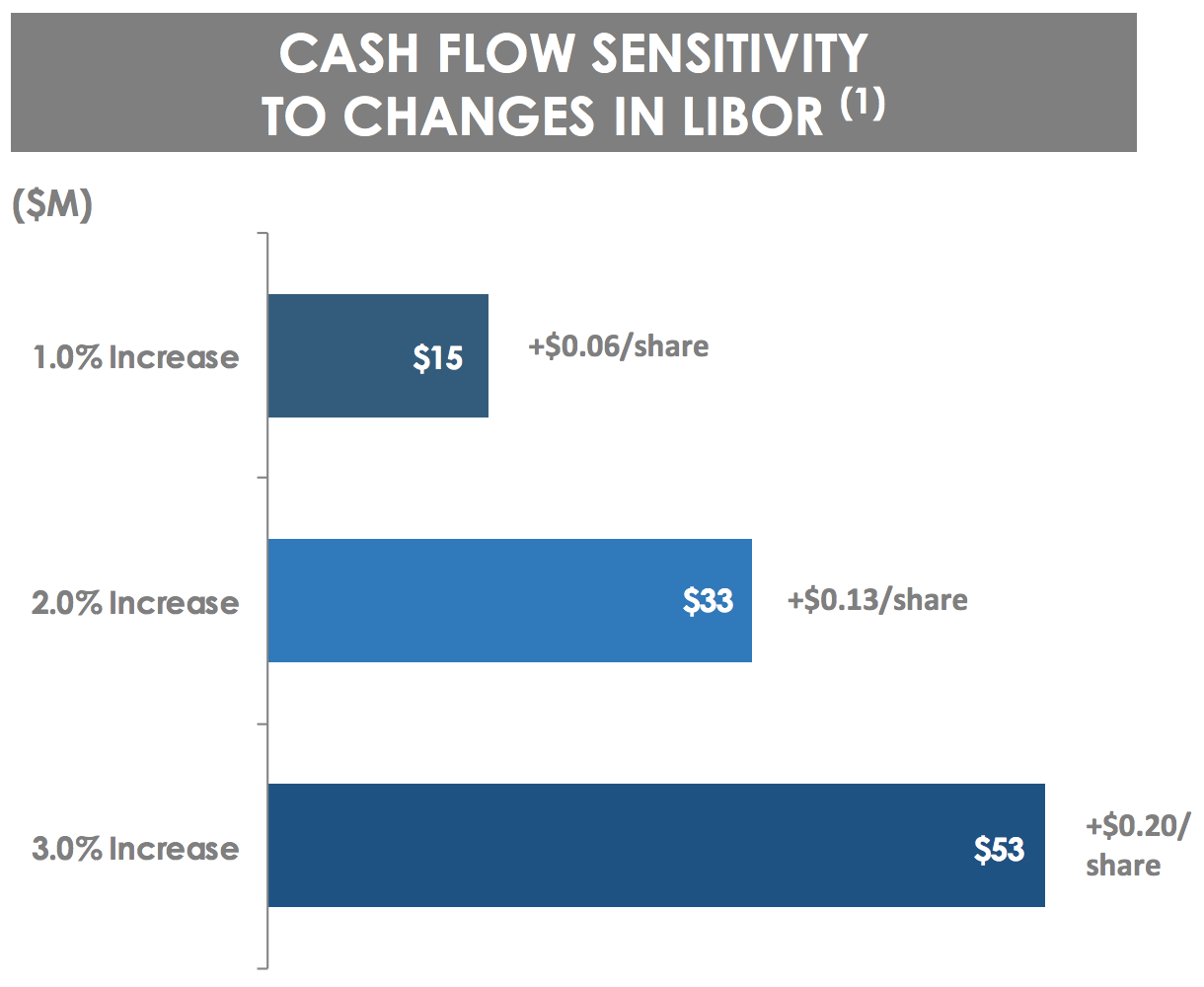

These are all commercial mortgage REITs that could continue growing well in a rising interest rate environment. For example, you can see Starwood Property Trust’s favorable cash flow sensitivity to changes in rates below.

Source: Starwood Property Trust Investor Presentation

Commercial mortgage REITs also use less leverage, meaning that their NAVs will decline less due to the decrease in their loan values compared to higher leveraged residential mortgage REITs, such as Annaly Capital Management (NLY).

Source: Annaly Capital Management Earnings Presentation

Since residential mortgage REITs (which invest mostly in fixed-rate residential mortgages) don’t see their cash flow grow when rates rise, especially when short-term rates rise faster than long-term ones (net interest margin compression), a rising interest rate environment can create long periods of decreasing cash flow, dividends, and share prices (which makes profitable growth very difficult).

As a result, residential mortgage REITs are arguably the riskiest kind of REIT to own when rates are rising.

However, just because commercial mortgage REITs are less risky than residential mortgage REITs doesn’t mean they aren’t also higher risk than their equity REIT cousins.

After all, their cash flows are highly tied to the health of the overall economy and their customers being able to continue making their mortgage payments.

During recessions, commercial mortgage REITs can face higher default rates and thus also be forced to cut their dividends.

That’s why most conservative dividend investors are generally better off avoiding mortgage REITs and sticking with high-quality equity REITs such as Realty Income, W.P. Carey (WPC), and Public Storage (PSA).

Interest Rate Sensitivity of Equity REITs

Equity REITs are interest rate sensitive, but you need to keep in mind that not all REITs are created equal.

The REIT industry is incredibly diverse with many different kinds of business models.

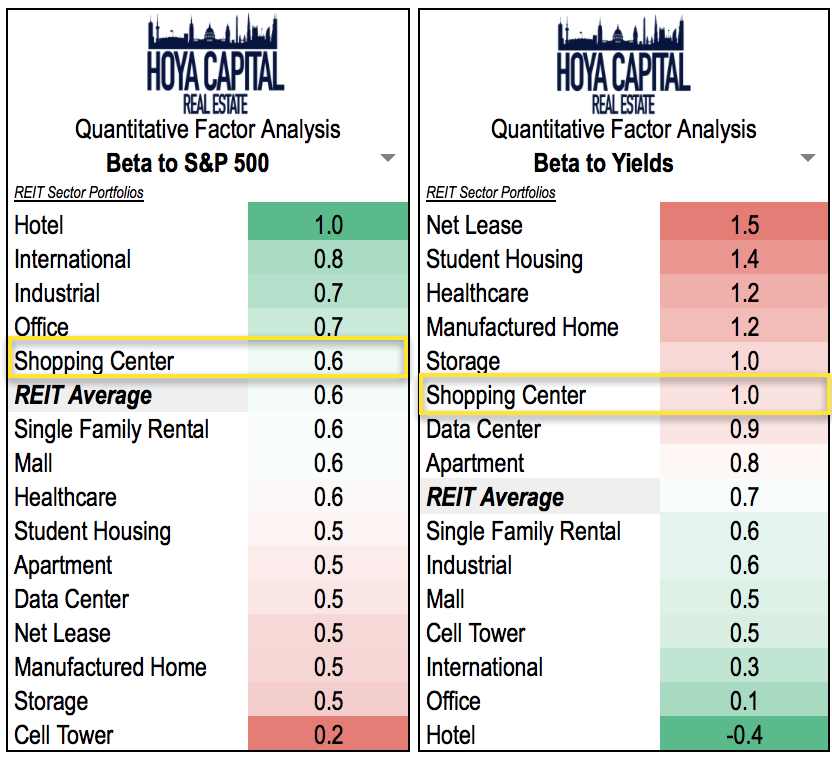

The table below shows two important factors to consider. First, certain sectors such as triple net lease REITs (e.g. Realty Income) have very high interest rate sensitivity.

Triple net lease REITs have a high 1.5 interest rate beta. That means that for every 1% increase in interest rates (10-year Treasury yield), the yield on triple net yield REITs increases by 1.5%.

On the other hand, hotel REITs such as Pebblebrook Hotel Trust (PEB) have negative interest rate betas, meaning that they have historically gone up when rates fall.

Source: Hoya Capital

What explains this seemingly strange occurrence? The answer is the business model, or more specifically the underlying length of the contracts underpinning the cash flow and the current bond alternative nature of the REIT industry.

Now that REITs are their own official stock sector, the majority of REIT share prices is determined by institutional capital, mostly mutual funds.

Some of this institutional capital is treating REITs as a kind of bond alternative, and like with bonds, the interest rate sensitivity of the asset is based on its duration.

For example, a two-year Treasury will generally decline by about 2% for every 1% increase in interest rates, while a 30-year Treasury would decline by about 30%.

For REITs, the duration that institutional managers are looking at is the length of the contracts that underpin how often the REIT can raise rent prices.

For example, hotel REITs generally own their properties and obtain cash flow from customers’ nightly stays.

Since hotel room prices change on a daily basis, there is very little inflation risk because room rates can be increased each day.

As a result, the hotel REIT interest rate sensitivity we saw above is signaling that this kind of REIT has low interest rate sensitivity because the duration is essentially 1 day.

On the other hand, triple net lease REITs generally sign very long-term rental contracts with tenants, typically between 10 and 20 years.

While these agreements include annual rental escalators to account for inflation, those are generally based on recent inflation rates. In other words, most triple net lease escalators are very low right now, about 1% to 2% a year.

Should inflation be higher than expected, say 3% to 4% over the length of the contract, then the inflation-adjusted value of the REITs cash flow could actually decrease over time.

Essentially, you can think of the weighted average duration of a REIT’s rental contracts as the duration of this bond alternative. REITs with longer durations and less flexibility to adjust the cash flow rates they receive from tenants are more sensitive to interest rates.

However, it’s also important to note that, as previously explained, REIT share prices aren’t entirely based on interest rates.

After all, while the last decade has seen many investors treat REITs as bond alternatives, there is still a big difference between risk-free assets (e.g. Treasury bonds) and equity REITs.

All equities are risky in the sense that the dividends aren’t guaranteed.

If a REIT runs into trouble, say through taking on too much debt right before a recession hits, then it can be forced to cut its dividend during an economic downturn, which happened with many REITs during the 2008-2009 financial crisis.

That explains why the beta of different REIT sectors to the S&P 500 is often the inverse of its interest rate beta.

In other words, while triple net lease REITs are the most interest rate sensitive (in terms of share price and dividend yield), they are also the least volatile REITs you can own.

In fact, triple net lease REITs are generally less volatile than the S&P 500 and lREITs in general (which, as an industry, are less volatile than the market at large).

Why is this? Because the very duration of contracted cash flow that affects the REIT’s “duration” also affects its cash flow, and thus dividend security.

For example, a hotel REIT may have very little interest rate sensitivity because it has a duration of just 1 day.

But that also means that hotel REITs have very little cash flow predictability because their AFFO is at the mercy of daily hotel customers.

As a result, their AFFO is the most volatile, and they must maintain lower AFFO payout ratios at the expense of long-term dividend growth.

If a hotel REIT were to grow its dividend too quickly, then the moment the next recession hits and hotel traffic falls, its payout will quickly become unsustainable and require a dividend cut.

This higher dividend risk (and slower dividend growth) explains why hotel REITs are the most cyclical and volatile sector of the industry.

On the other hand, triple net lease REITs, because their rental agreements can last for 20 years, have very steady and predictable cash flow that allows them to generate very consistent and safe dividend growth, often even during recessions (assuming their tenants can still make their payments).

This kind of REIT often attracts more conservative income investors who depend on dividends to fund their retirement.

These shareholders value the cash flow and dividend security above all else. As long as a REIT’s dividend remains safe, they are unlikely to sell even if interest rates increase.

After all, because a quality REIT will steadily raise its dividend over time, the yield on cost will also rise over time.

Shareholders who bought Realty Income shares back when it went public in 1994 are currently getting paid over 30% of their original investment each year, for example.

Even adjusting for inflation those shares are still paying over an 18% yield on cost.

Think of it like this. If you were an investor primarily focused on dividend safety and income to live off during retirement, would you sell a blue chip corporate bond that paid over 18% and was steadily raising its payout each year faster than inflation just because interest rates increased and the share price declined?

Of course not, because as long as the dividend is secure and growing you are unlikely to have a good reason to sell those shares.

How to Invest in REITs in a Rising Interest Rate Environment

While understanding how and why interest rates affect REIT share prices is helpful, at the end of the day REIT investors really want know how they should position their portfolios in the coming years. Should we make any important changes?

Fortunately, for investors with diversified portfolios (our preference is to invest no more than 25% of a portfolio's value in any sector), the answer is a very simple and adamant “no".

Market timing, or jumping in and out of stocks or sectors to try to take advantage of or avoid certain situations, is one of the worst things long-term investors can do.

Instead, the keys to successful long-term REIT investing are to:

1) Know yourself, your personality, time horizon, goals, and risk tolerance.

2) Make a well-thought-out personalized investing plan that meets your needs.

3) Stick to this plan, never investing based on emotions. Failing to plan your investments is the same as planning to fail at investing.

4) Do your research. Never buy a REIT until you’ve checked its long-term dividend track record, including its AFFO payout ratio history. You want to make sure that it’s stable over time and 85% or less (depending on the industry). Also check the balance sheet to make sure that a REIT’s debt levels are safe and that management isn’t likely to be forced to cut the payout during a recession (things like the leverage ratio, interest coverage ratio, current ratio, and credit rating).

5) Stick to your plan. Buy and hold as long as the investment thesis holds (i.e. the dividend is secure and the business is growing).

6) Add on dips (assuming you have new money coming in).

7) Reinvest the dividends if you can.

Follow this simple plan and you will be well on your way to reaching your financial goals, whatever kind of dividend growth stocks you invest in.

Higher Interest Rates Present Challenges and Opportunities for REIT Investing

While rising interest rates can certainly pose a challenge to some REITs, long-term investors with properly diversified dividend portfolios need not fear.

After all, the best quality REITs are led by experienced management teams with plenty of experience growing shareholder value in any kind of interest rate and economic environment.

The key to successful REIT investing is the same as with all dividend growth stocks. Do your research, buy high-quality names at reasonable prices, plan on holding them for the long term, add on dips, and reinvest the dividends.

In the meantime, take advantage of the market’s short to medium-term panics over rising rates to accumulate reasonably priced shares of the best REITs, locking in higher, steadily-growing yields.

While rising interest rates have caused REIT stocks to meaningfully underperform during certain periods of time, it’s also important to remember that higher rates are often a signal of investors’ expectations for stronger economic growth in the future.

Increased corporate spending, a tightening labor market, and greater economic activity translate into stronger occupancy rates, healthy rent growth, and overall stronger fundamentals for most REITs.

At the end of the day, executing a simple investment process, remaining diversified, and staying the course are the best things a REIT investor can do whether interest rates rise or fall from here.