Is Altria Still a Dependable High-Yield Dividend Growth Stock?

Over the past half century tobacco giant Altria (MO) has not only been a dependable source of safe and fast growing dividends, but it's also been one of the best performing stocks in the market.

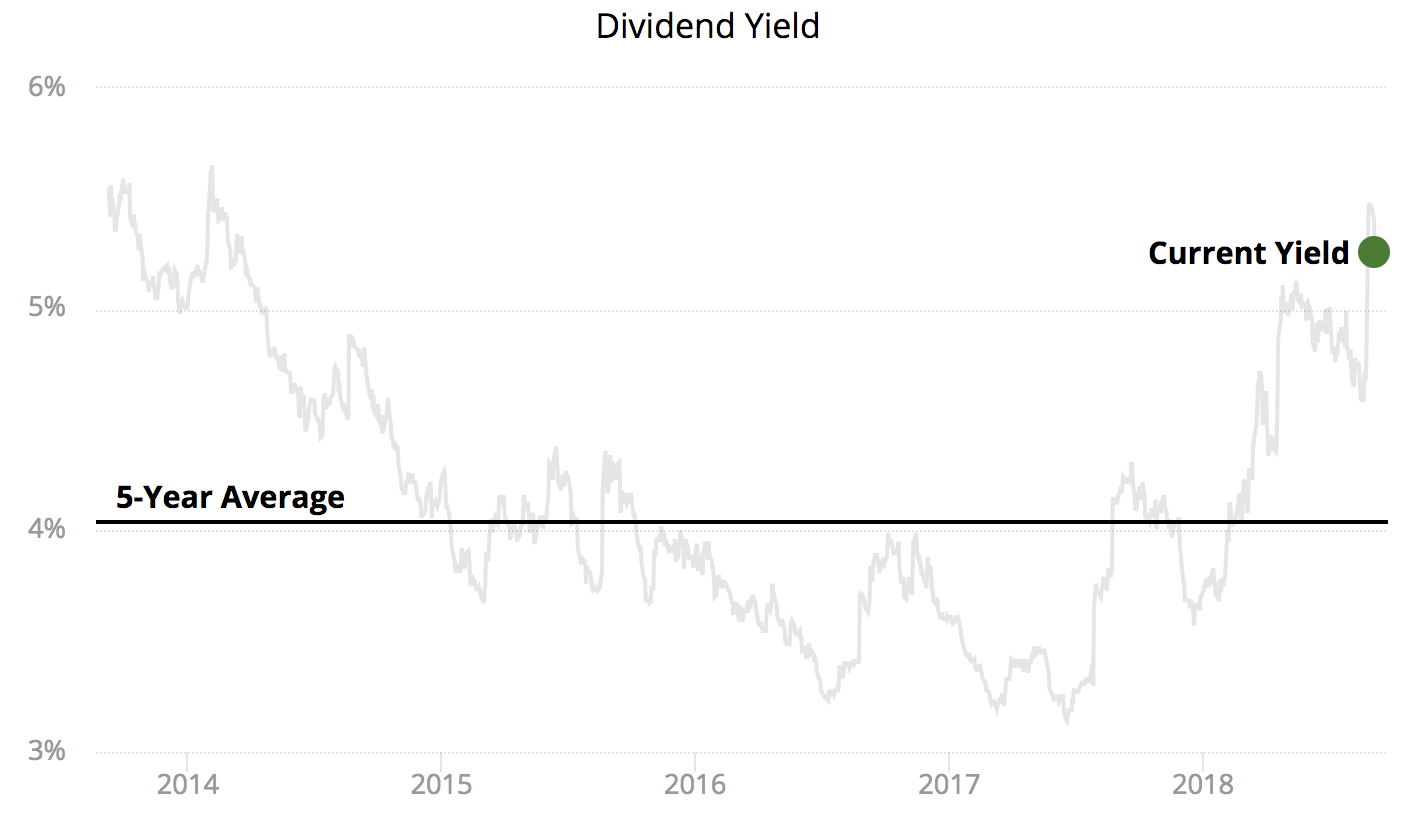

However, in 2018 MO's stock has slumped 15%, pushing its dividend yield to its highest level since 2014. As traditional cigarettes continue their secular decline and more alternative products enter the market, some investors are worried about Altria's long-term outlook and the safety of its dividend.

Source: Simply Safe Dividends

Let's take a closer look at the main reasons why Wall Street has turned sour on this future dividend king (49 consecutive years of dividend hikes) to determine if Altria still represents a reasonable long-term dividend growth investment.

Why Wall Street is Bearish on Altria

After spinning off Kraft (KHC) and Philip Morris International (PM) in 2008, Altria became a pure-play U.S.-focused tobacco company. Today 85% of its sales come from cigarettes.

However, U.S. smoking rates and thus cigarette volumes have been declining for over 50 years, and the industry is expected to record 3% to 4% annual volume declines for the foreseeable future.

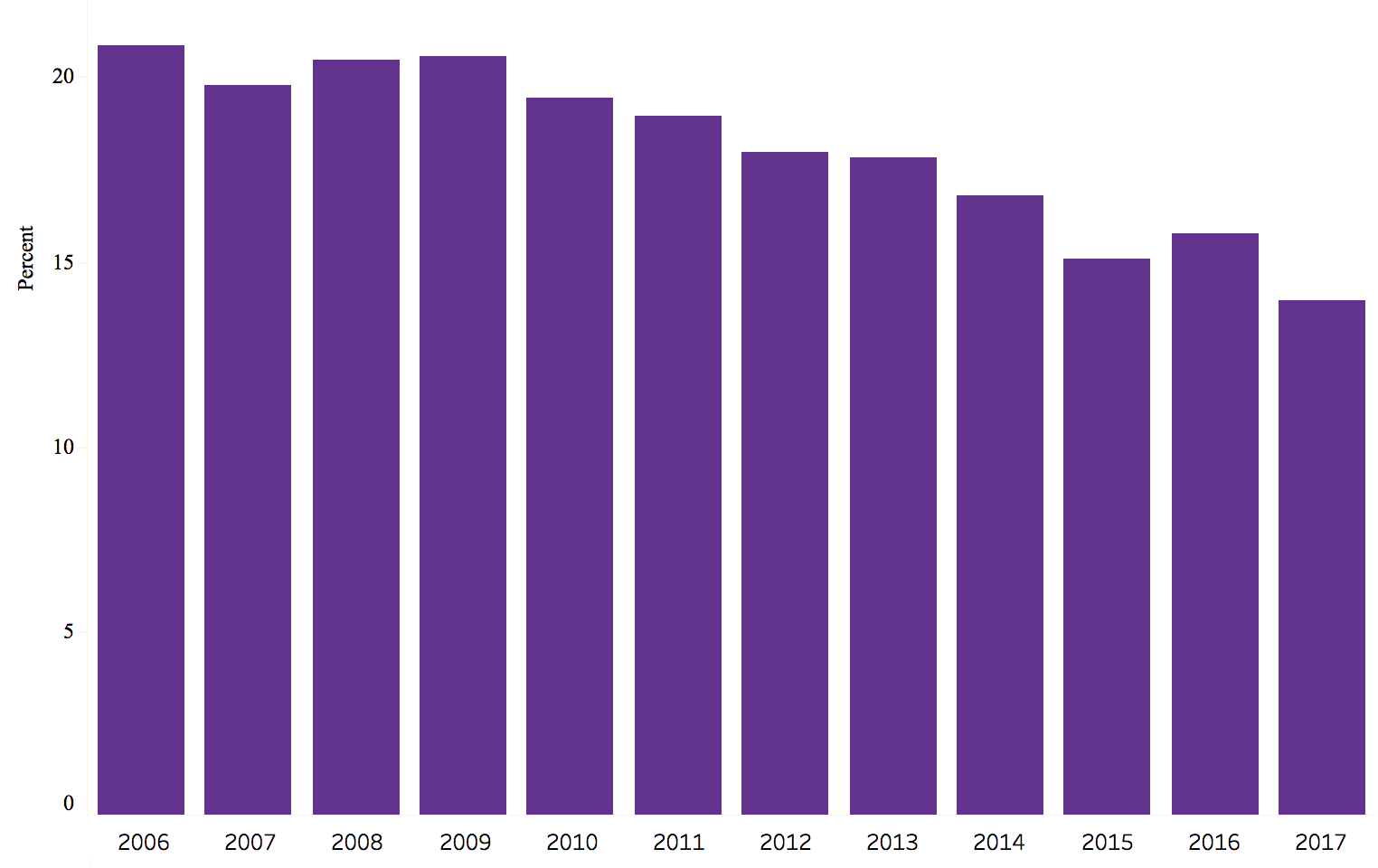

According to the Centers for Disease Control and Prevention’s (CDC) National Center for Health Statistics, adult smoking rates in 2017 hit an all-time low of 14%, down from about 16% in 2016, 20% in 2006, and more than 40% in 1965.

High school smoking rates fell to just 9%, also an all-time low. That puts U.S. smoking rates on track to meet the CDC's 2020 goal of a 12% adult smoking rate. The chart below plots the prevalence of current cigarette smoking among U.S. adults aged 18 and over.

Source: National Center for Health Statistics

Fortunately for Altria, the company's strong collection of brands (most notably Marlboro) means that it enjoys a dominant market share (about 40% in U.S. cigarettes) and excellent pricing power which it flexes to offset volume declines.

For example, historically the company has raised its cigarette prices 4% to 5% annually, while retaining market share and thus driving modest revenue growth.

However, in its most recent quarter Altria's core cigarette business saw a surprising decline in volumes of 11%. Even after adjusting for trade inventory levels the volume decline was 5%, steeper than the company has seen in recent years and worse than the industry's decline of 3.5%. As a result, Altria's company-wide net revenue contracted 3.6%.

The volume decline was largely the result of excise tax increases in Kentucky and Oklahoma and increased pricing pressure from major rivals who are offering promotions to try to gain market share. Such price wars tend to be brief in this oligopolistic industry, meaning that Altria's results seem likely to improve going forward. However, there are some long-term risks facing the company.

One of Altria's big growth plans is to offset declining cigarette volumes with reduced-risk products (RRPs). These include vaping products (which contain no tobacco) as well as "heat sticks" like IQOS, which was developed by Philip Morris.

Altria has exclusive rights to market IQOS in the U.S. and has been trying to get the product approved by the FDA for sale in the U.S. as a "reduced risk" product since it merely heats tobacco but doesn't create any toxic smoke. Altria has stated that it has the "aspiration of being the U.S. leader in authorized, non-combustible, reduced-risk products."

However, in February the FDA dealt Altria's reduced-risk product plans a blow. Despite an FDA study conducted by the National Academies of Sciences, Engineering, and Medicine that found that vaping products (e-cigarettes) were lower risk than traditional tobacco products, it concluded they couldn't be called "safe".

Just days later an FDA advisory panel unanimously declared that IQOS had not proven itself sufficiently superior to cigarettes to be labeled a "reduced risk" product. Altria can eventually still be granted approval to market IQOS in the U.S., but it will not be be able to sell it as a "safer" product.

Then, just a month later the FDA announced plans to create a regulatory roadmap to reduce nicotine levels in cigarettes to "non addictive levels".

According to a recent National Institutes of Health Study, reducing nicotine levels in cigarettes from 10-15 mg to 15 mg to 0.5 mg would achieve this goal. The FDA believes that by achieving these low nicotine levels it might be able to reduce the U.S. adult smoking rate from 14% today to less than 2% eventually.

The ultimate regulations are likely to take several years to develop and even longer to fully phase in. But such nicotine regulations arguably represent one of the biggest long-term risks to Altria's business model since the major tobacco lawsuits of the 1990s.

That's one reason why Altria plans to invest so heavily in less harmful produces like vaping and IQOS, which the FDA says it plans to encourage despite recent regulatory rulings have been less than friendly.

What about the fast-growing U.S. vaping market which Wells Fargo estimates was $5.1 billion in size at the end of 2017 and is expected to grow at about 15% annually for the next decade?

Unfortunately, there are two problems Altria is facing here. First, the U.S. cigarette market is about $80 billion per year. Even if vaping achieves the strong growth rates analysts expect, it may never become a large enough market for Altria to offset declines in cigarette volumes and revenues, should the FDA succeed in driving smoking rates into the low single-digits.

The second problem for Altria is that while it's a powerhouse in cigarette brands, that hasn't translated to its vaping products thus far. For example, according to Nielsen, here's how the $5 billion U.S. vaping market stacked up at the end of 2017:

JUUL: 46.8% share, up from 25% in 2016

Vuze (RJ Reynolds): 20.7%, down from 24.3% in 2016

MarkTen (Altria): 11.4%

Logic (Japan Tobacco): 7%

blue eCigs (ITG Brands): 4.4%

Analysts now think that JUUL has about 50% market share, which is roughly five times that of Altria's MarkTen vaping product line. Altria has been investing in vaping for five years, but JUUL came out of nowhere in 2016 to grab a larger market share in vaping than Altria even enjoys in cigarettes.

This highlights the challenges that the company faces in convincing its loyal cigarette users to switch to its brand of smokeless nicotine delivery systems which are clearly different than the traditional cigarette experience.

So with Altria facing so many uncertainties about its long-term growth profile, is it no longer a good high-yield dividend growth stock? Actually no. Despite its challenges, Altria is likely to remain a source of safe and growing dividends for the foreseeable future.

Altria'sDividend is Still Safe and Likely to Grow Over Time

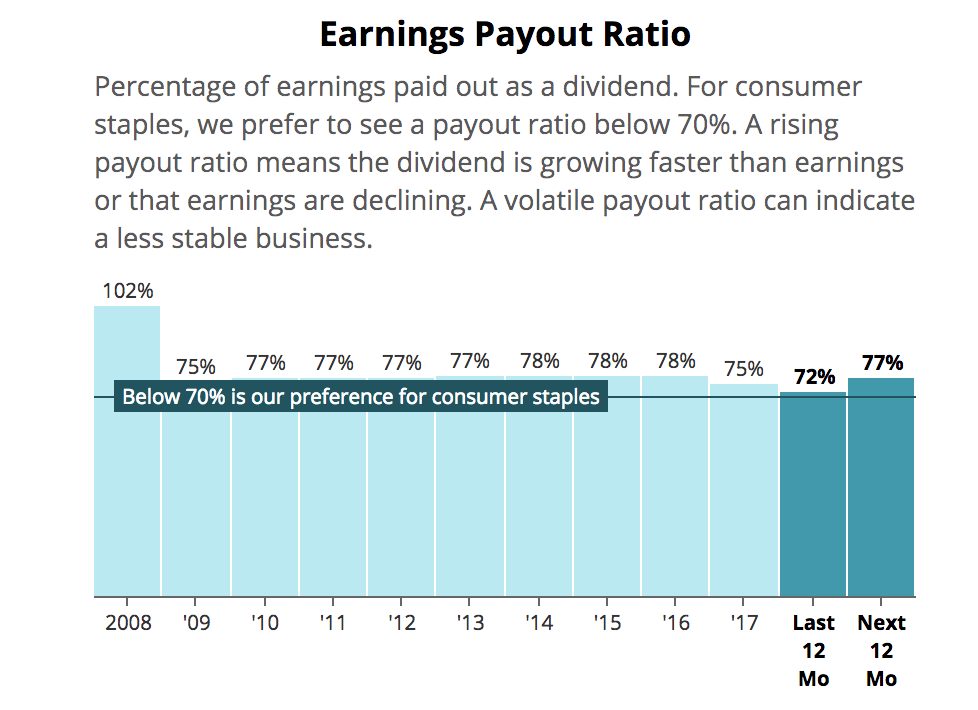

First, let's address the fears that Altria's dividend is no longer safe. Two of the most important factors to focus on are the payout ratio and the balance sheet.

Altria has a stated policy of paying dividends equivalent to 80% of adjusted EPS. As you can see, Altria's business remains comfortable within management's target. The firm also expects tax cuts to help drive 16% to 19% adjusted EPS growth this year.

As a result, despite some of the longer-term uncertainties facing the business, management was confident enough this year to announce two dividend hikes totaling 24%.

Source: Simply Safe Dividends

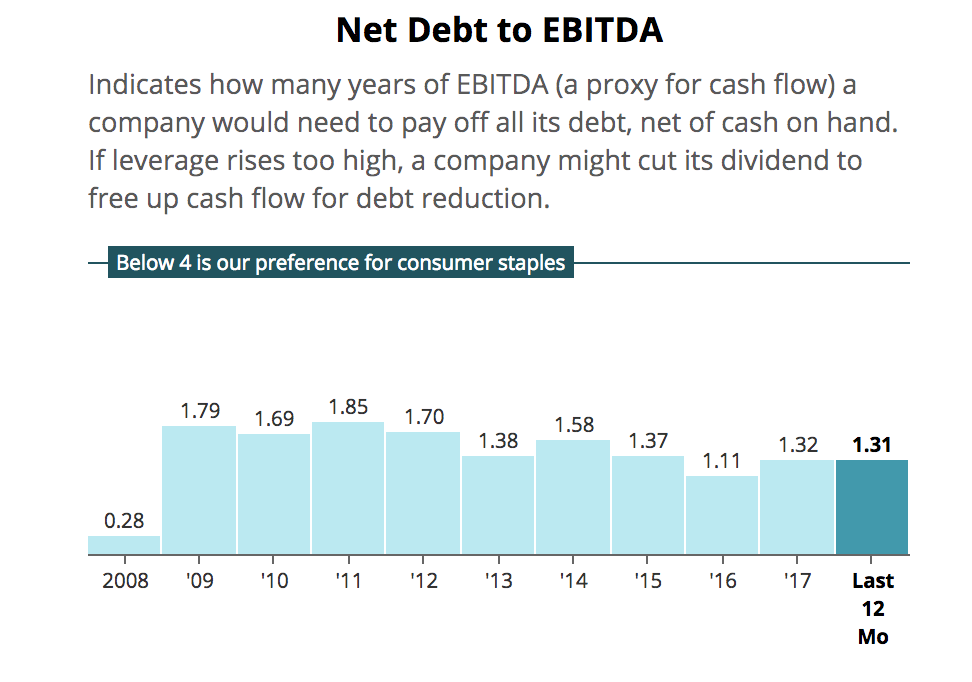

Meanwhile, Altria's net debt to EBITDA (leverage) ratio is 1.3, about industry average and somewhat below the firm's long-term levels. As a result of its reasonable debt levels and consistent cash flow generation, the company enjoys a strong A- credit rating.

Source: Simply Safe Dividends

From a financial perspective, the bottom line is that Altria's dividend is safe. The company has reasonable flexibility to continue honoring its dividend while still investing in products of the future.

But how what about Altria's long-term dividend growth prospects in the face of so many challenges and the evolving competitive landscape?

One major way Altria plans to keep growing its earnings is through cost cutting. The company is currently pursuing a $2 billion cost savings initiative (for perspective, Altria's revenue sits at $19.4 billion) that it believes will raise its operating margin from 40% to about 45% in the coming years.

Meanwhile, the company expects that once the current discounting war in the U.S. is over (likely by end of this year or early 2019) it will be able to continue its historically solid price increases to offset cigarette volume losses and continue driving modest revenue growth.

Finally, there's hope that reduced-risk products like IQOS should be approved to launch in the U.S. relatively soon. Altria believes it can achieve far better market share in heat sticks than it has so far in vaping.

That's because according to Martin King, CFO of Philip Morris which has been developing IQOS, heat sticks are superior to vaping products:

"It has higher conversion rates than e-cigs. The taste is closer, and the delivery of nicotine and the satisfaction of smokers is much closer to cigarettes."

In 38 countries around the world Philip Morris has found that IQOS brand loyalty is nearly identical to that of regular cigarettes with just 1% of customers switching to competing products.

That's probably because heat sticks are marketed under name brands like Marlboro, as opposed to vaping products (Altria's MarkTen) which are largely unknown to smokers. Vaping products can also be sold online, reducing some of the retail distribution advantages Altria has enjoyed.

Therefore, a key factor to monitor over the coming years is whether vaping or heat sticks win over more cigarette defector. The tobacco giants are obviously hoping for the latter to continue benefiting from the brand equity they've developed over many decades.

The rise of vaping products and heat sticks also cloud the outlook for profitability. As they battle for market share, Altria and Philip Morris are investing heavily to develop and market these products, some of which are unprofitable today, and there is plenty of regulatory uncertainty with how they will be taxed over the long term.

For now, management remains confident that ongoing cost cutting and modest share buybacks will continue driving adjusted EPS (and dividend) growth of 7% to 9% per year.

Closing Thoughts on Altria's Dividend and Outlook

It's not hard to see why Wall Street has been so bearish on Altria this year. The FDA has handed down several negative rulings that potentially jeopardize its long-term earning power and dividend growth plans.

However, it's important to remember that tobacco companies in general, and Altria in particular, have managed to generate excellent dividend growth and total returns over the past 50 years. That's despite a near constant onslaught of regulatory and legal risks, as well as a secular decline in U.S. smoking rates that has been going on since the 1960s.

Is this time different? There's always a chance. However, the transition from cigarettes to alternative products will likely play out over the course of many years, if not decades. Altria should remain a cash cow during this time, especially as it continues taking costs out of the business.

Meanwhile, it's far from certain that Altria will struggle to amass a strong market share position in vaping and heat-not-burn products over the long term. Thanks to its core cigarette business, the company still has immense financial resources and excellent distribution compared to its rivals.

Altria needs to keep investing as it adapts to evolving industry conditions, but the market's "shoot first, ask questions later" reaction has certainly lowered expectations for the stock, which sports a yield north of 5% and a forward P/E ratio below 15, a discount to the broader market's.

For income investors who are comfortable investing in the tobacco industry and understand the risks Altria is facing, the stock appears to remain a reasonable holding as part of a well-diversified portfolio. You just have to acknowledge that the company's range of possible long-term outcomes has widened somewhat, adding uncertainty to the story until more is known about the evolving cigarette alternatives market.