Dividend Payout Ratio: How to Calculate and Apply It

The dividend payout ratio reports the percentage of a company's profits that are paid out as a dividend to shareholders.

A company’s dividend payout ratio can indicate how safe a dividend payment is and how much room there is for management to grow the dividend. Lower payout ratios are better.

Gaining an understanding of the dividend payout ratio can help income investors make better decisions, avoid riskier dividend stocks, and improve the quality of their portfolios.

How to Calculate a Dividend Payout Ratio

Follow three steps to calculate a company's dividend payout ratio:

Calculate Annual Dividends per Share

Calculate Annual Earnings per Share

Divide Annual Dividends per Share by Annual Earnings per Share

Dividend Payout Ratio Example

Let's apply this dividend payout ratio formula to calculate Coca-Cola's (KO) 2021 payout ratio.

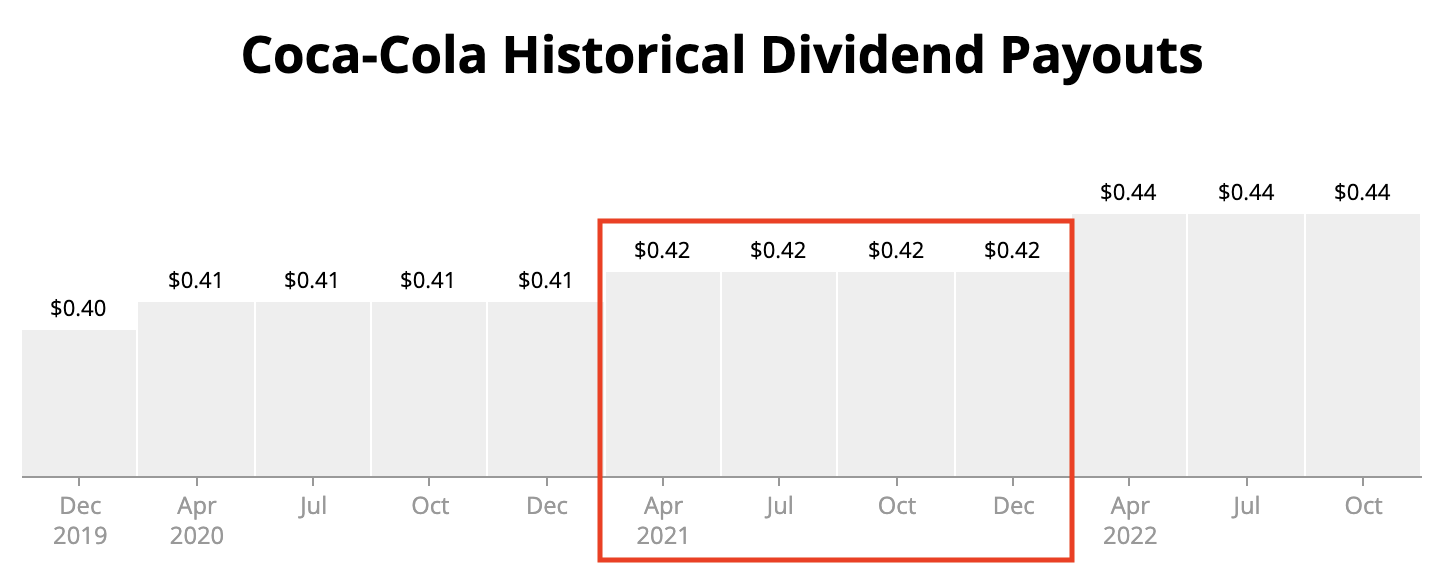

In 2021, Coca-Cola (KO) paid four quarterly dividends of 42 cents per share. Summing these dividends results in 2021 annual dividends per share of $1.68.

Source: Simply Safe Dividends

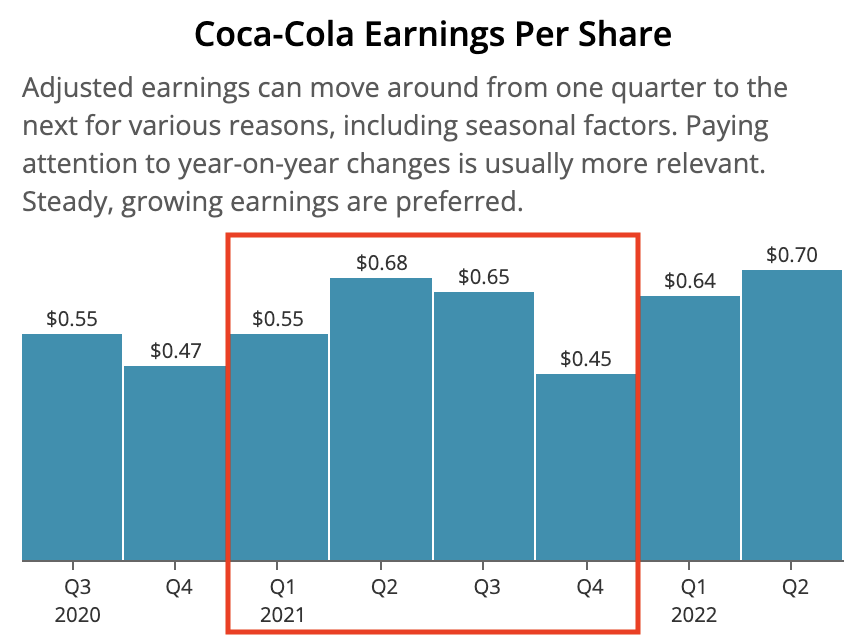

Now we need to calculate Coca-Cola's earnings per share over the same period.

The company's four quarterly reports have a combined earnings per share figure of $2.33 (55 cents in Q1 + 68 cents in Q2 + 65 cents in Q3 + 45 cents in Q4).

Source: Simply Safe Dividends

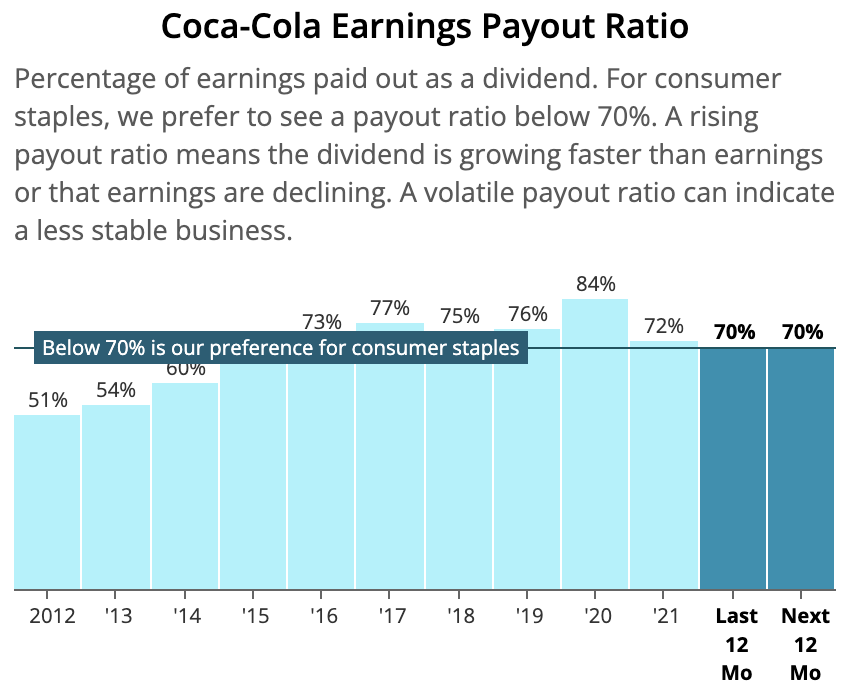

Dividing Coca-Cola's 2021 dividend per share ($1.68) by the firm's 2021 earnings per share ($2.33) calculates a dividend payout ratio of 72%.

This payout ratio means that for every $1 of profits generated by Coke, the company paid out 72 cents as a dividend.

The remaining 28 cents of earnings was retained for other uses, such as share repurchases, debt reduction, and acquisitions.

More Than One Payout Ratio Formula Exists

There are different ways to calculate the dividend payout ratio. The various methodologies differ in how they measure a company’s profits and the time period that is used.

You might wonder how profits can differ from one payout ratio formula to the next. Earnings are earnings, right? Not exactly…

Many companies report two different earnings figures each period. One set of earnings follows the Securities and Exchange Commission’s requirement that publicly traded companies adhere to Generally Accepted Accounting Principles (GAAP) for their financial reports.

Some companies choose to also present non-GAAP financial results. Non-GAAP results are usually reported to adjust out “one-time” events such as restructuring charges and non-cash impairments.

When applicable, companies report non-GAAP figures in an effort to give investors a more representative look at their actual operations by excluding accounting “noise”.

There is much debate over using GAAP or non-GAAP figures. In most cases, we believe non-GAAP results provide a better look at the actual business.

Besides GAAP and non-GAAP earnings, some investors like to analyze a company’s free cash flow payout ratio. Unlike earnings, which are impacted by non-cash accounting charges, free cash flow measures actual cash generated by a business each period.

For this reason, free cash flow can give a more realistic look at a company’s dividend payout ratio. After all, free cash flow is the lifeblood of a company. Without it, a business cannot sustainably pay a dividend.

They rely instead on industry-specific metrics like adjusted funds from operations (AFFO) and distributable cash flow (DCF) to calculate their dividend coverage.

These measures are similar to free cash flow but have several major differences, such as excluding a firm's growth capital expenditures.

Source: Simply Safe Dividends

The final major difference in how the dividend payout ratio can be calculated is the time period over which it is measured.

Some investors will use forward earnings estimates for a company, which are based on analysts’ projections of how much profit a firm will generate over the next year.

Others calculate the payout ratio based on the company’s results that have already been reported over the last 12 months, a single quarter, or a firm's most recent fiscal year.

Our website, Simply Safe Dividends, uses adjusted earnings and displays a company's historical payout ratios, as well as its projected payout ratio over the next year.

This makes it easy to see if a company's financial flexibility is increasing, decreasing, or staying about the same compared to history.

We also show our preferred payout ratio level for different types of firms to stay below.

Source: Simply Safe Dividends

What Is a Good Dividend Payout Ratio?

A payout ratio of 100% means that a company's dividend has consumed all of its earnings, leaving no flexibility to reinvest more in the business or keep the dividend covered if profits dip.

While this represents a bad payout ratio in most cases, what constitutes a "good" payout ratio depends on the type of business.

Most dividend-paying stocks have a payout ratio between 30% and 60%.

Stable, mature sectors such as telecom, utilities, and consumer staples maintain some of the highest payout ratios, usually between 50% and 75%.

This doesn’t mean these companies have riskier dividends, though. In fact, these are some of the best sectors for income because of their steady cash flows.

On the other side of the spectrum, the technology sector has one of the lowest payout ratios.

Technology businesses are generally characterized by a faster pace of change and reinvest more for growth to remain relevant and increase profits. As a result, they often pay out less than half of their earnings as a dividend.

Outside of extreme cases, whether a payout ratio is good or bad depends on the stability of a company's business model and a number of other factors, such as a firm's balance sheet strength, future capital spending needs, and reinvestment opportunities.

Generally speaking, we prefer to invest in dividend stocks with a payout ratio below 60%. Lower payout ratios provide more cushion for the dividend and make it easier for dividend growth to continue, even if earnings hit a temporary rough patch.

Go Beyond Dividend Payout Ratios to Assess Dividend Safety

Payout ratios are only one factor that investors should analyze before deciding to buy or sell a dividend stock, especially if the primary intent is to generate safe income in retirement.

The dividend payout ratio represents a snapshot in time. Unfortunately, business conditions can change quickly, and each business model handles change differently.

Some companies enjoy few fixed costs and sell recession-resistant products, lessening their exposure to the economy. But many businesses are tied closely to economic growth and are severely impacted by expansions and contractions.

Depending on the current macro environment and type of business being evaluated, the dividend payout ratio can be a misleading indicator of dividend safety.

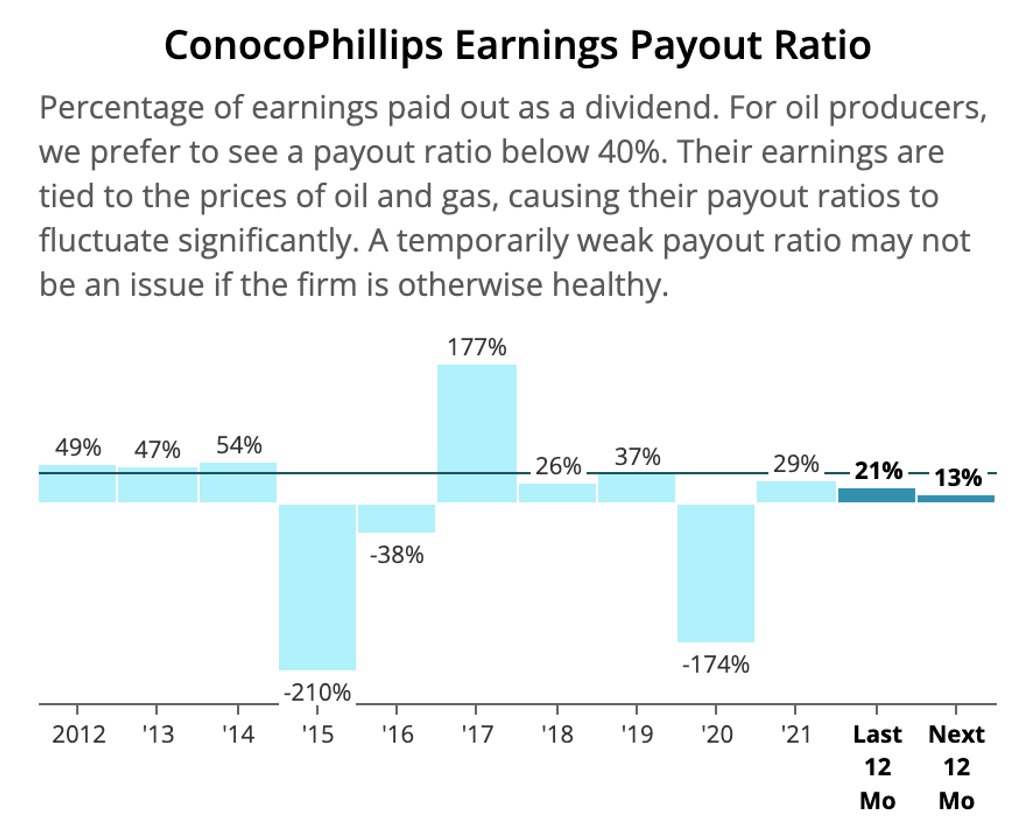

Let’s take an example. Suppose you were looking at ConocoPhillips (COP) in 2014.

You would have seen a company with a payout ratio consistently below 60% and more than 25 consecutive years of uninterrupted dividends, providing a sense of comfort.

Source: Simply Safe Dividends

Then, the price of oil crashed.

ConocoPhillips, an oil and gas exploration and production company, began burning through cash (i.e. a negative payout ratio) in 2015 and was forced to cut its dividend in early 2016.

Source: Simply Safe Dividends

ConocoPhillips is one example of why investors should look at a company’s dividend payout ratio over time to gauge its historical volatility and long-term trend.

Companies with safer dividends will typically be characterized by a smoother payout ratio with no major spikes.

ConocoPhillips also highlights the importance of understanding some of the other major risk factors impacting a company’s ability to pay its dividend.

Some of the big ones we pay attention to are the consistency of a company’s cash flow, how much debt is on the balance sheet, the firm's performance during recessions, and recent business trends.

Analyzing these factors takes a lot of work and monitoring, which is why we created our Dividend Safety Score™ system to save investors time and help them make better investment decisions.

Dividend Payout Ratio vs. Dividend Yield

By now, it should be clear that the dividend payout ratio is an entirely different metric than dividend yield.

Both metrics use a company's dividend, but their calculations are distinct:

Dividend Payout Ratio: Dividend divided by Earnings

Dividend Yield: Dividend divided by Stock Price

Investors can use payout ratios to gauge the safety of a dividend (higher levels are riskier), while dividend yield can help determine when to buy a stock and how much dividend income an investor will receive (higher dividend yields mean every dollar invested earns more income).

Closing Thoughts on Dividend Payout Ratios

Calculating dividend payout ratios can help size up the safety and growth prospects of a company’s dividend payment.

We generally prefer to invest in companies with payout ratios below 60%, but we are willing to go higher if the business is relatively stable (e.g. a regulated utility company).

Importantly, the dividend payout ratio is just one piece of the puzzle when it comes to assessing a company’s quality.

Factors such as debt and cash flow stability are also useful measures of dividend risk. They should all be analyzed together and over long enough periods of time to assess whether a company's dividend appears safe.