Energy Transfer LP Offers High Yield But Self-Dealing Management

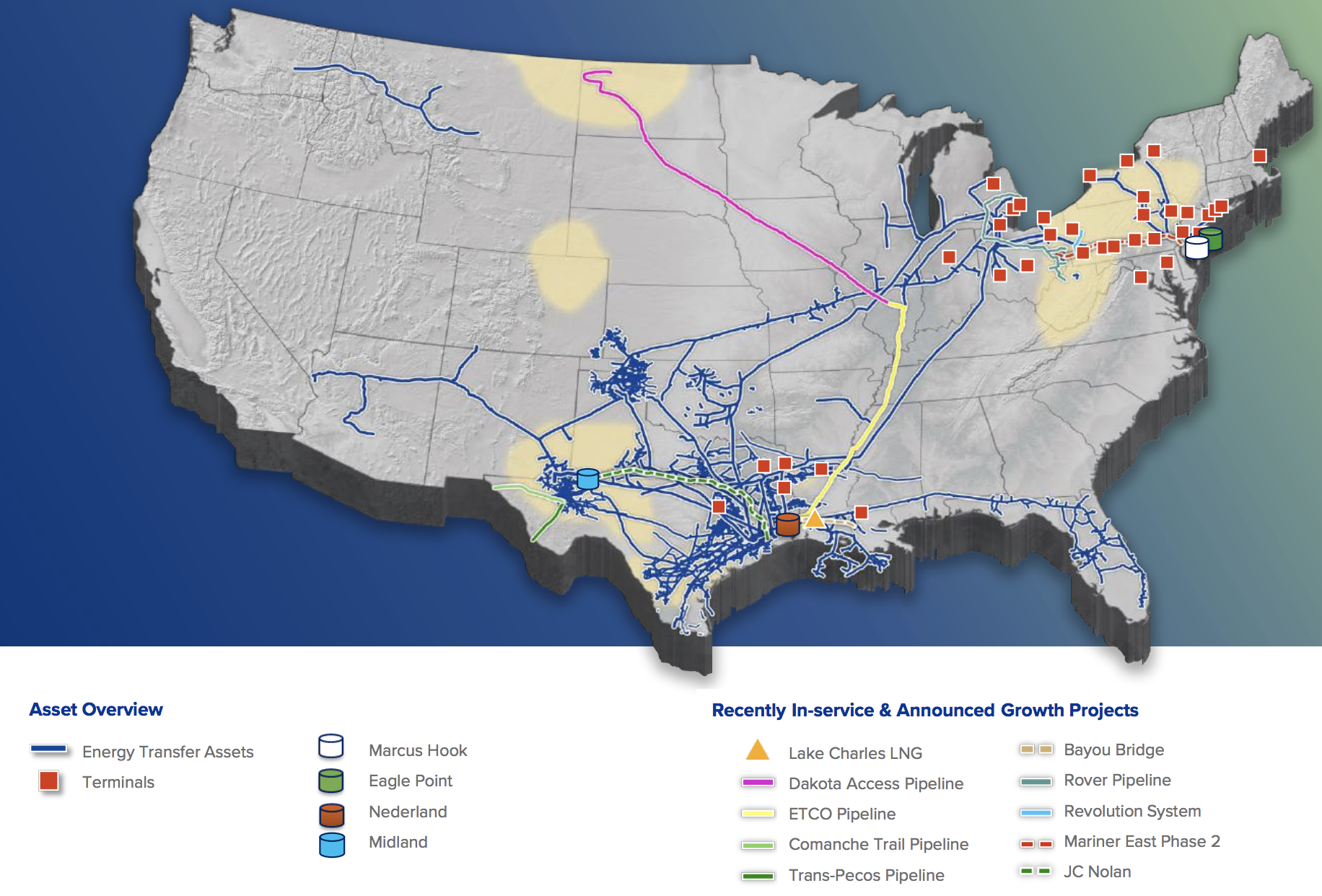

Energy Transfer LP (ET) began in 1996 as a small natural gas pipeline operator in Texas and has grown to become one of the largest providers of midstream energy services in the nation.

With a footprint in most of the major domestic production basins, the firm's pipelines, storage facilities, and terminals help move various fossil fuels from production sites to end users.

Source: Energy Transfer Investor Presentation

Energy Transfer's services include crude oil transportation and terminalling (25% of EBITDA); natural gas transportation and storage (24%); processing, storing, and transporting natural gas liquids and refined products (24%); and natural gas gathering and processing (15%).

Approximately 90% of the firm's EBITDA is generated from fee-based activities, reducing its sensitivity to commodity price fluctuations.

With over 85,000 miles of energy infrastructure nationwide, Energy Transfer's business enjoys several competitive advantages.

First, many of its assets are hard to replicate. Major projects often cost billions of dollars to complete, with a single mile of new pipeline costing over $7 million per mile to build in recent years. Meanwhile, various regulators have to sign off on new construction.

Most projects don't get approved unless there is an obvious need for additional takeaway capacity to address bottlenecks and price disparities between energy production hubs, creating relatively little overlap of pipeline systems.

As a result, new pipelines generally don't move forward unless contracts covering most of their capacity are already in place, reducing risk. Those contracts tend to be long-term, fixed-rate, and often include take-or-pay volume commitments.

Additionally, few substitutes exist for pipelines due to geographical constraints (oil and gas formations tend to be in hard-to-access areas) and their superior cost-efficiency and safety profile compared to alternatives such as rail and truck.

In a way, the midstream industry is similar to the utility sector in that it provides an essential service for energy markets and benefits from an oftentimes regulated, tollbooth-like business model, resulting in a stable cash flow stream.

Energy Transfer's scale makes it an especially important player in this industry. Approximately 30% of America's natural gas and crude oil is moved on the firm's pipelines. The nation's energy industry couldn't function without Energy Transfer's assets.

Energy Transfer also boasts the largest intrastate natural gas pipeline and storage system on the Gulf Coast (key market for refining, petrochemicals, and exports), has a strategic footprint in practically all of the major domestic production basins, and can move energy to market hubs across the Midwest, Gulf Coast, and Canada.

Thanks to its size, geographic reach, and asset diversification (no single segment contributes more than 30% of EBITDA), Energy Transfer is an especially attractive (if not essential) partner for most of its customers.

Despite these durable qualities, Energy Transfer ran its business too aggressively prior to the 2014-16 oil crash. The firm relied heavily on debt and equity markets to fund its major growth projects, maintained a highly levered balance sheet, had weak cash flow coverage for its distribution, and encountered several costly project delays.

In 2018, Energy Transfer (at the time named Energy Transfer Equity) executed a simplification transaction to improve its balance sheet, eliminate its costly incentive distribution rights, and provide better coverage of its distribution. This kept Energy Transfer Equity's distribution intact but resulted in effective distribution cuts for its sponsored MLPs (more on that later).

Importantly, the deal reduced Energy Transfer's cost of capital and shifted its business to a self-funding model. Rather than fund organic growth via equity issuances, which depend on fickle unit prices, Energy Transfer now funds its backlog with retained cash flow and modest amounts of debt.

With a healthy long-term distribution coverage ratio target of 1.7x to 1.9x and a reasonable leverage target of 4.0x to 4.5x to maintain its BBB- investment-grade credit rating from Standard & Poor's, Energy Transfer is in much better financial shape going forward.

Management has also moderated the firm's growth spending, further reducing risk. The partnership targets about $3 billion to $4 billion of annual growth capex. For context, Energy Transfer has over $90 billion in assets and an annual run rate of about $8 billion in distributable cash flow ($4 billion to $5 billion leftover after paying distributions).

In other words, the firm is not overly dependent on any single project, and it is generating a healthy amount of cash flow after distributions to help fund its growth and maintain an investment-grade balance sheet.

Despite Energy Transfer's improved risk profile, investors still have several concerns.

Key Risks

ET's stock has historically traded at a price-to-discounted cash flow multiple (P/DCF) that's about half as high as the multiples enjoyed by fellow investment-grade MLPs such as Enterprise Products Partners L.P. (EPD) and Magellan Midstream Partners, L.P. (MMP).

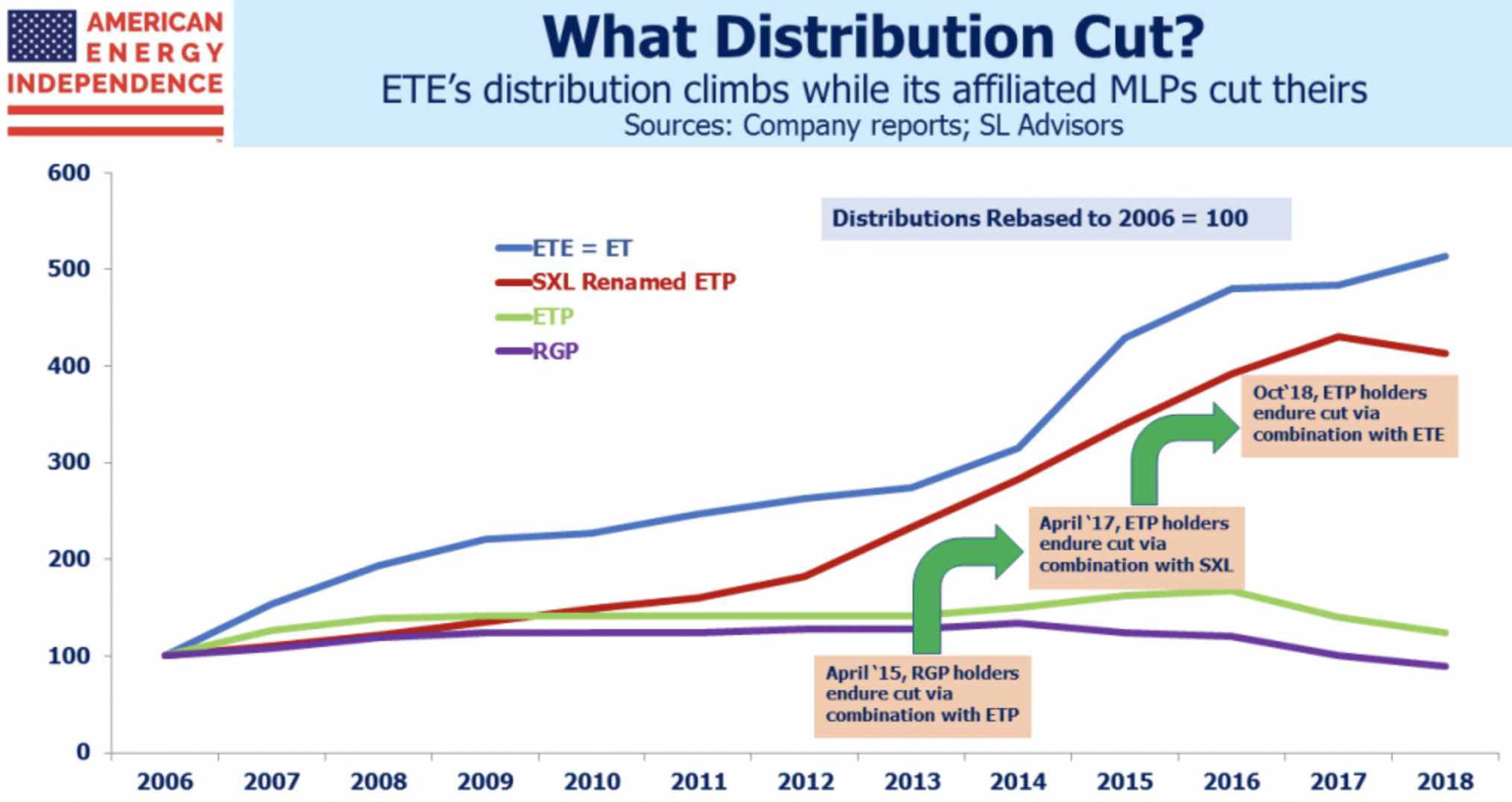

Energy Transfer's discount is driven by investors' lack of trust in the firm's management. SL Advisors, an asset manager specializing in midstream energy infrastructure, provided a nice summary of management's past shenanigans.

For example, in the last five years Energy Transfer imposed "stealth distribution cuts" across its affiliated MLPs while simplifying its business model and dealing with several project delays.

Management, led by Texas billionaire CEO Kelcy Warren, is most aligned with Energy Transfer Equity, which became Energy Transfer in 2018. As you can see, ET is the only partnership which has maintained steady or rising distributions.

Source: SL Advisors

Management's worst self-dealing behaviors were on display following ET's attempted $48 billion buyout of the Williams Companies (WMB) in 2015.

With oil prices falling lower, raising the risk profile of the deal and threatening Energy Transfer's credit rating, the firm's board wanted to retract its previous offer, which management felt was now too high.

After negotiations with the Williams Companies for a lower valuation failed, Energy Transfer decided to issue convertible preferred units to try and kill the deal. These securities were only issued to Warren, certain board members, and others whom Warren picked to be recipients.

As SL Advisors explained, these convertible preferred units diluted the subsequent value of ETE units, effectively lowering the cash-and-units offer the firm had made to the Williams Companies. Meanwhile, Warren and the firm's insiders were protected against any dilution and given preferential treatment to distributions, leaving common unitholders to bear the risk.

After the deal with the Williams Companies was canceled, Energy Transfer still chose to keep management's convertible preferreds outstanding. This sent a clear message to common unitholders that Warren is most interested in looking out for himself and the management team first.

Energy Transfer's annual report even states that the company's general partner, which is majority owned by Kelcy Warren, has reduced its fiduciary duties:

“Our general partner has limited its liability and reduced its fiduciary duties under the terms of our partnership agreement, while also restricting the remedies available for actions that, without these limitations, might constitute breaches of fiduciary duty.”

Unfortunately, this dynamic is unlikely to change. Energy Transfer's partnership agreement has a provision providing that any units held by a person who owns 20% or more of units then outstanding cannot be voted on any matter.

With ET's directors and executive officers owning 14% of units, it would therefore be very difficult for the general partner (which is run by ET's management team) to be removed without their consent. The stock is also unlikely to ever garner takeover interest.

Governance concerns seem like the most reasonable explanation for Energy Transfer's high yield and "cheap" valuation. As the MLP space continues evolving, what's to say another opportunity (a large acquisition, merger, etc.) won't come along where the common unitholders are left with the short end of the stick?

Aside from management, it's worth noting that Energy Transfer targets a higher amount of leverage compared to its investment-grade rated peers and has faced more execution issues (project delays, higher construction costs, environmental regulation violations, fines, etc.) with some of its major pipeline projects.

While these issues could suppress Energy Transfer's pace of distribution growth the next few years, they seem unlikely to threaten the distribution's safety given ET's diversified asset base, self-funding growth model, and solid payout ratio.

Finally, while midstream cash flows are relatively insensitive to commodity prices, the industry's long-term growth potential is dependent on favorable long-term energy prices.

Management teams are grappling with a wide range of potential outcomes here. For example, the International Energy Agency maintains several long-term forecasts which predict oil demand peaking as soon as 2020, or as late as 2040.

If oil and gas prices remain at low levels due to weak demand and elevated supply, then drilling activity would likely slow as shale producers come under even more pressure. This would reduce the need for new pipelines and other energy infrastructure, sapping the midstream industry's growth outlook.

Closing Thoughts on Energy Transfer

Energy Transfer's diversification across nearly all of the major U.S. producing basins, substantial customer base, self-funding growth model, high distribution coverage ratio target, and dependence on fee-based businesses, which generate about 90% of its cash flow, all lower its fundamental risk profile.

However, investors considering the stock have to be comfortable with management's potential for self-dealing in the future and believe that the stock's higher yield and cheaper multiple are worthy tradeoffs.

Conservative income investors interested in this industry might want to look at more proven midstream MLPs such as Magellan Midstream Partners and Enterprise Products Partners, whose management teams are better aligned with unitholders' interest and have demonstrated superior capital allocation track records.