Thoughts on Apple's Recent Slump and Dividend Appeal

While the stock market, in general, has had a rough few months, many popular tech stocks have been hammered far harder.

That includes Apple (AAPL), which saw its share price decline by as much as 40% since hitting an all-time high in October 2018. Apple's fall included a 10% single-day drop on January 2, 2019, when the company shocked Wall Street with a surprise revenue guidance cut for its first quarter of fiscal 2019.

Let's take a look at why the market has turned so bearish on this beloved consumer tech giant and, more importantly, determine whether Apple's long-term thesis and dividend growth prospects appear to remain intact.

Why Apple's Shares Plunged in Recent Months

Apple's most recent stock price slide began in early November after it released earnings that initially appeared great but scared the market for two reasons.

While in the quarter ended September 29, 2018, the iPhone maker's revenue and EPS grew a very strong 20% and 41%, respectively, management's guidance for its important holiday quarter called for relatively anemic sales growth of 3% at the midpoint.

Management explained that was partially due to expected currency headwinds as well as slowing growth in key emerging markets such as Turkey, India, Brazil, and Russia.

Potentially more alarming to investors was that management declared that going forward it would no longer be breaking out individual unit volumes on its sales, including for the iPhone which represents close to 60% of the company's revenue.

“As demonstrated by our financial performance in recent years, the number of units sold in any 90-day period is not necessarily representative of the underlying strength of our business...if you look at our revenue during the last three years, if you look at our net income during the last three years, if you look at our stock price in the last three years, there is no correlation to the units sold in any given period.” - Luca Maestri, CFO

While the company's CFO tried to justify the decision in a logical manner, many investors and analysts took this as an admission that Apple expects future iPhone volume growth to be flat, or potentially even negative.

In recent weeks, guidance cuts by various smartphone suppliers caused many analysts to lower their iPhone sales estimates on speculation that slowing global growth and America's escalating trade hostilities which China (about 20% of company sales) might cause Apple's sales and earnings to miss its disappointing initial guidance.

Those fears were confirmed on January 2, 2019, when Apple dropped a bombshell that rocked Wall Street and sent the tech sector into a one-day meltdown. In a letter to investors, CEO Tim Cook cut Apple's revenue guidance for its holiday quarter from a previous forecast of 3% growth to an expectation for a 5% decline.

"While we anticipated some challenges in key emerging markets, we did not foresee the magnitude of the economic deceleration, particularly in Greater China. In fact...over 100 percent of our year-over-year worldwide revenue decline, occurred in Greater China across iPhone, Mac, and iPad.

China’s economy began to slow in the second half of 2018...We believe the economic environment in China has been further impacted by rising trade tensions with the United States.

As the climate of mounting uncertainty weighed on financial markets, the effects appeared to reach consumers as well, with traffic to our retail stores and our channel partners in China declining as the quarter progressed. And market data has shown that the contraction in Greater China’s smartphone market has been particularly sharp." - Tim Cook, CEO

Apple's surprise guidance cut caused a further wave of downgrades including from Goldman Sachs (GS) analyst Rod Hall. Mr. Hall now expects Apple's full-year 2019 revenue to shrink by 5% and EPS to contract 4%.

He also went even so far as to compare Apple to Nokia, implying the company might struggle to ever achieve even modest earnings and free cash flow growth again.

Mr. Hall explained that continued weakening of China's economy and no likely quick resolution to the trade dispute between Washington and Beijing means that Apple's full-year 2019 growth issues are unlikely to improve anytime soon.

So with analysts' growth fears seemingly now justified by the firm's disappointing guidance, does this mean that Apple's long-term thesis is broken?

Revisiting Apple's Dividend Growth Thesis

It's certainly true that the escalating trade war between the U.S. and China isn't helping that country's growth rate (now the slowest in 25 years). The most recent economic data out of China shows the country slowing faster than expected, and its manufacturing sector is now contracting at a modest rate as well.

However, it's important to remember that China's GDP growth rate in 2019 is expected to slow but remain above 6%. And the trade war that appears to be directly hurting Apple's sales in that country seems likely to end sometime this year.

In recent weeks not only did the U.S. and China agree to halt any further tariffs (a truce brokered at the G20 Summit on December 1, 2018), but China has actually shown a willingness to roll back some retaliatory tariffs (such as a 25% tariff reduction on U.S. cars).

Meanwhile, U.S. officials, including President Trump himself, have said that negotiations are going "very well" and steady progress to end the trade war is being made.

On January 7 and 8, high-level trade talks took place in Washington to further help clear the path to a full ending of trade hostilities between the two nations. Basically, while the trade war is, in fact, hurting Apple very badly, ultimately this event is likely to prove a temporary growth headwind that will end at some point.

In addition, it's worth noting that Apple's long-term strategy has long been to shift its growth drivers from selling more iPhones to instead focus more on high-margin services and other product categories.

Specifically, in 2016 Cook said that Apple wanted to monetize its large installed customer base to double the size of its service revenue from about $25 billion per year to $50 billion by 2020.

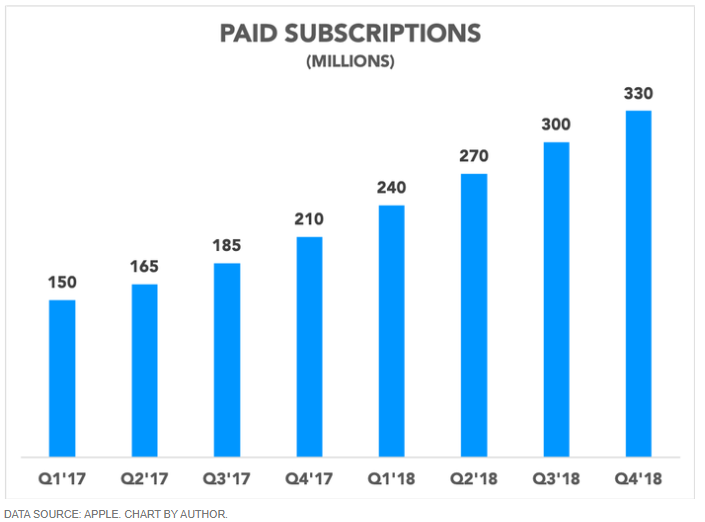

In recent years, Apple has taken meaningful strides towards that goal, converting much of its installed user base (now 1.4 billion devices per Cook's letter) into a rapidly growing subscriber base.

That has fueled close to 30% annual growth in service revenue, which analysts estimate has an operating margin north of 70% (above the company-wide operating margin of 27% last fiscal year).

According to Apple's revised guidance, service revenue during the holiday quarter came in at $10.8 billion, representing 28% growth and maintaining its long-term trend which puts the firm ahead of schedule for achieving its 2020 sales target of $50 billion.

Similarly, Apple continues breaking into new markets such as home speakers, premium headphones, and smartwatches, which has helped fuel its impressive growth in recent years. In the first fiscal quarter of 2019, wearables (AppleWatch and AirPods) grew nearly 50% year over year, and Apple continues to be the #1 smartwatch manufacturer in the world.

Overall, non-iPhone revenues grew 19% according to management, though Apple's continued high concentration of sales in iPhones will still result in a year-over-year decline in quarterly revenue.

However, thanks to the company's plans to get its net cash position (currently $130 billion) to zero over time, Apple's massive buybacks mean that the firm still expects to report record earnings for its holiday quarter.

Now it's certainly true that global smartphone upgrade cycles are lengthening, which is why overall worldwide smartphone sales are no longer expected to be very strong. In fact, market research firm IDC estimates that between 2017 and 2022 smartphone units will grow from just 1.5 billion to 1.7 billion (about 3% annual growth).

But while the potential addressable market for iPhones is no longer growing strongly, Apple's long-term thesis hasn't necessarily been based on continued booming iPhone sales revenues, but rather in its ability to monetize its very sticky ecosystem, created by the best customer loyalty in the industry.

For example, 70% of iPhone users won't even consider switching to another phone according to according to analyst firm Fluent. And per 451 Research, Apple's customer satisfaction for iPhones is the highest in the industry at 98%, which is why 80% of iPhone users plan to eventually replace their current iPhone with another one.

Apple's recent slide in China may suggest that globally its brand is losing some of its sway, but it's too soon to say. A quarter or two does not make a long-term trend. However, it brings to mind the main risk we noted in our January 2018 thesis:

Apple will remain largely dependent on hardware sales for the foreseeable future. Dividend investors considering the company should remain aware that the company's long-term growth prospects could come into question if the economics of the iPhone were to unexpectedly breakdown. For now, this seems unlikely thanks to the company's incredible brand strength, customer intimacy, and excellent balance sheet, which provides greater flexibility for Apple to adapt as needed.

Despite the scary guidance revision that has caused so much investor panic and analyst downgrades, ultimately the Wall Street consensus is that Apple's earnings (and thus dividend) growth rate should remain solid in fiscal 2020 and 2021, increasing around 12% per year.

While such long-term estimates must always be taken with a grain of salt, dividend investors can likely still expect double-digit payout hikes from the company. Apple's payout ratio remains low (projected at 24% over the next year), its balance sheet is in excellent health, and the business continues generating great cash flow. Tim Cook also confirmed in 2016 that Apple plans to raise its dividend every year.

With Apple's non-iPhone-based growth strategy appearing to remain on track, and the company now having enough net cash to repurchase about 20% of its shares in the coming years (actually more given its substantial free cash flow generated each quarter), fears that Apple will never grow again seem likely overblown.

Comparisons to Nokia (or Blackberry) are similarly unwarranted because neither of those companies was ever able to successfully establish or monetize its ecosystem as Apple has proven it can do.

Some investors may also wonder if Apple is the next IBM, another iconic tech company invested in by Warren Buffett's Berkshire Hathaway that saw its future turn bleaker. That comparison also seems unjustified given the unique cultural issues and shifting technological landscape IBM battled (more on that here).

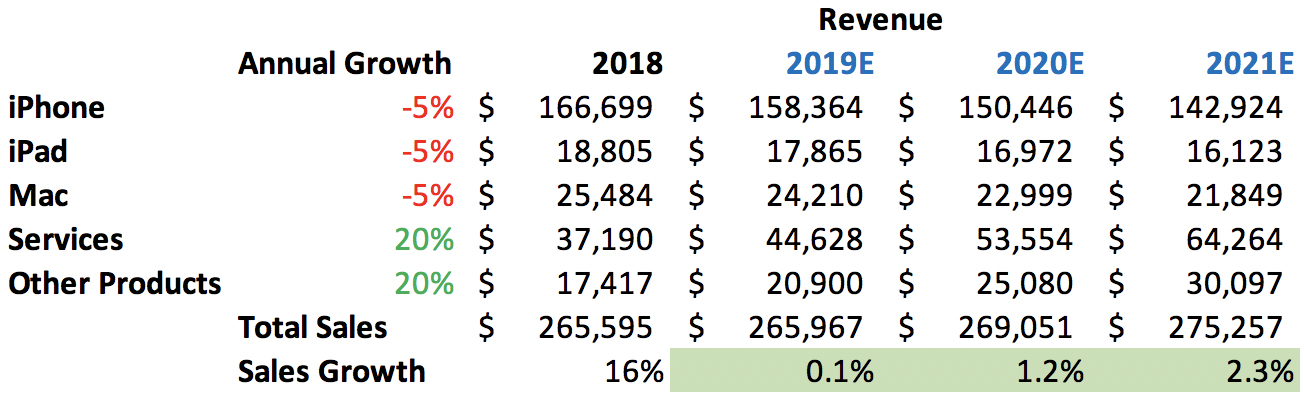

Even if Apple's iPhone, iPad, and Mac sales decline by 5% per year, so long as the company's high-margin Services and Other Products (AirPods, Apple TV, Apple Watch, Beats products, HomePod, iPod touch, etc.) continue their strong growth rates as management expects, the company's top line can continue edging higher.

Of course, the growth of Apple's services business is somewhat dependent on the number of devices it has in circulation. However, it seems unlikely Apple's base of hardware customers will meaningfully erode, plus the higher profitability of services should help support the company's long-term cash flow growth even if overall sales trends are less impressive.

Source: Simply Safe Dividends, Apple 10-K

Concluding Thoughts

Apple's surprise guidance cut may have understandably scared investors who have long worried that the company's best growth days are permanently behind it. And while it's almost certainly true that Apple will never return to triple-digit earnings growth again like it enjoyed during the early smartphone adoption phase, it's important to remember two things.

First, Apple's long-term dividend growth thesis is not based on continued blockbuster iPhone sales growth (stabilization to moderate expansion is most important). Rather, the company will depend on its sticky ecosystem of devices and services, a large and still growing installed device base, and continued growth of recurring subscription revenues.

Second, while the company's negative growth in China in the first quarter of fiscal 2019 (and possibly for most of this year) is a major short-term growth headwind, it's likely a temporary one that will improve once the U.S. and China end their trade war.

Ultimately, Apple's ability to deliver double-digit dividend growth for the foreseeable future appears to remain intact. However, the company's long-term growth rate may be more moderate than investors had hoped for given Apple's size and its lingering dependence on the saturated smartphone market.

But at today's valuation (forward P/E ratio below 13), Apple looks like a reasonable long-term dividend growth stock to consider as part of a well-diversified portfolio.