Founded in 1997, Kinder Morgan (KMI) is one of North America's largest midstream infrastructure companies, providing gathering, storage, transport, and processing services to the oil & gas industry.

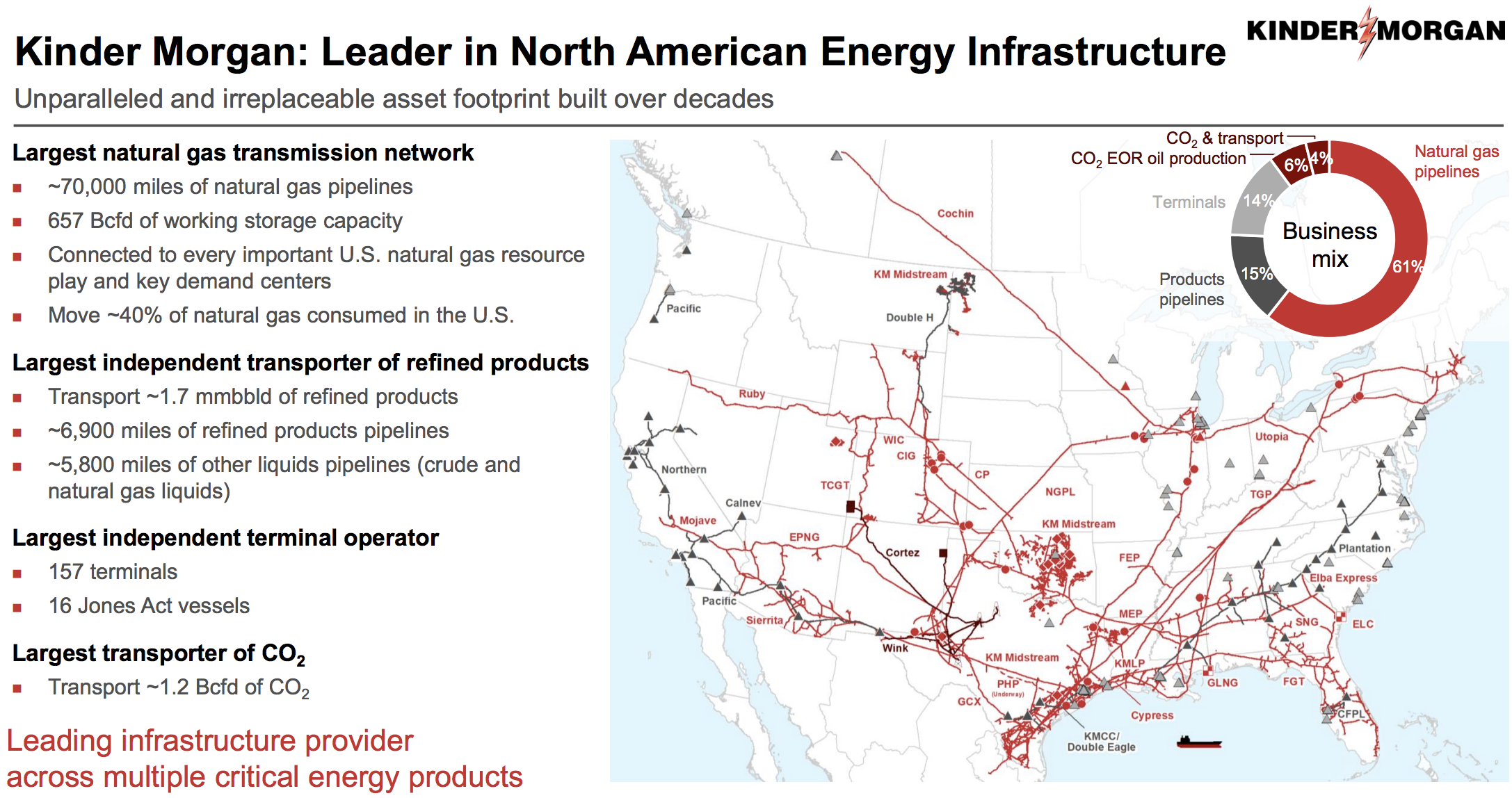

As you can see, Kinder Morgan's pipelines, storage facilities, and terminals are integrated into almost all parts of the domestic oil & gas industry, including every major gas and oil shale formation and export markets along the Gulf Coast.

Source: Kinder Morgan Investor Presentation

Natural gas pipelines generate 61% of Kinder Morgan's EBITDA, followed by products pipelines (15% – transports refined products and oil), terminals (14% – oil and petroleum product storage network) and CO2 (10% – carbon dioxide used for enhanced oil recovery and also transported).

About 66% of Kinder Morgan's cash flow is generated under fee-based, take-or-pay contracts for periods of up to 20-plus years. Another 25% of cash flow is fee-based, and 5% is hedged. In other words, Kinder Morgan has minimal direct exposure to commodity prices.

However, Kinder Morgan's dividend record is marred by a 75% cut in late 2015. (The firm had a Very UnsafeDividend Safety Score prior to its cut announcement.)

The payout reduction was made necessary by the firm's high leverage and dependence on issuing equity to fund its aggressive growth. As access to equity financing became restricted during the oil crash, Kinder Morgan needed to cut its dividend to protect its credit rating while it continued its expansion plans.

The company has since implemented a self-funding business model (eliminating its need to issue equity) and reduced its leverage in order to pay a much more sustainable dividend going forward.

Business Analysis

Operators in the midstream industry often enjoy meaningful competitive advantages for several reasons.

First, the industry is highly regulated at the state, local, and federal levels. In addition, it's very costly (in recent years a single mile of new pipeline cost over $7 million per mile to build) and time-consuming (an average of several years) to receive approval for and build new pipeline projects.

Only so many pipelines are needed within a particular geographic area as well, often resulting in a consolidated market. Due to limited competition, the Federal Energy Regulatory Commission oversees the rates charged by Kinder Morgan's interstate products and natural gas pipelines to ensure they are fair.

Pipelines also have few substitutes given their safety and cost-efficiency, along with geographical constraints (many oil & gas formations are in hard-to-access areas) that can make rail and truck transportation difficult.

Income investors most appreciate the fact that midstream infrastructure often operates like a toll road, where service providers receive fees for use of their pipes, storage facilities, and terminals. For example, around 90% of Kinder Morgan's cash flow is fee-based or from take-or-pay contracts.

This creates a relatively commodity price-insensitive and stable stream of cash flow from which to pay meaningful dividends.

Kinder Morgan's infrastructure is particularly valuable to the energy industry. Approximately 40% of the natural gas consumed in America travels on Kinder Morgan's pipelines for at least part of its journey from supply to end-use market, demonstrating the high dependence its customers have on the firm's assets.

With the largest natural gas network in the country, the firm is connected to all the major basins and market hubs. Natural gas production in these key supply basins is expected to grow significantly over the next decade as cheaper and cleaner gas replaces coal power and is exported to higher-cost international markets, providing Kinder Morgan with continued expansion opportunities.

Source: Kinder Morgan Investor Presentation

Kinder Morgan is also the largest independent transporter of refined products (15% of EBITDA) and the largest independent terminal operator (14% of EBITDA). The firm's scale in these markets once again makes it an essential partner for many energy producers and end users.

While this story may sound similar to the one peddled by management prior to the firm's 2015 dividend cut, today's Kinder Morgan is on much stronger ground.

The company has significantly reduced its financial leverage, improved its investment-grade credit rating from Standard & Poor's by one notch to BBB, moved to a conservative self-funding business model, and become more disciplined with its growth ambitions.

In fact, Kinder Morgan's growth capital backlog topped $18 billion at the end of 2014 but sits at about $4 billion today (and is not overly dependent on the success of any single project, most of which are focused on natural gas).

Management expects to invest $2 billion to $3 billion per year in expansion opportunities going forward, representing approximately 2% to 5% annual growth in the company's asset base.

Importantly, the firm's distributable cash flow (~$5 billion annually) now comfortably covers the dividend (~$2 billion) and nearly all of Kinder Morgan's discretionary spending, eliminating its need to access equity markets.

Overall, Kinder Morgan is in a fundamentally healthier position compared to several years ago. However, the industry still faces several risks.

Key Risks

Like most other midstream companies, Kinder Morgan faces risk from project cost overruns and delays. Fortunately, the firm's backlog is now focused on smaller, less costly, and less risky energy infrastructure projects.

While this is a positive for the firm's risk profile, a lack of major expansion projects also means that Kinder Morgan's cash flow and dividend growth rate will slow in the future, likely to a low- to mid-single digit pace.

Management has committed to a 25% dividend increase in 2020, but income investors should not extrapolate this type of payout growth going forward.

Additionally, it's worth noting that about 25% of Kinder Morgan's cash flow is not backed by minimum volume provisions, and its CO2 business (10% of EBITDA) is sensitive to oil prices and production volumes.

This isn't a problem if the U.S. energy renaissance continues and production rises over the coming decades as management expects. However, no one knows what the global energy landscape will look like a decade from now as the world pushes to reduce carbon emissions and embrace renewable energy.

For example, the International Energy Agency maintains several long-term forecasts which predict oil demand peaking as soon as 2020, or as late as 2040.

Meanwhile, in the short term, weak oil and gas prices due to the U.S. shale boom have significantly hurt the profitability of many fracking-focused energy producers. Shale companies are responding by cutting back on spending and taking actions to strengthen their fragile balance sheets.

These trends could weigh on U.S. oil and gas production, make it more difficult for energy producers to honor their contracts with midstream companies, and lead to excess pipeline capacity in some of Kinder Morgan's markets.

Fortunately, 77% of the firm's revenue is from customers with investment-grade credit ratings or substantial credit support, and nearly 70% of revenue comes from end-users of the products Kinder Morgan handles (rather than energy producers).

Overall, the company's improved balance sheet, higher retained cash flow, and more conservative growth ambitions help mitigate many of these concerns.

However, the evolution of energy should continue to be monitored given its potential to reduce the long-term need for new energy infrastructure, which would sap the midstream industry's growth outlook.

Closing Thoughts on Kinder Morgan

Kinder Morgan has come a long ways since its infamous 2015 dividend cut. The firm's balance sheet is in better shape, the dividend is nicely covered by cash flow, capital spending is more disciplined, and growth is largely self-funded.

The company's operations also remain diversified with a focus on critical natural gas infrastructure, and the vast majority of its cash flow is backed by take-or-pay contracts or fee-based earnings.

While the firm's smaller backlog means Kinder Morgan's dividend will likely grow at only a low- to mid-single digit pace after an expected 25% bump in 2020, the stock could still be a potentially decent income option to consider for investors who are comfortable with the midstream industry's risk profile.