Magellan Midstream Partners: An Impressive MLP for Income

Magellan Midstream Partners (MMP) is one of America’s largest master limited partnerships. The firm's pipeline systems primarily transport refined petroleum products such as gasoline and diesel fuel from refineries, helping them eventually reach gas stations, truck stops, airports, and other end users.

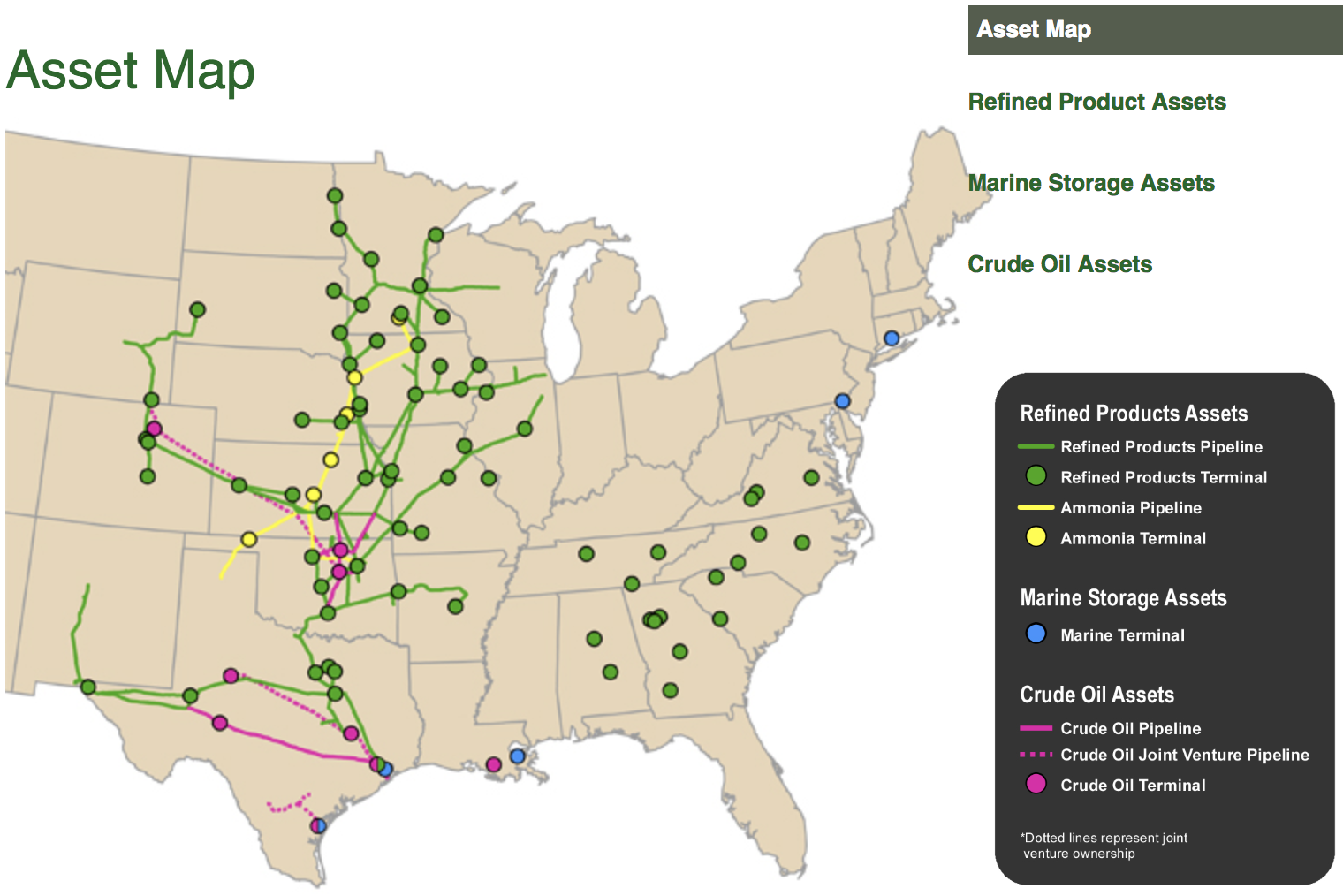

Magellan owns the longest refined products pipeline system in the country, extending over 9,700 miles from the Gulf Coast. The MLP also owns storage facilities, terminals, and several thousand miles of ammonia and oil pipelines.

Refined products generated 59% of Magellan's 2018 operating margin, followed by crude oil (34%) and marine storage (7%).

Source: Magellan Midstream

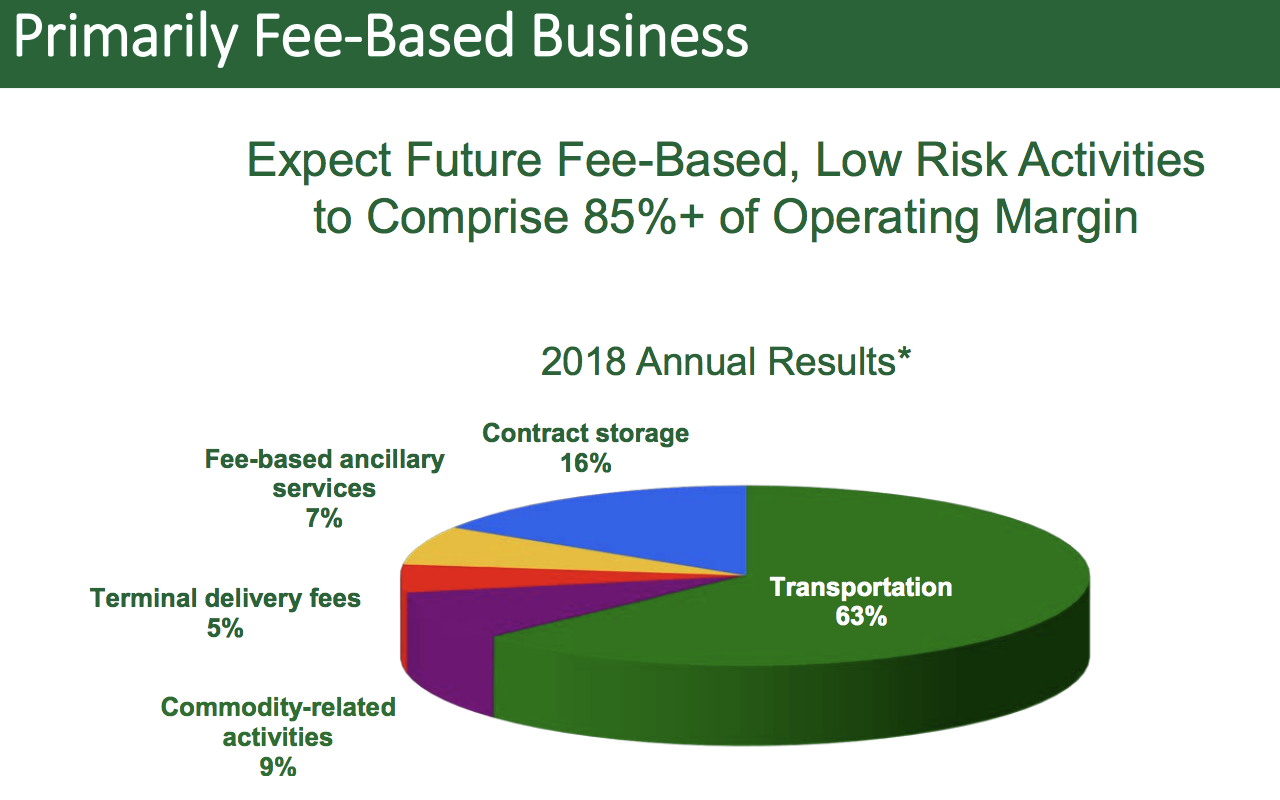

Magellan generates most of its cash flow from fixed-rate transportation and storage contracts that are generally insensitive to commodity prices. In fact, less than 10% of Magellan’s operating margin has any direct commodity exposure.

Source: Magellan Investor Presentation

Magellan's cash flow stability and conservative management team have allowed the firm to deliver high distribution growth each year since 2001.

Business Analysis

Operating pipelines is an attractive business for several reasons. First, few companies have the financial capital and industry relationships to compete.

Building a new pipeline can cost billions of dollars while taking years to complete (and legal challenges mean sometimes they don't get completed at all). Without connections to oil & gas producers, refineries, and regulators, it’s not possible to run a successful pipeline system.

Each region can only support so many pipelines as well. When coupled with the relatively flat demand growth in refined products, this has resulted in a fairly consolidated market with few opportunities for new entrants to pursue.

Magellan boasts the longest refined products pipeline system in the country and accesses nearly 50% of U.S. refining capacity, making it an especially attractive partner for its customers.

Additionally, there are few substitutes for pipelines thanks to their cost-efficiency and safety, as well as geographical constraints (oil and gas formations tend to be in hard-to-access areas). Most of the products moved by Magellan’s pipelines are also non-discretionary in nature, resulting in predictable demand patterns.

Besides its tollbooth-like business model, Magellan has taken steps to improve its risk profile over time. For example, the firm bought out its general partner in 2009, making it one of the first midstream MLPs to eliminate eliminate incentive distribution rights, or IDRs.

IDRs give the general partner (the manager and sponsor of the MLP) an increasing percentage of marginal distributable cash flow (DCF), up to 50% once the distribution climbs high enough. As a result, IDRs increase an MLP's cost of capital and make it more difficult for firms to find profitable enough growth projects.

Magellan was also one of the first MLPs to adopt a self-funding business model. Other than its equity-based buyout of its IDRs in 2010, Magellan has financed its growth entirely with retained cash flow and modest amounts of debt.

In other words, the firm's growth plans are detached from the unpredictable volatility of the stock market since Magellan does not need to issue equity.

Management is committed to maintaining one of the safest balance sheets in the industry as well, earning Magellan a BBB+ investment grade credit rating from Standard & Poor's which is tied for the highest rating in midstream energy. This helps the firm maintain access to dependable, low-cost debt capital.

As Magellan's COO Aaron Milford explained at an investor conference in June 2019, unlike many of its MLP peers which are under pressure to restructure, Magellan has always taken a conservative approach with its business model:

"We've always tried to run our business with maximum flexibility and resilience in terms of how we capitalize our business to make sure it has many options at all times to fund our business.

So we didn't get into sort of the treadmill of equity issuances and get into the issue of getting high leverage and sort of getting in that position where everything has to work perfectly all the time in order for you to run a disciplined business.

So we've always had a natural aversion to sort of that condition. So that wasn't something we created. That's just what we chose and how we chose to run our business."

Combined with an annual distribution coverage target of above 1.2x (i.e. a payout ratio no higher than about 83%), Magellan should have no trouble continuing to increase its distribution while also funding its growth projects.

Looking ahead, demand for gas, diesel, and jet fuel isn't increasing much in America. Magellan's long-term growth is expected to be driven by the firm's continued expansion into marine storage and oil pipelines, which have grown from next to nothing in 2009 to about 40% of Magellan's operating margin today.

More of the firm's incremental growth will come from serving America's booming shale oil production, especially in the Permian Basin, where roughly a third of total U.S. oil production is generated, according to Time and the U.S. Department of Energy.

U.S. shale oil production is expected to continue growing through the late 2020s. When combined with about strong growth in U.S. natural gas production, the Interstate Natural Gas Association of America estimates that by 2035 the U.S. might need nearly $800 billion in new midstream infrastructure, with about half of that going to oil pipelines and export capacity.

However, despite these opportunities, Magellan faces several risks.

Key Risks

While Magellan's track record of delivering reliable income is excellent, its contract profile, which underpins the firm's relatively commodity-insensitive cash flow, could be stronger.

While many MLPs aim for long-term (10-plus years) and volume committed contracts, in 2018 only 40% of Magellan's refined products shipments were subject to payment, volume, or term commitments with customers, and only for an average remaining life of three years.

However, Magellan's advantages in that business (due to few alternatives, Magellan's service-oriented approach, and the firm's breadth of integrated infrastructure) mean that customers almost always renew their contracts.

The firm's crude oil pipelines also don't have strong contract coverage. In 2018, about 40% of shipments on its crude oil pipelines were subject to long-term agreements, with an average life of five years.

Therefore, a sustained decrease in demand for the petroleum and refined products in the markets served by Magellan could hurt the amount of volume its moves and stores and the rates it can charge when contracts are up for renewal.

For example, on the refined products side of the business, increased fuel efficiency and a shift to electric vehicles could weigh on long-term demand for transportation fuel. And in the crude pipeline business, a sustained decline in the price of oil or unfavorable price spreads in different market hubs could hurt pipeline utilization in the basins Magellan serves.

Some investors also worry that the world's growing push to reduce carbon emissions and embrace renewable energy will cause fossil fuel demand to peak within 20 years, sooner than many energy executives expect.

Meanwhile, in the short term, weak oil and gas prices due to the U.S. shale boom have significantly hurt the profitability of many fracking-focused energy producers. Shale companies are responding by cutting back on spending and taking actions to strengthen their fragile balance sheets.

These trends could weigh on U.S. oil and gas production, make it more difficult for energy producers to honor their contracts with midstream companies, and lead to excess pipeline capacity in some of Magellan's markets, putting downward pressure on rates.

Magellan's conservative approach to growth, strong balance sheet, and solid operational track record mitigate most of these concerns, but it's important that long-term demand trends for refined products and oil remain stable.

Finally, investors should note that Magellan Midstream Partners, as an MLP, issues K-1 tax forms instead of 1099s. Owning the stock results in greater tax complexity, including potential headaches when held in tax-deferred accounts such as IRAs or 401(k)s.

Closing Thoughts on Magellan Midstream Partners

Magellan is arguably one of the best run and most conservative MLPs in America, with a disciplined management team, low financial leverage, predictable fee-based cash flow from stable refined products markets, and a relatively low cost of capital.

Combined with its commitment of paying safe and growing distributions, Magellan appears to be a quality choice for conservative income investors who are comfortable with the midstream energy industry's risk profile.